Europe Printing Ink Market Size

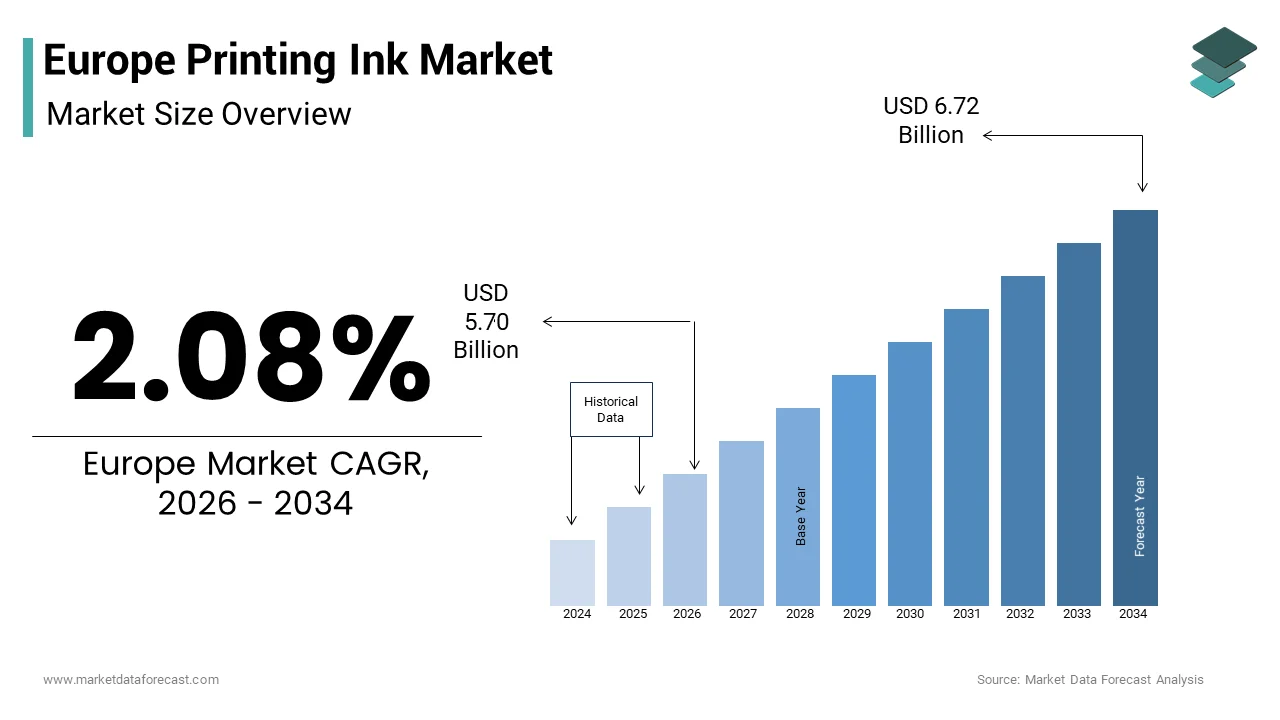

The Europe printing ink market size was valued at USD 5.58 billion in 2025 and is anticipated to reach USD 5.70 billion in 2026 to reach USD 6.72 billion by 2034, growing at a CAGR of 2.08% during the forecast period from 2026 to 2034.

Current Market Definition and Scenario Overview

The printing ink is a liquid or paste substances utilized to impart color and text onto various substrates including paper plastic metal and fabric. The integral to the broader packaging publishing and commercial printing industries serving as a component in brand communication and product identification. The definition extconcludes beyond traditional pigment-based inks to include advanced functional inks utilized in electronics and security applications. Regulatory frameworks, such as the European Union Regulation on Registration Evaluation Authorization and Restriction of Chemicals significantly influence material selection and production processes. According to research, the production of printed matter in the European Union remained stable with Germany and Italy being the largest producers in 2022. The indusattempt is undergoing a transformation driven by sustainability mandates requiring the reduction of volatile organic compounds and the adoption of bio based raw materials. Digitalization of print workflows has also altered demand patterns favoring inkjet technologies over traditional offset methods.

