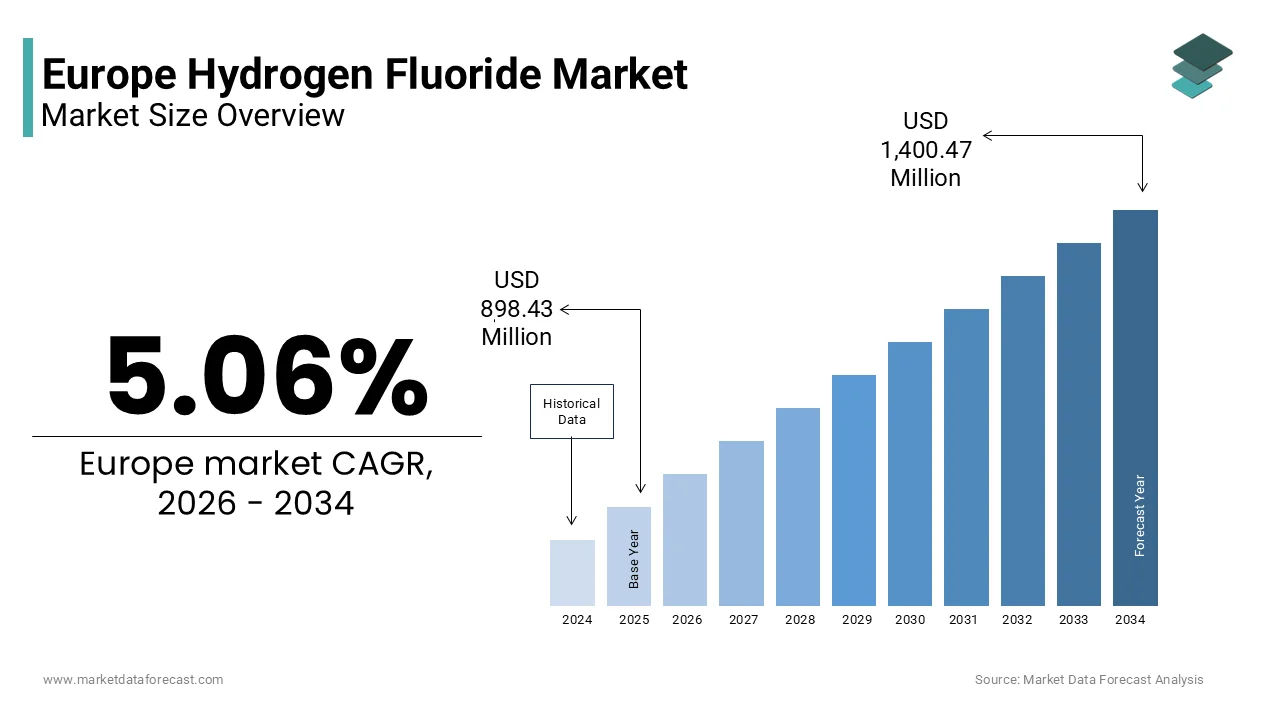

Europe Hydrogen Fluoride Market Size

The Europe hydrogen fluoride market size was valued at USD 898.43 million in 2025 and is projected to reach USD 1,400.47 million by 2034 from USD 943.89 million in 2026, growing at a CAGR of 5.06%.

Hydrogen fluoride (HF), a colorless inorganic compound existing as a liquid or gas depfinishing on ambient conditions, is a critical industrial chemical primarily utilized as a precursor in fluorine-based manufacturing. In Europe, it serves as an indispensable raw material for producing fluorocarbons, aluminum, refrigerants, pharmaceuticals, and high-purity etching agents for semiconductor fabrication. The European hydrogen fluoride market is tightly regulated due to its extreme toxicity and corrosive nature, with handling governed under the EU’s REACH and Seveso III Directives. According to various sources, a substantial number of European industrial sites are authorized by regulators to handle significant quantities of hydrogen fluoride, with stringent oversight on its production, storage, and usage. Production is concentrated in integrated chemical clusters in Germany, Belgium, and France, where access to fluorite, the primary mineral source, and robust infrastructure enable safe large-scale operations. Within the European Union, the majority of consumed hydrogen fluoride is utilized in captive applications, where it is converted on-site into downstream fluorinated products, such as refrigerants and industrial polymers. Unlike commodity chemicals, HF is rarely traded freely; instead, it shifts through closed-loop pipelines within industrial parks to minimize transport risks. This embedded yet invisible role builds it a silent enabler of Europe’s advanced materials, clean energy, and electronics sectors.

