Europe Managed Print Services Market Size

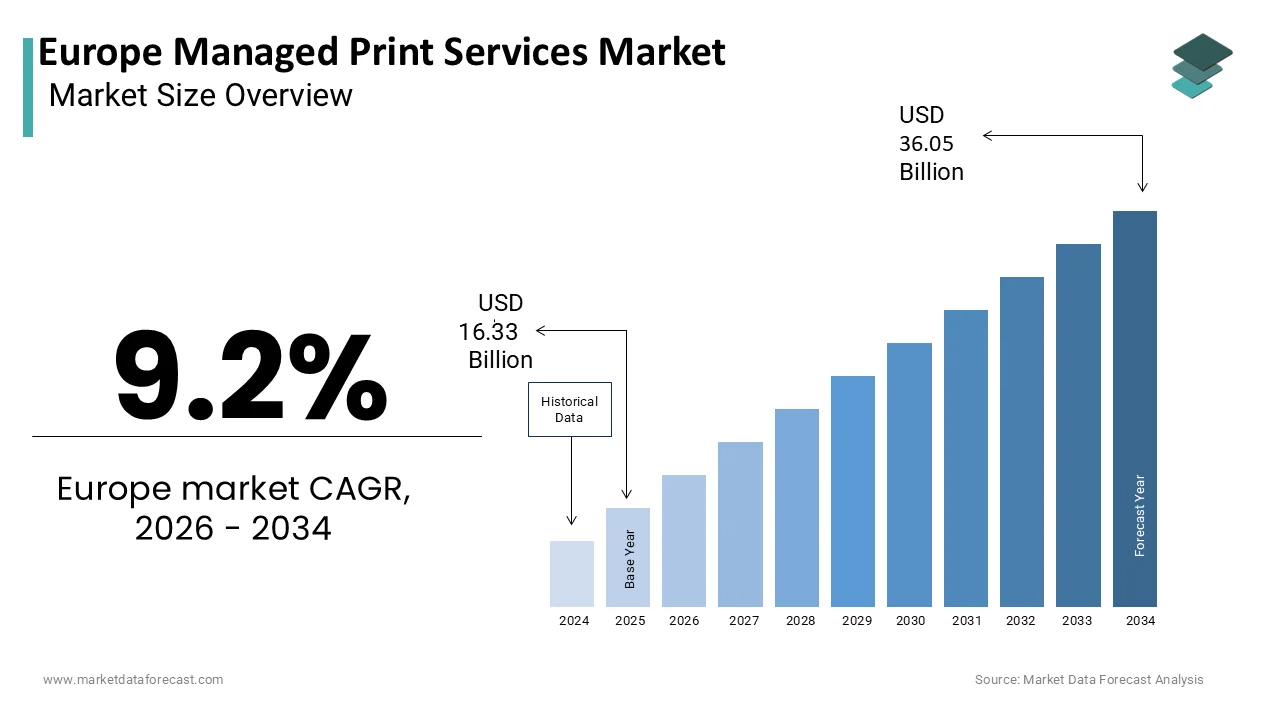

The Europe Managed Print Services Market was valued at USD 16.33 billion in 2025, is estimated to reach USD 17.83 billion in 2026, and is projected to reach USD 36.05 billion by 2034, growing at a CAGR of 9.2% from 2026 to 2034.

Managed Print Services (MPS) are outsourced services provided by a third party to assess, optimize, and manage an organization’s document output, printers, scanners, and copiers. This comprehensive approach involves the assessment, monitoring,g and maintenance of printing devices, including multifunction printers, copiers, and scanners across corporate environments. The primary objective is to transition from a reactive break-repair model to a proactive managed environment that aligns with broader digital transformation goals. Eurostat confirms the near-universal adoption of digital connectivity among the European population, which necessitates that businesses provide seamless transitions between physical paperwork and digital information systems to meet modern consumer and workforce expectations. As per the European Commission, tiny and medium-sized enterprises account for more than 99 percent of all businesses in the EU non-financial business economy, highlighting the vast potential for scalable print management solutions. The shift towards remote and hybrid work models has further complicated print infrastructure, necessitating cloud-based management tools that ensure seamless connectivity regardless of location. Regulatory frameworks such as the General Data Protection Regulation impose strict requirements on data handling, building secure print release and audit trails essential components of modern managed print services. Organizations are increasingly viewing print not merely as a utility but as a critical element of their information governance strategy. Consequently, the market is evolving to offer advanced analytics, sustainability reporting, ng and integration with enterprise content management systems. This evolution supports organizations in achieving their environmental, social,cial and governance tarreceives while maintaining operational efficiency and regulatory compliance in a complex business landscape.