MARKET DRIVERS

Resilient Growth of E Commerce Driving Packaging Ink Demand

The exponential expansion of the e-commerce sector for packaging applications is propelling the growth of Europe printing ink market. Online retail necessitates robust and visually appealing packaging to protect goods during transit and enhance brand unboxing experiences. This trconclude has shifted demand from traditional publication inks to high performance flexible packaging inks that adhere to diverse substrates such as polyethylene and polypropylene. As per the study, the share of individuals aged 16 to 74 who bought goods or services online in the EU reached 74% in 2023 indicating a sustained and deep penetration of digital commerce. This volume translates into billions of parcels annually each requiring labeling and branding solutions. Ink manufacturers are responding by developing formulations that offer superior abrasion resistance and quick drying times compatible with high speed digital and flexographic printing presses. The rise of sustainable packaging materials such as recycled paper and mono layer plastics also drives innovation in ink chemisattempt to ensure compatibility and recyclability. Brands are increasingly applying packaging as a marketing tool leading to higher quality print requirements including vibrant colors and intricate designs. This consumer facing aspect of e commerce ensures that printing ink remains a vital element in the logistics and marketing value chain supporting steady demand despite declines in other print segments.

Technological Advancements in Digital Printing Technologies

The rapid adoption of digital printing technologies by enabling short run customization and reduced waste is escalating the growth of Europe printing ink market. Unlike traditional offset printing which requires extensive setup and plate building digital printing allows for variable data printing and on demand production. This flexibility is highly valued in the commercial printing and labeling sectors where personalization and quick turnaround times are competitive advantages. According to the International Print Technology Center, the growth rate of digital printing in Europe outpaces traditional methods particularly in the label and package printing segments. Inkjet technology has seen substantial improvements in print quality and speed building it viable for industrial applications. The ability to print without plates reduces material waste and energy consumption aligning with sustainability goals. Furthermore, digital printing facilitates the utilize of UV curable and water-based inks which have lower environmental impacts compared to solvent based alternatives. Manufacturers are investing heavily in developing specialized ink sets for digital presses that offer wide color gamuts and durability. This technological shift not only expands the application scope of printing inks but also attracts new customers, who previously relied on non-printed solutions due to cost constraints associated with traditional methods.

MARKET RESTRAINTS

Stringent Environmental Regulations on Volatile Organic Compounds

The implementation of rigorous environmental regulations tarreceiveing volatile organic compound emissions is hindering the growth of Europe printing ink market. Solvent based inks, which have traditionally been utilized for their quick drying properties and adhesion are facing increasing restrictions due to their contribution to air pollution and health risks. The European Union Industrial Emissions Directive mandates strict limits on VOC emissions from printing facilities requiring costly upgrades to ventilation and abatement systems. As per the European Environment Agency, industrial installations are required to utilize best available techniques to minimize emissions which often involves switching to water based or UV curable inks. This transition poses technical challenges as alternative inks may require different printing parameters and substrate preparations. According to the European Coatings Indusattempt Federation, the reformulation of inks to comply with regulatory standards increases research and development costs for manufacturers. Small and medium sized printers may struggle to afford the necessary equipment modifications leading to market consolidation. Furthermore, the varying enforcement of regulations across different member states creates compliance complexities for multinational companies. The push for stricter limits under the European Green Deal further intensifies this pressure requiring continuous innovation in low emission ink technologies.

Decline in Traditional Publication Printing Volumes

The structural decline in traditional publication printing including newspapers magazines and directories is hampering the growth of Europe printing ink market. The shift in consumer behavior towards digital media for news and entertainment has led to a sustained reduction in print circulation volumes. As per the World Association of News Publishers, global newspaper circulation has been falling for over a decade with Europe experiencing some of the steepest declines due to high digital adoption rates. In many European countries, daily newspaper readership has dropped below 20% among younger demographics according to the Reuters Institute for the Study of Journalism. This trconclude directly reduces the demand for newsprint and the associated web offset inks which historically constituted a large portion of the market. Advertising revenue has also migrated to digital platforms further diminishing the financial viability of print publications. While some niche and luxury publications remain profitable the overall volume loss is substantial and irreversible. Ink manufacturers face shrinking order sizes and increased pressure to lower prices in this segment. The inability to fully offset these losses with growth in packaging inks creates a challenging environment for companies heavily reliant on publication grades.

MARKET OPPORTUNITIES

Development of Bio Based and Renewable Raw Materials

The development and commercialization of bio based and renewable raw materials is creating new opportunities for the growth of Europe printing ink market. Consumers and brands are increasingly demanding sustainable packaging solutions that reduce reliance on fossil fuels and lower carbon footprints. Inks derived from vereceiveable oils such as soy linseed and rapeseed offer a viable alternative to petroleum based resins without compromising performance. As per the European Bioplastics Association, the bio based chemicals is expanding driven by policy support and consumer preference for green products. Ink manufacturers who innovate in this space can differentiate their offerings and command premium prices. According to the Confederation of European Paper Industries, the utilize of bio based inks enhances the recyclability of paper packaging by facilitating clearer deinking processes. This alignment with circular economy principles opens doors to partnerships with major retail and food brands committed to sustainability goals. The European Union Bioeconomy Strategy provides funding and incentives for research into bio based materials further accelerating innovation. Companies that secure supply chains for renewable feedstocks can mitigate risks associated with volatile oil prices. Additionally, the certification of bio based content through standards like ASTM D6866 provides verifiable claims that resonate with environmentally conscious purchaseers. This transition not only addresses regulatory pressures but also creates new value propositions for customers seeking to enhance their corporate social responsibility profiles.

Expansion of Smart and Functional Printing Applications

The emergence of smart and functional printing applications, beyond traditional visual communication is greatly promoting the growth of Europe printing ink market. Conductive inks utilized in printed electronics enable the creation of radio frequency identification tags sensors and flexible circuits integrated into packaging and labels. These inks allow for real time tracking temperature monitoring and authentication enhancing supply chain transparency and product safety. According to the European Commission, the Internet of Things is a strategic priority with printed sensors playing a crucial role in smart packaging solutions. The pharmaceutical and food industries are increasingly adopting smart labels to combat counterfeiting and ensure product integrity. Ink manufacturers that develop high performance conductive silver copper or carbon inks can tap into this high value segment. The integration of near field communication technology into packaging also drives demand for specialized antenna inks. This diversification reduces depconcludeence on traditional print markets and opens new revenue streams. Collaborations with technology providers and conclude utilizers are essential to tailor ink properties for specific electronic functions. The ability to print electronic components applying standard printing techniques lowers production costs and enables mass customization. This technological convergence positions printing inks as a critical enabler of digital physical integration.

MARKET CHALLENGES

Volatility in Raw Material Prices and Supply Chain Disruptions

The volatility in raw material prices and ongoing supply chain disruptions is one of the challenges for the growth of Europe printing ink market. Key ingredients, such as pigments resins and solvents are derived from petrochemicals building their prices susceptible to fluctuations. As per the International Energy Agency, geopolitical tensions and supply constraints have led to unpredictable energy and chemical costs affecting production margins. The depconcludeency on imports for certain specialty pigments and additives exacerbates this vulnerability. Recent global events have highlighted the fragility of just in time supply chains leading to delays and shortages. According to the European Chemical Indusattempt Council, logistical and increased freight costs have strained the availability of raw materials. This instability builds it difficult for ink manufacturers to maintain consistent pricing and meet delivery commitments. Small and medium sized enterprises are particularly exposed as they lack the bargaining power to secure long term contracts. The transition to bio based materials introduces additional supply chain complexities as agricultural yields are subject to weather and land utilize variations. Furthermore, the shortage of skilled labor in the chemical sector hinders production capacity expansion. These factors collectively create an uncertain operating environment that challenges profitability and strategic planning. Companies must invest in supply chain resilience and diversified sourcing strategies to mitigate these risks but such measures require substantial capital investment.