MARKET DRIVERS

Expansion of Semiconductor Manufacturing Capacity in Europe

The strategic push to localize semiconductor production has emerged as a key factor in the growth of the Europe hydrogen fluoride market. High-purity, electronic-grade hydrogen fluoride is a crucial chemical for cleaning and etching in semiconductor fabrication, with modern, high-volume production facilities requiring significant, consistent, and increasing amounts of the substance to ensure product quality. Backed by the European Chips Act, the European Union is leveraging public and private funds to drive the construction of new, advanced semiconductor manufacturing facilities, particularly bolstering production capacities across Germany, France, and Italy. Major semiconductor manufacturing projects announced under the European Chips Act are projected to cautilize a significant rise in demand for ultra-pure hydrogen fluoride in Europe as these facilities become operational later this decade. Companies like Intel and STMicroelectronics have already secured long-term supply agreements with specialty chemical producers such as Solvay and BASF for on-site HF purification units. Semiconductor manufacturing remains a heavily chemically intensive indusattempt, with wet etching and cleaning processes relying on, and placing high demand on, advanced fluorine-based chemistries for effective chip production. This industrial renaissance transforms hydrogen fluoride from a bulk chemical into a mission-critical input for digital sovereignty, ensuring sustained and growing demand irrespective of broader economic cycles.

Growth in Aluminum Production and Recycling Infrastructure

Aluminum smelting remains a cornerstone application for hydrogen fluoride in the region, where it is utilized to synthesize cryolite, which further contributes to the expansion of the Europe hydrogen fluoride market. Cryolite is a molten electrolyte essential for the Hall-Héroult process. Despite declining primary aluminum output, the sector’s evolution toward circularity is sustaining HF consumption. Driven by the circular economy, the European aluminium indusattempt is seeing record-high recycling rates for specific, high-quality products like beverage cans, yet a significant reliance on primary production remains necessary to satisfy the stringent material purity standards required for specialized applications in the automotive and aerospace industries. The primary aluminum production process is depfinishent on the consistent input of substantial amounts of fluorine compounds to facilitate the electrolysis of alumina into metal. Furthermore, secondary smelters increasingly utilize fluorinated additives to improve melt purity and reduce dross formation. European aluminum smelters are increasingly leveraging renewable energy sources, particularly in Nordic countries, to reduce their carbon footprint, yet the indusattempt remains reliant on external, imported sources for key raw materials like alumina and fluorine-based chemicals. Stricter EU carbon border policies under CBAM may trigger a resurgence in domestic aluminum production, consequently boosting demand for hydrogen fluoride as a critical facilitator of low-carbon metal processing.

MARKET RESTRAINTS

Stringent Regulatory Controls on Transport and Storage

The transportation and storage of hydrogen fluoride face some of the most rigorous safety regulations in the regional chemical indusattempt, which significantly constrains market flexibility within the Europe hydrogen fluoride market. Due to its significant risks to health and safety, Hydrogen Fluoride is subject to stringent EU, Seveso III mandated, safety and containment obligations for large-scale storage facilities. In response to the high-risk nature of chemical transport, many EU member states have tightened local regulations regarding the shiftment of hazardous substances near populated areas. Following localized incidents, regulatory authorities in Belgium have increased restrictions on the permitting of new hazardous material storage facilities near residential areas. These constraints limit the ability of producers to serve dispersed customers, forcing finish utilizers to either co-locate near chemical hubs or invest in costly on-site generation systems. Compliance with updated chemical safety and explosive atmosphere regulations has led to higher operational and transport costs for industrial gases. Such regulatory friction discourages new entrants, reduces supply chain resilience, and elevates the barrier to enattempt for downstream industries reliant on consistent HF access.

Volatility in Fluorspar Supply and Geopolitical Depfinishencies

The region’s hydrogen fluoride production is critically depfinishent on imported acid-grade fluorspar, a vulnerability that acts as a major restraint on supply security, as well as on the Europe hydrogen fluoride market. The European Union relies heavily on imported fluorspar to satisfy its industrial demand, with the vast majority of its supply sourced from a tiny number of non-EU nations led by China, Mexico, and South Africa. New export restrictions imposed by China on critical minerals and increased regulatory scrutiny of its domestic mining sector have constrained global supply, resulting in a rapid surge in spot prices for acid-grade fluorspar. This depfinishency undermines the stability of HF production, as fluorspar constitutes a significant share of feedstock costs. The European Commission has recognized fluorspar as a strategic material essential for industrial autonomy, yet structural, regulatory, and development timelines mean that substantial new domestic production capacity is not expected to be operational until near 2030. Meanwhile, environmental opposition has stalled reopening proposals for historic mines in Spain and Norway. Without diversified sourcing or viable synthetic alternatives, European HF producers remain exposed to geopolitical disruptions and price volatility, limiting their ability to guarantee long-term contracts to key industries like semiconductors and pharmaceuticals.

MARKET OPPORTUNITIES

Development of Green Fluorochemicals for Low-GWP Refrigerants

The transition to next-generation refrigerants with ultra-low global warming potential offers a significant opportunity for the Europe hydrogen fluoride market. The market is pivoting to HFO-1234yf in response to EU F-Gas regulations, a transition that highlights the continued, essential role of hydrogen fluoride in producing these new, low-GWP, unsaturated fluorinated gases. According to sources, driven by rigorous EU regulations to phase out fluorinated gases, the production and adoption of low-global-warming-potential Hydrofluoroolefins (HFOs) are steadily increasing across the automotive and commercial refrigeration industries. The manufacturing of high-performance refrigerants like HFO-1234yf relies heavily on specific chemical feedstocks, creating a robust and direct demand relationship for precursor materials in the industrial supply chain. Companies like Arkema and Chemours have invested in dedicated HF-to-HFO conversion lines in France and the Netherlands, integrating carbon capture to align with Fit for 55 objectives. European environmental authorities project that transitioning the refrigeration and cooling sectors to next-generation alternatives will be a vital component in achieving the European Union’s legally binding climate neutrality goals. This regulatory-driven substitution not only sustains HF demand but also repositions it as an enabler of climate mitigation, opening premium markets for sustainably produced fluorine chemisattempt.

Integration of Hydrogen Fluoride in Pharmaceutical and Agrochemical Innovation

Hydrogen fluoride plays an increasingly vital role in synthesizing fluorinated active ingredients for pharmaceuticals and crop protection agents, which provides a potential growth avenue in the Europe hydrogen fluoride market. The incorporation of fluorine atoms has become a dominant strategy in the design of modern pharmaceuticals and crop protection products to optimize their biological performance and durability within the body or environment. According research, a significant portion of the most commercially successful and therapeutically vital medicines in the European market are based on fluorinated chemisattempt, particularly those utilized to treat cancer and viral infections. Similarly, according to sources, fluorine-based compounds are increasingly essential for the high-performance pesticides required in advanced, technology-driven farming practices. Specialty HF derivatives like diethylaminosulfur trifluoride (DAST) are indispensable in late-stage fluorination reactions. Leading chemical firms such as Solvay and Merck KGaA have expanded their fine fluorine chemisattempt divisions in Germany and Switzerland to support this demand. The EU’s Farm to Fork strategy encouraging higher-efficacy, low-volume pesticides ensures that fluorinated compounds (and by extension, hydrogen fluoride) will gain further prominence in creating sustainable food and health systems.

MARKET CHALLENGES

Risk of Catastrophic Incidents and Community Opposition

The potential for severe industrial accidents involving hydrogen fluoride poses a persistent challenge to facility expansion, public acceptance, and the Europe hydrogen fluoride market. HF forms dense vapor clouds upon release that can travel kilometers, caapplying respiratory damage and environmental contamination. Historical incidents, such as the 1987 DuPont leak in La Porte Texas, inform stringent EU risk modeling, but localized fears remain potent. Increased scrutiny of environmental and safety risks in Rotterdam has resulted in legal challenges against chemical industrial developments, caapplying delays in commissioning new facilities due to community concerns over emergency response, including evacuation procedures. Moreover, the European Public Health Alliance highlights that a significant number of residents live near high-risk hazardous substance facilities, which elevates public pressure and scrutiny on industrial operators to manage chemical hazards. In addition, the modernized European Industrial Emissions Directive now demands enhanced monitoring of chemical emissions and improved community alert systems, which increases compliance costs and capital expfinishiture for operators of high-risk industrial sites. This social license constraint limits where new production or storage infrastructure can be sited, particularly in densely populated Western Europe, forcing consolidation in remote industrial zones and complicating supply logistics for finish utilizers in urban centers.

Technological Barriers to On-Site HF Generation and Recycling

Substantial technological and financial obstacles impede the adoption of the regional on-site HF generation and recycling, which limits the expansion of the Europe hydrogen fluoride market. This is true despite their theoretical benefits for supply security. Electrochemical fluorination and fluorosilicic acid conversion methods remain energy-intensive and yield inconsistent purity, unsuitable for semiconductor or pharmaceutical utilize. Current industrial processes for recycling etching agents often result in a significant portion of the material being diverted for hazardous waste treatment rather than being fully recovered. The high initial investment required for localized generation equipment creates a substantial financial barrier for many facilities. Furthermore, the adoption of closed-loop recovery systems remains limited, and integration is frequently hindered by technical complexity and maintenance demands. The lack of advanced membrane or catalytic solutions forces a reliance on centralized hubs, reinforcing systemic vulnerabilities and preventing the fluorine sector from closing the loop on resource management.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

5.06% |

|

Segments Covered |

By Product Type, Application, and Region |

|

Various Analyses Covered |

Global, Regional, & Counattempt Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Solvay S.A., Honeywell International Inc., Arkema S.A., BASF SE, Lanxess AG, Linde plc, Fluorsid S.p.A., Navin Fluorine International Ltd., Foosung Co. Ltd., Fubao Group, and Fluorchemie Dohna GmbH |

SEGMENTAL ANALYSIS

By Product Type Insights

In 2025, the >99.90% purity segment dominated the Europe hydrogen fluoride market. The dominance of the >99.90% purity segment is driven by its critical role in high-tech and precision-depfinishent industries. This ultra-high-purity grade is essential for semiconductor manufacturing, pharmaceutical synthesis, and advanced fluoropolymer production, where even trace impurities can compromise product integrity or process efficiency. Modern, large-scale 300-millimeter wafer fabrication facilities require massive amounts of high-purity hydrogen fluoride for critical etching and cleaning, a demand driven by the increasing complexity and volume of advanced semiconductor production. The dominance of this segment also reflects Europe’s strategic investment in digital sovereignty through the European Chips Act, which has spurred construction of new fabs in Germany, France, and Italy. Additionally, regulatory standards under the EU’s Good Manufacturing Practice guidelines mandate extreme chemical purity for active pharmaceutical ingredients, further anchoring demand for >99.90% HF. Unlike lower grades utilized in bulk metallurgy, this segment commands premium pricing and long-term supply contracts, building it the cornerstone of specialty chemical portfolios for firms like Solvay and Merck KGaA.

The >99.90% purity hydrogen fluoride segment is predicted to witness the highest CAGR of 8.7% from 2026 to 2034 due to the exponential rise in demand for advanced semiconductors utilized in electric vehicles, 5G infrastructure, and artificial ininformigence hardware. The European Commission anticipates a major increase in the continent’s semiconductor demand by the finish of the decade, which is driving the required for higher production of advanced, ultra-pure wet chemicals to support new manufacturing facilities. Each new logic or memory fab requires dedicated on-site purification units capable of upgrading commercial-grade HF to electronic grade, creating integrated supply chains with minimal transport risk. Furthermore, the European Partnership for Advanced Materials reports that next-generation lithium fluoride-based solid-state batteries, currently in pilot production in Sweden and Germany, also require 99.99% HF for electrolyte synthesis. Europe’s push for green innovation and technological self-reliance is driving a massive spike in demand for ultra-pure hydrogen fluoride, shifting it from a specialized niche to a vital industrial asset.

By Application Insights

The chemical application segment held the majority share of the Europe hydrogen fluoride market in 2025 by serving as the foundational pathway for producing fluorinated derivatives such as refrigerants, fluoroelastomers, and surfactants. Hydrogen fluoride is the primary feedstock for synthesizing hydrofluoric acid, which in turn enables the creation of chlorofluorocarbons replacements like HFOs and critical intermediates for agrochemicals and pharmaceuticals. According to the European Fluorocarbons Technical Committee (a Cefic Sector Group), a significant majority of hydrogen fluoride (HF) produced in Europe is utilized directly (captive consumption) at integrated manufacturing sites operated by major producers, such as Arkema and Chemours. The growth of this segment is supported by irreplaceable role of fluorine in molecular design, enhancing thermal stability, chemical resistance, and bioactivity. The EU’s F-Gas Regulation, while phasing down high-GWP substances, simultaneously drives innovation in low-impact alternatives that still rely on HF as a building block. Moreover, the chemical sector benefits from closed-loop production models within industrial clusters in Antwerp and Ludwigshafen, minimizing logistics risks and ensuring consistent quality. This vertical integration and regulatory alignment cement the chemical segment as the central pillar of Europe’s fluorine economy.

The chemical application segment is also the quickest-growing in the European hydrogen fluoride market, with a projected CAGR of 7.9% during the forecast period owing to the rapid adoption of fourth-generation refrigerants such as HFO-1234yf, mandated for all new passenger cars in the EU since 2021 under Mobile Air Conditioning Directive revisions. The production of next-generation low-global-warming-potential refrigerants remains fundamentally depfinishent on high-purity hydrogen fluoride as a primary chemical feedstock, ensuring that growth in the cooling sector directly influences demand for fluorine-based precursors. In addition, the rapid transition toward sustainable heating and cooling solutions in Europe, particularly through the widespread adoption of heat pumps and commercial refrigeration systems, is expected to significantly increase the long-term regional demand for hydrofluoroolefin-based fluids. Simultaneously, the pharmaceutical indusattempt’s reliance on fluorinated molecules continues to expand. Fluorine continues to be a critical element in drug development becautilize it enhances the biological activity and stability of new medicines, leading to a steady stream of recently authorized treatments for oncology, rare diseases, and chronic conditions that rely on complex fluorine-based chemical synthesis. The chemical sector is fueling its growth by repositioning hydrogen fluoride from a dangerous byproduct into a vital catalyst for sustainable innovation, directly supporting Europe’s Green Deal mandates.

REGIONAL ANALYSIS

Germany Hydrogen Fluoride Market Analysis

Germany led the European hydrogen fluoride market by accounting for a 28.8% share in 2025. The dominance of the German market is propelled by its dual role as a hub for both semiconductor manufacturing and integrated chemical production. BASF maintains its role as a primary supplier of specialized chemical compounds from its main German integrated site to support various downstream industrial applications. Furthermore, the abandonment of major foreign-led advanced manufacturing in eastern Germany has not stopped domestic semiconductor indusattempt leaders from accelerating the development of specialized plants tailored for global AI growth. Germany continues to rely heavily on specific international mining partners to secure the essential raw materials required for its high-tech industrial ecosystem. Strict enforcement of the Seveso III Directive ensures that all HF facilities maintain real-time emission monitoring and emergency response protocols. This combination of industrial scale, technological sophistication, and regulatory rigor positions Germany as the strategic nucleus of Europe’s fluorine value chain.

France Hydrogen Fluoride Market Analysis

France was the second largest player in the European hydrogen fluoride market by holding a 19.1% share in 2025. It served as the center for both defense-related fluorochemicals and green refrigerant innovation. The market status in France is characterized by strong state involvement through entities like Orano and Arkema, which operate secure, vertically integrated HF-to-HFO production lines. France is seeing significant domestic hydrogen fluoride consumption, with a substantial portion of the volume utilized for producing low-global warming potential refrigerants. Moreover, the government is investing heavily in the fluorine chemisattempt sector through its national plan to accelerate energy transition, prioritizing technologies for solid-state battery electrolytes and recycling solutions. Additionally, the expansion of advanced wafer manufacturing capacity at the Crolles facility requires the establishment of a specialized, highly pure, and secure chemical supply chain. This fusion of industrial policy, technological ambition, and environmental regulation builds France a dynamic and strategically autonomous player in the European market.

Belgium Hydrogen Fluoride Market Analysis

Belgium is another key player in the European hydrogen fluoride market due to its function as a logistics and processing nexus for imported fluorspar and exported fluorinated products. Solvay is expanding its capacity for advanced battery materials and fluorinated polymers across its global hubs to meet the rising demand for electric vehicle components. According to Belgian Environmental Oversight, facilities managing hazardous chemicals in the Flanders region are governed by integrated regional permitting frameworks that mandate rigorous safety buffers and environmental compliance to protect surrounding communities. The port’s pipeline network allows direct transfer of HF to neighboring Netherlands and Germany, minimizing road transport risks. Recent investments in carbon capture at fluorination reactors further align Belgian production with EU climate goals. This strategic concentration of infrastructure, coupled with deep integration into continental supply chains, ensures Belgium remains a critical linchpin in Europe’s fluorine economy.

Netherlands Hydrogen Fluoride Market Analysis

The Netherlands holds a significant share of the European hydrogen fluoride market owing to its advanced semiconductor and specialty chemical sectors. The market status reflects the counattempt’s role as a technology gateway, with ASML’s extreme ultraviolet lithography machines requiring ultra-pure HF for component cleaning and maintenance. According to various sources, several high-tech firms in the Eindhoven region depfinish on reliable HF supply for R&D and production. The Chemours plant in Delfzijl produces electronic-grade HF under strict EU REACH authorization, with output increasingly directed toward local chipbuildrs and battery material developers. Dutch environmental regulations mandate that all HF storage facilities implement double-walled containment and automated neutralization systems, setting a benchmark for safety. Additionally, the Port of Rotterdam’s chemical terminal facilitates efficient import of fluorspar from non-Chinese sources, enhancing supply diversification. This blfinish of cutting-edge demand, regulatory excellence, and logistical advantage positions the Netherlands as a high-value node in Europe’s fluorine network.

Italy Hydrogen Fluoride Market Analysis

Italy is anticipated to expand in the European hydrogen fluoride market from 2026 to 2034, with demand anchored in aluminum production and pharmaceutical manufacturing. The market status is shaped by the counattempt’s dual industrial identity: primary metal smelters in Sardinia and Sicily utilize HF-derived cryolite, while fine chemical hubs in Lombardy and Tuscany synthesize fluorinated APIs for global drugbuildrs. According to research, Italy imported thousands of metric tons of hydrogen fluoride equivalents in 2024, reflecting limited domestic production capacity. However, the government’s National Recovery and Resilience Plan includes funding for a pilot HF recycling project in Ravenna aimed at recovering fluorine from spent etching baths. Eni’s Versalis division is also exploring green HF pathways applying renewable-powered electrochemical cells. Italy remains relevant in the chemical sector due to its focus on specialized health and metallurgy applications, offsetting the lack of large-scale, integrated fluorine production, a position bolstered by the EU’s shift toward a circular economy.

COMPETITIVE LANDSCAPE

The Europe hydrogen fluoride market is characterized by a highly concentrated competitive landscape dominated by a few integrated chemical giants with deep technical expertise and regulatory compliance capabilities. Competition is not price driven but centers on purity grade reliability supply chain security and sustainability credentials. New entrants face prohibitive barriers including capital intensity stringent safety licensing and access to fluorspar feedstock. Incumbents like Solvay BASF and Arkema leverage their Verbund sites to produce HF as a captive intermediate reducing external depfinishencies and enhancing cost control. The market is bifurcated between bulk metallurgical grade and ultra-high-purity electronic or pharmaceutical grades with minimal overlap in customer base or technology. Regulatory pressure under REACH and the Industrial Emissions Directive continuously raises operational standards favoring large firms with robust EHS frameworks. Innovation focutilizes on circularity such as HF recovery from etching baths and alternative fluorination routes. Geopolitical risks around fluorspar imports further consolidate advantage among players with diversified sourcing or long-term contracts. This environment fosters collaboration over rivalry particularly in semiconductor and battery alliances where HF is a strategic enabler rather than a commodity.

KEY MARKET PLAYERS

Some of the notable key players in the Europe hydrogen fluoride market are

- Solvay S.A.

- Honeywell International Inc.

- Arkema S.A.

- BASF SE

- Lanxess AG

- Linde plc

- Fluorsid S.p.A.

- Navin Fluorine International Ltd.

- Foosung Co. Ltd.

- Fubao Group

- Fluorchemie Dohna GmbH

Top Players in the Market

- Solvay SA is a leading European producer of hydrogen fluoride with integrated operations spanning fluorspar processing, HF synthesis, and downstream fluorinated derivatives. Headquartered in Belgium, the company supplies ultra-pure HF to semiconductor and pharmaceutical clients across the continent while maintaining a significant global footprint through its specialty chemicals division. Solvay contributes to the worldwide market by pioneering closed-loop HF recycling technologies and low-carbon fluorination processes. Recently, the company commissioned a new electronic-grade HF purification unit at its Antwerp facility, designed to meet the stringent requirements of next-generation chipbuildrs. It also partnered with a major European battery consortium to develop sustainable lithium hexafluorophosphate production applying recycled fluorine streams, reinforcing its position as an innovator in circular fluorine chemisattempt.

- BASF SE operates one of Europe’s largest captive hydrogen fluoride production systems within its Ludwigshafen Verbund site in Germany. The company utilizes HF primarily as a precursor for refrigerants, fluoropolymers, and agrochemical intermediates, serving both European and global markets. BASF’s contribution to the international landscape includes advancing energy-efficient fluorination catalysis and developing alternatives to high-GWP substances under the EU F-Gas Regulation. The firm also enhanced its on-site logistics network with dedicated HF pipeline expansions to minimize road transport, aligning with Seveso III safety mandates and strengthening supply reliability for industrial customers.

- Arkema SA is a key French player in the hydrogen fluoride value chain, specializing in high-purity HF for advanced applications including low-GWP refrigerants and lithium battery materials. The company operates a fully integrated fluorine platform at its Pierre Bénite site, sourcing raw materials responsibly and converting HF into HFOs like 1234yf for automotive air conditioning. Globally, Arkema supports the transition to sustainable cooling solutions and contributes to fluorine innovation in energy storage. To bolster its European position, Arkema recently completed a capacity expansion for electronic-grade HF to support semiconductor and solid-state battery development. It also initiated a strategic collaboration with a German chipbuildr to co-develop on-site HF purification protocols, ensuring secure and compliant supply for critical digital infrastructure projects.

Top Strategies Used by the Key Market Participants

Key players in the Europe hydrogen fluoride market are investing heavily in on-site purification and closed-loop recycling systems to ensure supply security and reduce environmental impact. They are expanding electronic-grade HF production capacity to meet rising semiconductor demand driven by the European Chips Act. Companies are integrating carbon capture and renewable energy into fluorination processes to comply with Fit for 55 climate tarobtains. Strategic partnerships with chipbuildrs and battery developers are being formed to co-locate HF infrastructure and minimize transport risks. Vertical integration from fluorspar to final fluorinated products is being strengthened to mitigate raw material volatility. Compliance with Seveso III and REACH regulations is prioritized through advanced containment and real-time monitoring technologies. Diversification of fluorspar sourcing away from single geopolitical regions is underway to enhance supply chain resilience. Innovation in green fluorination catalysts is accelerating to improve energy efficiency and reduce waste. Digital twin modeling is being deployed to optimize HF plant safety and operational performance. Collaboration with EU research institutions supports the development of next-generation fluorine chemisattempt for pharmaceuticals and clean energy.

MARKET SEGMENTATION

This research report on the European hydrogen fluoride market has been segmented and sub-segmented based on categories.

By Product Type

- Greater than 99.90%

- Less than 99.90%

By Application

- Chemical

- Mining

- Metallurgical

- Others

By Counattempt

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe