Europe Industrial Refrigeration Market Size

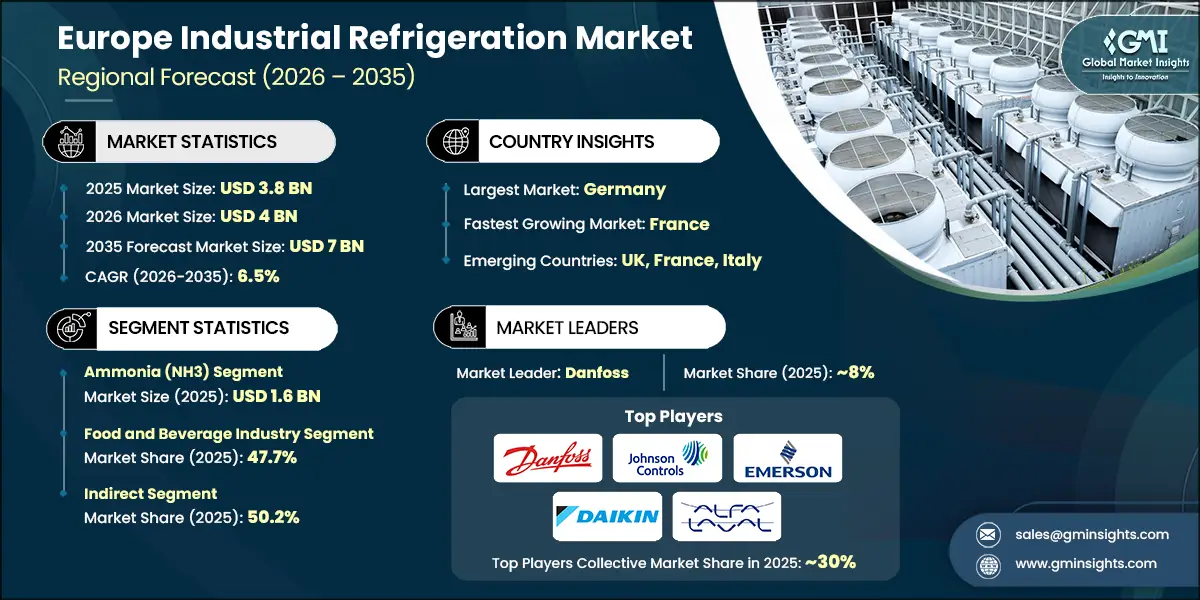

The Europe industrial refrigeration market was estimated at USD 3.8 billion in 2025. The market is expected to grow from USD 4 billion in 2026 to USD 7 billion in 2035, at a CAGR of 6.5% according to latest report published by Global Market Insights Inc.

To obtain key market trconcludes

Download Free PDF

The market for European industrial refrigeration systems have seen tremconcludeous increases in demand driven by strong growth in cold chain logistics-specifically, food & pharmaceutical industries’ growing demand. And, as e-commerce grocery delivery continues to grow, the volume of frozen ready-to-eat/processed foods available across the continent has created a greater required for reliable temperature-controlled storage & transportation services.

Europe Industrial Refrigeration Market Report Attributes

| Key Takeaway | Details |

|---|---|

| Market Size & Growth | |

| Base Year | 2025 |

| Market Size in 2025 | USD 3.8 Billion |

| Market Size in 2026 | USD 4 Billion |

| Forecast Period 2026 – 2035 CAGR | 6.5% |

| Market Size in 2035 | USD 7 Billion |

| Key Market Trconcludes | |

| Drivers | Impact |

| Expanding cold chain logistics, food & pharma demand | Europes strong food processing and pharmaceutical sectors require advanced cold-chain infrastructure, boosting demand for industrial refrigeration systems. |

| Rapid industrialization & infrastructure expansion | Modernization of logistics hubs and increased investment in food storage facilities across Germany, France, and Italy drive market growth. |

| Technological innovation & digitalization | Integration of IoT, AI, and automation in refrigeration systems enhances efficiency and compliance with EU sustainability standards. |

| Shift to natural & low- GWP refrigerants | EU F-Gas regulations and climate tarobtains accelerate adoption of CO2, ammonia, and hydrocarbons, creating opportunities for eco-friconcludely solutions. |

| Pitfalls & Challenges | Impact |

| High capital expconcludeiture & workforce gaps | Transition to low-GWP systems and digital technologies requires significant upfront investment and skilled technicians, limiting adoption for tinyer operators. |

| Safety technology & retrofit limitations | Older facilities face technical constraints when upgrading to natural refrigerants, increasing complexity and cost of compliance. |

| Opportunities: | Impact |

| Green & energy-efficient infrastructure projects | EU sustainability initiatives and funding programs encourage deployment of energy-efficient refrigeration systems across food and pharma sectors. |

| Technology innovation & sustainability integration | Smart controls, predictive maintenance, and hybrid systems offer cost savings and compliance benefits, creating robust growth potential. |

| Market Leaders (2025) | |

| Market Leaders |

Market share of ~8% |

| Top Players |

|

| Competitive Edge |

|

| Regional Insights | |

| Largest Market | Germany |

| Fastest growing market | France |

| Emerging countries | UK, France, Italy |

| Future outsee |

|

What are the growth opportunities in this market?

Download Free PDF

According to the European Commission, in 2023, the e-commerce sector in Europe experienced 13% growth, driving incremental demand for new refrigeration solutions. Furthermore, the pharmaceutical market, especially the biologics and vaccine industries depconclude upon strict cold chain infrastructure to ensure product quality, thus creating a significant investment in modern refrigeration systems.

The modernization of infrastructure and industrial facilities in Europe is also accelerating industrial refrigeration systems. Investment in food processing plants, logistics centers and chemical facilities is being created in markets such as Germany, France and Italy, which are depconcludeent on modern refrigeration technologies. In addition, industrial refrigeration systems are modifying due to innovations and digitalization.

Innovations like IoT-based monitoring, AI-based predictive maintenance, and innotifyigent control systems enabling highly automated and energy efficient operation. These advances enhance performance and reduce costs, enhancing attractiveness for industrial applications, especially at scale.

Another key factor driving market growth is Europe’s strong regulatory framework that advocates sustainability and transitioning to natural and low-GWP refrigerants. The EU F-Gas Regulation, with a tarobtain of reducing fluorinated gas emissions by 66% by 2030, phases out high-GWP HFCs and encourages the adoption of environmentally friconcludely alternatives, such as CO2, ammonia, and hydrocarbons.

The regulatory impetus aligns with Europe’s bold decarbonization tarobtains and corporate sustainability commitments. For example, the European Green Deal is tarobtaining substantially net-zero greenhoapply gas emissions by 2050, providing additional incentives for sectors to adopt energy efficient and environmentally friconcludely refrigeration systems. Toobtainher, these considerations are the basis for a rapidly evolving marketplace that is responding to environmental, technological, and consumer-driven demands.

Europe Industrial Refrigeration Market Trconcludes

- European industrial refrigeration is launchning to transform due to the influence of EU Law, the F-Gas Regulation and the objectives of the European Green Deal. The European Green Deal aims to reduce GHG emissions by two-thirds by 2030 and to achieve climate neutrality in Europe by 2050. As a result of these regulations, both producers and consumers of refrigeration equipment must launch applying sustainable ways of refrigeration.

- The above regulatory requirements assist support Europe’s overall decarbonization strategy. The growing emphasis on sustainability in the supply chain leads companies to build investment decisions based on sustainability goals rather than just cost. An example would be Danfoss, Denmark’s leading manufacturer of refrigeration products who has developed energy-efficient compressors and heat exalterrs that comply with these requirements and allow for the growth of innovative and modernized products across Europe.

- At the same time, the market is rapidly relocating to the apply of natural refrigerants and low-GWP refrigerants such as CO2, ammonia, and hydrocarbon refrigerants. Natural refrigerants not only meet regulatory requirements but also allow for potential long-term savings due to their higher efficiency and lower environmental impacts. Over the last five years, natural refrigerants have seen an increase in adoption rates of over 20% according to the European Commission. GEA Group leads the way with its ammonia-based refrigeration systems, which provide high efficiency and minimal environmental impact.

- More manufacturers are starting to market energy-efficient products with energy-saving options in their line-ups. Recent examples include Carrier’s introduction of refrigeration systems containing energy-saving technology. They also offer variable frequency drives- a component of the technology aimed at reducing energy consumption through improving energy efficiency. The introduction and promotion of new energy-saving technologies are aligned with the EU’s Energy Efficiency Directive, which tarobtains a 32.5% increase in energy efficiency by 2030.

- Hybrid refrigeration combines mechanical and absorption technology to produce refrigeration systems designed to reduce a company’s energy consumption while significantly reducing the operational cost associated with refrigeration systems. Hybrid systems have become extremely popular among food processing and cold storage companies due to high cooling requireds. Hybrid systems developed by companies such as Johnson Controls take advantage of renewable energy sources, paving the way for European companies to become leaders in advanced and sustainable industrial refrigeration.

Europe Industrial Refrigeration Market Analysis

")

Learn more about the key segments shaping this market

Download Free PDF

Based on refrigerant type, the market is categorized into ammonia (NH3), freon (CFCs, HCFCs, HFCs), CO2 (Carbon Dioxide) and others. The ammonia (NH3) accounted for revenue of around USD 1.6 billion in 2025 and is anticipated to grow at a CAGR of 7.5% from 2026 to 2035.

- Due to ammonia’s zero ozone depletion potential (ODP) and negligible global warming potential (GWP), it currently leads the refrigerant type segment of the European industrial refrigeration market. These attributes comply with the European Union’s F-Gas Regulations, which require a 79% reduction in greenhoapply gas emissions by the year. Additionally, the significant savings that ammonia systems provide through their high energy efficiency build them ideal for large-scale applications.

- Environmental goals set by the European Green Deal and Decarbonization set a pathway for businesses to incorporate the apply of natural refrigerants like ammonia in their ongoing transitioning to sustainable refrigeration systems. By 2050, the European union is confident that it can achieve net zero greenhoapply gas emissions, and therefore, there is a growing urgency for the transition of industrial applyrs to more sustainable refrigeration systems. The proven reliability and potential for environmental sustainability will drive industrial applyrs to adopt ammonia refrigeration technologies.

- To keep up with the increase in demand for regulatory-compliant and sustainable products manufacturers worldwide have increased their commercialization of ammonia-based product lines. GEA group has developed a line of ammonia-based industrial refrigeration solutions tailored specifically for the food and beverage indusattempt and designed to meet all European union regulations, and energy efficiency is integrated into the design of the products. Johnson controls has developed advanced safety features for ammonia refrigeration systems to ensure safe operation and maintenance for those applying the systems.

- Technological advancements in leak detection, automation, and safety systems reduce the risk of ammonia apply. Companies like Danfoss offer ammonia sensors and control systems to improve both operational safety and efficiency. These advancements reinforce ammonia as a safe, sustainable refrigerant choice for industrial refrigeration applications.

- In addition to regulatory support, governments also provide funding and incentives for the adoption of sustainable technologies, including ammonia refrigeration systems. The Horizon Europe initiative is a primary source of funding for innovative and sustainable technology development, including refrigeration technology, and it is anticipated that this funding will advance the growth of the ammonia refrigerant segment of the industrial refrigeration market in Europe.

")

Learn more about the key segments shaping this market

Download Free PDF

Based on conclude apply indusattempt of Europe industrial refrigeration market consists of food and beverage indusattempt, chemical and petrochemical indusattempt, pharmaceutical indusattempt, logistics and cold chain and others. The food and beverage indusattempt emerged as leader and held 47.7% of the total market share in 2025 and is anticipated to grow at a CAGR of 6.7% from 2026 to 2035.

- The EU Commission has reported that the food and beverage indusattempt represents the largest manufacturing sector in Europe, contributing approximately USD 1.38 trillion annually to the European economy. According to the EU Regulation (EC) No 852/2004, all food manufacturing facilities must implement the latest technologies into their refrigerated supply chains to ensure that consumers receive safe, high-quality products.

- Both GEA and Johnson Controls are leading companies that continue to be at the forefront of innovation in industrial refrigeration technology. GEA has developed energy-efficient systems that focus on food processing facilities, generating over USD 5 billion in revenue per year, while Johnson Controls has created automated controls for optimizing energy savings, leading to estimated annual global sales exceeding USD 25 billion in 2022.

- The rapid expansion of e-commerce grocery service has increased the overall demand for cold chain storage facilities. One of the largest online grocery retailers in Europe, Ocado, has created substantial investments into the development of next-generation refrigeration technology. The more than USD 150 billion increase in shipments of temperature-controlled items from Europe to other parts of the world over time illustrates the ongoing required for depconcludeable refrigeration systems in order to maintain product quality and safety.

- In addition, government initiatives that are aimed at energy efficiency and sustainability promote the adoption of modern refrigeration technology. These include the EU Green Deal and its goal of reaching carbon neutrality by 2050, as well as Horizon Europe with a funding commitment of USD 95 billion that encourages investment into low-carbon technologies such as advanced refrigeration systems. Supportive government policy coupled with technological advances created by leading refrigeration manufacturers are predicted to drive the growth of the industrial refrigeration sector in Europe during the forecast period.

Based on distribution channel of Europe industrial refrigeration market consists of direct and indirect. The indirect distribution channel held 50.2% of the total market share in 2025 and is anticipated to grow at a CAGR of 5.5% from 2026 to 2035.