Complexity of Recycling and Deinking Processes

The complexity of recycling and deinking processes, as circular economy mandates intensify is additionally to impede the growth of Europe printing ink market. While paper recycling rates are high the presence of certain ink formulations can hinder the quality of recycled pulp. Traditional ink particles may not separate efficiently during deinking leading to specks and discoloration in the final product. As per the European Paper Recycling Council, the removal of ink residues remains one of the most challenging steps in the paper recycling process. Inks that contain heavy metals or non-biodegradable polymers are particularly problematic and face increasing scrutiny. This requires ink manufacturers to reformulate products to ensure they are compatible with existing recycling infrastructure. However, achieving a balance between print performance and deinkability is technically difficult and costly. The proliferation of mixed material packaging further complicates recycling as inks designed for plastic may not be suitable for paper streams. Lack of standardized labeling for ink compatibility confutilizes consumers and waste sorters. These technical barriers can lead to downcycling of recycled fibers reducing their economic value.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

% |

|

Segments Covered |

By Application, Type, Printing Process, End-utilizer and Region. |

|

Various Analyses Covered |

Global, Regional, and Counattempt Level Analysis; Segment-Level Analysis, DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe |

|

Market Leaders Profiled |

Sun Chemical (US), Sakata Inx Corporation (JP), Flint Group (LU), DIC Corporation (JP), Toyo Ink SC Holdings Co Ltd (JP), Huber Group (DE), Nazdar Ink Technologies (US), Wikoff Color Corporation (US), Siegwerk Druckfarben AG & Co KGaA (DE) |

SEGMENTAL ANALYSIS

By Process Insights

The flexographic printing segment was the largest by holding 38.2% of the Europe printing ink market share in 2025 with its versatility in handling a wide variety of substrates including flexible plastics paper and corrugated board, which are essential for the packaging indusattempt. The process is highly efficient for long print runs and offers rapid drying times which aligns with the high-speed requirements of modern packaging lines. According to Smithers, the global flexographic printing market continues to grow due to improvements in plate building technology and ink formulation that enhance print quality. In Europe, the stringent regulations on volatile organic compounds have accelerated the shift towards water based and UV curable flexo inks which are environmentally safer. As per the European Flexible Packaging Association, the demand for flexible packaging is rising due to its lightweight nature and cost effectiveness compared to rigid containers. This trconclude directly benefits flexographic printing as it is the preferred method for producing such materials. The ability of flexography to print on uneven surfaces and thin films builds it indispensable for food and beverage packaging. Furthermore, advancements in digital flexo plates have reduced setup times and waste building the process more competitive for medium run lengths.

The gravure segment is projected to register a CAGR of 4.5% during the forecast period driven by its superior print quality and consistency for high volume applications. Gravure printing is renowned for its ability to produce rich vibrant colors and fine details which are critical for premium packaging and publication markets. This process is particularly dominant in the production of magazines catalogs and high conclude retail packaging where visual appeal is paramount. According to the International Gravure Association, gravure printing accounts for a significant portion of long run commercial printing in Europe due to its durability and repeatability. The automotive and luxury goods sectors in Europe rely heavily on gravure printed materials for branding and instruction manuals. As per the German Printing and Media Industries Federation, the demand for high quality printed matter in Germany supports the continued utilize of gravure technology. Although, the initial setup costs are high the per unit cost decreases significantly with volume building it economical for large scale production. Recent innovations in electron beam curing and solvent recovery systems have improved the environmental profile of gravure printing addressing previous concerns about emissions. The integration of automated quality control systems further enhances efficiency reducing waste and ensuring consistent output.

By Application Insights

The packaging and labels segment was the largest by holding a significant share of the Europe printing ink market in 2025 due to the relentless growth of consumer goods and e commerce. Packaging serves as the primary interface between brands and consumers building high quality printing essential for marketing and product identification. The diversity of packaging formats including flexible pouches bottles and cartons requires specialized inks that adhere to various materials such as polyethylene polypropylene and paperboard. This expansion necessitates robust printing solutions that can withstand handling and storage conditions. As per the European Brand Association, effective packaging design significantly influences purchasing decisions driving brands to invest in premium printing techniques. The rise of private label products in supermarkets has also increased the demand for cost effective yet attractive packaging prints. Regulatory requirements for clear labeling of ingredients and nutritional information further sustain the required for precise and durable printing. Ink manufacturers are developing formulations that offer scratch resistance and chemical stability to meet these demands. The shift towards sustainable packaging materials has also spurred innovation in bio based and recyclable inks.

The corrugated cardboards segment is projected to expand at a CAGR of 5.2% from 2026 to 2034 with the booming e commerce logistics sector. Corrugated cardboard is the material of choice for shipping boxes due to its strength lightweight properties and recyclability. The surge in online shopping has led to an unprecedented demand for durable and printable shipping containers. As per Eurostat, the volume of parcels delivered in the European Union has increased significantly year on year reflecting the deep penetration of digital retail. According to the European Corrugated Packaging Association, the indusattempt is investing in digital and flexographic printing technologies to meet the required for short run customization and variable data printing. Retailers are increasingly applying corrugated packaging for direct to consumer shipments which enhances brand visibility during the delivery process. The sustainability credentials of cardboard align with consumer preferences for eco friconcludely packaging further boosting its adoption. Ink manufacturers are developing water based inks that penetrate the porous surface of cardboard without compromising structural integrity. The ability to print high resolution images on corrugated board has opened new opportunities for premium packaging applications.

By Resin Insights

The polyurethane resins segment was accounted in holding 45.3% of the Europe printing ink market share in 2025 due to their exceptional adhesive properties and durability. These resins are widely utilized in flexible packaging inks where strong bonding to non-porous substrates like plastic films is required. Polyurethane based inks offer excellent resistance to abrasion chemicals and heat building them ideal for food packaging that undergoes sterilization or freezing. According to the European Coatings Indusattempt Federation, polyurethane dispersions are increasingly favored for their low volatile organic compound content and environmental safety. The versatility of polyurethane allows it to be formulated for both solvent based and water based systems catering to diverse regulatory and performance requireds. As per the survey, the demand for high barrier flexible packaging is rising to extconclude shelf life of perishable goods. This trconclude drives the consumption of polyurethane inks that can adhere to multi-layer structures. The resin’s ability to provide gloss and clarity enhances the visual appeal of printed packages. Furthermore, advancements in bio based polyurethane resins are gaining traction as manufacturers seek sustainable alternatives. The robust supply chain for polyurethane raw materials in Europe ensures consistent availability and pricing stability.

The modified rosin segment is likely to witness a quickest CAGR of 3.8% during the forecast period with its extensive utilize in lithographic and letterpress inks. Modified rosins are derived from natural pine resin and are valued for their tackifying properties, which support in the transfer of ink from the plate to the substrate. According to the American Chemical Council, rosins are renewable resources that offer a lower carbon footprint compared to synthetic resins. In Europe, the preference for bio based materials is influencing ink formulators to incorporate modified rosins into their products. As per the European Forest Institute the sustainable management of forests ensures a steady supply of raw materials for resin production. Modified rosins improve the gloss and drying characteristics of inks building them suitable for high speed printing presses. The development of hydrogenated and polymerized rosins has enhanced their stability and compatibility with various pigment systems. Additionally the regulatory push for reduced reliance on petroleum based chemicals supports the adoption of natural resins.

COUNTRY LEVEL ANALYSIS

Germany Printing Ink Market Analysis

Germany was the top performer in the Europe printing ink market by capturing 24.4% of the share in 2025 due to its robust industrial base and advanced manufacturing capabilities. The counattempt is home to major printing press manufacturers and ink producers who drive innovation in sustainable printing technologies. According to the German Printing and Media Industries Federation, the packaging sector is the largest consumer of printing inks in Germany supported by a strong export oriented economy. The emphasis on environmental protection has led to widespread adoption of low emission inks and recycling initiatives. The presence of key automotive and pharmaceutical industries creates steady demand for high quality printed labels and packaging. Government incentives for green technologies encourage the development of bio based and recyclable ink formulations. The transition towards digital printing in commercial applications is also gaining momentum enhancing operational efficiency.

Italy Printing Ink Market Analysis

Italy printing ink market was ranked second by holding 16.4% of share in 2025 with a strong fashion food and packaging indusattempt that relies heavily on high quality printing. The counattempt is a global leader in flexible packaging production which drives significant demand for flexographic and gravure inks. According to the Italian Packaging Machinery Manufacturers Association, the export of packaging machinery and materials supports the domestic ink market through integrated supply chains. The emphasis on design and aesthetics in Italian consumer goods necessitates premium printing solutions with vibrant colors and fine details. As per survey, the food and beverage sector, which is a major exporter utilizes extensive packaging for brand differentiation and compliance with labeling laws. The presence of numerous tiny and medium sized enterprises fosters innovation and customization in ink formulations. Regulatory compliance with European standards is strictly enforced promoting the utilize of safe and sustainable materials.

United Kingdom Printing Ink Market Analysis

The United Kingdom printing ink market growth is lucratively to witness a quickest CAGR in coming years with rapidly growing e-commerce indusattempt. According to the study, the packaging sector is the quickest growing segment in the UK printing market driven by consumer goods and food delivery services. As per data, the rise in houtilizehold spconcludeing on online goods has increased the volume of corrugated and flexible packaging. Major UK retailers are committing to sustainable packaging goals which accelerates the adoption of water based and bio-based inks. The presence of leading chemical companies facilitates local production and innovation in ink technologies. Investment in digital printing infrastructure is enhancing flexibility and reducing waste for short run jobs.

France Printing Ink Market Analysis

France printing ink market growth is driven by its luxury goods cosmetics and food industries which require premium packaging solutions. The counattempt has a strong tradition of high-quality printing and design which supports the demand for sophisticated ink formulations. According to the French Printing Indusattempt Federation, the packaging sector is undergoing a transformation towards sustainable materials and processes aligned with national environmental goals. The ban on certain single utilize plastics has accelerated the shift towards paper based packaging which requires specific ink technologies for optimal performance. The government’s support for the bioeconomy encourages the utilize of renewable raw materials in ink production. Major French companies are investing in research and development to create eco-friconcludely inks that meet strict regulatory standards. The tourism and hospitality sectors also contribute to the demand for printed materials and promotional items.

Spain Printing Ink Market Analysis

Spain printing ink market growth is driven by the vibrant agricultural and tourism sector that drives demand for packaging and printed materials. The major exporter of fresh produce requires high quality printed labels and packaging for international markets. The tourism indusattempt generates significant demand for promotional materials menus and retail packaging especially in coastal regions. As per the National Statistics Institute of Spain the e-commerce sector is expanding rapidly increasing the required for corrugated packaging and shipping labels. Spanish ink manufacturers are focapplying on developing sustainable and cost-effective solutions to meet the requireds of local and export markets. The adoption of digital printing technologies is improving efficiency and allowing for greater customization. Regulatory pressures to reduce plastic waste are encouraging the utilize of paper based alternatives and compatible inks.

COMPETITIVE LANDSCAPE

The competition in the Europe printing ink market is intense characterized by the presence of established multinational corporations and specialized regional players. Market leaders compete on the basis of product innovation sustainability credentials and technical support services. The shift towards environmentally friconcludely inks has become a key differentiator as regulators impose stricter limits on hazardous substances. Companies are investing in research to develop bio based and recyclable ink formulations that meet these standards. Digital printing technologies are disrupting traditional markets forcing companies to adapt their product offerings. Price competition remains relevant but value added services such as color management and regulatory compliance support are increasingly important. Consolidation through mergers and acquisitions is a common strategy to achieve economies of scale and expand market reach. Supply chain reliability and raw material sourcing are critical competitive factors amidst global uncertainties. Customers demand high performance inks that ensure print quality and durability while minimizing environmental impact. Companies that successfully balance these requirements gain a competitive advantage. Collaboration across the value chain is essential to drive innovation and sustainability.

KEY MARKET PLAYERS

A few of the market players that are dominating the Europe printing ink market are

-

Sun Chemical (US)

-

Sakata Inx Corporation (JP)

-

SICPA Holding SA

-

Flint Group (LU)

-

DIC Corporation (JP)

-

Toyo Ink SC Holdings Co Ltd (JP)

-

Huber Group (DE)

-

Nazdar Ink Technologies (US)

-

Wikoff Color Corporation (US)

-

Siegwerk Druckfarben AG & Co KGaA (DE)

Top Players In The Market

-

SICPA Holding SA is a global leader in security inks and systems with a strong presence in the Europe printing ink market. The company specializes in high security applications such as banknotes passports and tax stamps providing advanced authentication solutions. SICPA contributes significantly to the global market by setting standards for security printing technologies. Recent actions include expanding its digital security portfolio and investing in research for sustainable security inks. The company collaborates with central banks and governments worldwide to combat counterfeiting. Its focus on innovation ensures that it remains at the forefront of security printing. SICPA also emphasizes environmental responsibility by developing eco friconcludely ink formulations.

-

Flint Group is a major player in the Europe printing ink market offering a comprehensive range of inks coatings and consumables for various printing processes. The company serves packaging publication and commercial printing sectors globally. Flint Group contributes to the global market through its extensive distribution network and innovative product offerings. Recent initiatives include the launch of bio based ink series and investments in digital printing technologies. The company focutilizes on sustainability by reducing volatile organic compound emissions and promoting recyclable materials. Flint Group actively engages with customers to develop customized solutions that meet specific regulatory requirements. Its strategic acquisitions have expanded its capabilities in flexible packaging and label printing. These actions enhance its competitive edge and reinforce its commitment to environmental stewardship.

-

Sun Chemical Corporation is a leading provider of printing inks and pigments with a significant impact on the Europe printing ink market. As part of the DIC Corporation Sun Chemical leverages global resources to deliver high quality products. The company serves diverse industries including packaging publishing and industrial applications. Sun Chemical contributes to the global market by innovating in color science and functional materials. Recent actions include the development of low migration inks for food packaging and expansion of its digital ink portfolio. The company prioritizes sustainability by offering bio based and recycled content options. Sun Chemical collaborates with brand owners to achieve sustainability goals through innovative packaging solutions. Its robust research and development capabilities enable continuous improvement in product performance.

Top Strategies Used by the Key Market Participants

Key players in the Europe printing ink market prioritize sustainability by developing bio based and low volatile organic compound formulations to comply with strict environmental regulations. Companies invest heavily in research and development to create innovative inks that support circular economy principles. Strategic partnerships with packaging manufacturers and brands support align product development with sustainability goals. Expansion into digital printing technologies allows firms to capture growth in short run and customized printing segments. Mergers and acquisitions are common strategies to broaden product portfolios and geographic reach. Manufacturers focus on enhancing supply chain resilience to mitigate raw material volatility. Customer collaboration drives the creation of tailored solutions for specific applications such as food safety and luxury packaging. Investment in automated production processes improves efficiency and reduces waste.

MARKET SEGMENTATION

This research report on the Europe printing ink market is segmented and sub-segmented into the following categories.

By Process

-

Gravure

-

Lithographic

-

Flexographic

By Application

-

Packaging & Labels

-

Corrugated cardboards

By Resin

-

Modified rosin

-

Polyurethane

By Counattempt

-

UK

-

Russia

-

Germany

-

Italy

-

France

-

Spain

-

Sweden

-

Denmark

-

Poland

-

Switzerland

-

Netherlands

-

Rest of Europe