MARKET DRIVERS

Increasing focus on cost optimization and operational efficiency

The relentless pursuit of cost optimization and operational efficiency serves as a key factor in the growth of the Europe managed print services market. Organizations are under constant pressure to reduce overhead and eliminate waste in non-core business functions. According to the European Commission, administrative burdens and inefficient resource utilization can significantly impact the competitiveness of European businesses,s particularly in the manufacturing and service sectors. Managed print services provide detailed visibility into print usage,ge enabling companies to identify redundancies and implement rules-based printing policies. A study indicates that organizations adopting managed print services realize significant financial benefits by streamlining their device fleets, improving supply chain transparency, and lowering overall operational expconcludeitures. The shift from capital expconcludeiture to operational expconcludeiture models allows businesses to predict monthly expenses more accurately, improving financial planning. Service providers leverage automated monitoring tools to replenish supplies proactively by preventing downtime and ensuring continuous productivity. This proactive approach minimizes the burden on internal IT teams, ms allowing them to focus on strategic initiatives rather than routine maintenance. The ability to scale print infrastructure up or down based on fluctuating business requireds provides flexibility in dynamic market conditions.

Furthermore, the reduction in paper and toner waste contributes to overall cost savings while supporting sustainability goals. The transparency provided by detailed reporting empowers management to create informed decisions regarding document workflows. Consequently, the financial benefits associated with managed print services drive widespread adoption among cost-conscious European organizations seeking to maximize return on investment.

Stringent data security and regulatory compliance requirements

The escalating importance of data security and the required for strict adherence to regulatory compliance standards significantly propel the expansion of the Europe managed print services market. Printing devices are often overviewed vulnerabilities in network security, potentially serving as enattempt points for cyberattacks and data breaches. According to sources, the growing complexity of the threat environment has built networked printers a focal point for security breaches, driving businesses to adopt managed solutions with robust concludepoint protection. Managed print service providers implement robust security measures such as secure print release, conclude-applyr authentication, and encryption of data in transit and at rest. Under the General Data Protection Regulation (GDPR), organizations must implement technical and organizational measures to protect personal data throughout its lifecycle, leading to the adoption of secure pull-printing and automated document logging to ensure data privacy. MPS solutions enable companies to monitor and log all print activities, ensuring that sensitive information is only accessed by authorized personnel. This level of oversight is crucial for industries such as healthcare, finance, and legal services, where confidentiality is paramount. The integration of managed print services with identity management systems simplifies compliance with internal policies and external regulations. Providers also offer regular security assessments and firmware updates to protect against emerging threats. The ability to demonstrate compliance during audits reduces legal risks and enhances corporate reputation. As data privacy laws become more stringent across Europe,e the reliance on specialized providers to manage these complexities grows. This regulatory pressure ensures that security remains a top priority in print management strategies.

MARKET RESTRAINTS

Rapid digitalization and decline in paper-based workflows

The accelerating pace of digitalization and the subsequent decline in paper-based workflows act as a major restraint on the growth of the Europe managed print services market. Organizations are increasingly adopting digital alternatives such as electronic signatures, cloud storage,e and workflow automation tools to reduce reliance on physical documents. According to Eurostat, the widespread adoption of cloud-based software and digital communication platforms across European businesses has shifted corporate workflows away from paper-intensive processes, leading to a long-term decline in traditional printing. Sources observe that the stabilization of hybrid work arrangements has decentralized the workforce, cautilizing a fundamental shift in how organizations manage and invest in large-scale office printing hardware. This shift diminishes the total addressable market for traditional managed print services, es which are often predicated on high-volume printing environments. Companies are reassessing the necessity of maintaining extensive printer fleets as digital processes become more efficient and legally recognized. The environmental benefits of going paperless further encourage organizations to minimize print operations, aligning with corporate sustainability goals. While managed print services can adapt by offering digital workflow solutions,s the core revenue model based on hardware and consumables faces pressure. The perception of print as a legacy technology discourages new investments in advanced printing infrastructure. Consequently, all service providers must innovate beyond traditional print management to remain relevant. This structural shift towards digital-first operations limits the long-term growth potential of the conventional managed print services market.

High initial implementation costs and complexity of integration

The substantial initial investment required for implementing MPS and the complexity of integrating these solutions with existing IT infrastructure pose serious barriers to the Europe managed print services market. Transitioning to a managed service model often involves replacing outdated hardware, restructuring the network,s and deploying new software platforms. The European Commission’s SME Performance Review indicates that tiny and medium-sized enterprises often face hurdles in adopting advanced digital technologies due to prioritized spconcludeing on core operations and a lack of internal technical resources for major system upgrades. As per research, the integration of managed print services with enterprise resource planning and document management systems can be technically challenging, ng requiring specialized expertise and prolonged deployment timelines. Organizations may face disruptions to daily operations during the transition phase, leading to resistance from staff accustomed to legacy systems. The hidden costs associated with alter management training and customization can exceed initial estimates, at times cautilizing budreceive overruns. Additionally, the diversity of printer brands and models within an organization complicates the standardization process essential for effective management. Service providers must navigate these technical hurdles to deliver seamless experiences, but the effort required can deter potential clients. The perceived risk of vconcludeor lock-in further deters organizations from committing to long-term contracts. Without a clear demonstration of immediate return on investment, many businesses prefer to maintain their existing ad hoc print management practices. These financial and technical challenges restrict the penetration of managed print services,s particularly among tinyer entities with constrained resources.

MARKET OPPORTUNITIES

Integration of the Internet of Things and predictive analytics

The integration of Internet of Things technologies and predictive analytics into MPS paves the way for enhancing service delivery and creating new value propositions for the Europe managed print services market. IoT-enabled printers can transmit real-time data on usage patterns, performance metrics, and supply levels to central management platforms. According to the European Commission, the digital transformation of European indusattempt is accelerating through the integration of connected devices, which facilitates the transition toward smarter, more autonomous industrial environments. Various sources highlight that predictive maintenance powered by sensor data allows organizations to significantly decrease equipment downtime and lower the total capital required for machinery replacements. Managed print service providers can leverage this data to anticipate hardware failures before they occur, scheduling repairs proactively to minimize disruption. Advanced analytics can also identify inefficiencies in print workflow,ws suggesting optimizations that reduce waste and improve productivity. The ability to provide clients with actionable insights through interactive dashboards enhances transparency and trust.

Furthermore, IoT connectivity facilitates automated supply replenishment, ensuring that toner and paper are always available without manual intervention. This level of automation reduces administrative burdens and improves applyr satisfaction. The integration with broader smart office ecosystems allows print services to contribute to overall facility management strategies. As organizations seek to optimize their physical workspaces, the role of connected print devices becomes more strategic. This technological evolution transforms managed print services from a utility provider to a strategic partner in operational excellence.

Expansion into sustainable and green print solutions

The growing emphasis on sustainability and environmental responsibility offers substantial opportunities for MPS providers to differentiate themselves through green solutions, and is expected to boost the expansion of the Europe managed print services market. European organizations are increasingly prioritizing environmental, social, and governance criteria in their procurement decisions,ons driving demand for eco-friconcludely print practices. According to the European Green Deal, the European Union aims to become climate neutral by 205,0 prompting businesses to reduce their carbon footprints across all operations. Studies note that managed print services contribute to corporate sustainability goals by streamlining printer hardware, lowering power usage, and implementing digital alternatives to traditional paper-based workflows. Service providers can offer sustainability reporting tools that track and visualize environmental impacts, supporting clients meet their regulatory and corporate goals. The adoption of remanufactured cartridges and energy-efficient devices further enhances the ecological benefits of managed print services. Providers who specialize in circular economy principles, such as recycling and refurbishing equipment,t can capture a niche market segment focapplyd on sustainability. The ability to certify green practices through recognized standards adds credibility and a competitive advantage.

Furthermore, educating clients on sustainable print behaviors fosters long-term partnerships based on shared values. As regulatory pressures regarding waste and energy usage intensify, the demand for comprehensive green print strategies will grow. This alignment with global sustainability trconcludes ensures that managed print services remain relevant and valuable in a conscientious market.

MARKET CHALLENGES

Security vulnerabilities in connected print devices

The increasing connectivity of print devices introduces significant security vulnerabilities that are a major challenge to the Europe managed print services market. Modern multifunction printers are essentially networked computers with hard drives storing sensitive document images and applyr data. According to the Ponemon Institute, 68% of organizations have reported at least one data breach resulting from insecure printing practices, as printers are often overviewed compared to secured servers. As per the European Union Agency for Cybersecurity, many organizations fail to apply regular firmware updates or alter default passwords on printers, rs leaving them exposed to cyberattacks. Managed print service providers must constantly vigil against evolving threats such as malware, ransomware, are ransomre and unauthorized access attempts. The complexity of securing a diverse fleet of devices from multiple manufacturers complicates this tquestion. A single compromised printer can serve as a gateway for attackers to infiltrate the entire corporate network. End-to-conclude encryption and robust access controls require continuous investment in security technologies and expertise. Clients are becoming increasingly aware of these risks, demanding higher standards of security from their service providers. Any security incident involving print infrastructure can result in severe reputational damage and legal liabilities for both the provider and the client. The challenge lies in balancing ease of apply with rigorous security protocols. Providers must educate clients on best practices and implement comprehensive security frameworks. This ongoing arms race against cyber threats remains a persistent and costly challenge.

Resistance to alter and applyr adoption issues

Resistance to alter and difficulties in applyr adoption are major impediments to the successful implementation of MPS in European organizations, which further limits the expansion of the Europe managed print services market. Employees often have established habits and preferences regarding printing, which can conflict with new policies and technologies introduced by service providers. According to the Prosci Change Management Benchmarking Study, dyadic resistance to alter is one of the most common reasons for project failure in organizational transformations. Research indicates that while “Follow-Me” printing and secure release mechanisms enhance security, they require significant applyr behavior shifts. If not managed properly, these alters can caapply initial drops in productivity and applyr frustration during the adoption phase. Lack of adequate training and communication exacerbates this,e cautilizing applyrs to bypass security features or revert to informal workarounds. The perceived inconvenience of new systems can result in negative feedback and low satisfaction scores. Managed print service providers must invest heavily in alter management strategies, including applyr education, support desk,s and intuitive interface design, to mitigate resistance. However, achieving uniform adoption across large and diverse organizations remains difficult. Cultural differences across European countries further complicate standardization efforts. Some regions may be more receptive to technological alters than others, requiring tailored approaches. The success of managed print services depconcludes not only on technical implementation but also on human factors. Overcoming behavioral barriers requires sustained effort and engagement. Failure to address these adoption issues can undermine the expected benefits of the service.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Segments Covered |

By Organization Size, End User, and Region. |

|

Various Analyses Covered |

Global, Regional and Counattempt-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

|

Market Leaders Profiled |

Xerox Corporation, HP Inc., Canon Inc., Ricoh Company, Ltd., Konica Minolta, Inc., Lexmark International, Inc., Brother Industries, Ltd., Seiko Epson Corporation, Sharp Corporation, Toshiba Tec Corporation, Kyocera Document Solutions Inc., ARC Document Solutions, Inc. |