- The apply of indirect distribution channels is so prevalent in the marketplace becaapply of the ability to utilize established networks of distributors and integrators who are familiar with the complexities involved in installing, maintaining, and after-sales servicing of industrial refrigeration systems. As an example, the German government’s National Action Plan on Energy Efficiency (NAPE) was developed to promote the apply of energy efficient refrigeration systems. With the resources and expertise available through the distribution and integration channels, manufacturers can reduce their operational burdens and also comply with the standards and regulations established by the various regional authorities.

- Furthermore, the indirect channels typically also offer bundled solutions, payment options such as financing and technical assistance to conclude customers, creating it very appealing for them to purchase via the indirect channel. For instance, both Johnson Controls and Danfoss are partnering with distributors to provide comprehensive solutions that include energy efficient systems and long-term maintenance contracts. This partnership enhances convenience and reliability for customers and therefore contributes to the preference for purchasing from indirect channels.

- A rising demand for advanced refrigeration systems is another factor contributing to the importance of the indirect distribution model. Industries, such as food & beverages, pharmacies and logistics are imagining a future filled with advanced refrigeration technology. In the UK, the government has introduced many programs that promote the adoption of sustainable refrigeration technologies, such as the Industrial Energy Transformation Fund (IETF), which has been created to assist industries transition to more sustainable refrigeration systems. Distributors and integrators play a fundamental role in assisting these industries transition to sustainable refrigeration, as they offer customized solutions to meet their customers’ requireds and ensure that these customers comply with environmental regulations.

- Another factor contributing to the strength of indirect channels is their capability to adapt to the various requireds of the European market through the apply of multiple indirect channels. A good example is how GEA Group relies on its locally based distributors in France to provide solutions that meet specific regional requirements. Additionally, as manufacturers continue to stress the importance of Energy efficiency and Sustainability, the benefits of indirect distribution channels will continue to improve and establish their dominance and growth within the European industrial refrigeration segment as a result of these two factors combined.

")

Looking for region specific data?

Download Free PDF

In the European industrial refrigeration market, Germany held revenue of around USD 1.6 billion in 2025 and is anticipated to grow at a CAGR of 7% from 2026 to 2035.

- In 2023, the value of the German pharmaceutical and bio-tech industries totals about USD 52 billion, according to the German federal minisattempt of economic affairs and climate action. The production of vaccines and biologics depconcludes significantly on having reliable cold-chain infrastructure throughout Germany. With EU regulations pertaining to greenhoapply gas emissions, there is a required for low-GWP refrigerants and energy efficient systems across all continents. It is the German companies GEA group USD 52 billion in sales in 2023 and Bitzer USD 1 billion dollars in sales annually that have been leading the charge in this area.

- Germany’s efforts to be an Indusattempt 4.0 leader and drive digitalisation is incorporating the apply of IoT enabled monitoring, predictive maintenance and automation within their refrigeration systems into German indusattempt. German company Siemens is on the leading edge of IoT technology adoption as well as investing heavily in logistics hubs, renewable sources of energy and sustainability initiatives, thus continuing to be an important contributor to growth within Europe’s industrial refrigeration market.

In the European industrial refrigeration market, U.K. held revenue of around USD 700 million in 2025 and is anticipated to grow at a CAGR of 6.5% from 2026 to 2035.

- The U.K market is driven by strong demand from food processing, cold storage, and retail sectors, which require reliable and energy-efficient systems to maintain product integrity. Government initiatives under the U.K.’s Net Zero Strategy and compliance with EU-aligned F-Gas regulations are accelerating the transition to low-GWP refrigerants and advanced energy-saving technologies. This regulatory push, combined with rising investments in smart refrigeration and heat recovery systems, is creating significant opportunities for modernization and sustainable innovation across the counattempt.

Europe Industrial Refrigeration Market Share

In 2025, the prominent manufacturers in Europe industrial refrigeration indusattempt are Danfoss, Johnson Controls, Emerson, Daikin Europe and Alfa Laval collectively held the market share of ~30%. These prominent players are proactively involved in strategic concludeeavors, such as mergers & acquisitions, facility expansions & collaborations, to expand their product portfolios, extconclude their reach to a broad customer base, and strengthen their market position.

- Danfoss consistently leads the market by driving innovation in energy-efficient refrigeration components and advanced digital solutions. The company builds substantial investments in smart controls, IoT-enabled monitoring, and variable-speed technologies, all designed to maximize system performance and significantly reduce energy consumption. Its strong focus on low-GWP refrigerants and strict compliance with EU F-Gas regulations firmly establish Danfoss as a sustainability pioneer.

- Johnson Controls leverages its extensive expertise in integrated building and refrigeration systems to deliver comprehensive, future-ready solutions that seamlessly integrate sustainability with advanced automation. The company strategically invests in AI-driven predictive maintenance, cloud-based monitoring platforms, and state-of-the-art control systems to enhance operational efficiency and reliability. Through tarobtained acquisitions, such as CO2 refrigeration specialists, Johnson Controls strengthens its portfolio of natural refrigerant solutions.

- Emerson maintains its competitive edge by focapplying on innovative compressor technology, IoT integration, and digital transformation. The company develops advanced hermetic and semi-hermetic compressors optimized for natural and low-GWP refrigerators, ensuring compliance with stringent EU regulations. Emerson’s innovative smart refrigeration solutions feature real-time monitoring, predictive analytics, and energy optimization tools, enabling customers to minimize downtime and reduce operational costs.

Europe Industrial Refrigeration Market Companies

Major players operating in the Europe industrial refrigeration indusattempt include:

- Alfa Laval

- Carel

- Daikin Europe

- Danfoss

- Emerson

- EVAPCO

- Frascold

- Haier

- Johnson Controls

- Kelvion

- LU-VE

- Mayekawa Europe

- MTA

- SCM Frigo

- Star Refrigeration

Daikin Europe distinguishes itself with innovative HVAC and refrigeration systems that prioritize energy efficiency and environmental compliance. The company invests heavily in low-GWP refrigerant technologies, hybrid cooling systems, and heat recovery solutions to meet and exceed EU climate tarobtains. By integrating IoT and AI into its systems, Daikin enhances reliability and performance through advanced features like remote monitoring and predictive maintenance.

Alfa Laval stands out with advanced heat transfer and fluid handling solutions that drive efficiency and sustainability in industrial refrigeration. The company focapplys on low-GWP refrigerant compatibility and energy-saving technologies, including plate heat exalterrs and hybrid cooling systems, to meet EU climate and decarbonization tarobtains. By embedding IoT-enabled monitoring and predictive maintenance features, Alfa Laval ensures optimized performance, reduced downtime, and compliance with stringent environmental regulations, reinforcing its leadership in sustainable refrigeration solutions.

Europe Industrial Refrigeration Indusattempt News

- In November 2025, Danfoss commissioned a new production line for BOCK brand compressors in Tianjin, China. These compressors utilize natural CO2 refrigerant, supporting low-GWP technology for cold chain logistics and industrial heat pump applications.

- In November 2025, Kaltra introduced advanced compact microchannel condensers designed for compatibility with low-GWP refrigerants (R454B, R32, R290), reinforcing its commitment to sustainability-focapplyd applications.

- In May 2025, Embraco launched innovative hermetic compressors optimized for hydrocarbons and low-GWP synthetics, supplemented by comprehensive position papers addressing the EU’s transition to sustainable refrigerants.

- In April 2025, GEA unveiled “NEXUS,” a cutting-edge modular compressor solution with integrated heat recovery, leveraging natural refrigerants to maximize energy efficiency and minimize carbon emissions.

- In January 2025, Emerson, a leading technology and engineering company, completed its acquisition of AspenTech, a premier software provider for process industries, in a transaction worth approximately USD 11 billion. This acquisition is set to significantly enhance Emerson’s capabilities in digital transformation and automation, enabling the delivery of integrated solutions that optimize energy consumption, improve operational efficiency, and drive superior performance.

The Europe industrial refrigeration market research report includes in-depth coverage of the indusattempt, with estimates & forecast in terms of revenue (USD Billion) and volume (Million Units) from 2022 to 2035, for the following segments:

Market, By Component

- Compressor

- Rotary screw compressor

- Centrifugal compressor

- Reciprocating compressors

- Diaphragm compressors

- Others

- Condenser

- Evaporator

- Controls

- Others

Market, By Refrigerant Type

- Ammonia (NH3)

- Freon (CFCs, HCFCs, HFCs)

- CO2 (Carbon Dioxide)

- Others

Market, By Capacity

- Below 500KW

- 0.5 – 1MW

- 1-5 MW

- Above 5MW

Market, By System configuration type

- Packaged and self-contained systems

- Remote and split systems

- Modular and containerized systems

Market, By Energy efficiency

- Class A (Highest Efficiency)

- Class B-C (High Efficiency)

- Class D-E (Medium Efficiency)

- Class F-G (Lower Efficiency)

Market, By Automation level

- Manual

- Semi-Automated Systems

- Fully Automated

Market, By End Use Indusattempt

- Food and beverage indusattempt

- Chemical and petrochemical indusattempt

- Pharmaceutical indusattempt

- Logistics and cold chain

- Others

Market, By Distribution Channel

The above information is provided for the following countries:

- Germany

- UK

- France

- Italy

- Spain