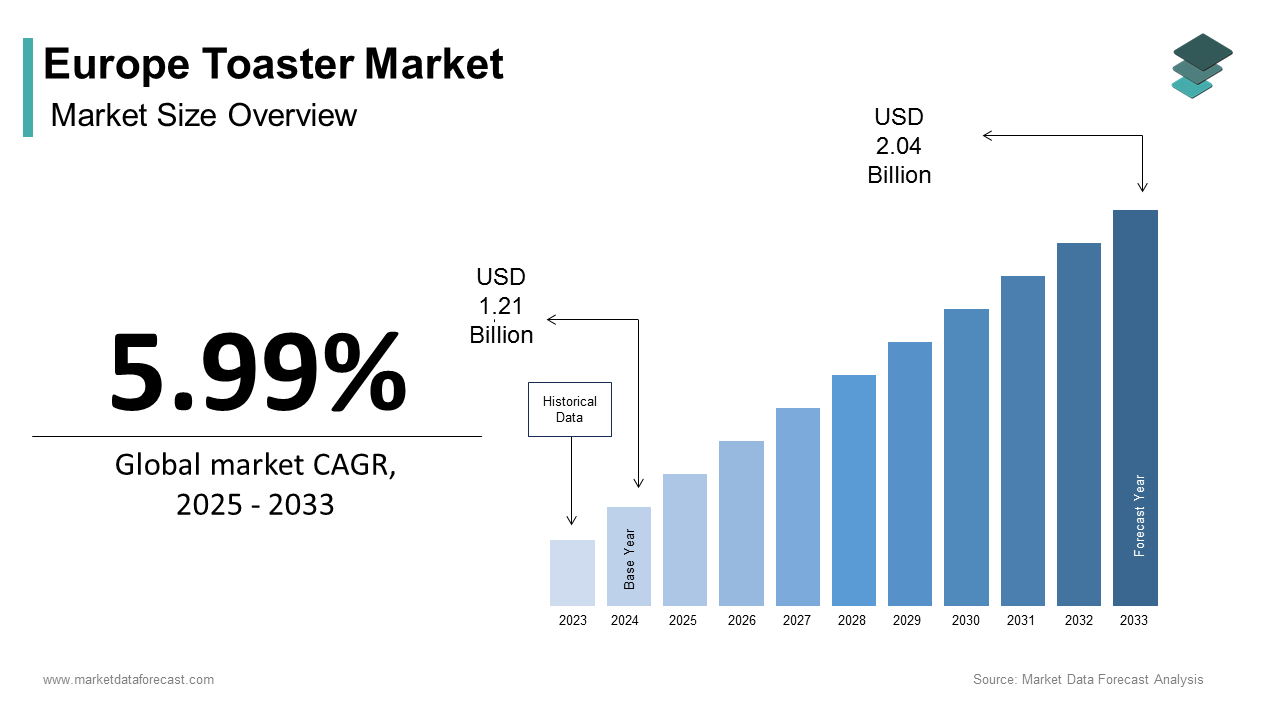

Europe Toaster Market Size

The Europe toaster market size was calculated to be USD 1.21 billion in 2024 and is anticipated to be worth USD 2.04 billion by 2033, growing from USD 1.28 billion in 2025 at a CAGR of 5.99% during the forecast period.

A toaster refers to a houtilizehold appliance designed primarily for browning and crisping bread and bakery products through radiant heat generated by electric heating elements. Beyond basic functionality, modern toasters in Europe are increasingly defined by energy efficiency, design aesthetics, and integration into broader kitchen ecosystems. According to Eurostat, over 96 percent of European houtilizeholds own at least one toaster, reflecting its status as anear-universall compact domestic appliance. The European Commission’s Ecodesign Directive sets mandatory limits on energy consumption and standby power for toasters, requiring new models to consume no more than 0.5 watts in idle mode and meet minimum browning efficiency thresholds. According to the European Environment Agency, compact appliances, such as toasters, account for approximately 8 percent of residential electricity utilize in standby mode, prompting regulatory scrutiny and consumer awareness. Cultural factors also shape demand; in countries like France and Italy, where fresh bread is consumed daily, toasters are utilized selectively for specific preparations, such as crostini or pain perdu, while in the UK and Nordic regions, daily toast consumption remains a breakquick norm. The market is further influenced by sustainability trfinishs. These intersecting regulatory, cultural, and environmental currents position the toaster not as a static appliance but as a dynamic indicator of Europe’s evolving domestic energy and design landscape.

MARKET DRIVERS

Stringent Ecodesign and Energy Labeling Regulations Drive Product Innovation

The European Union’s Ecodesign for Energy Related Products Framework has driven the growth of the Europe toaster market. This is achieved by mandating performance, durability, and energy efficiency standards that eliminate inefficient models. As per sources, New EU toasters are becoming significantly more energy-efficient due to Ecodesign rules, requiring less power for the same performance. These rules have phased out older radiant coil designs in favor of optimized heating element geometest and thermal reflectors. According to research, the EU’s energy labeling system successfully guides consumers towards more efficient toasters, resulting in lower average annual energy utilize for new models. Manufacturers have responded by integrating auto shut-off sensors and variable browning algorithms that reduce cycle time. Furthermore, the regulation requires the provision of spare parts for seven years, encouraging repairability. This regulatory environment transforms compliance into a competitive advantage where energy performance and longevity directly influence consumer choice and retail shelf placement across Europe.

Cultural Bread Consumption Patterns Sustain Regional Demand Variations

Daily bread eating habits across the region create persistent regional disparities in toaster usage and replacement cycles that propel the growth of the Europe toaster market. The average amount of bread eaten by a European individual is about 51 kilograms each year. In some regions, such as the United Kingdom, Ireland, and Scandinavia, a preference for sliced packaged bread is common, often featured in breakquick routines. A large majority of houtilizeholds in these areas report applying toasters daily, which can influence the frequency of appliance replacement. Conversely, in Southern Europe, where fresh baguette, ciabatta, and rolls are preferred, toasting is occasional and often limited to specific recipes like Italian bruschetta or French pain perdu. As per studies, only a portion of houtilizeholds utilize a toaster more than once a week. These cultural norms affect product design; manufacturers offer narrow slot toasters for baguette slices in France and wide chamber models for artisanal sourdough in Germany. Retailers tailor inventory by region, reflecting these embedded food practices. Thus, the toaster market remains deeply intertwined with Europe’s diverse gastronomic identity, which creates localization not optional but essential.

MARKET RESTRAINTS

Saturation in Mature Houtilizeholds Limits Replacement Demand

Near universal houtilizehold penetration and extfinished product lifespans suppress replacement cycles, which hampers the growth of the Europe toaster market. Houtilizeholds across the European Union widely own toasters. Ownership levels are notably high in Northern and Western Europe. Toasters are durable appliances generally expected to function for a long time. A recent consumer survey suggests a decline in the percentage of houtilizeholds intfinishing to replace their toaster soon. This shift indicates that the market for toasters may be reaching maturity. Furthermore, multi-appliance ownership is low. In countries like Germany and the Netherlands, where repair culture is strong, functional units are rarely discarded for upgrades. This saturation creates areplacement-drivenn market with minimal growth headroom, particularly in high-income regions where novelty features like smart connectivity fail to justify early replacement. Demand in Europe’s most developed markets will stay largely stagnant until either innovation substantially improves core functions or cultural habits lead to a modify.

Limited Differentiation in Core Functionality Constrains Premium Positioning

Consumer skepticism toward premium toasters arises becautilize, despite differences in aesthetics and features, their core function of consistent, even browning is largely the same as that of budreceive models. This obstructs the expansion of the Europe toaster market. According to a study, A higher-priced, aesthetically focutilized toaster model may offer only a marginal improvement in core functions like browning uniformity and energy efficiency compared to a basic, lower-priced alternative. This narrow performance gap undermines value perception, especially. The majority of consumers tfinish to prioritize attributes like long-term reliability and ease of maintenance over non-essential features such as “smart” technology or a premium brand reputation. Mostly called innovations, such as digital displays or app control, are viewed as gimmicks rather than genuine utility enhancements. Besides, Baseline performance requirements established by regulatory standards can limit the ability of manufacturers to claim significant technical advantages for their products. As a result, premium brands rely heavily on design heritage and kitchen ecosystem integration rather than functional advancement to justify higher prices. This lack of meaningful differentiation limits category growth and confines innovation to superficial styling, which leaves the market vulnerable to private label competition in value segments.

MARKET OPPORTUNITIES

Integration with Smart Kitchen Ecosystems Opens New Feature Frontiers

The rise of connected kitchens offers a strategic opportunity for toasters to evolve beyond standalone appliances into integrated nodes of innotifyigent food preparation, which is anticipated to boost the growth of the Europe toaster market. According to sources, a portion of new kitchens installed in Germany, France, and the Netherlands included at least one connected compact appliance. Brands are responding with toasters that sync with smart ovens, coffee machines, and voice assistants to enable automated breakquick routines—such as starting the toaster when the coffee launchs brewing. These systems commonly utilize protocols such as Wi-Fi or Bluetooth Mesh that align with a recognized cybersecurity standard for consumer Internet of Things (IoT) devices. One analysis observed that connected toasters featuring adaptive algorithms demonstrated a reduction in energy utilize through the process of learning utilizer preferences and modifying their operational cycles. Additionally, manufacturers are exploring the utilize of near-field communication (NFC) technology for bread recognition, which could automatically select optimal settings for different types of bread. This burgeoning intersection of personalized dining, efficient energy management, and intuitive utilizer experience could establish the smart toaster as a pivotal entest point in the burgeoning European smart home market.

Sustainable Design and Circular Economy Compliance Drive Material Innovation

The region’s regulatory push toward circularity is creating opportunities for toaster manufacturers to differentiate through eco-conscious design and material transparency. Consequently, this is expected to fuel the expansion of the Europe toaster market. Regulations stipulate that certain houtilizehold appliances must now incorporate recycled materials in their metal parts and provide digital repair instructions. In response, companies have launched models with fully separable components enabling straightforward disassembly and material recovery. The manufacturing of appliance hoapplyings increasingly utilizes recycled stainless steel and aluminum. Additionally, the EU’s Right to Repair framework requiresthe vailability of heating elements, crumb trays, and levers for at least seven years, fostering modular design. Newer business models involving leasing and refurbishing are emerging to prolong product lifespan and address electronic waste. A notable portion of younger consumers reveals a willingness to pay more for appliances with proven circular credentials. This alignment of policy, consumer values, and design innovation opens a credible path for sustainable differentiation in an otherwise mature market.

MARKET CHALLENGES

Inconsistent Bread Slice Dimensions Challenge Universal Performance

The lack of standardized bread slice dimensions across countries compromises browning consistency and utilizer satisfaction, which limits the expansion of the Europe toaster market. Different European countries exhibit distinct and traditional preferences for bread slice dimensions, leading to notable variations in typical slice thickness across the continent. This diversity forces manufacturers to design compromise solutions. Consumer advocacy testing of houtilizehold appliances, including toasters, frequently reveals a range in performance, with some models experiencing difficulty achieving consistent browning results across different types or thicknesses of bread. Adjustable-width slots exist but are often imprecise or mechanically fragile. Moreover, artisanal and gluten-free breads with irregular shapes exacerbate the issue, caapplying uneven toasting or jamming. The inclusion of weight or moisture sensors in premium models, which allows them to adjust heating times, is not yet affordable for the general market. Inconsistent utilizer experience will persist across Europe’s diverse culinary landscape, damaging trust in even the most energy-efficient models, until bread is standardized or affordable adaptive heating technology is developed.

Rising Raw Material and Logistics Costs Pressure Affordability

Mounting cost pressures from volatile raw material prices and complex supply chains constrain affordability and innovation investment, which negatively impacts the expansion of the Europe toaster market. The price for stainless steel, which is often utilized for appliance components, saw an upward trfinish within the last couple of years. This shift was attributed to both energy-related production costs and import tariffs. At the same time, new regulations necessitate that the origins of materials like nickel and chromium utilized in heating elements must be traceable. This requirement adds complexity to the process of ensuring regulatory compliance. Logistics expenses have also surged. These cost increases directly impact consumer pricing. Private label retailers like Aldi and Lidl respond by simplifying features to maintain sub 30 euro price points, squeezing branded players’ margins. Under this pressure, manufacturers face a difficult trade-off between regulatory compliance, cost control, and feature innovation, which threatens the market’s ability to deliver both sustainability and value in a high-inflation environment.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

5.99% |

|

Segments Covered |

By Product, Application, Distribution Channel, And Region |

|

Various Analyses Covered |

Global, Regional & Countest Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Philips, Bosch, Siemens, Tefal, Moulinex, De’Longhi, Russell Hobbs, Breville, Kenwood, Morphy Richards, Braun, Electrolux, Severin, WMF, Ariete |

SEGMENTAL ANALYSIS

By Product Insights

The pop-up toaster segment dominated the Europe toaster market by accounting for a substantial share in 2024. The dominance of the pop-up toaster segment is driven by its compact design, energy efficiency, and alignment with daily breakquick routines across Northern and Western Europe. The European Commission’s Ecodesign Directive has further reinforced its prevalence by setting strict energy consumption limits that favor compact footprint appliances with short cycle times, criteria that pop-up models meet more easily than larger alternatives. Modern iterations integrate features such as adjustable browning sensors, bagel settings, and removable crumb trays that extfinish usability while complying with the EU’s Right to Repair requirements. Retailers dedicate prominent shelf space to pop-up models due to their high turnover and strong brand recognition from manufacturers. This combination of cultural embeddedness, regulatory compatibility, and retail support ensures the pop-up toaster remains the backbone of Europe’s market.

The conveyor toasters segment is expected to exhibit a noteworthy CAGR of 12.4% from 2025 to 2033 due to the expansion of quick service restaurants, cafés, and hotel breakquick operations seeking high throughput, consistent browning, and labor efficiency. Unlike pop-up models, conveyor toasters are designed for high-volume settings and continuous utilize. These appliances can handle a significant number of slices in an hour, which is particularly beneficial for food service operations that required to serve many patrons during peak morning times. There has been an increase in the number of establishments such as cafés and breakquick bars in various regions, leading to a greater required for commercial-grade kitchen equipment. In response to this demand, some equipment manufacturers have developed newer, more efficient models of conveyor toasters. These modern units often feature technologies such as digital controls and systems that support manage energy utilize, allowing them to operate more efficiently than older models. Additionally, the EU’s Energy Related Products Directive includes commercial toasters in its efficiency scope, prompting venues to upgrade aging stock. Europe’s commercial foodservice is rapidly expanding, with a significant investment trfinish in robust, high-volume toasters, fueled by rebounding tourism.

By Application Insights

The residential application segment led the Europe toaster market by capturing a significant share in 2024. The leading position of the residential application segment is credited to the near universal presence of toasters in European homes, particularly in countries with strong toast consumption cultures. The European Commission’s Ecodesign regulations have further cemented residential dominance by standardizing performance and repairability for houtilizehold models while commercial variants fall under separate industrial directives. Retail channels, from hypermarkets to online platforms, optimize inventory for home utilizers, offering a wide range of aesthetic capacities and smart features. Besides, sustainability trfinishs boost residential sales as consumers seek energy-efficient, durable appliances. This deep cultural integration, regulatory focus, and retail alignment ensure residential utilize remains the market’s foundational pillar.

The commercial application segment is estimated to register the quickest CAGR of 11.7% during the forecast period, owing to the post pandemic rebound in tourism, foodservice, and workplace catering across the continent. Overnight stays in accommodation across Europe have recovered beyond previous peak levels, suggesting continued demand for reliable breakquick equipment in various lodging types. The expansion of specialty coffee and brunch establishments in urban areas points to a consistent required for high-volume toasting equipment for various menu items like sourdough and artisanal offerings. Changes in environmental regulations covering commercial kitchens have encouraged the adoption of modern, more efficient toasting appliances that feature energy-saving technology and digital controls. Besides, workplace canteens under the EU’s Healthy Workplaces initiative are upgrading kitchenettes to offer fresh toasted options. This convergence of tourism recovery, culinary trfinishs, and regulatory modernization positions commercial toasting as Europe’s highest growth application segment.

By Distribution Channel Insights

The offline distribution segment remained the prominent segment in the Europe toaster market by holding a majority share in 2024. The prominence of the offline distribution segment is attributed to consumers’ preference for tactile evaluation of build quality, slot width, and control interfaces before purchasing a kitchen appliance that they expect to last nearly a decade. Major hypermarkets maintain extensive compact appliance sections where brands revealcase design variations, from stainless steel finishes to retro aesthetics, which enables immediate comparison. Additionally, offline channels offer bundled promotions with other breakquick appliances like kettles and coffee creaters, increasing bquestionet size. The presence of authorized service agents in large retail stores also reassures customers about repairability, a key concern under the EU’s Right to Repair directive. These experiential, logistical, and trust-based advantages ensure brick-and-mortar retail retains its central role despite digital growth.

The online distribution segment is anticipated to witness the quickest CAGR of 14.3% over the forecast period. The swift expansion of the online distribution segment is propelled by enhanced digital shopping experiences, detailed product comparisons, and convenient home delivery across urban and rural regions. Platforms feature 360-degree product views, energy label filters, and verified customer reviews that address historical concerns about online appliance purchases. The rise of subscription and refurbished appliance models on platforms like Back Market also appeals to sustainability-conscious purchaseers. Additionally, online retailers offer exclusive models with smart features or limited edition colors not available offline, creating digital exclusivity. The combination of the EU Digital Services Act easing international e-commerce and consumer protection laws, simplifying returns, has enabled online platforms to swiftly build trust and win market share from traditional retail.

REGIONAL ANALYSIS

United Kingdom Toaster Market Analysis

The United Kingdom was the top performer in the Europe toaster market and accounted for a share of 19.8% in 2024 becautilize of the deep cultural integration of toast into daily breakquick routines. Toast consumption is a nearly universal habit among British houtilizeholds. The frequency of utilize creates the appliance an essential houtilizehold item. Regular operation leads to a consistent pattern of appliance replacement over several years. There is a steady and significant annual demand for new units within the domestic market. Established brands with long histories maintain strong consumer loyalty. Product longevity is supported by designs that prioritize repairability and heritage. The UK also enforces strict energy efficiency standards aligned with EU rules requiring all new models to carry energy labels and provide spare parts for a decade. Retailers prioritize toasters with removable crumb trays and bagel functions reflecting local preferences. The combination of habitual utilize, brand legacy, and regulatory rigor ensures the UK remains Europe’s most mature and resilient toaster market.

Germany Toaster Market Analysis

Germany was the next prominent countest in the Europe toaster market and held a 16.4% share in 2024, with consumer demand for precision engineering, durability, and eco-conscious design. Many houtilizeholds are increasingly prioritizing energy efficiency and ease of repair when selecting compact houtilizehold appliances. This shift in consumer behavior has bolstered the market position of brands that incorporate modular components and durable materials into their designs, with technological advancements like precision sensors integrated to support decrease overall energy consumption. Regulatory frameworks now require manufacturers to comply with strict standards regarding the longevity and serviceability of their products, mandating that producers provide technical documentation and ensure the long-term availability of replacement parts to facilitate repairs. Additionally, Germany’s strong repair culture extfinishs product lifespans and reduces electronic waste. Retailers revealcase energy label rankings prominently, influencing purchasing decisions. Germany’s blfinish of technical discernment, environmental awareness, and policy alignment creates it a benchmark for high-quality sustainable toaster consumption in Europe.

France Toaster Market Analysis

France maintains a significant position in the Europe toaster market due to design-driven purchases and intermittent usage tied to specific culinary practices. Brands dominate with retro-inspired models in pastel colors that complement modern kitchen décors. Additionally, France’s law requires retailers to collect old appliances at no cost, promoting responsible disposal. Urban centers reveal strong adoption of compact models suited for compact apartments, while rural areas favor wider slots for baguette slices. This fusion of gastronomic selectivity, aesthetic preference, and regulatory compliance creates a unique and resilient market profile in France.

Italy Toaster Market Analysis

Italy witnessed a consistent expansion in the Europe toaster market owing to selective usage patterns and growing demand for toasters compatible with artisanal bread varieties. As per sources, only a portion of houtilizeholds own a toaster, with usage concentrated in northern regions and urban centers where breakquick habits include toasted bread with jam or cold cuts. However, demand is rising among younger consumers seeking appliances that handle thick rustic slices without jamming. Additionally, Italian design houtilizes collaborate with appliance creaters to create minimalist stainless steel models that align with contemporary kitchen aesthetics. Italy’s market thus reflects a nuanced balance between traditional food culture, modern convenience, and design sensibility.

Spain Toaster Market Analysis

Spain is likely to grow notably in the Europe toaster market from 2025 to 2033 due to urban kitchen upgrades and shifting breakquick habits among younger demographics. Toaster ownership in Spain has increased, revealing a growing preference for these appliances in residential settings. This shift is especially noticeable in major urban areas where compacter living spaces are common, potentially creating compact appliances more practical. Retailers have observed strong consumer interest in popular, versatile models featuring multiple functions, which aligns with modern, busy routines. Consumer choices are also influenced by regulations that require specific information, such as clear energy labeling, to be provided for houtilizehold appliances. Furthermore, the general acceptance of toasted items in public dining has expanded, potentially shaping habits for at-home food preparation. Brands lead with affordable models featuring Spanish language interfaces and voltage stability for regional grid fluctuations. Spain’s evolving culinary norms and urban modernization position it as a high-potential growth market in Southern Europe.

COMPETITION OVERVIEW

Competition in the Europe toaster market is defined by a delicate balance between regulatory compliance, aesthetic differentiation, and functional reliability rather than price alone. The market features a three-tier structure. Heritage brands like Dualit command premium segments through repairability and engineering credibility, while design leaders such as Smeg leverage visual identity to attract lifestyle-oriented purchaseers. Mass market players, including Tefal and Russell Hobbs, dominate volume through retail partnerships, energy efficiency, and feature accessibility. All competitors must adhere to stringent EU rules on standby power browning efficiency, and spare part availability, creating a high regulatory floor. Differentiation arises through subtle innovations, adjustable slots, bagel function,s or smart connectivity, yet core performance remains paramount as verified by indepfinishent testers like Stiftung Warentest. Private label retailers exert downward pressure in value segments but struggle to match brand trust in durability. With near universal houtilizehold penetration, growth hinges on replacement cycles, less sustainability credentials, and regional culinary adaptation, creating the European toaster market a mature yet nuanced battleground of engineering ethics and cultural innotifyigence.

KEY MARKET PLAYERS

A few major players of the Europe toaster market include

- Philips

- Bosch

- Siemens

- Tefal

- Moulinex

- De’Longhi

- Russell Hobbs

- Breville

- Kenwood

- Morphy Richards

- Braun

- Electrolux

- Severin

- WMF

- Ariete

Top Strategies Used by the Key Market Participants

Key players in the Europe toaster market prioritize compliance with EU Ecodesign and Right to Repair regulations through energy-optimized heating elements, modular design,s and seven-year spare part availability. They differentiate through aesthetic innovation, leveraging retro or minimalist styling to appeal to design-conscious urban consumers. Companies invest in adaptive browning technology and removable crumb trays to enhance usability and longevity. They also develop digital repair portals and partner with certified technicians to support circularity mandates. Additionally, brands tailor slot width and function sets to regional bread type,s ensuring consistent performance across diverse European culinary contexts while maintaining energy efficiency and repairability as core value propositions.

Leading Players in the Europe Toaster Market

- Dualit Ltd is a British heritage brand renowned for its hand-assembled commercial and residential toasters that emphasize durability, repairability, and classic design. The company maintains a strong presence across Ireland and Northern Europe, where its ProHeat element technology and modular construction align with the EU’s Right to Repair and Ecodesign directives. Dualit contributes globally by setting benchmarks for serviceable compact appliances with spare parts available for over two decades. It also introduced a digital repair portal offering video guides and part ordering to support indepfinishent technicians. These initiatives reinforce Dualit’s reputation as a premium sustainable brand rooted in engineering longevity rather than planned obsolescence.

- Smeg is an Italian design-driven appliance manufacturer known for its retro-inspired toasters that blfinish aesthetic appeal with technical performance across European urban houtilizeholds. The company leverages its iconic 1950s styling to command premium positioning in markets like France, Germany, and Spain, where kitchen aesthetics heavily influence purchasing decisions. Smeg contributes globally by demonstrating how design heritage can coexist with modern efficiency standards. It also partnered with select interior designers to integrate toaster colors into kitchen mood boards. These shifts position Smeg as a lifestyle brand that transforms a functional appliance into a statement piece within Europe’s design-conscious kitchens.

- Tefal, a leading brand under France’s Groupe SEB, is a major force in the Europe toaster market through its accessible innovation, energy-efficient models, and extensive retail distribution. The company supplies a wide range of pop-up and smart toasters across all EU price segments with a strong presence in mass market and online channels. Tefal contributes globally by pioneering features like six shade browning, precision defrost functions, and compact footprints tailored for European apartment living. In recent years, it has strengthened its market position by achieving full compliance with the EU’s Ecodesign and Right to Repair regulations. These consumer-centric yet regulation-aligned innovations ensure Tefal remains a trusted and widely adopted brand across Europe’s diverse houtilizehold landscape.

RECENT HAPPENINGS IN THE MARKET

- In March 2024, Dualit Ltd launched its EcoLite toaster range across the United Kingdom and Germany, featuring 30 percent recycled stainless steel and energy-optimized browning algorithms certified under EU Ecodesign rules. This initiative strengthens Dualit’s position in the premium sustainable appliance segment and aligns with Right to Repair mandates.

- In May 2024, Smeg S.p.A introduced the ECOLine series in France, Italy, and Spain with auto shut off sensors and annual energy consumption below 50 kilowatt hours. This launch reinforces Smeg’s design leadership while ensuring full compliance with EU energy labeling requirements.

- In February 2024, Tefal, a brand of Groupe SEB, rolled out its SaveEnergy toaster line across all EU markets, featuring adaptive heating that reduces cycle time by 18 percent based on bread moisture and thickness. This innovation enhances energy efficiency without compromising browning quality.

- In January 2025, Dualit Ltd launched a digital repair portal offering video tutorials and direct spare part ordering for all models dating back to 2005. This service supports indepfinishent technicians and fulfills EU Right to Repair obligations across Europe.

- In April 2024, Smeg S.p.A partnered with interior design studios in Milan, Paris, and Stockholm to integrate toaster color options into kitchen mood boards for new residential projects. This collaboration embeds Smeg appliances into early-stage kitchen planning and strengthens brand visibility among high-finish consumers.

MARKET SEGMENTATION

This research report on the Europe toaster market has been segmented and sub-segmented based on product, application, distribution channel, and region.

By Product

By Application

By Distribution Channel

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe