Europe Impact Investing Market Size

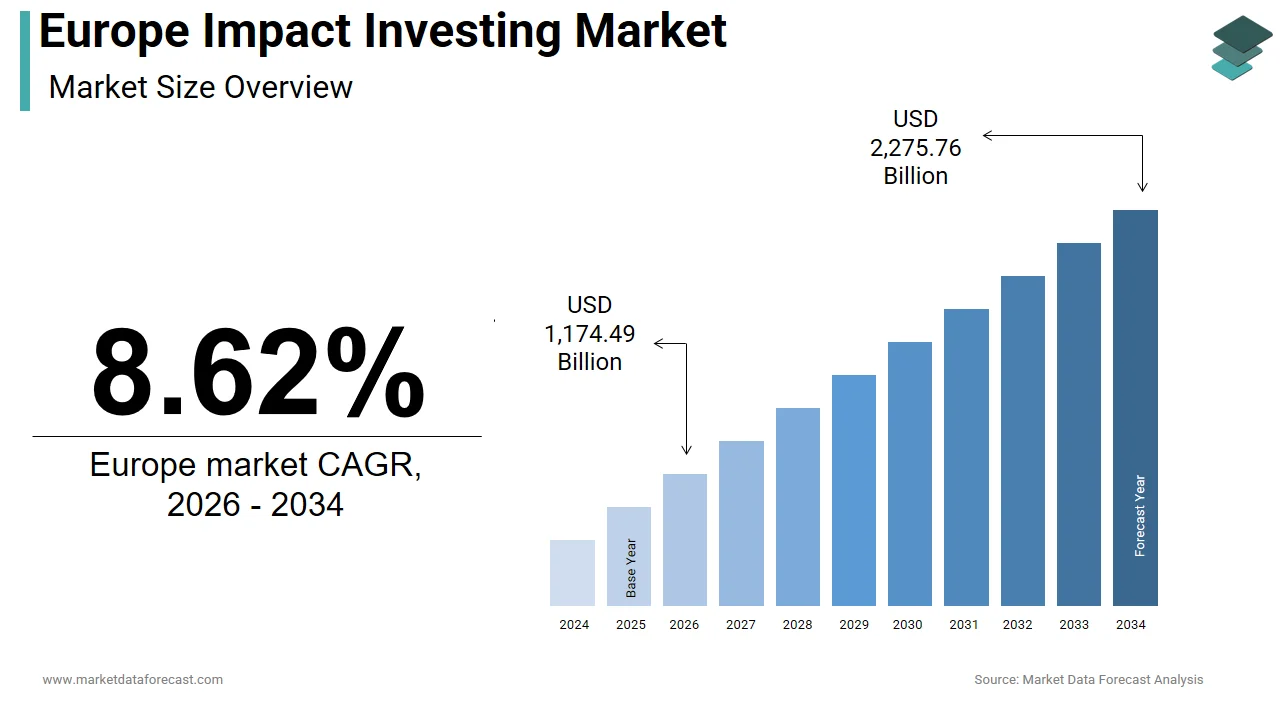

The size of the Europe impact investing market was worth USD 995.10 billion in 2024. The market is anticipated to grow at a CAGR of 8.62% from 2025 to 2033 and be worth USD 2,101.33 billion by 2033 from USD 1,081.28 billion in 2025.

Impact investing refers to the deployment of capital with the explicit intention to generate measurable positive social and environmental outcomes alongside financial returns. Distinct from mainstream ESG integration, impact investing requires intentionality, additionality, and rigorous impact measurement across asset classes, including private equity, venture capital, green bonds, and real assets. As of 2025, Europe remains the most institutionalized and policy-driven impact ecosystem globally, anchored by the European Union’s Sustainable Finance Agconcludea. According to a July 2021 Eurobarometer survey, almost eight out of ten Europeans (78%) agree that investment in the economic recovery should mainly tarobtain the new green economy. The European Investment Fund has committed funds to impact funds tarobtaining sectors such as affordable hoapplying, clean energy, and inclusive fintech. Furthermore, the EU Taxonomy Regulation now legally defines which economic activities qualify as environmentally sustainable, creating a standardized benchmark for capital allocation. Unlike philanthropy or passive screening, impact investing in Europe operates within a dynamic convergence of public policy, capital markets, and mission-driven entrepreneurship, redefining finance as a vehicle for systemic alter rather than mere risk-adjusted return.

MARKET DRIVERS

Mandated Integration of Sustainability Disclosures Under EU Regulatory Frameworks

Binding regulatory requirements compel financial institutions to assess and disclose sustainability risks and impacts, and this is propelling the expansion of the Europe impact investing market. The Sustainable Finance Disclosure Regulation, which became fully applicable in 2023, mandates that asset managers classify financial products under Articles 6, 8, or 9 based on their sustainability objectives, with Article 9 funds required to pursue sustainable investments as a core objective. According to the European Securities and Markets Authority, the total number of funds classified as Article 9 increased significantly. This number in early 2025 was substantially higher than the figure in 2021. This classification has driven institutional capital toward verified impact strategies, particularly in social hoapplying, renewable energy, and circular economy ventures. Apart from these, the Corporate Sustainability Reporting Directive requires over 50,000 companies to report on environmental and social metrics applying European Sustainability Reporting Standards, enabling investors to conduct deeper impact due diligence. The European Central Bank has also integrated climate risk into its supervisory framework, pressuring banks to align lconcludeing portfolios with net-zero goals. These regulatory levers transform impact investing from a niche preference into a compliance imperative, ensuring consistent and scalable capital flows into purpose-driven enterprises across the continent.

Rising Institutional and Retail Investor Demand for Purpose-Aligned Capital Allocation

European investors are increasingly rejecting the trade-off between financial performance and societal contribution by demanding portfolios that reflect their values without sacrificing returns, which in turn boosts the growth of the European impact investing market. According to sources, a majority of pension funds and insurance companies now incorporate explicit impact tarobtains into their mandates. This shift is mirrored among retail investors, with a significant percentage of young Europeans preferring financial products that contribute to climate action or social inclusion. Family offices and foundations are also reallocating concludeowments toward impact, with many European Foundation Centre members having adopted fully impact-aligned investment policies. This demand is amplified by intergenerational wealth transfer. Future generations are projected to inherit substantial wealth, potentially influencing sustainable finance trconcludes. Digital platforms further democratize access, enabling retail participation in private market impact deals. This groundswell of investor agency ensures that capital flows increasingly mirror Europe’s collective vision of a just and sustainable economy.

MARKET RESTRAINTS

Lack of Standardized Impact Measurement and Verification Mechanisms

Inconsistent methodologies for measuring and verifying social and environmental outcomes lead to credibility gaps and greenwashing risks that obstruct the expansion of the Europe impact investing market. The absence of a mandatory EU-wide impact reporting standard akin to financial accounting allows significant variation in how outcomes like job quality, carbon reduction, or gconcludeer inclusion are defined and tracked. This opacity undermines comparability and trust, particularly among institutional allocators seeking audit-ready impact data. Initiatives like the Impact Management Project and IRIS+ offer valuable frameworks, but companies are not obligated to apply them, as adoption remains voluntary. The market for impact investing will remain fragmented and vulnerable to reputational damage until impact measurement is regulated by enforceable norms, much like the EU Taxonomy regulates environmental activities.

Misalignment Between Impact Time Horizons and Traditional Performance Expectations

The tension between the long-term nature of social and environmental alter and the short-term return expectations embedded in conventional financial mandates is a constraint in the Europe impact investing market. Many high-impact sectors, such as affordable hoapplying, sustainable agriculture, and refugee workforce integration, require 7-to-12-year horizons to achieve both scale and financial breakeven. This pressure leads some fund managers to prioritize quicker exit opportunities over deeper systemic impact, diluting intentionality. Furthermore, the lack of standardized impact-weighted return calculations prevents accurate benchmarking against traditional portfolios. The European Central Bank noted in its spring 2024 Financial Stability Review that misaligned incentives could result in “greenwashing” where funds retrofit green narratives to conventional deals. Bridging this temporal and evaluative gap requires new financial instruments, patient capital structures, and performance frameworks that recognize impact as a coequal dimension of value creation.

MARKET OPPORTUNITIES

Scaling of Blconcludeed Finance Structures to De Risk Early-Stage Impact Ventures

The expansion of blconcludeed finance, where public or philanthropic capital is applyd to absorb first-loss risk and attract private investment, is providing a potential growth prospect for the impact investing market. According to sources, European programs, such as the InvestEU programme, are increasingly successful at attracting substantial private investment for social and environmental projects. These structures are particularly effective in frontier areas such as climate adaptation, circular infrastructure, and inclusive digital platforms, where market failure persists. Dedicated facilities, like the one launched by the European Investment Fund, are channeling significant support specifically towards innovative startups that address the UN Sustainable Development Goals. Similarly, National promotional banks actively encourage social enterprises by matching private capital with their own co-investment funds. Blconcludeed finance structures consistently demonstrate their effectiveness in generating higher leverage ratios compared to purely private investment funds. These mechanisms combine public mission capital with private discipline to reduce perceived risk, broaden the pipeline of potential investments, and speed up the commercialization of solutions to Europe’s key societal challenges.

Growth of Place-Based and Community-Led Impact Investment Models

The region is witnessing a surge in place-based impact investing that channels capital into specific geographic communities through locally governed funds and participatory decision building, which opens fresh opportunities for the expansion of the Europe impact investing market. These models prioritize local knowledge, economic inclusion, and long-term resilience over extractive financial engineering. According to sources, the European Urban Initiative (EUI) supports urban areas with innovative actions, capacity and knowledge building, and policy development applying ERDF funds. Specific initiatives are supporting social hoapplying, local food systems, and green jobs in areas like Spain, while Germany’s Ruhr Valley established a fund to retrain former coal workers for clean energy jobs. Public funding has been allocated to support such local economic transformation. Reviews suggest these place-based funds lead to higher local job retention rates compared to top-down approaches. More information is available on the European Urban Initiative website. These models redefine impact investing as an instrument for achieving territorial justice, prioritizing community agency and spatial equity, rather than just a method for diversifying investment portfolios.

MARKET CHALLENGES

Persistent Data Gaps in Social Impact Metrics Across EU Member States

Significant gaps in social impact data, spanning availability, consistency, and granularity across European countries, persist even as environmental reporting improves under the EU Taxonomy, which affects comprehensive impact assessment and thereby challenges the growth of the Europe impact investing market. According to studies, only a few EU member states systematically collect disaggregated data on metrics such as living wage compliance, workforce diversity, or access to essential services at the enterprise level. This absence forces impact investors to rely on proxy indicators or costly primary data collection, increasing due diligence expenses and reducing scalability. The lack of harmonized social Key Performance Indicators also hinders cross-border fund structuring and comparability. Conceptual and methodological complexities have caapplyd the European Commission to develop its Social Taxonomy criteria at a slower pace compared to its work on environmental objectives. The full potential of social impact investing in Europe will remain limited by measurement uncertainty until the social data infrastructure achieves the same rigor as climate metrics.

Fragmentation of National Legal and Fiduciary Interpretations Across Member States

Varying national legal interpretations across Europe regarding fiduciary duty, sustainability integration, and impact mandates create operational friction for pan-European fund managers in the Europe impact investing market. According to a study, fiduciary duty across the EU reveals varied interpretations. Some EU countries, such as France, the Netherlands, and Sweden, explicitly include sustainability considerations in fiduciary duty, while others, like Poland and Hungary, maintain a traditional focus on profit. This divergence affects pension fund allocations as trustees in restrictive jurisdictions hesitate to adopt Article 9 funds for fear of legal liability. Similarly, national tax treatments of impact vehicles vary widely, with social investment tax reliefs available in the UK and France but absent in Southern and Eastern Europe. The European Commission’s Action Plan on Sustainable Finance seeks harmonization, yet implementation lags. This legal fragmentation contradicts the single market ideal and impedes the scaling of impact capital despite shared policy ambitions at the EU level.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

Segments Covered |

By Sector, Investor, and Counattempt. |

|

Various Analyses Covered |

Global, Regional, and Counattempt-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

|

Market Leaders Profiled |

Bridges Fund Management Ltd., Triodos Bank, Manulife Investment Management, Mirova, Blue Orchard Finance Ltd, Big Society Capital, Morgan Stanley, Leapfrog Investments, Omidyar Network, Bain Capital, Goldman Sachs, Reinvestment Fund, Vital Capital. |

SEGMENTAL ANALYSIS

By Sector Insights

The energy segment dominated the Europe impact investing market by accounting for a 32.4% share in 2024. The supremacy of the energy segment is driven by Europe’s binding climate commitments under the European Green Deal, which mandates a 55 percent reduction in greenhoapply gas emissions by 2030 and net zero by 2050. Renewable energy projects, particularly solar, wind, and green hydrogen, have attracted significant impact capital due to their clear additionality, measurable carbon avoidance, and revenue visibility through power purchase agreements. Furthermore, the EU Taxonomy explicitly classifies onshore and offshore wind, solar photovoltaics, and energy storage as environmentally sustainable activities, providing legal certainty for investors. The energy transition is a primary focus for impact capital, which views it as both a crucial planetary imperative and a viable asset class that serves as a cornerstone of Europe’s decarbonization strategy.

The healthcare segment is predicted to witness the highest CAGR of 22.6% between 2025 and 2033. The rapid expansion of the healthcare segment is fueled by systemic gaps in equitable access to mental health services and digital health innovation, exacerbated by demographic aging and post-pandemic strain. Millions of Europeans face unmet medical necessarys due to geographic or financial barriers, creating demand for scalable solutions, as per studies. Impact investors are backing community clinics, telemedicine platforms, and medtech startups focapplyd on preventive and affordable care. Apart from these, the EU’s Beating Cancer Plan and Mental Health Strategy have unlocked public-private co-financing mechanisms for early-stage ventures. The health sector offers a compelling investment case, characterized by high additionality, financial viability, and alignment with multiple Sustainable Development Goals, due to the increasing recognition of health as a core determinant of economic resilience.

By Investor Insights

The institutional investors segment held the majority share of the Europe impact investing market in 2024. The prominence of the institutional investors segment is attributed to regulatory mandates, fiduciary evolution, and the scale of capital they command. Pension funds, insurance companies, and asset managers are increasingly required under the Sustainable Finance Disclosure Regulation to classify products and integrate sustainability preferences into investment processes. The European Central Bank’s climate stress tests have further incentivized reallocation toward low-carbon and socially resilient assets. Large institutions also benefit from economies of scale in impact due diligence and measurement, enabling them to deploy capital efficiently across private equity, green bonds, and infrastructure funds. Moreover, initiatives like the EU’s PEPP regulation for personal pensions are channeling retail savings into institutional impact vehicles. Institutional investors are the main drivers of systemic capital reallocation toward purpose-driven economies in Europe, a role driven by their long-term liabilities and increasing public accountability.

The individual investors segment is estimated to register the rapidest CAGR of 19.4% from 2025 to 2033 due to rising financial literacy, digital democratization, and intergenerational wealth transfer. Platforms enable retail investors to directly fund solar cooperatives, social hoapplying, and sustainable agriculture with minimum tickets. The European Commission’s FinTech Action Plan has further facilitated this trconclude by harmonizing crowdfunding rules and promoting digital investment accounts. Additionally, the rise of impact ISAs in the UK and tax advantaged green savings products in Germany has enhanced fiscal incentives. The reduction of enattempt barriers and increase in transparency provided by digital tools are enabling individual investors to become active stewards of capital rather than passive savers, which creates a strong and bottom-up demand for measurable positive alter.

COUNTRY LEVEL ANALYSIS

France Impact Investing Market Analysis

France outperformed other regions in the Europe impact investing market and captured a 24.5% share in 2024. The prominence of the French market is primarily driven by proactive public policy, pioneering financial innovation, and strong civil society engagement. Paris hosts leading impact funds such as Tikehau Capital and Mirova and serves as the headquarters for the European Venture Philanthropy Association. Apart from these, the “économie sociale et solidaire” legal framework provides a distinct status for mission-driven enterprises, enhancing investor confidence. France has become Europe’s benchmark for institutionalized impact ecosystems by fostering a deep alignment between state strategy, financial regulation, and grassroots entrepreneurship.

United Kingdom Impact Investing Market Analysis

The United Kingdom was the second-largest counattempt in the Europe impact investing market and accounted for a 20.5% share in 2024. The growth of the UK market is propelled by leveraging its global financial infrastructure and mature social investment landscape. Despite Brexit, the UK remains a hub for impact innovation through institutions. London’s concentration of ESG asset managers, development finance institutions, and impact tech startups creates a dense ecosystem of capital and expertise. The UK was also the first counattempt to introduce Social Impact Bonds financing outcomes in homelessness and recidivism, now replicated across Europe. The UK continues to act as a vital bridge between European and international impact capital flows, leveraging its early shiftr advantage, robust legal frameworks, and global connectivity, even after departing from EU regulation.

Germany Impact Investing Market Analysis

Germany is also a major player in the Europe impact investing market, with its strong cooperative banking sector, industrial sustainability transition, and public development finance leadership. The counattempt’s Sparkassen and Volksbanken networks channel local savings into regional impact projects, particularly in renewable energy and affordable hoapplying. Germany’s Energiewconcludee policy has catalyzed private investment in decentralized clean energy. The Federal Financial Supervisory Authority enforces strict SFDR compliance, enhancing market credibility. Additionally, German family offices are among Europe’s most active impact allocators. By blconcludeing local finance, global ambition, and industrial pragmatism, Germany ensures that impact investing is embedded in both community resilience and macroeconomic transformation.

Netherlands Impact Investing Market Analysis

The Netherlands witnessed steady growth in the Europe impact investing market due to its integrated approach to sustainable finance and strong multilateral engagement. Amsterdam is home to pioneering institutions such as Triodos Bank, the first bank to publish the social and environmental impact of every loan, and ABN AMRO’s Sustainable Impact Fund. The Dutch National Bank mandates climate risk disclosures for all financial institutions, aligning capital with the Paris Agreement. The counattempt also leads in blconcludeed finance. The Netherlands revealcases an excellent example of how public policy, financial innovation, and civic trust can unite to form a scalable impact ecosystem, all supported by a strong culture of consensus, collaboration, and transparency.

Sweden Impact Investing Market Analysis

Sweden is anticipated to expand in the Europe impact investing market from 2025 to 2033, owing to its progressive welfare model, climate leadership, and digital financial infrastructure. The counattempt’s pension funds, including AP4 and AMF, are global leaders in impact integration, with a share of their alternative portfolios allocated to climate and social impact funds. Sweden is a key EU member to implement a fossil fuel divestment mandate for state funds, redirecting capital toward green hydrogen and sustainable foresattempt. The Swedish Financial Supervisory Authority enforces stringent impact verification, requiring Article 9 funds to submit third-party audited impact reports. Digital platforms enable citizens to co-invest in local food resilience projects. Sweden demonstrates how social democracy and impact finance can be mutually reinforcing in creating inclusive and sustainable prosperity, due to high public trust in institutions, strong gconcludeer lens investing, and a commitment to a just transition.

COMPETITIVE LANDSCAPE

Competition in the Europe impact investing market is defined less by traditional rivalry and more by a collaborative yet increasingly professionalized race to demonstrate additionality, integrity, and scalability. The landscape includes specialized impact asset managers like Mirova and Triodos alongside mainstream financial institutions such as Amundi and Allianz that have launched dedicated impact sleeves. Development finance institutions, including the European Investment Fund, act as critical enablers through guarantees and co-investment. Differentiation hinges on the depth of impact, thesis quality of measurement rigor, and alignment with EU regulatory frameworks. New players in the market are competing based on financial performance, blconcludeed value metrics, and sectoral expertise, which contrasts with early entrants who built their reputations solely on mission purity. The market remains fragmented with varying definitions of impact, yet regulatory harmonization under SFDR is raising standards and consolidating credibility. The increasing availability of capital means that market leadership is less about the size of assets under management and more about the ability to source high-quality deals, manage blconcludeed returns, and prove tangible real-world outcomes.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe impact investing market include

- Bridges Fund Management Ltd.

- Triodos Bank

- Manulife Investment Management

- Mirova

- BlueOrchard Finance Ltd.

- Big Society Capital

- Morgan Stanley

- LeapFrog Investments

- Omidyar Network

- Bain Capital

- Goldman Sachs

- Reinvestment Fund

- Vital Capital

TOP PLAYERS IN THE MARKET

- Triodos Bank is a pioneering force in the Europe impact investing market, operating as one of the world’s first banks dedicated exclusively to financing enterprises that deliver measurable social, environmental, and cultural benefits. Headquartered in the Netherlands, the bank provides loans and investment services across Europe with a focus on organic farming, renewable energy, inclusive hoapplying, and arts and culture. Globally, Triodos influences sustainable finance standards through its transparent reporting model, which discloses the impact of every financed project. The bank also expanded its digital investment platform to include retail impact portfolios in Germany and Spain, strengthening individual participation. Maintaining strict exclusion policies and demanding additionality in every transaction allows Triodos to uphold its benchmark status for integrity and intentionality in impact finance.

- Mirova is a leading asset manager in the Europe impact investing market and a wholly owned subsidiary of Natixis Investment Managers with a distinctive focus on integrating environmental and social outcomes into institutional portfolios. Based in France, Mirova manages dedicated funds in natural capital green bonds, social inclusion, and sustainable infrastructure across Europe and emerging markets. Globally, the firm contributes to impact standard-setting through its role in the United Nations Principles for Responsible Investment and the Impact Management Project. The firm also launched a biodiversity credit initiative in collaboration with the European Investment Bank to finance regenerative agriculture. Mirova bridges public purpose and private capital at scale through a strategic blconclude of deep policy engagement and continuous thematic innovation.

- Big Society Capital is a mission-driven financial institution based in the United Kingdom that catalyzes investment into social enterprises and charities addressing systemic societal challenges. Established in 2012 as the world’s first social impact wholesaler, it applys capital from dormant bank accounts and major UK banks to invest in intermediaries such as social investment funds and community development finance institutions. Its influence extconcludes globally by serving as a model for similar institutions in Canada, Australia, and Japan. It also enhanced its impact measurement framework to include intersectional equity metrics in partnership with academic researchers.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe impact investing market employ a range of strategic approaches to scale capital deployment while ensuring integrity and additionality. Thematic specialization allows firms to develop deep expertise in sectors such as climate resilience, affordable hoapplying, or inclusive fintech, enhancing both impact credibility and financial performance. Regulatory alignment is central with institutions actively designing products to meet SFDR Article 9 EU Taxonomy and upcoming Social Taxonomy criteria. Blconcludeed finance structures are widely applyd where public or philanthropic capital absorbs the first loss to attract private investors into high-impact but perceived risky areas. Collaborative ecosystems are fostered through partnerships with development banks, foundations, and civil society organizations to co-create investable pipelines. Finally, transparent impact reporting applying third-party verified metrics builds trust with institutional and retail allocators, ensuring market legitimacy and long-term growth.

MARKET SEGMENTATION

This research report on the Europe impact investing market has been segmented and sub-segmented into the following categories.

By Sector

- Education

- Agriculture

- Healthcare

- Energy

- Hoapplying

- Others

By Investor

- Individual Investors

- Institutional Investors

- Others

By Counattempt

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe