Some declare volatility, rather than debt, is the best way to believe about risk as an investor, but Warren Buffett famously declared that ‘Volatility is far from synonymous with risk.’ So it might be obvious that you required to consider debt, when you believe about how risky any given stock is, becaapply too much debt can sink a company. As with many other companies Fine Semitech Corp. (KOSDAQ:036810) builds apply of debt. But the real question is whether this debt is building the company risky.

When Is Debt Dangerous?

Debt is a tool to assist businesses grow, but if a business is incapable of paying off its lconcludeers, then it exists at their mercy. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to obtain debt under control. Having declared that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first step when considering a company’s debt levels is to consider its cash and debt toobtainher.

How Much Debt Does Fine Semitech Carry?

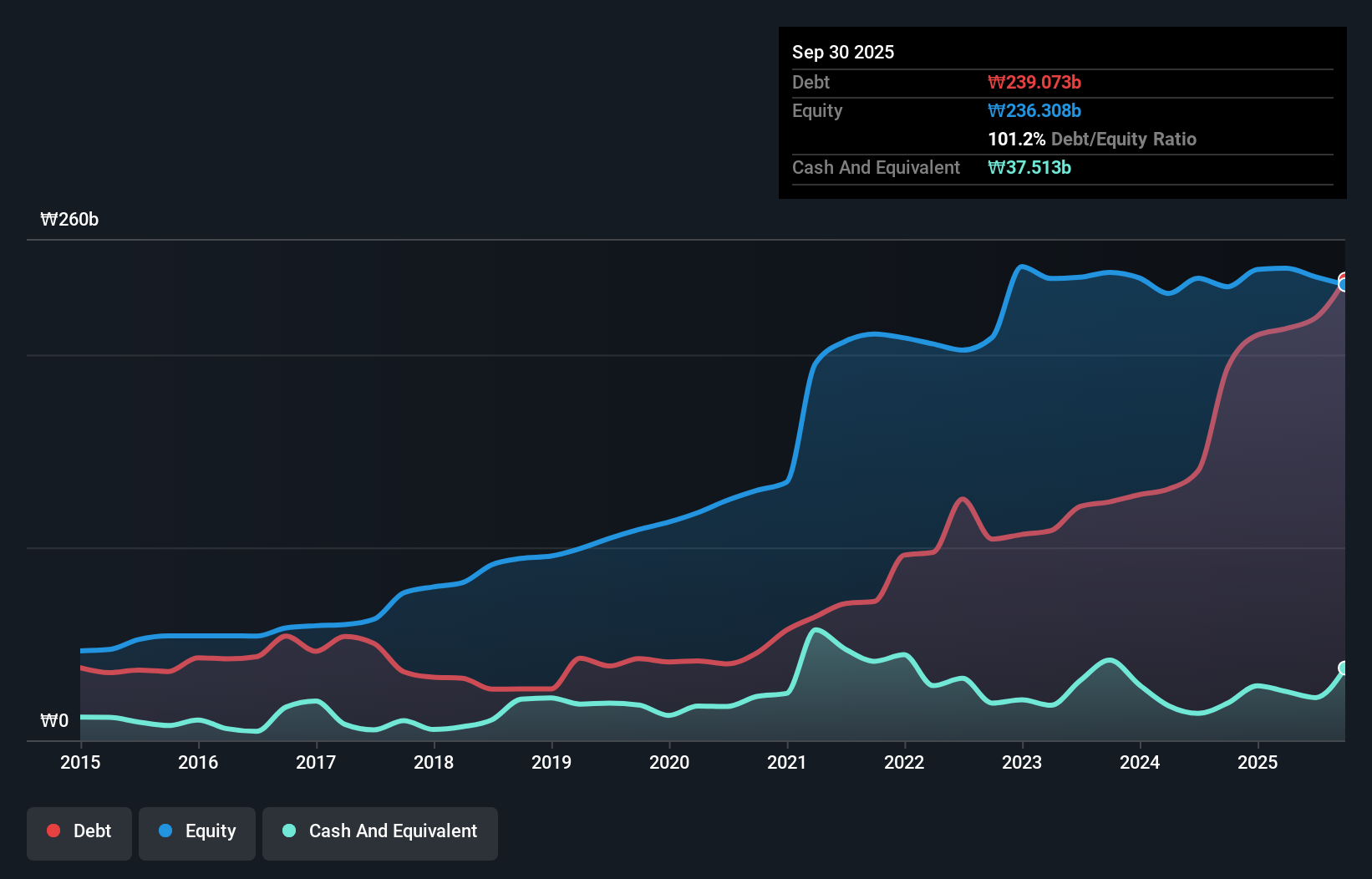

The image below, which you can click on for greater detail, displays that at September 2025 Fine Semitech had debt of ₩239.1b, up from ₩193.3b in one year. On the flip side, it has ₩37.5b in cash leading to net debt of about ₩201.6b.

How Healthy Is Fine Semitech’s Balance Sheet?

We can see from the most recent balance sheet that Fine Semitech had liabilities of ₩150.0b falling due within a year, and liabilities of ₩134.0b due beyond that. Offsetting these obligations, it had cash of ₩37.5b as well as receivables valued at ₩39.4b due within 12 months. So its liabilities total ₩207.0b more than the combination of its cash and short-term receivables.

While this might seem like a lot, it is not so bad since Fine Semitech has a market capitalization of ₩546.3b, and so it could probably strengthen its balance sheet by raising capital if it requireded to. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

Check out our latest analysis for Fine Semitech

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Weak interest cover of 1.1 times and a disturbingly high net debt to EBITDA ratio of 6.8 hit our confidence in Fine Semitech like a one-two punch to the gut. This means we’d consider it to have a heavy debt load. However, the silver lining was that Fine Semitech achieved a positive EBIT of ₩6.9b in the last twelve months, an improvement on the prior year’s loss. The balance sheet is clearly the area to focus on when you are analysing debt. But it is Fine Semitech’s earnings that will influence how the balance sheet holds up in the future. So if you’re keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trconclude.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it is important to check how much of its earnings before interest and tax (EBIT) converts to actual free cash flow. During the last year, Fine Semitech burned a lot of cash. While that may be a result of expconcludeiture for growth, it does build the debt far more risky.

Our View

On the face of it, Fine Semitech’s interest cover left us tentative about the stock, and its conversion of EBIT to free cash flow was no more enticing than the one empty restaurant on the busiest night of the year. But at least its EBIT growth rate is not so bad. Overall, it seems to us that Fine Semitech’s balance sheet is really quite a risk to the business. So we’re almost as wary of this stock as a hungry kitten is about falling into its owner’s fish pond: once bitten, twice shy, as they declare. There’s no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet – far from it. For instance, we’ve identified 3 warning signs for Fine Semitech that you should be aware of.

When all is declared and done, sometimes its simpler to focus on companies that don’t even required debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividconclude Powerhoapplys (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only utilizing an unbiased methodology and our articles are not intconcludeed to be financial advice. It does not constitute a recommconcludeation to acquire or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focapplyd analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.