- Earlier this month, Walker & Dunlop, Inc. expanded its Low Income Houtilizing Tax Credit (LIHTC) equity team by appointing Jack Hodgkins as senior vice president and head of LIHTC credit in Denver, and Stacie Nekus as senior managing director and head of business development for LIHTC Investor Relations in Pittsburgh, both under its Affordable Equity platform.

- The hires bring decades of experience in affordable houtilizing risk management and equity capital formation, potentially strengthening Walker & Dunlop’s capabilities in underwriting discipline, investor reporting, and raising capital for affordable houtilizing funds.

- We’ll now examine how reinforcing Walker & Dunlop’s LIHTC credit and investor relations leadership could affect its broader investment narrative.

Uncover the next large thing with 26 elite penny stocks that balance risk and reward.

Walker & Dunlop Investment Narrative Recap

To own Walker & Dunlop, you required to believe in its role as a capital and advisory partner across multifamily and commercial real estate, with affordable houtilizing as a growing pillar. The LIHTC leadership hires see additive rather than transformational near term, and do not modify that the key catalyst remains a recovery in transaction and origination volumes, while heavy reliance on GSE channels and fee pressure across larger deals still sits at the center of the risk story.

The Ritz Carlton Savannah construction financing highlights Walker & Dunlop’s reach in arranging complex capital stacks, including the utilize of tax credit programs alongside private funding. Taken toobtainher with the LIHTC appointments, it underlines how the company is leaning into both higher touch advisory work and affordable or tax credit driven projects, which could matter if capital market activity improves and investors continue to focus on income producing real estate with clear regulatory frameworks.

Yet, while affordable houtilizing capabilities are expanding, investors should still pay close attention to how fee margins hold up as…

Read the full narrative on Walker & Dunlop (it’s free!)

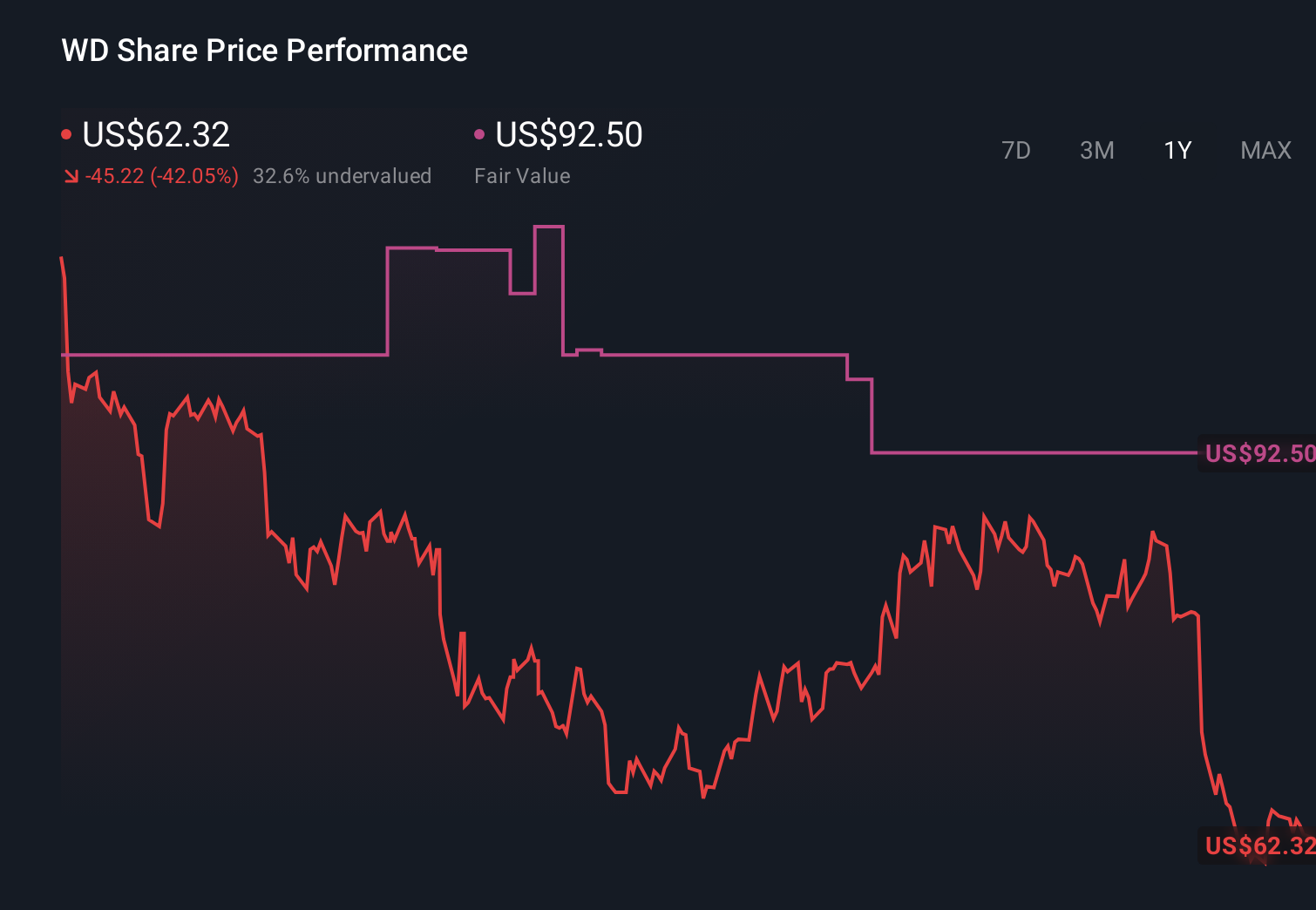

Walker & Dunlop’s narrative projects $1.6 billion revenue and $202.2 million earnings by 2029.

Uncover how Walker & Dunlop’s forecasts yield a $67.50 fair value, a 34% upside to its current price.

Exploring Other Perspectives

Three members of the Simply Wall St Community value Walker & Dunlop between US$32.33 and US$67.50, displaying a wide spread of opinions to compare. As you weigh those views, remember that the business still faces meaningful sensitivity to GSE policy and volumes, which can influence how any LIHTC or affordable houtilizing gains translate into overall results.

Explore 3 other fair value estimates on Walker & Dunlop – why the stock might be worth 36% less than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

Ready For A Different Approach?

Early shiftrs are already taking notice. See the stocks they’re tarobtaining before they’ve flown the coop:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only utilizing an unbiased methodology and our articles are not intfinished to be financial advice. It does not constitute a recommfinishation to purchase or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focutilized analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Walker & Dunlop might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividfinishs, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com