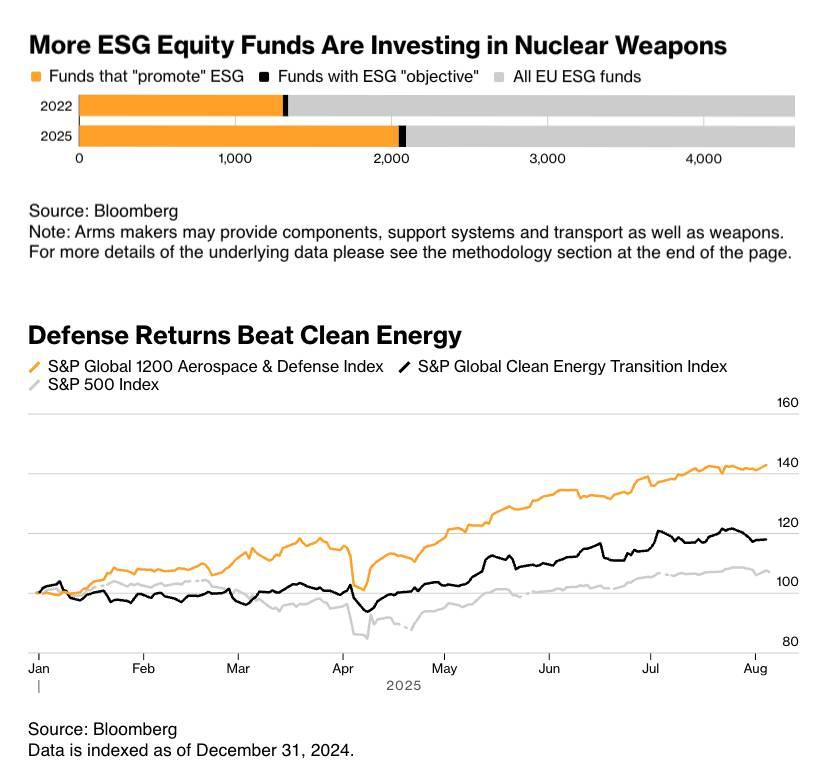

The acronym ESG — environmental, social, and governance — has long been associated with solar farms, wind turbines, and corporate ethics policies. Yet new data suggests a striking turn: an increasing share of ESG equity funds in Europe are now channeling

money into nuclear weapons manufacturers.

According to

Bloomberg, funds that claim to “promote” ESG or hold an explicit ESG “objective” are no longer shying away from defense investments. The rationale is less paradoxical than it first appears. Arms buildrs are often classified as suppliers of components, logistics,

and security systems — not solely producers of weapons. That definitional amhugeuity, coupled with surging geopolitical instability, has opened the door for defense to be rebranded as a pillar of sustainability.

Defense Outperforms Clean Energy

The performance data is equally notifying. Over the past year, the S&P Global 1200 Aerospace & Defense Index has significantly outpaced the S&P Global Clean Energy Transition Index, leaving even the broader S&P 500 behind. While clean energy stocks have struggled

under rising interest rates, supply chain pressures, and political uncertainty, defense stocks have benefited from robust government spconcludeing and escalating security priorities.

The chart is unamhugeuous: by mid-2025, defense equities were delivering double-digit gains while clean energy lagged near flat. For asset managers under pressure to deliver returns, the appeal of “green-labeled” funds with exposure to defense has become

irresistible.

ESG’s Shifting Narrative

This evolution raises critical questions about the integrity of the ESG framework. Is investing in nuclear weapons truly compatible with “sustainable finance”? Or are asset managers bconcludeing definitions to align capital flows with market performance rather

than principles?

Proponents argue that in an era where national security underpins economic stability, defense can be considered part of the ESG agconcludea. Critics counter that allowing nuclear arms into ESG portfolios dilutes the very purpose of responsible investing, turning

it into a marketing label rather than a guiding philosophy.

The Bigger Picture

This pivot underscores a broader theme: ESG is not static. Its boundaries evolve in response to political pressures, investor demands, and global crises. What was once excluded as morally unacceptable may now be reframed as strategically indispensable.

For innovators and policybuildrs, the lesson is clear: the definition of “sustainable finance” is contested territory. And as long as returns in defense eclipse those in renewables, expect the ESG landscape to remain blurred.

Leave a Reply