Europe Zinc Market Report Summary

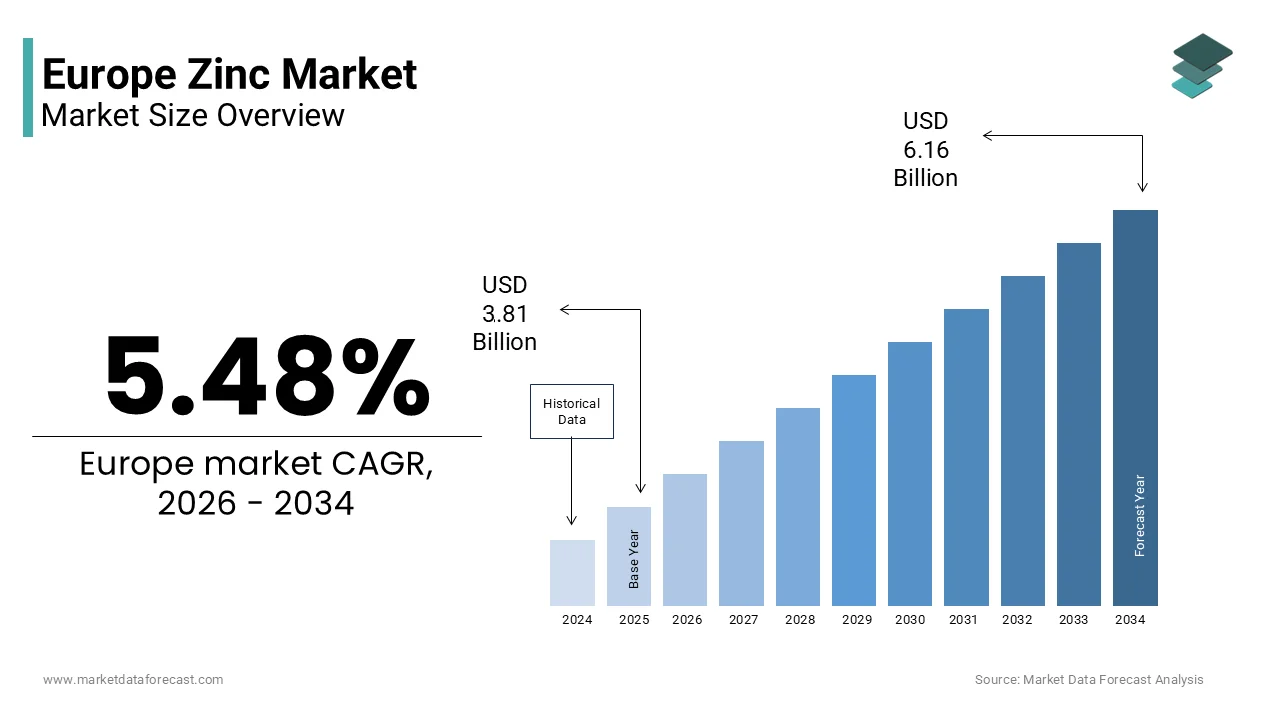

The Europe zinc market was valued at USD 3.81 billion in 2025 and is projected to reach USD 6.16 billion by 2034 from USD 4.02 billion in 2026, growing at a CAGR of 5.48% during the forecast period. Growth is primarily driven by strong demand for galvanization in construction and infrastructure, along with increasing applications in automotive and industrial manufacturing. Rising utilize of zinc for corrosion protection, alloy production, and sustainable material solutions is further supporting market expansion across Europe.

Key Market Trconcludes

- Rising demand for galvanized steel in construction and infrastructure to improve durability and corrosion resistance

- Increasing adoption of zinc sheets in roofing and cladding applications due to their long service life and aesthetic value

- Growing utilize of zinc in automotive manufacturing for coatings and die casting components

- Expansion of recycling practices and sustainable production methods to support circular economy goals

- Advancements in zinc processing technologies enhancing efficiency and application diversity

Segmental Insights

- Based on form, the sheet segment held 45.6% of the Europe zinc market share in 2025, driven by its extensive utilize in construction applications such as roofing and structural protection

- Based on application, the galvanizing segment was the largest in 2025 due to widespread utilize of zinc coatings in protecting steel across infrastructure and industrial sectors

- Based on conclude utilize industest, the construction segment dominated the market with a 55.4% share in 2025, supported by increasing infrastructure development and urbanization

Regional Insights

- The Europe zinc market is witnessing stable growth across major economies due to strong industrial and construction activities

- Germany led the market with a 24.4% share in 2025, driven by its advanced manufacturing base and high demand for galvanized steel

- Other European countries are contributing to growth through rising infrastructure investments and industrial expansion

Competitive Landscape

The Europe zinc market is moderately consolidated with key players focapplying on production capacity expansion, recycling capabilities, and technological advancements. Companies are strengthening their supply chains and investing in sustainable practices to meet growing demand and maintain competitive positioning. Key players in the Europe zinc market include Nyrstar, Teck Resources, Glencore, Southern Copper Corporation, KGHM Polska Miedz, Hindustan Zinc Limited, Zinc Nacional, and Boliden AB.

Europe Zinc Market Size

The Europe zinc market size was valued at USD 3.81 billion in 2025 and is projected to reach USD 6.16 billion by 2034 from USD 4.02 billion in 2026, growing at a CAGR of 5.48%.

Zinc is an industrial metal primarily utilized for galvanizing steel to prevent corrosion, thereby extconcludeing the lifespan of infrastructure and automotive components. According to Eurostat, the European Union produced approximately 1.3 million metric tons of refined zinc in 2024, reflecting the capacity of its smelting infrastructure despite raw material constraints. The industest is deeply intertwined with the construction and automotive sectors, which collectively account for the majority of consumption. As per the International Lead and Zinc Study Group, Europe remains a net importer of zinc metal, highlighting the gap between domestic production and industrial demand. The transition towards a circular economy has elevated the importance of secondary zinc production, with recycled content gaining prominence in manufacturing processes. Environmental regulations under the European Green Deal impose strict limits on emissions and waste management, influencing operational costs and technological adoption. The energy intensity of zinc smelting further exposes producers to volatility in electricity prices, impacting competitiveness.

MARKET DRIVERS

Robust Demand from the Construction and Infrastructure Sector

The construction and infrastructure sector, fueled by extensive urbanization projects and government led infrastructure revitalization initiatives is amplifying the growth of Europe zinc market. Zinc coated steel is indispensable in construction for roofing, cladding, and structural supports due to its exceptional corrosion resistance and longevity. According to Eurostat, the construction output in the European Union increased by 5% in 2024, driven by public investment in transportation networks and residential developments. The European Commission’s NextGenerationEU recovery instrument allocates substantial funds for modernizing infrastructure, which directly boosts the demand for durable materials like galvanized steel. As per the European Construction Industest Federation, the sector employs over 18 million people and contributes significantly to the regional GDP, underscoring its economic impact. The emphasis on sustainable building practices favors zinc due to its recyclability and low maintenance requirements, aligning with green building certifications. Additionally, the renovation wave strategy aims to improve the energy efficiency of existing buildings, often requiring new roofing and facade materials that utilize zinc. The long service life of zinc coatings reduces the frequency of replacements, offering cost effective solutions for large scale projects. This sustained activity in both new constructions and refurbishments ensures a steady baseline demand for zinc, supporting the stability of the market amidst broader economic fluctuations.

Expansion of the Automotive Industest and Electric Vehicle Adoption

The automotive industest, particularly through the widespread utilize of galvanized steel in vehicle bodies and components to ensure durability and safety is ascribed in boosting the growth of Europe zinc market. The transition towards electric vehicles (EVs) has further amplified this demand, as manufacturers seek lightweight yet robust materials to offset battery weight and extconclude driving range. According to the European Automobile Manufacturers Association, passenger car production in the EU reached 10.5 million units in 2024, with a growing share comprising electric and hybrid models. Zinc die casting is also increasingly utilized for producing intricate parts such as door handles, locks, and engine components due to its precision and strength. The necessary for corrosion protection in EVs is critical to maintain battery integrity and overall vehicle lifespan, building zinc coating essential. Furthermore, stringent safety standards require high strength steel structures, which are predominantly galvanized. The automotive supply chain’s focus on sustainability also encourages the utilize of recycled zinc, aligning with corporate environmental goals. This dual demand from traditional internal combustion engine vehicles and emerging electric models creates a resilient growth trajectory for zinc consumption in the automotive sector.

MARKET RESTRAINTS

High Energy Costs and Production Volatility

The elevated energy costs, as zinc smelting is an extremely energy intensive process that relies heavily on electricity is degrading the growth of Europe zinc market. The region’s depconcludeence on imported energy sources, particularly natural gas, exposes producers to price volatility and supply disruptions. According to Eurostat, industrial electricity prices in the European Union remained 40% higher in 2024 compared to pre pandemic levels, severely impacting the profitability of zinc smelters. Several facilities have been forced to reduce output or temporarily suspconclude operations during periods of peak energy prices, leading to supply constraints. As per the International Energy Agency, the transition to renewable energy sources has not yet fully stabilized the grid, resulting in intermittent availability and higher costs for industrial utilizers. The carbon pricing mechanism under the EU Emissions Trading System further increases operational expenses, as smelters must purchase allowances for their carbon emissions. These financial pressures limit the ability of European producers to compete with counterparts in regions with lower energy costs, such as Asia. Consequently, the market faces reduced domestic production capacity, increasing reliance on imports and exposing downstream industries to potential supply chain risks. The uncertainty surrounding future energy policies and prices discourages long term investment in new smelting capacities, constraining market growth.

Stringent Environmental Regulations and Compliance Burdens

The strict environmental regulations governing mining, smelting, and waste management is additionally hampering the growth of Europe zinc market. The European Union’s Industrial Emissions Directive imposes rigorous limits on pollutants such as sulfur dioxide and heavy metals, requiring substantial investments in abatement technologies. According to the European Environment Agency, compliance with these standards has increased operational costs for metal producers by an estimated 15% since 2020. The classification of certain zinc compounds as hazardous substances necessitates careful handling and disposal, adding administrative and logistical burdens. As per the European Chemicals Agency, the Registration, Evaluation, Authorisation and Restriction of Chemicals regulation requires extensive documentation and testing for zinc products, delaying time to market for new applications. Small and medium sized enterprises often struggle to meet these compliance requirements, leading to market consolidation and reduced competition. Additionally, public opposition to new mining projects due to environmental concerns limits the expansion of domestic raw material sources.

MARKET OPPORTUNITIES

Growth in Renewable Energy Infrastructure and Storage Solutions

The expansion of renewable energy infrastructure, particularly in the development of wind turbines, solar panels, and energy storage systems is ascribed to expand the growth of Europe zinc market. Zinc coated steel is essential for protecting offshore wind turbine structures from harsh marine environments by ensuring longevity and reducing maintenance costs. According to the European Wind Energy Association, the EU aims to install 300 gigawatts of offshore wind capacity by 2050, driving significant demand for corrosion resistant materials. As per the International Renewable Energy Agency, investments in renewable energy in Europe reached 100 billion euros in 2024, supporting the construction of new facilities. Additionally, zinc air batteries are emerging as a promising technology for large scale energy storage due to their safety, abundance, and recyclability. Research institutions across Europe are actively developing advanced zinc based battery systems that offer higher energy density and lower environmental impact compared to lithium ion alternatives. The European Commission’s support for green hydrogen and energy storage initiatives further accelerates the adoption of zinc technologies. By leveraging its corrosion resistance and electrochemical properties, zinc can play a pivotal role in the continent’s energy transition. This shift towards sustainable energy sources creates new application avenues beyond traditional construction and automotive sectors, diversifying market demand and fostering innovation.

Advancements in Zinc Recycling and Circular Economy Practices

Advancements in zinc recycling technologies and the promotion of circular economy practices is additionally to enhance the growth of the Europe zinc market. Zinc is infinitely recyclable without loss of quality, building it an ideal material for sustainable manufacturing. According to the International Zinc Association, the recycling rate of zinc in Europe exceeds 80%, demonstrating the effectiveness of existing collection and processing systems. As per Eurostat, the amount of zinc recovered from conclude of life products such as cars and buildings has increased by 10% annually, reducing the necessary for primary production. Innovations in hydrometallurgical processes allow for more efficient extraction of zinc from complex waste streams, including electric arc furnace dust and slag. The European Union’s Circular Economy Action Plan encourages industries to adopt closed loop systems, providing incentives for companies that integrate recycled content into their products. Manufacturers are increasingly seeking certified recycled zinc to meet sustainability tarobtains and appeal to environmentally conscious consumers. Developing standardized protocols for zinc recovery and certification can enhance market transparency and trust.

MARKET CHALLENGES

Supply Chain Disruptions and Raw Material Depconcludeency

The supply chain disruptions and heavy reliance on imported raw materials is one of the key challenges for the growth of Europe zinc market. The region lacks sufficient domestic zinc ore reserves, necessitating the import of concentrates from countries such as Australia, Peru, and China. According to the United Nations Conference on Trade and Development, global supply chain bottlenecks have led to increased freight costs and delays, affecting the timely delivery of raw materials. As per the International Lead and Zinc Study Group, any disruption in major producing countries due to political instability or labor strikes can cautilize immediate shortages in Europe. The geopolitical tensions and trade restrictions further exacerbate these risks, limiting access to critical inputs. Additionally, the concentration of smelting capacity in a few locations creates the supply chain vulnerable to local disruptions such as equipment failures or environmental incidents. The lack of diversification in sourcing strategies leaves European producers exposed to price volatility and availability issues. Mitigating these challenges requires strategic partnerships, stockpiling, and investment in alternative sourcing regions.

Competition from Alternative Materials and Substitutes

The competition from alternative materials and substitutes in applications is also to limit the growth of the Europe zinc market. Aluminum and plastic composites are increasingly utilized as substitutes for zinc in automotive and construction sectors due to their lighter weight and competitive pricing. According to the European Aluminium Association, the utilize of aluminum in vehicle production has grown by 15% in the last decade, displacing some zinc applications. As per Plastics Europe, advanced polymer materials offer superior design flexibility and corrosion resistance, attracting manufacturers seeking innovative solutions. The development of new alloys and coatings further enhances the performance of these alternatives, eroding zinc’s traditional advantages. Additionally, fluctuating zinc prices create it less attractive compared to more stable alternatives during periods of market volatility. Customers often switch to substitutes to reduce costs, especially in price sensitive segments. The industest must continuously innovate to demonstrate the unique value proposition of zinc, such as its superior galvanizing properties and recyclability. However, the perception of zinc as a commodity rather than a specialized material limits its differentiation.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

5.48% |

|

Segments Covered |

By Form, Application, End Use Industest, and Region |

|

Various Analyses Covered |

Global, Regional, & Countest Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Nyrstar (BE), Teck Resources (CA), Glencore (CH), Southern Copper Corporation (US), KGHM Polska Miedz (PL), Hindustan Zinc Limited (IN), Zinc Nacional (MX), Boliden AB (SE) |

SEGMENTAL ANALYSIS

By Form Insights

The sheet form segment was accounted in holding 45.6% of the Europe zinc market share in 2025 with sthe extensive utilize of zinc sheets in architectural applications, particularly for roofing, cladding, and facade systems. Zinc sheets are favored for their aesthetic appeal, durability, and ability to develop a protective patina over time, which enhances the longevity of buildings. According to the European Copper Zinc and Brass Association, the construction sector in Europe consumes a significant portion of rolled zinc products, with architectural applications representing a stable and high value segment. The renovation of historic buildings and the construction of modern sustainable structures have bolstered demand for zinc sheets, as architects prioritize materials that offer both visual distinctiveness and environmental benefits. Additionally, zinc sheets are fully recyclable, aligning with the stringent sustainability standards imposed by green building certifications such as BREEAM and LEED. The ease of installation and low maintenance requirements further contribute to their popularity among contractors and developers.

The powder form segment is anticipated to witness a quickest CAGR of 5.8% from 2026 to 2034 with the increasing adoption of zinc powder in the production of zinc rich paints and coatings, which provide superior corrosion protection for steel structures. The demand for anti corrosive coatings is rising across various industries, including marine, automotive, and infrastructure, due to the necessary for extconcludeed asset life and reduced maintenance costs. As per the International Zinc Association, the utilize of zinc rich primers has increased by 10% in industrial applications, reflecting a shift towards more effective corrosion management strategies. Additionally, advancements in powder metallurgy have expanded the utilize of zinc powder in the production of sintered parts and chemical applications, such as pharmaceuticals and agriculture. The versatility of zinc powder allows for customization in particle size and purity, catering to diverse technical requirements. The focus on sustainability and resource efficiency also favors zinc powder, as it enables precise application and minimal waste.

By Application Insights

The galvanizing application segment was the largest by occupying a significant share of the Europe zinc market in 2025 owing to the galvanizing in protecting steel from corrosion, which is essential for infrastructure, automotive, and construction projects. Hot dip galvanizing is the most widely utilized method, providing a robust and long lasting protective layer that significantly extconcludes the service life of steel components. According to the European General Galvanizers Association, the galvanizing industest in Europe processes millions of tons of steel annually, underscoring its industrial significance. The durability of galvanized steel reduces the necessary for frequent maintenance and replacement by offering cost effective solutions for large scale projects. As per Eurostat, public investment in infrastructure, including bridges, highways, and energy networks, remains a priority in the European Union, driving steady demand for galvanized products. The automotive industest also relies heavily on galvanized steel for vehicle bodies to ensure safety and longevity, particularly in harsh weather conditions. Furthermore, the emphasis on sustainability favors galvanizing, as zinc is fully recyclable and the process has a relatively low environmental impact compared to alternative coating methods.

The die casting application segment is likely to register a quickest CAGR of 5.2% throughout the forecast period owing to the increasing demand for precision engineered components in the automotive, electronics, and hardware industries. Zinc die casting offers excellent fluidity, allowing for the production of complex shapes with thin walls and high dimensional accuracy. According to the European Die Casting Association, the automotive sector is the largest consumer of zinc die castings, utilizing them for parts such as door handles, locks, and engine components. The transition to electric vehicles has further boosted demand, as manufacturers seek lightweight yet strong materials to improve energy efficiency. As per the European Automobile Manufacturers Association, the production of electric vehicles in Europe is rising, creating new opportunities for zinc based components. Additionally, the electronics industest utilizes zinc die castings for hoapplyings and connectors due to their electromagnetic shielding properties and aesthetic finish. Advances in die casting technology, such as vacuum assisted processes, have improved the quality and consistency of zinc parts, building them suitable for high performance applications. The ability to recycle zinc scrap generated during the die casting process also aligns with circular economy goals.

By End Use Industest Insights

The construction conclude utilize industest segment was the largest by holding 55.4% of the Europe zinc market share in 2025 with the extensive utilize of zinc in roofing, cladding, and structural components, where its corrosion resistance and aesthetic qualities are highly valued. Zinc sheets and alloys are preferred for their ability to withstand harsh weather conditions and maintain their appearance over decades, reducing long term maintenance costs. According to the European Construction Industest Federation, the construction sector is a major contributor to the European economy, with significant investments in both new builds and renovations. The European Green Deal and related sustainability initiatives encourage the utilize of durable and recyclable materials, favoring zinc over less sustainable alternatives. The renovation wave strategy, aimed at improving energy efficiency in existing buildings, also drives demand for zinc based facade systems and roofing solutions. Additionally, zinc’s compatibility with other building materials and its ease of installation create it a preferred choice for architects and contractors. The presence of established suppliers and standardized installation practices further supports its widespread adoption.

The automotive conclude utilize industest segment is esteemed to register a quickest CAGR of 4.9% from 2026 to 2034 with the increasing utilize of zinc in vehicle manufacturing, particularly for galvanizing steel bodies and producing die cast components. The shift towards electric vehicles (EVs) has amplified this demand, as autocreaters require lightweight and corrosion resistant materials to enhance battery range and vehicle durability. According to the European Automobile Manufacturers Association, EV production in Europe is accelerating, with millions of units expected to be produced annually in the coming years. Zinc coated steel is essential for protecting EV chassis and body panels from rust, ensuring safety and longevity. As per Statista, the average amount of zinc utilized per vehicle has increased due to the complexity of modern automotive designs and the necessary for advanced protection. Additionally, zinc die castings are utilized for intricate parts such as transmission components and interior fittings, benefiting from the metal’s precision casting capabilities. The automotive industest’s focus on sustainability also promotes the utilize of recycled zinc, aligning with corporate environmental goals. Collaborations between zinc producers and autocreaters facilitate the development of specialized alloys and coatings tailored to EV requirements.

REGIONAL ANALYSIS

Germany Zinc Market Analysis

Germany was the top performer in the Europe zinc market by holding 24.4% of the share in 2025 with the rising demand for the zinc products in automotive and construction sectors. According to the German Federal Statistical Office, Germany is the largest producer of automobiles in Europe, with millions of vehicles manufactured annually, each requiring substantial amounts of galvanized steel and die cast components. The construction industest also contributes heavily to zinc consumption, with ongoing infrastructure projects and residential developments utilizing zinc for roofing and cladding. As per the German Zinc Forum, the countest has a well established recycling infrastructure for zinc, supporting sustainable production practices. Germany’s central location and advanced logistics network facilitate the distribution of zinc products across the continent. The presence of major zinc processors and downstream manufacturers ensures a stable supply chain and high quality standards. Additionally, the countest’s commitment to environmental sustainability encourages the adoption of green technologies and recycled materials. Government incentives for energy efficient buildings and electric vehicles further boost zinc demand.

Italy Zinc Market Analysis

Italy zinc market was positioned second by holding 18.3% of share in 2025 with the architectural heritage and design excellence, which drive the demand for zinc sheets in roofing and facade applications. According to the Italian National Institute of Statistics, the construction sector in Italy has revealn resilience, with significant investments in renovation and restoration projects. Zinc is preferred for its aesthetic versatility and durability, building it ideal for both historic and modern buildings. As per the Italian Zinc Development Association, the utilize of zinc in architectural projects has increased, supported by government incentives for energy efficient renovations. The automotive industest in Italy, although compacter than Germany’s, also contributes to zinc demand through local manufacturing and aftermarket services. Italy’s strong export market for luxury goods and machinery utilizes zinc die castings for high quality components. The countest’s focus on sustainability and circular economy principles promotes the recycling of zinc materials. Strategic partnerships with international suppliers ensure a reliable flow of raw materials.

France Zinc Market Analysis

France zinc market is expected to witness a quickest CAGR in coming years with the utilize of zinc for architectural purposes in Paris and other major cities, where zinc roofs are iconic. According to the French Ministest of Ecological Transition, strict urban planning regulations and heritage preservation efforts favor the utilize of traditional materials like zinc. The construction sector in France is robust, with ongoing projects in hoapplying and public infrastructure driving steady demand. As per the French Zinc Committee, the architectural segment accounts for a significant portion of zinc consumption, supported by a strong culture of craftsmanship and design. The automotive and aerospace industries also contribute to zinc demand, utilizing galvanized steel and die cast components for manufacturing. France’s commitment to environmental sustainability encourages the utilize of recyclable materials, aligning with zinc’s eco-friconcludely profile. The presence of major zinc suppliers and processors in the region ensures efficient distribution and technical support.

Spain Zinc Market Analysis

Spain zinc market growth is likely to grow with the tourism related infrastructure and residential developments. According to the Spanish National Statistics Institute, construction activity in Spain has rebounded, with increased investment in coastal and urban projects. Zinc is widely utilized for roofing and cladding in these developments due to its resistance to saline environments and aesthetic appeal. As per the Spanish Association of Zinc Producers, the automotive industest also contributes to zinc consumption, with several major manufacturers operating plants in the countest. The production of vehicles for domestic and export markets requires galvanized steel and die cast parts. Spain’s focus on renewable energy infrastructure, including wind farms, creates additional demand for corrosion resistant materials. The countest’s strategic location facilitates trade with North Africa and Latin America, expanding market opportunities. Government policies supporting sustainable construction and energy efficiency promote the utilize of durable materials like zinc.

United Kingdom Zinc Market Analysis

The United Kingdom zinc market growth is likely to have a prominent opportunities in coming years with the rising prominence for infrastructure and automotive sectors. According to the Office for National Statistics, investment in infrastructure projects, including transport and energy networks, continues to support zinc consumption. The construction industest utilizes zinc for roofing and cladding in both commercial and residential buildings, valuing its durability and low maintenance. As per the Society of Motor Manufacturers and Traders, the UK automotive sector remains a significant consumer of galvanized steel and die cast components, despite shifts in production volumes. The transition to electric vehicles presents new opportunities for zinc applications in battery hoapplyings and structural parts. The UK’s regulatory framework emphasizes sustainability and carbon reduction, encouraging the utilize of recyclable materials. Post Brexit trade arrangements have required adjustments in supply chains, but established relationships with European suppliers ensure continuity.

COMPETITIVE LANDSCAPE

The competition within the Europe zinc market is characterized by a consolidated structure dominated by a few large integrated producers and trading houtilizes. These key players compete primarily on the basis of production efficiency sustainability credentials and supply chain reliability. The high capital intensity of smelting operations and strict environmental regulations create significant barriers to entest for new competitors. Companies differentiate themselves through advancements in recycling technologies and the ability to offer low carbon zinc products. Price volatility in energy and raw materials necessitates robust risk management strategies and flexible contracting models. The shift towards circular economy principles drives competition in secondary zinc recovery rates and quality. Collaborative efforts with downstream industries assist tailor products to specific applications such as automotive galvanizing and architectural roofing. Regulatory compliance serves as a critical factor influencing competitive dynamics with firms investing heavily in emission reduction technologies. The market remains sensitive to global supply disruptions and geopolitical tensions affecting concentrate availability.

KEY MARKET PLAYERS

Some of the notable key players in the Europe zinc market are

- Nyrstar (BE)

- Teck Resources (CA)

- Glencore (CH)

- Southern Copper Corporation (US)

- KGHM Polska Miedz (PL)

- Hindustan Zinc Limited (IN)

- Zinc Nacional (MX)

- Boliden AB (SE)

Top Players in the Market

- Nyryst NV operates as a leading integrated zinc mining and recycling company with significant production assets across Europe. The company contributes to the global market by supplying high quality zinc metal and alloys derived from both primary concentrates and secondary recycled materials. Recent strategic actions include the expansion of its recycling capabilities at facilities in Belgium and the Netherlands to enhance circular economy practices. Nyryst focutilizes on reducing carbon emissions through energy efficiency improvements and the adoption of renewable energy sources in its smelting operations. By investing in advanced hydrometallurgical technologies the firm improves recovery rates and product purity. These initiatives strengthen its position as a sustainable supplier while ensuring consistent output for key industries such as construction and automotive.

- Glencore plc is a major diversified natural resource company with substantial zinc mining and marketing operations influencing the European market. The company plays a critical role in global supply chains by trading and distributing zinc metal and concentrates from its international portfolio. Recent efforts to strengthen its market position involve optimizing logistics networks and securing long term off take agreements with European smelters and consumers. Glencore invests heavily in sustainability initiatives aiming to reduce the environmental footprint of its mining activities. The firm leverages its extensive trading platform to manage price volatility and ensure reliable supply for downstream industries. Its strategic partnerships with local producers facilitate efficient material flow into Europe. This approach ensures stability in supply and supports the growing demand for zinc in infrastructure and manufacturing sectors across the region.

- Boliden AB is a prominent Swedish mining and smelting company known for its high efficiency and low carbon footprint in zinc production. The company contributes significantly to the European market through its integrated operations in Sweden and Ireland which produce high grade zinc metal. Recent actions include substantial investments in electrification and digitalization at its smelters to enhance energy efficiency and reduce emissions. Boliden focutilizes on developing innovative solutions for battery metals and recycled materials aligning with the green transition. The company strengthens its market position by maintaining strong relationships with key industrial customers in the automotive and construction sectors. Its commitment to safety and environmental performance sets industest benchmarks. These strategic shifts ensure long term competitiveness and reliability in supplying essential zinc products to the European market.

Top Strategies Used by the Key Market Participants

Key players in the Europe zinc market primarily focus on enhancing recycling capabilities to secure secondary raw material supplies and reduce depconcludeency on imported concentrates. Companies invest heavily in energy efficient technologies to lower production costs and meet stringent carbon emission tarobtains. Strategic partnerships with downstream industries ensure stable demand and facilitate the development of specialized zinc alloys. Vertical integration allows firms to control quality and optimize supply chain logistics. Digital transformation initiatives improve operational efficiency and predictive maintenance in smelting processes. Sustainability reporting and certification are utilized to build trust with environmentally conscious customers. Diversification into high value added products such as zinc powder and chemicals assists mitigate commodity price volatility.

MARKET SEGMENTATION

This research report on the European zinc market has been segmented and sub-segmented based on categories.

By Form

By Application

- Galvanizing

- Die Casting

- Others

By End Use Industest

- Construction

- Transportation

- Consumer Goods

By Countest

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe