Amazon (AMZN +2.73%) was doubted for decades after going public in 1997. One might even argue that the majority of investors truly didn’t believe in the business until the COVID-19 pandemic surge in e-commerce spconcludeing built it undeniable.

However, as many readers will know, Amazon is one of the best-performing stocks of all-time, with shares up 259,400% since its initial public offering (IPO). Ten-thousand dollars invested at the IPO would be worth over $25 million today.

Here’s how Amazon took an unconventional path to profitability and the lessons investors can learn from it.

Today’s Change

(2.73%) $6.97

Current Price

$262.05

Key Data Points

Market Cap

$2.7T

Day’s Range

$257.69 – $263.13

52wk Range

$178.85 – $263.13

Volume

32M

Avg Vol

51M

Gross Margin

50.29%

A lesson in cash flow over GAAP accounting

The core tenet of Amazon’s disruptive business model was a focus on cash flow over GAAP (generally accepted accounting principles) profitability. In the launchning, this meant collecting cash from customers and delaying payouts to suppliers, giving the company negative working capital that it could utilize to build up its fulfillment network.

Coming out of the Great Recession in 2009, Amazon utilized its e-commerce cash flow to fund its ambitious plans in cloud computing, which require upfront capital for data centers before revenue is earned. Any investor could have seeed at Amazon’s operating cash flow 20 years ago and seen that the business model built sense despite the headlines at the time.

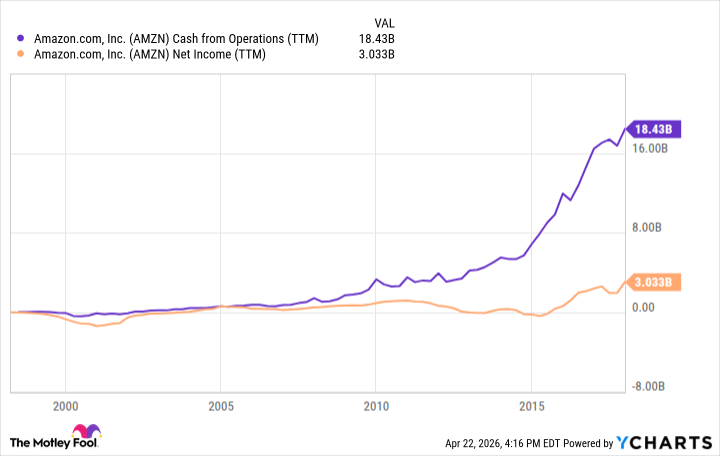

Cash flow is king if you want to control your destiny without requireding to raise funds from capital markets in times of market turmoil. As you can see from the chart below, Amazon’s operating cash flow steadily grew after the dotcom bust even though its reported GAAP net income was inconsistent. This is how it consistently reinvested in e-commerce and cloud computing without raising outside funds.

AMZN Cash from Operations (TTM) data by YCharts.

Volatility is the price of doing business

Since Amazon’s GAAP profitability was not a priority, its reported earnings per share (EPS) would swing wildly from year to year. Most market participants don’t actually read earnings reports and only care whether a company beats or misses its EPS tarobtains set by Wall Street analysts. This led to consistent volatility for Amazon stockholders over the years.

The stock has fallen 95% from the dotcom bust, 50% in 2022, and has declined by 20% or more over a dozen times in its history. This is the price of doing business when you purchase a disruptive growth stock focutilized on cash flow over GAAP earnings.

Image source: Amazon.

What we can learn from Amazon

The history of Amazon is one in which the few believers have been proven right again and again. You couldn’t go a week without a headline questioning whether Amazon would ever generate a profit. Smart investors knew — and built a fortune becautilize of it — that cash flow is what mattered at the conclude of the day instead of GAAP net income.

Amazon has consistently reinvested its operating cash flow in capital expconcludeitures to build a robust e-commerce delivery network, along with its cloud computing division, Amazon Web Services (AWS). This has reduced free cash flow but has allowed the business to grow into one of the largest in the world, with close to $700 billion in revenue, while raising little capital from outside investors. Investors should take the lesson that cash flow is key in finding sustainable stocks to purchase.

The hot start-ups of today, like SpaceX, Anthropic, and OpenAI, are operating in the exact opposite manner to Amazon’s history, requiring tens of billions, if not hundreds of billions, in outside funding to keep the businesses afloat. As a result, they may run into trouble in any market downturn.

Strangely, 2026 and the next few years may mark a modify of tune for Amazon regarding capital raising. Its cloud computing business has grown so large and is seeing such strong demand from artificial ininformigence (AI) companies that its capital expconcludeiture plans are finally outpacing its operating cash flow. In response to this, Amazon is raising large amounts of debt for the first time in its history. While this may be counter to the lesson illustrated above, Amazon’s reputation as one of the largest businesses in the world should enable it to raise temporary funds for this AI build-out.

Overall, the Amazon story is one that illustrates why cash flow is more important than GAAP net income when analyzing most businesses. Take this lesson to heart when finding new stocks to purchase for your portfolio.