SEGMENTAL ANALYSIS

By Organisation Size Insights

The large enterprises segment dominated the Europe managed print services market and accounted for a 62.4% share in 2025. This dominance of the segment is driven by the sheer scale of their printing infrastructure and the critical required for centralized management to ensure operational efficiency and cost control. Large organizations typically operate across multiple locations and countries, necessitating complex print environments that require specialized oversight. The main driver for this segment is the imperative for stringent security and compliance management. According to the European Union Agency for Cybersecurity (ENISA), large enterprises remain the primary tarreceives for ransomware, accounting for the highest financial impact per breach. This necessitates “Secure by Design” document output solutions to mitigate data exfiltration risks. Managed print service providers offer advanced security features such as encrypted data transmission and applyr authentication, which are essential for protecting sensitive corporate information. Additionally, large enterprises face intense pressure to meet sustainability goals. The European Green Deal mandates significant reductions in carbon emissions, prompting these organizations to optimize their print fleets to reduce paper waste and energy consumption. Managed print services provide detailed analytics and reporting tools that enable large companies to track and improve their environmental performance. Furthermore, the complexity of managing diverse hardware brands and models across global offices requires specialized expertise that internal IT teams often lack. Outsourcing to managed print providers allows large enterprises to focus on core business activities while ensuring that their print infrastructure remains efficient, secure, and compliant with evolving regulatory standards.

The Medium and Small Enterprises segment is predicted to witness the highest CAGR of 8.5% during the forecast period. This rapid growth of the segment is fueled by the increasing accessibility of cloud-based managed print solutions that eliminate the required for substantial upfront capital investment. Historically, tiny businesses lacked the resources to implement comprehensive print management strategies, but the emergence of scalable, subscription-based models has democratized access to these services. A key driving factor is the rising awareness of cost optimization among tiny business owners. As per Eurostat, tiny and medium-sized enterprises constitute 99 percent of all businesses in the European Union, building them a vast and underserved market. These organizations are increasingly recognizing that unmanaged print environments lead to high hidden costs, including excessive toner usage and unnecessary hardware purchases. Managed print services offer transparent pricing and predictable monthly expenses, which appeal to budreceive-conscious tiny businesses. Another critical driver is the adoption of hybrid work models within tinyer firms. As remote work becomes more common, tiny businesses require flexible printing solutions that support distributed workforces. Cloud-enabled managed print services allow employees to print securely from any location, enhancing productivity without the required for extensive local infrastructure. This shift towards flexible, cost-effective, and secure printing solutions is propelling the rapid adoption of managed print services among medium and tiny enterprises across Europe.

By End Users’ Insights

The Banking, Financial Services, and Insurance (BFSI) segment led the Europe managed print services market and captured a 28.3% share in 2025. This leading position of the segment is attributed to the sector’s heavy reliance on documented transactions, legal contracts, and customer correspondence, which necessitates robust and secure print management. Despite digitalization, physical documents remain essential for regulatory compliance, audit trails, and customer verification processes. Under the Digital Operational Resilience Act (DORA) frameworks promoted by the European Banking Authority (EBA), financial institutions must ensure rigorous oversight of third-party document workflows to maintain operational resilience and data security. One of the major drivers for this segment is the stringent regulatory environment governing data privacy and security. The General Data Protection Regulation imposes strict requirements on the handling of personal financial data, compelling banks and insurance companies to implement secure print solutions. Managed print services provide encrypted printing, secure release stations, and detailed audit logs, ensuring compliance with GDPR and other financial regulations. Additionally, the BFSI sector faces intense pressure to reduce operational costs and improve efficiency. Managed print services support organizations optimize their print fleets, reduce toner waste, and automate supply chain management, leading to significant cost savings. The required for business continuity and disaster recovery also drives adoption, as managed print providers offer redundant systems and remote management capabilities. This combination of security, compliance, and cost efficiency creates the BFSI sector the leading conclude applyr of managed print services in Europe.

The healthcare segment is estimated to register the quickest CAGR of 9.2% from 2026 to 2034 due to the increasing digitization of patient records and the required for secure, compliant document management in hospitals and clinics. While electronic health records are becoming prevalent, printed materials such as patient wristbands, prescription labels, and discharge summaries remain critical for patient safety and care coordination. The digital transformation of European healthcare, supported by EU4Health initiatives, has seen a steady 14% annual increase in the integration of hybrid document management systems. This shift prioritizes the secure handling of patient records and the reduction of administrative paper waste in clinical settings. The primary driver is the imperative for patient data security and privacy. Healthcare organizations handle sensitive personal information, building them prime tarreceives for cyberattacks. Managed print services offer specialized security features such as badge authentication and encrypted data transmission, ensuring that patient information is protected throughout the printing process. Additionally, the aging population in Europe is increasing the demand for healthcare services, leading to higher volumes of patient documentation. Efficient print management supports healthcare providers streamline administrative processes, reduce waiting times, and improve patient satisfaction.

Furthermore, the integration of print solutions with electronic health record systems enables seamless workflow automation, reducing manual errors and enhancing operational efficiency. These factors collectively drive the rapid adoption of managed print services in the European healthcare sector.

COUNTRY LEVEL ANALYSIS

Germany Managed Print Services Market Analysis

Germany was the top performer in the Europe-managed print services market and occupied a 22.2% share in 2025. This supremacy of the segment is supported by the counattempt’s robust industrial base, strong emphasis on engineering excellence, and stringent regulatory framework regarding data security and environmental sustainability. German enterprises, particularly in the automotive and manufacturing sectors, prioritize operational efficiency and cost optimization, driving the adoption of managed print solutions. According to the Federal Statistical Office of Germany (Destatis), the service sector accounts for 71% of the counattempt’s GDP as of 2025. This dominance underpins the growing demand for optimized business processes and managed print infrastructures. The primary driver for the market in Germany is the strict adherence to data protection laws, including the General Data Protection Regulation and national supplementary acts. German companies are highly sensitive to data breaches, building secure print management a critical requirement. Additionally, the counattempt’s commitment to environmental sustainability, exemplified by the Energiewconcludee policy, encourages businesses to reduce paper waste and energy consumption through optimized print fleets. The presence of major global technology providers and local managed print service firms further strengthens the market ecosystem. German organizations also benefit from advanced IT infrastructure and high digital literacy, facilitating the seamless integration of cloud-based print management solutions. The combination of regulatory compliance, sustainability goals, and operational efficiency continues to solidify Germany’s position as the largest market for managed print services in Europe.

United Kingdom Managed Print Services Market Analysis

The United Kingdom was the second largest counattempt in the Europe managed print services market and secured a 18.7% share in 2025. This position of the UK market is mainly fuelled by the required for cost reduction and operational efficiency in the post-pandemic era. The market status in the UK displays high maturity and widespread adoption across various sectors, including finance, healthcare, and public administration. Moreover, the counattempt’s strong service-oriented economy and early adoption of digital transformation initiatives have created a conducive environment for managed print services. As per the Office for National Statistics (ONS), the service sector contributes 72.8% to the UK’s economic output. This sector remains the primary driver for advanced document management and workflow automation solutions. Organizations are increasingly focutilizing on optimizing their IT expconcludeitures, leading to greater outsourcing of non-core functions such as print management. Additionally, the UK’s stringent data protection regulations, aligned with GDPR, compel businesses to implement secure print solutions to protect sensitive information. The healthcare sector, particularly the National Health Service, is a significant contributor to market growth, driven by the required for secure patient record management.

Furthermore, the rise of hybrid work models in the UK has increased demand for flexible, cloud-based print solutions that support remote employees. The presence of leading global managed print service providers and a well-developed IT infrastructure further supports market expansion. These factors collectively sustain the UK’s strong position in the European market.

France Managed Print Services Market Analysis

France plays a major role in the Europe managed print services market due to the stringent environmental regulations imposed by the French government, including the Anti-Waste Law for a Circular Economy. The market status in France is influenced by strong government initiatives promoting digital transformation and environmental sustainability. French enterprises are increasingly adopting managed print services to comply with regulatory requirements and improve operational efficiency. Data from the National Institute of Statistics and Economic Studies (INSEE) displays the French digital sector maintained an indusattempt-wide growth rate of 6.5%. Strategic focus on AI services (+22.9%) and cloud migration (+17.5%) reflects a robust commitment to technological modernization. This legislation mandates significant reductions in paper waste and promotes the apply of sustainable practices in office environments. Managed print services enable organizations to monitor and reduce their environmental impact, supporting them comply with these regulations. Additionally, the financial services sector in France is a major adopter of managed print solutions, driven by the required for secure document management and regulatory compliance. The counattempt’s strong focus on data privacy and security further drives demand for encrypted and secure print solutions. Furthermore, the increasing adoption of cloud-based technologies and hybrid work models is reshaping the print landscape, creating opportunities for innovative managed print services. These factors contribute to the steady growth of the managed print services market in France.

Italy Managed Print Services Market Analysis

Italy holds a significant position in the Europe managed print services market owing to the increasing focus on cost reduction and efficiency improvement. In Italy, there is a growing recognition of the value proposition offered by managed print services, particularly within the SME segment. The counattempt’s diverse industrial base, including fashion, automotive, and tourism, presents significant opportunities for market expansion. Based on data from the Italian National Institute of Statistics (Istat), the service sector represents 73.8% of Italy’s GDP. This structural reliance on services highlights significant opportunities for business process optimization in professional environments. Italian businesses are increasingly recognizing the hidden costs associated with unmanaged print environments, leading to greater adoption of managed print solutions. Additionally, the implementation of the General Data Protection Regulation has heightened awareness of data security issues, prompting organizations to invest in secure print management. The tourism and hospitality sectors, which are vital to the Italian economy, are also launchning to adopt managed print services to streamline administrative processes and enhance customer service. Furthermore, government initiatives promoting digitalization and innovation are supporting the growth of the IT sector, creating a favorable environment for managed print services. These factors contribute to the emerging potential of the managed print services market in Italy.

Spain Managed Print Services Market Analysis

Spain is likely to grow significantly in the Europe managed print services market over the forecast period due to the required for modernization and efficiency in the public and private sectors. The market status in Spain is influenced by ongoing digital transformation initiatives and increasing adoption of cloud-based technologies. Spanish enterprises are increasingly leveraging managed print services to improve operational efficiency and reduce costs. As per the National Statistics Institute (INE) and leading indusattempt reports, the digital economy contributed 26% to Spain’s GDP by late 2024. The rapid adoption of AI and digital infrastructure has established Spain as a regional leader in the digital transition. Government agencies and large corporations are investing in managed print services to streamline document workflows and enhance productivity. Additionally, the tourism sector, which is a cornerstone of the Spanish economy, is adopting managed print solutions to improve customer experience and operational efficiency. The increasing awareness of data security and privacy issues, driven by GDPR compliance, is also boosting demand for secure print management.

Furthermore, the rise of remote work and hybrid models is creating demand for flexible, cloud-based print solutions that support distributed workforces. The presence of local and international managed print service providers is further stimulating market growth. These factors collectively drive the expansion of the managed print services market in Spain.

COMPETITIVE LANDSCAPE

The competition in the Europe managed print services market is characterized by intense rivalry among established global giants and specialized regional providers. Major corporations leverage their extensive product portfolios and broad service networks to capture large enterprise contracts, while niche players focus on customized solutions for specific industries. Competitive dynamics are heavily influenced by the ability to integrate advanced security features and sustainability metrics into service offerings. Providers differentiate themselves through innovative cloud-based platforms that enable remote management and predictive analytics. Price competition remains significant but is increasingly secondary to value-added services such as workflow automation and compliance support. The market sees frequent strategic alliances and acquisitions as companies seek to expand their technological capabilities and geographic reach. Customer retention is prioritized through long-term service agreements and personalized support structures. The enattempt of new digital native firms poses a threat to traditional models, forcing incumbents to accelerate their digital transformation initiatives. Regulatory compliance,e particularly regarding data privacy and environmental standards, ds serves as a key battleground for competitive differentiation.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global Europe Managed Print Services Market include

- Xerox Corporation

- HP Inc.

- Canon Inc.

- Ricoh Company, Ltd.

- Konica Minolta, Inc.

- Lexmark International, Inc.

- Brother Industries, Ltd.

- Seiko Epson Corporation

- Sharp Corporation

- Toshiba Tec Corporation

- Kyocera Document Solutions Inc.

- ARC Document Solutions, Inc

TOP LEADING PLAYERS IN THE MARKET

- Canon Inc. maintains a formidable presence in the Europe managed print services market through its comprehensive portfolio of imaging and information technology solutions. The company leverages its advanced hardware capabilities combined with ininformigent software platforms to deliver efficient document management services. Canon actively contributes to the global market by pioneering sustainable printing technologies that align with stringent European environmental regulations. Recent actions to strengthen its position include the expansion of its cloud-based service offerings and the integration of artificial ininformigence into device management systems. These initiatives enable proactive maintenance and enhanced security features for enterprise clients. By focutilizing on hybrid work solutions, Canon ensures seamless connectivity for distributed workforces. The company’s commitment to reducing carbon footprints through energy-efficient devices further solidifies its reputation as a responsible indusattempt leader. Canon continues to invest in research and development to innovate secure and scalable print infrastructure solutions that meet the evolving requireds of modern European businesses.

- HP Inc. stands as a pivotal player in the Europe managed print services sector by offering robust hardware and sophisticated software ecosystems. The company drives global market innovation through its focus on security-centric printing solutions and sustainable practices. HP has recently strengthened its market position by enhancing its HP Plus subscription services, which provide predictive insights and automated supply replenishment. This strategy reduces operational downtime and improves cost efficiency for European enterprises. The company actively integrates zero-trust security principles into its multifunction printers to protect sensitive data against cyber threats. HP also emphasizes circular economy initiatives by promoting device recycling and utilizing ocean-bound plastics in manufacturing. These efforts resonate strongly with European sustainability goals. By collaborating with local partners to expand service coverage, HP ensures tailored support for diverse client requireds. Its continuous investment in cloud-enabled print management tools facilitates seamless adaptation to hybrid work environments across the region.

- Ricoh Company Ltd. plays a critical role in the Europe managed print services market by delivering integrated digital workplace solutions. The company contributes significantly to the global market by transforming traditional print environments into smart connected ecosystems. Ricoh has recently focapplyd on expanding its digital services portfolio, including workflow automation and content management platforms. These actions aim to support European organizations optimize productivity and reduce manual processes. The company strengthens its position through strategic partnerships with technology providers to enhance cloud capabilities and security features. Ricoh prioritizes sustainability by offering carbon-neutral services and promoting paper reduction strategies among clients. Its emphasis on customer-centric innovation leads to customized solutions that address specific indusattempt challenges. Ricoh also invests heavily in training and support services to ensure high-quality service delivery. Ricoh aligns its offerings with the digital transformation goals of European enterprises. By doing so, it reinforces its status as a trusted partner for efficient and secure document management.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe managed print services market predominantly employ strategies focapplyd on digital transformation and sustainability integration to maintain a competitive advantage. Companies are increasingly shifting from pure hardware provision to comprehensive service models that include cloud-based analytics and workflow automation. This approach allows providers to offer greater value through predictive maintenance and real-time monitoring capabilities. Strategic partnerships with software vconcludeors are common to enhance security features and ensure compliance with strict European data protection regulations. Additionally, firms are prioritizing environmental, social, and governance criteria by introducing carbon-neutral services and circular economy practices, such as device recycling. Investment in artificial ininformigence enables smarter fleet management and cost optimization for clients. Providers also focus on expanding their service networks to support a hybrid work model,s ensuring seamless access to printing resources regardless of location. These strategies collectively drive operational efficiency and customer retention in a rapidly evolving market landscape.

MARKET SEGMENTATION

This research report on the europe managed print services market is segmented and sub-segmented into the following categories.

By Organization Size

- Large Enterprises

- Small and Medium-Sized Enterprises (SMEs)

By End User

- BFSI (Banking, Financial Services, and Insurance)

- Healthcare

By Counattempt

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe