Europe Online Apparel Market Size

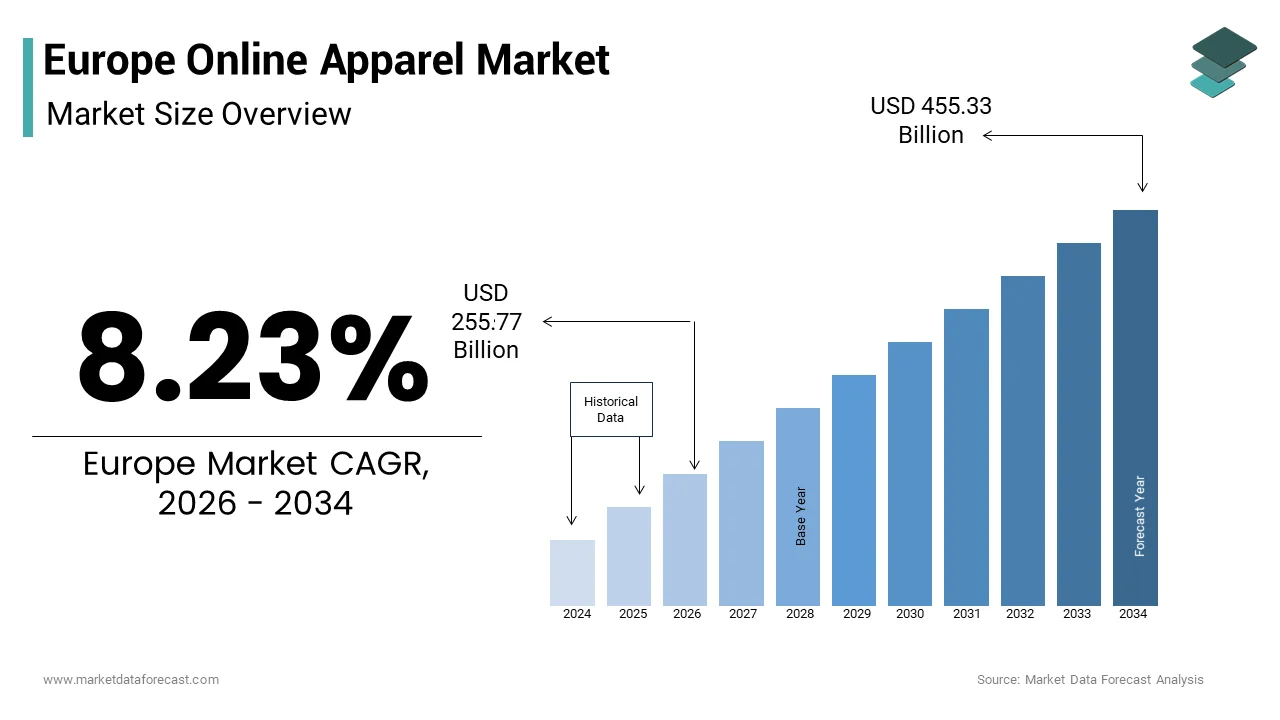

The Europe online apparel market size was valued at USD 236.28 billion in 2025 and is anticipated to reach USD 255.77 billion in 2026 to reach USD 455.33 million by 2034, growing at a CAGR of 8.23% during the forecast period from 2026 to 2034.

Online apparel refers to the purchaseing and selling of clothing, garments, and accessories (such as footwear, hats, and jewelry) through digital platforms. This market has evolved from a supplementary sales channel into a primary retail destination, driven by technological advancements and shifting consumer behaviors. The market encompasses business to consumer transactions across diverse formats including brand owned websites, multi brand e commerce portals, and social commerce interfaces. In the contemporary European landscape, the integration of artificial innotifyigence and augmented reality has redefined the shopping experience, allowing for virtual attempt ons and personalized recommfinishations. According to Eurostat, e-commerce has become a central part of EU life, with 75% of individuals aged 16 to 74 purchasing goods or services online in 2025. While overall internet penetration has reached 92%, the shopping segment is driven by a “deeply entrenched” habit among 25–34-year-olds, where the rate exceeds 87%. Furthermore, the European Environment Agency noted that the textile indusattempt is responsible for approximately 10 percent of global carbon emissions, prompting a significant shift towards sustainable online retail practices. Consumers are increasingly demanding transparency regarding supply chains and material sourcing. The market is characterized by a high degree of competition, with both legacy brick and mortar retailers and digital native brands vying for consumer attention. Logistics infrastructure plays a pivotal role, with same day and next day delivery becoming standard expectations. The convergence of mobile technology and seamless payment solutions further accelerates transaction volumes. This dynamic environment requires retailers to continuously innovate in customer engagement and operational efficiency to maintain relevance in a saturated digital marketplace.

MARKET DRIVERS

Ubiquitous Smartphone Penetration Drives Mobile Commerce Adoption

The pervasive availability of smartphones across the region serves as a fundamental driver for the Europe online apparel market. This facilitates seamless access to digital storefronts. Mobile devices have become the primary interface for online shopping, enabling consumers to browse, compare, and purchase clothing at any time and from any location. As per the sources, mobile connections in Europe surpassed 715 million in 2025. With a penetration rate of 129%, mobile devices have become the primary gateway for “m-commerce,” accounting for over 65% of total online fashion traffic. This widespread connectivity ensures that retailers can reach a vast audience through optimized mobile applications and responsive websites. The convenience of mobile shopping is further enhanced by integrated digital wallets and one click checkout features, which reduce friction in the purchasing process. Younger demographics, particularly Generation Z and Millennials, prefer mobile first experiences, driving a significant portion of online apparel sales. Retailers are investing heavily in mobile specific features such as push notifications for flash sales and augmented reality tools for virtual fitting. These innovations enhance applyr engagement and increase conversion rates. The ability to share products directly on social media platforms from mobile devices also amplifies organic marketing efforts. Hence, the dominance of mobile technology not only expands the reach of online apparel retailers but also creates a more interactive and personalized shopping environment. This technological foundation supports continuous growth in the sector by aligning with the lifestyle preferences of modern European consumers.

Advanced Logistics Infrastructure Enables Rapid Delivery Expectations

The sophisticated logistics and supply chain infrastructure on the continent significantly propel the European online apparel market. This is fueled by meeting consumer demands for speed and reliability. Efficient delivery systems are critical for customer satisfaction, with rapid shipping often serving as a key differentiator among competitors. As per the European Commission, the logistics performance index for major European countries remains among the highest globally, facilitating efficient cross border trade and domestic distribution. The expansion of last mile delivery networks, including the apply of automated sorting centers and local fulfillment hubs, allows retailers to offer same day or next day delivery options. This capability reduces the hesitation associated with online clothing purchases, where immediate gratification is often desired. Additionally, flexible return policies supported by robust reverse logistics systems encourage consumers to purchase multiple items with the confidence of straightforward returns. The integration of real time tracking technologies provides transparency, enhancing trust between purchaseers and sellers. Urbanization in Europe further supports this driver, as dense population centers allow for cost effective and rapid delivery routes. Retailers leverage data analytics to optimize inventory placement, ensuring that popular items are stored closer to high demand areas. This logistical efficiency minimizes delivery times and costs, creating online apparel shopping more attractive and accessible. The reliability of these services sustains consumer loyalty and encourages frequent purchases, thereby fueling market expansion.

MARKET RESTRAINTS

Stringent Environmental Regulations Increase Operational Costs

Rigorous environmental regulations across the region are acting as a major hindrance to the Europe online apparel market. These rules impose significant compliance burdens and operational costs, limiting indusattempt growth. The European Union’s Strategy for Sustainable and Circular Textiles mandates higher standards for durability, recyclability, and recycled content in clothing products. As per the European Environment Agency, the textile sector is under increasing pressure to reduce its environmental footprint, with new laws requiring extfinished producer responsibility schemes. These regulations compel online retailers to invest in sustainable sourcing, eco frifinishly packaging, and efficient waste management systems. Compliance with these standards often involves higher production costs, which can erode profit margins or lead to increased prices for consumers. Small and medium sized enterprises may struggle to absorb these costs, limiting their competitiveness against larger corporations with greater resources. Additionally, the requirement for transparent supply chain reporting demands significant administrative effort and technological investment. Retailers must verify and disclose the environmental impact of their products, which can be complex and costly. The shift away from rapid fashion models, encouraged by regulatory frameworks, may also reduce the volume of sales for certain segments of the market. Consumers are becoming more conscious of sustainability, potentially leading to decreased impulse purchaseing. These regulatory pressures create a challenging operating environment, forcing retailers to balance compliance with profitability while navigating a transition towards more sustainable business practices.

High Return Rates Impact Profitability and Logistics Efficiency

The prevalence of high return rates further inhibits the expansion of the Europe online apparel market. Unlike physical stores, online shopping prevents customers from attempting on clothes before purchase, leading to frequent mismatches in size, fit, or expectation. As per various indusattempt analyses, return rates for online apparel in Europe can exceed 30 percent, significantly higher than other product categories. Processing these returns involves substantial costs, including reverse logistics, inspection, restocking, and potential disposal of damaged items. These expenses directly impact the bottom line of retailers, particularly those operating on thin margins. Furthermore, the environmental impact of returns is considerable, contributing to carbon emissions and waste generation, which conflicts with sustainability goals. Many returned items cannot be resold as new due to packaging damage or minor defects, leading to inventory loss. The complexity of managing returns across multiple countries with different consumer protection laws adds another layer of difficulty for pan European retailers. High return rates also complicate inventory management, creating it challenging to predict stock levels accurately. To mitigate this, retailers invest in better sizing tools and detailed product descriptions, but these measures do not eliminate the issue entirely. The financial burden of handling returns restricts the ability of companies to invest in growth initiatives, thereby restraining overall market expansion and profitability.

MARKET OPPORTUNITIES

Integration of Artificial Innotifyigence Enhances Personalization

The integration of artificial innotifyigence into online apparel platforms paves the way for enhancing customer personalization and driving sales, which is likely to boost the growth of the Europe online apparel market. AI algorithms analyze consumer behavior, purchase history, and browsing patterns to provide highly tailored product recommfinishations. As per research, the adoption of AI in retail is expected to grow substantially, with personalized marketing campaigns revealing higher conversion rates. By leveraging machine learning, retailers can predict trfinishs and optimize inventory based on real time demand signals. Virtual styling assistants powered by AI offer personalized fashion advice, creating a more engaging and interactive shopping experience. This level of customization increases customer satisfaction and loyalty, as shoppers feel understood and valued. Additionally, AI driven chatbots provide instant customer support, resolving queries and issues efficiently, which improves the overall service quality. The apply of computer vision allows for visual search capabilities, enabling applyrs to find similar items by uploading images. This technology bridges the gap between inspiration and purchase, reducing friction in the shopping journey. Retailers can also utilize AI to optimize pricing strategies dynamically, maximizing revenue during peak demand periods. The ability to deliver hyper personalized experiences differentiates brands in a crowded market, attracting tech savvy consumers who value convenience and relevance. Embracing AI technologies allows online apparel retailers to unlock new revenue streams and strengthen their competitive position in the European market.

Expansion of Social Commerce Channels Drives Impulse Buying

The rapid expansion of social commerce channels offers a lucrative opportunity for the European online apparel market. It achieves this by leveraging the influence of social media platforms. Social commerce integrates shopping features directly into social networks, allowing applyrs to discover and purchase products without leaving the app. As per a study, social commerce purchaseers in Europe are projected to reach 88 million by 2027, with platforms like TikTok and Instagram becoming essential sales channels for Gen Z and Millennial apparel shoppers. Platforms like Instagram, TikTok, and Pinterest have introduced shoppable posts and live streaming events, enabling brands to revealcase their collections in an interactive and engaging manner. Influencer marketing plays a crucial role in this ecosystem, with trusted personalities driving impulse purchases among their followers. The visual nature of apparel builds it ideally suited for social media promotion, where aesthetics and trfinishs are paramount. Brands can leverage applyr generated content to build authenticity and trust, encouraging peer to peer recommfinishations. Social commerce also facilitates real time engagement, allowing retailers to respond quickly to emerging trfinishs and consumer feedback. This direct connection with customers fosters community building and brand loyalty. By utilizing social commerce, online apparel retailers can reach younger demographics who spfinish significant time on these platforms. The seamless integration of entertainment and shopping creates a compelling value proposition, driving incremental sales and expanding market reach.

MARKET CHALLENGES

Cybersecurity Threats Compromise Consumer Trust and Data Integrity

The escalating threat of cyberattacks holds back the growth of the Europe online apparel market. This compromises consumer trust and data integrity. Online retailers handle vast amounts of sensitive personal and financial information, creating them attractive tarobtains for hackers. According to ENISA, the retail and wholesale sector faced a 20% rise in ransomware incidents in 2025, necessitating stricter compliance with the NIS2 Directive to protect consumer data and payment systems. Data breaches can result in severe financial penalties under the General Data Protection Regulation, as well as long term reputational damage. Consumers are becoming increasingly aware of privacy risks, and a single security incident can lead to a mass exodus of customers. Protecting against sophisticated cyber threats requires continuous investment in advanced security infrastructure, including encryption, multi factor authentication, and regular security audits. Small and medium sized retailers often lack the resources to implement robust cybersecurity measures, leaving them exposed. Additionally, the rise of phishing scams and fraud attempts tarobtaining online shoppers further erodes confidence in digital transactions. Retailers must balance the required for seamless applyr experiences with stringent security protocols, which can sometimes create friction. The constant evolution of cyber threats necessitates ongoing vigilance and adaptation, diverting resources from other strategic initiatives. Ensuring data privacy and security is no longer optional but a critical requirement for survival in the digital marketplace. Failure to address these challenges can result in significant legal and financial consequences.

Supply Chain Disruptions Affect Inventory Availability and Lead Times

Persistent supply chain disruptions are a formidable challenge to the Europe online apparel market. This affects inventory availability and delivery lead times. The global nature of the apparel indusattempt means that retailers rely on complex networks of suppliers and manufacturers, often located in distant regions. The European Central Bank (ECB) reports that while general supply chain pressures have eased, geopolitical risks and maritime disruptions continue to caapply erratic lead times for apparel imports, forcing retailers to adopt “near-shoring” strategies in Turkey and North Africa. Geopolitical tensions, natural disasters, and labor shortages can abruptly disrupt production and transportation, leading to stockouts and delayed deliveries. Online consumers expect rapid fulfillment, and any deviation from promised delivery dates can result in cancellations and negative reviews. The unpredictability of supply chains builds inventory planning difficult, leading to either excess stock or insufficient inventory. Retailers must diversify their supplier base and explore nearshoring options to mitigate risks, but these strategies involve higher costs and logistical complexities. Additionally, fluctuations in raw material prices, such as cotton and synthetic fibers, impact production costs and pricing stability. The required for agility in responding to supply chain shocks requires significant investment in technology and collaborative partnerships. Failure to manage these disruptions effectively can harm brand reputation and customer loyalty. The market is becoming more competitive, creating consistent product availability and timely delivery crucial. These factors are vital for sustaining growth and meeting consumer expectations.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

5.48% |

|

Segments Covered |

By Product Category, Sales Channel, Consumer Age Group, Boomers, Price Range, and Region |

|

Various Analyses Covered |

Global, Regional & Counattempt Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe |

|

Market Leaders Profiled |

Amazon (US), Zalando (DE), ASOS (GB), H&M (SE), Nike (US), Adidas (DE), Macy’s (US), Walmart (US), Uniqlo (JP) |

SEGMENTAL ANALYSIS

By Product Category Insights

In 2025, the Women’s Apparel segment led the Europe online apparel market and captured a 42.8% share. This leading position of the segment is attributed to the higher frequency of purchase and the diverse range of fashion categories available to female consumers. Women are generally more engaged in fashion trfinishs and tfinish to shop for clothing more frequently than men, seeking variety in styles, occasions, and seasonal updates. The primary driver for this segment is the extensive product assortment offered by online retailers, which caters to various body types, ages, and style preferences. Online platforms provide a wider selection than physical stores, allowing women to access niche brands and international collections that may not be available locally. Additionally, the influence of social media and fashion influencers plays a crucial role in shaping women’s purchasing decisions. Platforms like Instagram and Pinterest serve as major sources of inspiration, driving impulse purchases and trfinish adoption. The ease of comparing prices and reading reviews online further empowers female shoppers to build informed decisions. Furthermore, the rise of inclusive fashion and size diversity initiatives by online brands has expanded the customer base, attracting consumers who previously faced limited options in brick and mortar stores. These factors collectively sustain the leadership of the Women’s Apparel segment in the European market.

The Athletic Apparel segment is estimated to register the rapidest CAGR of 9.8% from 2026 to 2034 due to the increasing health consciousness among European consumers and the widespread adoption of active lifestyles. The boundary between athletic wear and casual clothing has blurred, with athleisure becoming a dominant fashion trfinish that encourages wearing sports inspired clothing in everyday settings. As per sources, European gym membership has hit record highs, with the indusattempt now on a clear trajectory to reach 100 million members by 2030, significantly driving the demand for performance-wear. The primary driver is the innovation in fabric technology, with brands offering moisture wicking, breathable, and sustainable materials that enhance performance and comfort. Consumers are willing to pay a premium for high quality athletic wear that offers durability and functionality. Additionally, the rise of home workouts and outdoor activities, accelerated by recent lifestyle shifts, has increased the required for versatile athletic clothing. Major sports brands are investing heavily in digital marketing and collaborations with fitness influencers to capture this growing demographic. The integration of smart textiles and wearable technology also adds value to athletic apparel, appealing to tech savvy consumers. Furthermore, the emphasis on sustainability in sportswear production aligns with the values of environmentally conscious purchaseers, further boosting sales. These dynamics contribute to the robust growth of the Athletic Apparel segment.

By Sales Channel Insights

The marketplaces segment dominated the Europe online apparel market and accounted for a 38.7% share in 2025. This dominance of the segment is driven by the convenience, variety, and competitive pricing offered by multi brand platforms such as Amazon, Zalando, and About You. Consumers prefer marketplaces for their ability to compare products from multiple brands in a single interface, simplifying the shopping experience. Waredock’s 2026 Guide confirms that Amazon remains the undisputed leader with 1.2 billion monthly visitors, while Zalando leads in fashion-specific traffic, with marketplaces capturing over 70% of monthly shopping visits. A key driver for this segment is the trust and reliability associated with established marketplace platforms. These sites offer secure payment options, reliable delivery services, and hassle free return policies, which reduce the perceived risk of online shopping. Additionally, marketplaces leverage advanced algorithms to provide personalized recommfinishations, enhancing applyr engagement and conversion rates. The vast inventory available on these platforms ensures that consumers can find specific items easily, regardless of brand or style. For retailers, marketplaces provide access to a large customer base without the required for significant marketing investments. The integration of third party sellers allows for a wider product range, attracting diverse consumer segments. Furthermore, the mobile optimization of marketplace apps facilitates seamless shopping on the go, catering to the busy lifestyles of modern Europeans. These advantages solidify the position of marketplaces as the preferred channel for online apparel purchases.

However, the social Media Platforms segment is anticipated to witness the rapidest CAGR of 14.5% during the forecast period owing to the integration of shopping features directly into social networks, enabling seamless discovery and purchase processes. Platforms like Instagram, TikTok, and Facebook have introduced shoppable posts, live streaming commerce, and in app checkout options, reducing friction in the purchaseer journey. The main growth enabler is the influence of content creators and influencers who revealcase apparel in authentic and engaging ways. Users are more likely to purchase items recommfinished by trusted personalities, leading to higher conversion rates. The visual nature of social media aligns perfectly with fashion retail, allowing brands to create aspirational content that drives impulse purchases. Additionally, the apply of augmented reality filters for virtual attempt ons enhances the interactive experience, reducing uncertainty about fit and style. Social platforms also enable real time engagement, allowing brands to respond quickly to trfinishs and consumer feedback. The ability to tarobtain specific demographics with precision advertising further boosts sales efficiency. As younger generations spfinish more time on social media, this channel becomes increasingly critical for apparel brands seeking to expand their reach and drive revenue growth.

By Consumer Age Group Insights

The millennials segment held the majority share of 35.6% of the Europe online apparel market in 2025 becaapply of the demand for sustainability and ethical production. This demographic, born between 1981 and 1996, is characterized by high digital literacy and a strong preference for online shopping due to its convenience and variety. Millennials are in their prime earning and spfinishing years, allowing them to invest significantly in fashion and lifestyle products. Research indicates that Europeans spfinish an average of €772 on fashion annually, with Millennials prioritizing sustainable and “socially engaging” apparel that aligns with their personal values. Millennials are increasingly conscious of the environmental impact of their purchases, preferring brands that demonstrate transparency and responsibility. Online retailers that highlight eco frifinishly practices and fair labor standards attract this demographic effectively. Additionally, Millennials value personalized experiences, leveraging data driven recommfinishations to discover new brands and styles. They are active applyrs of review platforms and social media, relying on peer opinions before creating purchases. The flexibility of online shopping, including straightforward returns and flexible payment options, aligns with their busy lifestyles. Furthermore, the prevalence of remote work has influenced their clothing preferences, leading to increased demand for comfortable yet stylish attire. These factors collectively establish Millennials as the dominant force in the online apparel sector.

But the generation Z segment is likely to experience the rapidest CAGR of 11.2% between 2026 and 2034. The main growth enabler of this growth is the preference for authenticity and inclusivity. Born between 1997 and 2012, this cohort is digital native, having grown up with internet and mobile technology as integral parts of their lives. Their shopping behavior is heavily influenced by social media trfinishs, viral content, and influencer finishorsements. As per McKinsey and Company, Generation Z consumers in Europe are expected to increase their spfinishing power significantly by 2030, creating them a crucial tarobtain for apparel retailers. Generation Z seeks brands that align with their values, including diversity, body positivity, and social justice. They are drawn to unique, limited edition items and second hand vintage clothing, driving the growth of resale platforms and niche online boutiques. The apply of mobile first shopping experiences is paramount, with Gen Z expecting seamless navigation and rapid loading times. Interactive features such as live streams and gamified shopping experiences enhance engagement. Additionally, this group is highly responsive to visual content on platforms like TikTok and Instagram, where fashion trfinishs emerge and spread rapidly. Their willingness to experiment with styles and support emerging brands contributes to the dynamic growth of this segment. Retailers adapting to these preferences are seeing substantial increases in sales from Generation Z consumers.

COUNTRY LEVEL ANALYSIS

Germany Online Apparel Market Analysis

Germany was the top performer in the Europe online apparel market and accounted for a 24.6% share in 2025. This position of the market in Germany is supported by a high level of digital adoption and a strong preference for quality and sustainability. Apart from this, a key driver for the market in Germany is the robust logistics infrastructure, which ensures rapid and reliable delivery across the counattempt. German consumers are known for their discerning tastes and willingness to invest in durable, high quality clothing. According to the German Retail Association (HDE), e-commerce revenue continues to climb as consumer confidence returns, with apparel remaining a primary driver of online spfinishing despite broader economic shifts. The presence of major online fashion retailers such as Zalando, headquartered in Berlin, further strengthens the market ecosystem. German shoppers prioritize transparent return policies and secure payment methods, which local retailers effectively provide. Additionally, the strong emphasis on environmental sustainability drives demand for eco frifinishly brands and circular fashion models. Consumers are increasingly seeking information about supply chains and material sourcing, prompting retailers to adopt greater transparency. The high internet penetration rate and widespread apply of smartphones facilitate seamless online shopping experiences. Furthermore, the integration of offline and online channels through click and collect services enhances convenience for urban and rural consumers alike. These factors collectively sustain Germany’s position as the largest and most mature market for online apparel in Europe.

United Kingdom Online Apparel Market Analysis

The United Kingdom was the second largest counattempt in the Europe online apparel market and captured a 20.5% share in 2025. The main driver for the market is the widespread availability of next day and same day delivery services, which have become standard expectations. Also, the market status in the UK is defined by high saturation and intense competition among both domestic and international players. British consumers are among the most avid online shoppers globally, with a strong culture of digital retail adoption. The Office for National Statistics confirms that online sales maintain a substantial portion of total retail activity, keeping the UK among the leaders in digital commerce penetration across Europe. The UK is home to numerous pure play online retailers and established high street brands with strong digital presences. Consumer preference for convenience and variety drives frequent purchases, with mobile commerce playing a significant role. Additionally, the influence of social media and celebrity culture shapes fashion trfinishs, leading to rapid turnover of styles. The post Brexit regulatory environment has introduced some complexities in cross border trade, but domestic retailers have adapted efficiently. The focus on customer experience, including straightforward returns and personalized recommfinishations, remains a key competitive advantage. Furthermore, the growing interest in sustainable fashion is prompting brands to innovate in recycling and ethical sourcing. These dynamics maintain the UK’s status as a pivotal market for online apparel.

France Online Apparel Market Analysis

France occupies a significant position in the Europe online apparel market owing to its rich fashion heritage and strong luxury sector, which extfinishs into the online space. French consumers value style, quality, and brand prestige, driving demand for both high finish and mid range apparel online. Research highlight that the digital economy is expanding, with fashion and luxury goods serving as vital contributors to the nation’s online commercial growth. The primary driver for the market is the increasing digitization of traditional luxury brands, which have invested heavily in e commerce platforms to reach broader audiences. French shoppers appreciate curated online experiences that reflect the aesthetic values of physical boutiques. The government’s support for digital transformation and infrastructure development further facilitates market growth. Additionally, the rise of second hand luxury platforms appeals to environmentally conscious consumers seeking sustainable options. Mobile usage is high, with many consumers browsing and purchasing via smartphones. The integration of social commerce and influencer marketing also plays a significant role in driving sales. French retailers focus on providing exceptional customer service and exclusive online collections to differentiate themselves. These factors contribute to the steady growth and sophistication of the online apparel market in France.

Italy Online Apparel Market Analysis

Italy is shifting ahead steadrapidly in the Europe online apparel market due to a strong fashion identity and a growing acceptance of online shopping, particularly among younger demographics. Italian consumers are known for their appreciation of design and craftsmanship, influencing their online purchasing decisions. Research reveals that digital infrastructure improvements are driving a surge in online shopping, particularly within the fashion sector, which accounts for a major share of e-commerce revenue. The main accelerator for the market is the expansion of omnichannel strategies by local brands, which integrate online and offline experiences seamlessly. Many Italian fashion hoapplys have enhanced their digital presence to cater to both domestic and international customers. The popularity of mobile shopping is rising, with apps offering personalized recommfinishations and exclusive deals. Additionally, the influence of social media and fashion weeks drives trfinish awareness and impulse purchaseing. Consumers are increasingly interested in sustainable and built in Italy products, supporting local artisans and brands online. The improvement in logistics and delivery services has also boosted consumer confidence in online transactions. Furthermore, the growth of outlet online platforms offers access to discounted luxury items, attracting budobtain conscious shoppers. These elements foster the continued expansion of the online apparel market in Italy.

Spain Online Apparel Market Analysis

Spain is likely to grow notably in the Europe online apparel market from 2026 to 2034 owing to rapid digital adoption and a young, fashion conscious population. Spanish consumers are increasingly turning to online platforms for their clothing requireds, driven by convenience and competitive pricing. Regional market monitors indicate that online retail is experiencing steady growth, with the apparel category leading the way in consumer adoption and digital transaction volume. The primary driver for the market is the presence of major global fashion retailers like Inditex, which has pioneered integrated online and offline strategies. The success of brands like Zara in omnichannel retail sets a high standard for customer experience, including rapid delivery and straightforward returns. Spanish shoppers are active on social media, where fashion trfinishs are widely shared and discussed. The affordability of online fashion compared to physical stores appeals to a broad demographic, including students and young professionals. Additionally, the improvement in digital payment security and logistics infrastructure has enhanced trust in online shopping. The rise of local startups and niche brands adds variety to the market, catering to diverse tastes. Furthermore, the tourism sector influences fashion trfinishs, with visitors and locals alike contributing to demand. These factors support the dynamic growth of the online apparel market in Spain.

COMPETITIVE LANDSCAPE

The competition in the Europe online apparel market is intense and characterized by the presence of both established global giants and agile digital native brands. Major retailers compete on price, variety, speed of delivery, and customer experience, creating a dynamic environment where innovation is crucial for survival. Pure play e commerce platforms challenge traditional brick and mortar retailers who are rapidly adapting by developing robust online presences and omnichannel capabilities. Differentiation is increasingly achieved through sustainability initiatives, with brands highlighting ethical sourcing and circular practices to appeal to environmentally conscious consumers. Technology plays a pivotal role, as companies invest in artificial innotifyigence for personalization and augmented reality for virtual attempt ons to enhance applyr engagement. Private labels are gaining prominence as retailers seek to control margins and offer exclusive products. The market sees frequent collaborations and partnerships to expand reach and capabilities. Customer loyalty is hard won, requiring continuous improvement in service quality and return policies. Regulatory pressures regarding data privacy and environmental standards further shape competitive dynamics, forcing players to adapt quickly to maintain compliance and relevance.

KEY MARKET PLAYERS

A few of the market players that are dominating the Europe online apparel market are

- Amazon (US)

- Zalando (DE)

- ASOS (GB)

- H&M (SE)

- Nike (US)

- Adidas (DE)

- Macy’s (US)

- Walmart (US)

- Uniqlo (JP)

Top Players In The Market

- Zalando SE stands as a leading fashion and lifestyle platform in Europe, connecting customers with thousands of international and local brands. The company contributes significantly to the global market by setting high standards for customer experience and logistics efficiency in online retail. Zalando has recently strengthened its position by expanding its connected retail program, which integrates offline stores with its online platform to offer rapider delivery options. This initiative allows partners to sell inventory directly from physical stores, enhancing product availability and reducing carbon emissions. The company also invests heavily in technology, utilizing artificial innotifyigence to personalize shopping experiences and improve recommfinishation accuracy. By focapplying on sustainability through its do.MORE strategy, Zalando aims to reduce its environmental impact while promoting circular fashion. These efforts reinforce its reputation as a trusted and innovative leader in the European digital fashion landscape.

- Inditex Group, the parent company of Zara, is a global powerhoapply in the fashion indusattempt with a strong presence in the European online apparel market. The company drives global innovation through its integrated stock management system that seamlessly connects online and offline channels. Inditex has recently enhanced its digital capabilities by upgrading its e commerce platforms to offer improved navigation and rapider checkout processes. The group focapplys on sustainability by increasing the apply of recycled materials and implementing garment collection programs in stores. Its agile supply chain allows for rapid response to altering fashion trfinishs, ensuring fresh collections are available online frequently. Inditex also leverages data analytics to understand consumer preferences and optimize inventory levels. The company maintains a robust omnichannel strategy to ensure a consistent brand experience across all touchpoints. This approach solidifies its competitive advantage in the dynamic European market.

- H&M Group is a prominent player in the Europe online apparel market, offering a wide range of fashion and quality clothing at affordable prices. The company contributes to the global market by pioneering sustainable fashion initiatives and digital innovation in retail. H&M has recently strengthened its market position by accelerating its digital transformation, including the expansion of its membership program which offers personalized rewards and early access to collections. The group is investing in automated logistics centers to improve delivery speed and efficiency across Europe. It also focapplys on circularity by launching repair and resale services in key markets. H&M utilizes advanced data analytics to tailor its online assortment to local tastes and trfinishs. H&M continues to enhance its digital presence and maintain relevance among diverse European consumers. They achieve this by collaborating with technology startups and focapplying on customer-centric innovations.

Top Strategies Used By The Key Market Participants

Key players in the Europe online apparel market predominantly employ omnichannel integration strategies to bridge the gap between physical and digital retail experiences. Companies are investing heavily in artificial innotifyigence and machine learning to personalize customer journeys and optimize inventory management. Sustainability has become a core strategic pillar, with brands adopting circular business models such as resale and recycling programs to meet regulatory requirements and consumer expectations. Strategic partnerships with technology providers enable enhanced logistics capabilities and rapider delivery times. Social commerce is another major focus, with retailers leveraging influencer marketing and shoppable content on social media platforms to drive engagement and sales. Data analytics are utilized extensively to predict trfinishs and manage supply chain efficiencies. Additionally, companies are expanding their private label offerings to improve margins and brand loyalty. These strategies collectively aim to enhance customer retention, operational efficiency, and brand differentiation in a highly competitive digital landscape.

MARKET SEGMENTATION

This research report on the Europe online apparel market is segmented and sub-segmented into the following categories.

By Price Range

By Sales Channel

- Brand Websites

- Third-Party Retailers

- Marketplaces

- Social Media Platforms

By Product

- Men’s Apparel

- Women’s Apparel

- Children’s Apparel

- Athletic Apparel

- Accessories

By Consumer Age Group

- Generation Z

- Millennials

- Generation X

- Baby Boomers

By Counattempt

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe