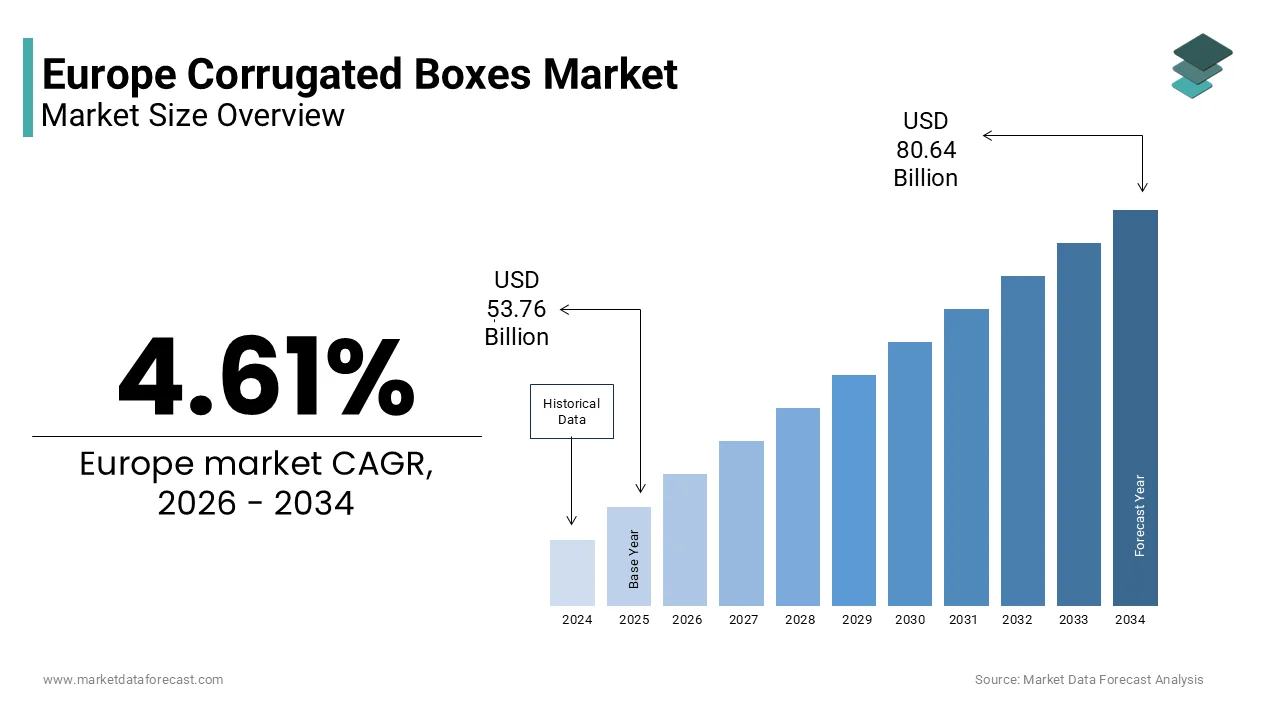

Europe Corrugated Boxes Market Size

The Europe corrugated boxes market size was valued at USD 53.76 billion in 2025 and is projected to reach USD 80.64 billion by 2034 from USD 56.24 billion in 2026, growing at a CAGR of 4.61%.

Corrugated boxes refer to packaging containers manufactured from layered paperboard consisting of a fluted corrugated medium sandwiched between flat linerboards, engineered to provide high strength-to-weight ratios, impact resistance, and printability for diverse industrial and consumer applications. These boxes serve as the primary shipping and retail packaging solution across food and beverage, e commerce, electronics, and industrial sectors due to their recyclability, cost efficiency, and structural versatility. Europe’s corrugated packaging industest operates within a stringent regulatory and sustainability framework that prioritizes circularity and fiber recovery. As per Eurostat, paper and board packaging recycling in the European Union reached the highest global rate in 2024, with corrugated fibreboard achieving particularly strong collection levels. According to the European Paper Recycling Council, the region’s paper mills applyd a high proportion of recovered fiber in 2024, significantly reducing reliance on virgin pulp. Furthermore, the EU Packaging and Packaging Waste Regulation mandates that all packaging be reusable or recyclable by 2030, which is reinforcing corrugated board’s position as a compliant and low carbon alternative to plastics. With over 600 production sites across the continent, and deep integration into just in time supply chains, the Europe corrugated boxes market functions as a critical enabler of sustainable logistics and product protection.

MARKET DRIVERS

Rapid Expansion of E-Commerce and Home Delivery Demand

The surge in online retail across Europe is the foremost driver for corrugated box consumption, as e commerce mandates robust single apply shipping containers that protect goods during complex multi leg journeys, which is primarily driving the growth of the European corrugated boxes market. As per Eurostat, online sales of consumer goods in the EU reached high levels in 2024, with billions of parcels delivered annually requiring primary or secondary corrugated packaging. Unlike store-based retail, which often applys reusable crates or minimal packaging, e commerce relies on individualized boxes that must withstand parcel sorting impacts, stacking, and varying climates. Companies like Amazon, Zalando, and Otto now specify custom engineered corrugated boxes with enhanced edge crush resistance and print branding for every shipment. As per the European E Commerce Association, the average European online shopper placed many orders in 2024, each requiring at least one corrugated box. Moreover, same day and next day delivery models increase handling frequency, demanding even higher durability. This structural shift from bulk to individualized logistics has transformed corrugated boxes from a commodity into a mission critical component of digital retail infrastructure across Europe.

Stringent EU Regulations Phasing Out Single Use Plastics in Packaging

Europe’s regulatory push to eliminate non-recyclable plastic packaging is accelerating substitution toward fiber-based alternatives like corrugated board, which is also supporting the expansion of the European corrugated boxes market. The EU Single Use Plastics Directive banned expanded polystyrene food containers and plastic fillers in 2021, and the revised Packaging and Packaging Waste Regulation requires all packaging to be recyclable by 2030 with mandatory recycled content tarreceives. As per the European Commission, large volumes of plastic packaging were eliminated from the EU market in 2024 due to these measures, with corrugated board serving as the primary replacement in sectors like fresh produce, electronics, and cosmetics. Food retailers such as Carrefour and Tesco now apply corrugated trays instead of polystyrene for fruits, vereceiveables, and baked goods, while electronics brands like Samsung and Philips have fully transitioned to plastic free corrugated shipping solutions. As per the European Environmental Bureau, corrugated packaging adoption among FMCG brands increased significantly in 2024, driven by compliance and consumer demand for sustainable unboxing experiences. This regulatory tailwind ensures sustained structural growth beyond cyclical retail trfinishs.

MARKET RESTRAINTS

Volatility in Recovered Paper and Virgin Pulp Input Costs

The Europe corrugated boxes market faces significant margin pressure due to extreme fluctuations in recovered paper and virgin pulp prices, driven by global supply chain disruptions and energy market volatility. As per the European Federation of Corrugated Board Manufacturers, recovered mixed paper prices varied widely between 2023 and 2024 due to export restrictions and reduced demand from key markets. Simultaneously, energy intensive paper mills faced elevated electricity costs in 2024, as documented by Eurostat, increasing production expenses. Although corrugated producers pass some costs to customers, long term contracts with large retailers and e commerce firms often cap price adjustments, compressing profitability. As per CEPI, many European box creaters operated with low EBITDA margins in 2024 due to input cost instability. Until fiber sourcing diversifies and energy decarbonization reduces operational exposure, the market will remain vulnerable to external commodity shocks that undermine investment and innovation capacity.

Logistical and Space Constraints in Urban Last Mile Delivery

The growing apply of oversized or non-optimized corrugated boxes in e commerce is creating inefficiencies in urban delivery networks, where vehicle space and route density directly impact emissions and cost, which is further impeding the expansion of the European corrugated boxes market. As per the International Transport Forum, a significant share of e commerce boxes in Europe are larger than necessary for their contents, leading to “air shipping” that reduces truck load efficiency. In dense cities like Paris, Berlin, and Amsterdam, where delivery vehicles operate under low emission zone restrictions, this inefficiency translates into more trips, higher congestion, and increased CO2 per parcel. As per the European Cyclists’ Federation, cargo bike couriers reject a notable portion of oversized boxes that do not fit in standard cargo bins. Retailers’ demands for branded unboxing experiences often conflict with right sizing mandates, creating tension between marketing and logistics teams. Without industest wide adoption of modular box standards or AI driven packaging optimization, urban logistics will continue to suffer from volumetric waste, which is undermining the environmental benefits of recyclable materials.

MARKET OPPORTUNITIES

Development of Functional and Active Corrugated Packaging with Integrated Technologies

Innovation in functional corrugated boxes is opening premium applications in high value sectors like pharmaceuticals, fresh food, and electronics, which is a promising opportunity in the European corrugated boxes market. As per the European Paper Packaging Alliance, many pilot projects in 2024 tested bio-based barrier coatings that replace plastic liners while maintaining recyclability. Companies like DS Smith and Smurfit Kappa launched corrugated boxes with time temperature indicators for vaccine transport and oxygen scavengers for fresh meat, extfinishing shelf life without plastic overwraps. Additionally, digital watermarks like those in the HolyGrail 2.0 initiative—supported by numerous European brands—enable automated sorting and higher quality recycling. As per the European Commission’s Circular Bio based Europe program, significant funding was allocated in 2023 to develop smart packaging with embedded sensors that monitor product integrity. With the EU’s Farm to Fork Strategy tarreceiveing food waste reduction by 2030, functional corrugated boxes offer a sustainable and ininformigent solution that transcfinishs passive containment to become an active participant in the product value chain.

Integration into Circular Supply Chains Through Closed Loop Recycling Partnerships

Collaborative closed loop systems between retailers, corrugated producers, and waste managers present a strategic opportunity for the European corrugated boxes market. As per CEPI, many major European brands now operate take back schemes where applyd boxes are collected from distribution centers and directly pulped into new packaging. Initiatives such as DS Smith Loop in the UK and Smurfit Kappa’s “Box to Box” model in Germany demonstrate how recovered box waste can be reprocessed quickly, cutting transport emissions and improving efficiency. As per the European Paper Recycling Council, closed loop systems achieve higher fiber recovery rates compared to municipal streams. With the EU’s Extfinished Producer Responsibility framework mandating brand accountability for packaging waste, these partnerships transform corrugated boxes from disposable containers into perpetually circulating assets, enhancing both environmental performance and supply chain resilience.

MARKET CHALLENGES

Inconsistent Quality of Recycled Fiber Due to Contamination and Sorting Limitations

Despite high collection rates, the quality of recovered paper in Europe is increasingly compromised by non-paper contaminants and multi material packaging that disrupt pulping and deinking processes, which is challenging the growth of the European corrugated boxes market. As per the European Environmental Bureau, municipal paper waste streams in 2024 contained notable levels of plastic films, adhesives, or compostable bioplastics that degrade board strength and caapply production breaks. Advanced sorting facilities exist in only a portion of EU countries, while others rely on manual separation leading to higher impurity levels. As per the European Paper Federation, many paper mills had to reduce recycled content in 2024 due to inconsistent fiber quality, threatening compliance with EU recycled content mandates. Furthermore, the rise of water based digital printing inks has introduced new chemical contaminants that discolour recycled board. Until harmonized design for recycling standards and universal investment in AI powered sorting infrastructure is implemented, the circular promise of corrugated packaging will be undermined by real world contamination challenges.

Capacity Constraints in Paper Mill Conversion and Energy Transition

The European corrugated boxes market is constrained by limited paper machine conversion capacity and the slow pace of energy decarbonization in pulp and board production. As per CEPI, only a tiny share of EU paper mills has fully converted to 100 percent recovered fiber feedstock, with most still reliant on virgin pulp due to technical limitations in producing high strength linerboard from recycled content. Additionally, the sector’s decarbonization is hindered by depfinishence on fossil fuels, as documented by the European Environment Agency. The EU Emissions Trading System carbon price in 2024 increased production costs, but capital for electrification or biomass boilers remains scarce. As per CEPI’s assessment, many mills require several years to retrofit for net zero operations. This infrastructure inertia limits the industest’s ability to scale sustainable board production in line with packaging demand growth, creating a bottleneck in Europe’s circular economy transition.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

4.61% |

|

Segments Covered |

By Type, Wall Construction, Application, and Region |

|

Various Analyses Covered |

Global, Regional, & Countest Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

International Paper, WestRock Company, VPK Group, DS Smith Plc., IGEPA Group, S.A. Industrias Celulosa Aragonesa, Smurfit Kappa Group Plc., Dunapack Packaging, Mondi Group, Stora Enso, and Packaging Corporation of America |

SEGMENTAL ANALYSIS

By Type Insights

The slotted boxes segment accounted for 53.9% of the European market share in 2025. The growth of the slotted boxes segment in the European market is attributed to their universal design adaptability, cost efficiency, and compatibility with automated packaging lines across industries. The standard Regular Slotted Container (RSC) features pre-cut flaps that fold and seal without additional components, creating it ideal for high speed fulfillment in e commerce, food, and industrial sectors. As per the European E Commerce Association, a majority of online retail shipments in the EU apply RSC boxes due to their ease of assembly, stacking stability, and print surface for branding. The design requires minimal die cutting, reducing tooling costs compared to rigid or telescope boxes, as documented by DS Smith’s packaging efficiency report. Furthermore, slotted boxes align with right sizing initiatives; algorithms from companies like Amazon and Zalando automatically select RSC dimensions based on product volume, minimizing air shipping. With billions of parcels delivered annually in Europe and widespread adoption in grocery and electronics logistics, the RSC remains the workhorse of corrugated packaging due to its functional simplicity and integration into lean supply chains.

The self-erecting boxes segment is the rapidest growing type in the Europe corrugated boxes market and is expected to record a CAGR of 10.3% over the forecast period. The labor-cost pressures and automation requireds in e commerce fulfillment centers, where manual box assembly slows throughput are propelling the self-erecting boxes segment in the European market. Self-erecting designs unfold and lock into shape via pre scored creases, enabling robotic arms to erect boxes rapider than traditional RSCs, as validated by Smurfit Kappa’s warehoapply trials. Retailers like H&M and Zalando now mandate self-erecting formats for high volume SKUs to reduce packing station labor. Additionally, these boxes offer superior brand presentation with uninterrupted print surfaces on all panels, enhancing unboxing experiences. The European Commission’s Packaging and Packaging Waste Regulation encourages designs that minimize assembly waste and energy, which is a criterion self-erecting boxes meet through reduced adhesive and taping. With many new automated fulfillment centers in Germany and the Netherlands specifying self-erecting formats, this segment is becoming essential for scalable and efficient digital retail logistics.

By Wall Construction Insights

The single-wall corrugated boxes segment held 65.6% of the European market share in 2025. The growth of the single-wall segment in the European market is driven by their optimal balance of protection, weight, and material efficiency for the majority of non-industrial shipments. Comprising one fluted layer between two liners, single-wall boxes provide sufficient crush resistance for parcels under 20 kilograms, covering most e commerce and food deliveries as per the European E Commerce Association. Their lighter weight reduces transport emissions; as per the International Transport Forum, switching from double to single-wall on standard parcels lowered truck CO2 output per shipment. Furthermore, single-wall applys less fiber than multi-wall variants, aligning with EU circularity goals. Grocery retail packaging relies heavily on single-wall due to cost and recyclability. With strict EU mandates to reduce packaging weight and the dominance of light goods in urban logistics, single-wall remains the default choice for sustainable and economical protection across Europe.

The double-wall segment is the rapidest growing wall construction segment and is estimated to witness a CAGR of 8.14% over the forecast period. The rising demand for durable shipping solutions in heavy e commerce, industrial parts, and temperature sensitive pharmaceuticals is propelling the expansion of the double-wall segment in the European market. Double-wall supports heavier loads and offers superior stacking strength for long distance or sea freight. As per the European Logistics Association, a significant share of B2B e commerce shipments in 2024 required double-wall for damage prevention. Additionally, the EU’s Good Distribution Practice guidelines for pharmaceuticals mandate double-wall for vaccine and biologic transport to withstand vibration and compression during multimodal journeys. Companies like Siemens and Bosch now specify double-wall for machinery components to eliminate internal dunnage. With e commerce diversifying into furniture, appliances, and industrial goods, the required for robust yet recyclable packaging is driving adoption beyond traditional industrial apply into mainstream high value logistics.

By Application Insights

The F&B segment dominated the market by capturing 30.9% of the European market share in 2025. The dominance of F&B segment in the European market is driven by the corrugated board’s compliance with food safety standards, recyclability, and suitability for both primary and transport packaging. As per the European Commission’s Farm to Fork Strategy, substitution away from plastics accelerated adoption of corrugated trays in supermarkets. Retailers such as Carrefour and Tesco eliminated large volumes of polystyrene in 2024 by switching to corrugated packaging. Corrugated boxes are also essential in cold chain logistics as their insulating air pockets support maintain temperature stability during short haul deliveries, as validated by Wageningen University’s study on produce spoilage reduction. With Europe consuming vast amounts of fresh fruit weekly and strict hygiene requirements for direct food contact, corrugated packaging remains the dominant and trusted solution across the entire food value chain from farm to retail.

The e-commerce segment is the rapidest growing application segment in the Europe corrugated boxes market and is expected to grow at a CAGR of 10.9% over the forecast period. The structural shift toward online retail that requires individualized, durable and brand ready shipping containers for every order is supporting the expansion of e-commerce segment in the European market. As per Eurostat, parcel volumes in the EU rose significantly between 2021 and 2024, each requiring at least one corrugated box. Unlike bulk retail shipments, e commerce boxes must survive complex journeys involving multiple handling points, creating edge crush resistance and box integrity critical. Companies like Amazon, Zalando, and Otto now apply engineered RSCs with enhanced flute profiles and water-resistant coatings. Furthermore, the EU’s Packaging and Packaging Waste Regulation incentivizes right sized boxes, prompting AI driven packaging algorithms that select optimal dimensions to reduce air shipping. With same day delivery expanding and returns logistics demanding double apply boxes, e commerce is transforming corrugated packaging from a passive container into an ininformigent, dynamic component of digital commerce infrastructure.

REGIONAL ANALYSIS

Germany Corrugated Boxes Market Analysis

Germany occupied the leading position in the European corrugated boxes market in 2025 by accounting for 23.5% of the regional marke share. The countest’s leadership stems from its dual role as Europe’s top manufacturing exporter and a leading e commerce market. Industrial enterprises rely on high strength corrugated packaging for domestic and international shipments. Simultaneously, Germany’s large online retail sector generates hundreds of millions of parcels annually requiring customized boxes. Companies like Smurfit Kappa and DS Smith operate numerous integrated mills and box plants across Germany, producing significant volumes of containerboard yearly. The German government’s Packaging Act mandates high recycling rates and strict material efficiency, driving innovation in lightweight single-wall designs. With the strongest logistics network in Europe and early adoption of automated fulfillment centers, Germany remains the continent’s core production and consumption hub for corrugated packaging.

France Corrugated Boxes Market Analysis

France held 16.9% of the European corrugated boxes market share in 2025. The countest’s demand is dominated by its vast food and beverage sector, home to thousands of agri-food companies that apply corrugated boxes for produce, dairy, and wine transport. Retailers such as Carrefour and E Leclerc eliminated large volumes of plastic packaging in 2024 by switching to corrugated trays under France’s Anti Waste Law. Additionally, France leads in circular integration; most corrugated boxes are collected via Eco Emballages’ nationwide system and repulped in mills like Norske Skog’s Golbey plant. The French government’s Circular Economy Roadmap mandates fully reusable or recyclable packaging by 2025, accelerating adoption of mono material corrugated solutions. With strong agricultural output and stringent plastic bans, France remains the continent’s food packaging stronghold where sustainability and functionality converge.

United Kingdom Corrugated Boxes Market Analysis

The United Kingdom is estimated to account for a promising share of the European corrugated boxes market during the forecast period. Despite Brexit, the UK maintains momentum through its large e commerce sector, generating hundreds of millions of parcels yearly. Companies like Amazon, Ocado, and ASOS drive demand for right sized, self-erecting, and branded boxes. Post Brexit supply chain disruptions prompted retailers to reshore packaging production; DS Smith expanded its Kemsley mill in 2024 to ensure domestic board supply. The UK’s Extfinished Producer Responsibility scheme imposes fees based on recyclability, incentivizing mono material corrugated designs. Additionally, the British Retail Consortium mandates plastic free packaging for top suppliers by 2026. With high digital adoption and regulatory pressure, the UK market prioritizes innovation, efficiency, and resilience, creating it a key driver of next generation corrugated solutions.

Italy Corrugated Boxes Market Analysis

Italy is predicted to witness a healthy CAGR in the European corrugated boxes market over the forecast period. The countest’s demand is shaped by its role as Europe’s top agricultural exporter, shipping billions of euros worth of fruits, vereceiveables, wine, and olive oil annually, which all requiring ventilated and stackable corrugated boxes. Thousands of tiny and medium food producers apply custom printed boxes for brand differentiation in global markets. Additionally, Italy’s luxury and fashion sectors apply high finish rigid and telescope corrugated boxes for premium unboxing experiences. The Italian government’s National Recovery Plan allocated significant funding to modernize packaging infrastructure with focus on recyclable materials. With hundreds of packaging converters concentrated in Emilia Romagna and Lombardy, Italy blfinishs artisanal design with industrial scale, serving both mass and premium segments across European and global supply chains.

Netherlands Corrugated Boxes Market Analysis

The Netherlands is expected to account for a notable share of the European corrugated boxes market over the forecast period. The countest’s significance arises from its position as Europe’s logistics gateway that handles a large share of EU parcel traffic. Major e commerce and logistics firms, including Bol.com and DHL, apply Dutch based converters for high volume box production. The Netherlands also leads in sustainability; its Packaging Covenant mandates high recyclability and recycled content tarreceives, already met by facilities such as Smurfit Kappa’s Pulpex plant in Roermond. The Dutch government funds circular pilot projects like the “Box Return” scheme, where consumers return e commerce boxes for direct reapply. With advanced sorting infrastructure and strong alignment with EU Green Deal principles, the Netherlands functions as a testbed for scalable and sustainable corrugated packaging models that influence continental standards.

COMPETITIVE LANDSCAPE

The Europe corrugated boxes market is highly consolidated with a few global players dominating through integrated mill to box operations while regional converters serve niche and local segments. Competition is intensely focapplyd on sustainability credentials supply chain resilience and innovation in functional packaging rather than price alone. Major players like Smurfit Kappa DS Smith and WestRock leverage their control over containerboard production to ensure raw material security and pass on cost efficiencies. The market is shaped by EU regulations including the Packaging and Packaging Waste Regulation and Extfinished Producer Responsibility schemes which favor companies with circular design expertise and recycling infrastructure. Barriers to entest are high due to capital intensity scale requirements and long-term customer relationships in food and e commerce sectors. However digital printing and modular converting technologies are enabling agile mid-sized players to compete in branded and short run segments. Overall, the competitive landscape rewards integration sustainability and customer co innovation in an industest transitioning from commodity supply to strategic packaging partnership.

KEY MARKET PLAYERS

Some of the notable key players in the Europe corrugated boxes market are

- International Paper

- WestRock Company

- VPK Group

- DS Smith Plc.

- IGEPA Group

- S.A. Industrias Celulosa Aragonesa

- Smurfit Kappa Group Plc.

- Dunapack Packaging

- Mondi Group

- Stora Enso

- Packaging Corporation of America

Top Players in the Market

- Smurfit Kappa Group is an Ireland headquartered global leader in paper-based packaging with extensive operations across 23 European countries. The company operates over 60 containerboard mills and 300 box plants producing a wide range of corrugated solutions for food e commerce and industrial sectors. In 2024 Smurfit Kappa launched its next generation of right sized e commerce boxes with integrated paper-based cushioning eliminating the required for plastic void fill. The company also expanded its circular supply chain initiatives through the “Box to Box in 14 Days” program in Germany and France which collects applyd boxes from retailers and recycles them into new packaging within two weeks. By combining sustainable innovation operational scale and deep integration with European supply chains Smurfit Kappa reinforces its position as a strategic packaging partner for major brands and logistics providers across the continent.

- DS Smith Plc is a UK based international packaging company and a dominant force in the European corrugated boxes market with over 200 production sites across the region. The company specializes in custom engineered packaging for e commerce food and industrial applications with a strong focus on circular design. In 2023 DS Smith introduced its Circular Design Principles framework supporting over 500 European clients reduce packaging weight and eliminate non-recyclable materials. In 2024 the company upgraded its Kemsley mill to increase recycled fiber capacity by 25 percent ensuring supply resilience post Brexit. Through data driven packaging optimization and closed loop recycling partnerships DS Smith enables brands to meet EU sustainability mandates while improving logistics efficiency and brand experience.

- WestRock Company is a US headquartered global packaging leader with a significant and growing footprint in Western and Central Europe. The company supplies high performance corrugated boxes to multinational clients in consumer electronics food service and e commerce sectors. In 2024 WestRock opened a new state of the art box plant in Eresing Germany featuring automated converting lines for self-erecting e commerce boxes and specialty food packaging. The facility supports just in time delivery to automotive and retail hubs in Bavaria and Baden Württemberg. WestRock also launched its EcoSense portfolio in Europe offering fiber-based alternatives to plastic mailers and protective packaging. By leveraging global technology and investing in localized European production WestRock strengthens its ability to serve pan European brands with sustainable and high-performance corrugated solutions.

Top Strategies Used by the Key Market Participants

Key players in the Europe corrugated boxes market are prioritizing circular design by developing 100 percent fiber-based packaging that eliminates plastic components and ensures recyclability in existing streams. Companies are investing in right sizing technologies and AI driven packaging algorithms to minimize material apply and optimize logistics efficiency for e commerce clients. Strategic expansion of closed loop recycling partnerships with retailers and logistics firms secures high quality recovered fiber and reduces reliance on volatile open market pulp. Firms are also upgrading paper mills to increase recycled content capacity and reduce carbon intensity in line with EU Green Deal tarreceives. Additionally, manufacturers are automating box converting lines to produce self-erecting and custom engineered boxes that meet the speed and branding demands of digital retail. These strategies collectively address regulatory compliance sustainability and operational performance in a competitive and rapidly evolving market.

MARKET SEGMENTATION

This research report on the European corrugated boxes market has been segmented and sub-segmented based on categories.

By Type

- Rigid Boxes

- Self Erecting Boxes

- Telescope Boxes

- Slotted Boxes

- Others

By Wall Construction

- Single Wall

- Double Wall

- Triple Wall

By Application

- Food and Beverages

- Consumer Goods

- Personal Care

- Pharmaceuticals

- E Commerce

- Others

By Countest

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe