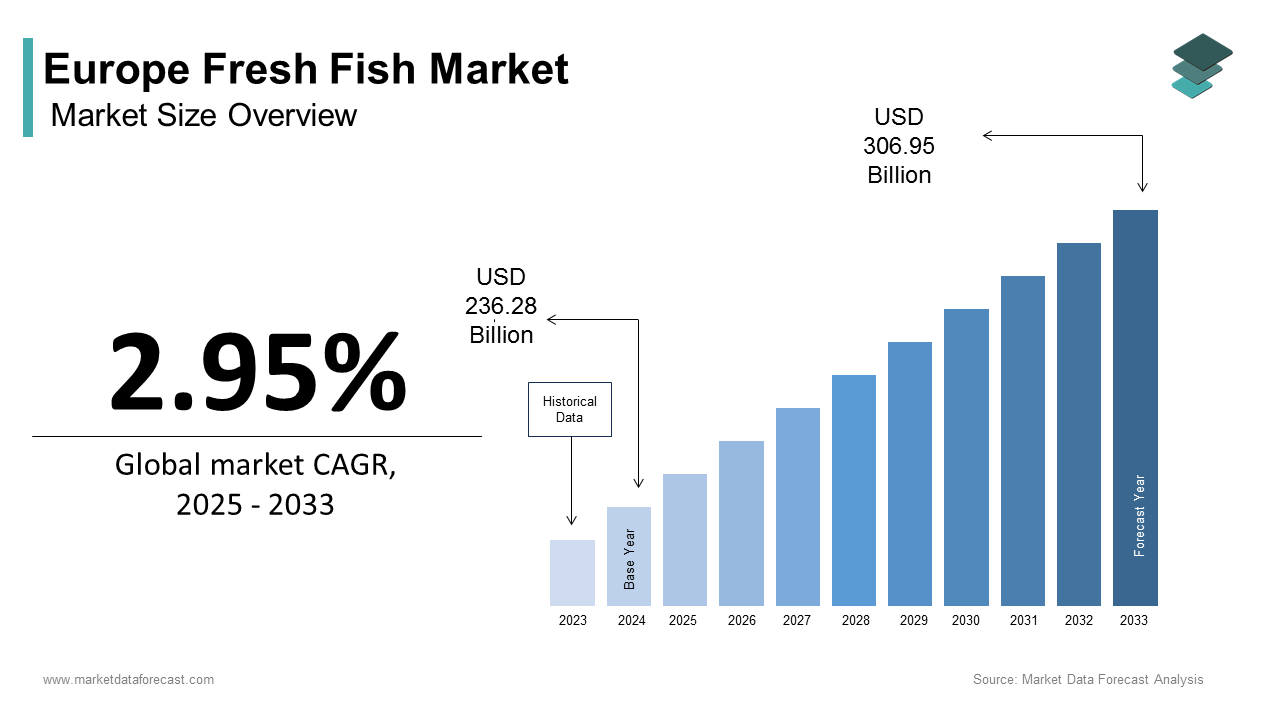

Europe Fresh Fish Market Size

The Europe fresh fish market size was calculated to be USD 236.28 billion in 2024 and is anticipated to be worth USD 306.95 billion by 2033, from USD 243.25 billion in 2025, growing at a CAGR of 2.95% during the forecast period.

Fresh fish refers to fish that have been recently caught or harvested and have not undergone any preservation beyond chilling to maintain their original qualities intact without deterioration. This market is deeply interwoven with coastal economies, maritime heritage, and evolving dietary norms across the continent. National consumption patterns vary significantly, with Portugal and Spain leading at over 50 kilograms per person per year, while Central European countries like Germany and Poland remain below the EU average. Supply chains range from tiny-scale day boats landing directly at local fish markets to large integrated processors serving supermarket chains under strict cold chain protocols. The interplay of ecological stewardship, consumer health awareness, and logistical precision defines the contemporary structure of Europe’s fresh fish ecosystem.

MARKET DRIVERS

Strong Consumer Preference for Fresh Over Processed Seafood

European consumers exhibit a pronounced and finishuring preference for fresh fish over frozen or canned alternatives, which propels the growth of the Europe fresh fish market. This is driven by sensory expectations, culinary tradition, and perceived nutritional superiority. This preference is institutionalized in national dietary guidelines, with France’s Program National Nutrition Santé recommfinishing two servings of fish per week, preferably fresh and locally sourced. Retailers reinforce this demand through live counters, ice bed displays, and same-day delivery promises, with supermarkets in Italy and Spain dedicating space to fresh fish sections, as per sources. Moreover, the rise of pescatarian and Mediterranean diets has elevated fish to a protein staple. This cultural and health-anchored demand ensures consistent pull through the supply chain, sustaining premium positioning and minimizing reliance on value-added processing.

Integration of Traceability and Origin Transparency Systems

The demand for verifiable provenance and ethical sourcing has become a major factor driving the expansion of the Europe fresh fish market. A majority of consumers across Europe place strong importance on knowing where and how their fish is caught, often revealing a preference for sustainably certified options, according to sources. This focus on transparency is reinforced by European Union regulations that require detailed traceability from fishing vessels to retail shelves, covering specifics such as species, origin, and production method, as per research. Major retailers like Carrefour and Edeka have implemented digital QR code systems, allowing shoppers to access real-time data on vessel identity, catch date, and stock health status. These systemic shifts transform traceability from a compliance burden into a competitive differentiator, enhancing consumer trust and brand loyalty in an increasingly conscientious marketplace.

MARKET RESTRAINTS

Stringent Quota Restrictions Under the Common Fisheries Policy

The European Union’s Common Fisheries Policy imposes scientifically derived annual catch limits that constrain the growth of the Europe fresh fish market. These restrictions directly impact fishers’ livelihoods and market availability, with Spanish and French fleets reporting 12 to 18 percent fewer landings of regulated species between 2021 and 2023, according to national fisheries ministries. While essential for long-term stock viability, these measures create supply gaps that elevate prices and increase reliance on imports from non-EU countries, which account for a portion of EU fish consumption, as per sources. The tension between ecological prudence and market stability remains a structural restraint on the fresh fish sector’s growth potential.

High Perishability and Cold Chain Vulnerabilities

It is among the most perishable food commodities, which in turn restricts the expansion of the Europe fresh fish market. It has a typical shelf life of only three to five days under optimal refrigeration, posing significant logistical and economic challenges. In developed markets, sensor analyses from distribution networks in the Netherlands indicated that a noticeable share of retail deliveries faced brief but important temperature fluctuations during the final stage of transport, according to sources. These breaches accelerate spoilage, trigger safety rejection, and erode consumer confidence. Investment in real-time monitoring, insulated packaging, and decentralized processing remains uneven across the EU, hindering systemic progress toward the Farm to Fork tarreceive of halving food waste by 2030 and constraining the sector’s operational resilience.

MARKET OPPORTUNITIES

Expansion of Aquaculture for High-Demand Species

Regional aquaculture is emerging as a strategic buffer against wild catch volatility by producing consistent volumes of premium fresh fish such as sea bass, sea bream, mackerel, nd trout, which generates potential opportunities for the growth of the Europe fresh fish market. Furthermore, the EU’s Strategic Guidelines for Sustainable Aquaculture prioritize species with high consumer demand and low environmental impact, aligning production with market requireds. This controlled production model not only enhances supply security but also meets stringent welfare and feed sustainability criteria increasingly demanded by European consumers.

Growth of Direct-to-Consumer and Short Supply Chain Models

Alternative distribution channels such as fish box subscriptions, farm gate sales, and digital fishmongers are gaining traction by offering superior freshness, transparency, and support for local fishers, and this provides fresh opportunities for the expansion of the Europe fresh fish market. Also, there has been an increase in direct fish sales across Western Europe, with platforms connecting consumers to day boat landings within 24 hours. These models reduce handling steps, cut waste, nd return higher revenue to fishers compared to traditional auction routes, as per studies. Urban consumers, particularly in Germany and Sweden, are driving adoption. Municipal policies further support this shift, with cities like Barcelona and Copenhagen providing grants for community fish hubs that integrate landing, processing, and retail. When the value chain is collapsed, these initiatives are able to enhance quality control, strengthen coastal economies, and align with EU goals for resilient localized food systems.

MARKET CHALLENGES

Labor Shortages in Post-Harvest Processing and Distribution

Acute and persistent shortages of skilled labor in vital post-harvest roles, including gutting, filleting, grading, and cold chain logistics, are slowing down the expansion of the Europe fresh fish market. The European Commission estimates that the EU requires substantial seasonal and permanent workers annually for fish processing, yet recruitment exists in key hubs. The United Kingdom’s departure from the EU exacerbated this crisis. Many tiny processors lack the capital to automate delicate tquestions like hand filleting, leaving them vulnerable to throughput bottlenecks and quality inconsistencies. The sector’s ability to maintain a consistent supply and meet premium quality standards remains fundamentally constrained without structural solutions like vocational training partnerships, revised immigration pathways, or modular automation.

Regulatory Fragmentation in Import Certification and Health Controls

Significant disparities persist in national implementation of import health checks and certification protocols, creating delays and compliance uncertainty for non-EU suppliers, which in turn holds back the growth of the Europe fresh fish market. These delays directly impact freshness, with every 12-hour hold increasing spoilage risk, as per studies. Furthermore, third-counattempt exporters must navigate divergent national requirements for labeling allergen declarations and cold chain documentation even after EU-level approval. The administrative friction inflates costs, reduces predictability, and discourages reliable supply from sustainable non-EU fisheries, thereby limiting consumer choice and market resilience in a region heavily depfinishent on imports.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

2.95% |

|

Segments Covered |

By Product, Form, Distribution Channel, and Region. |

|

Various Analyses Covered |

Global, Regional, & Counattempt Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

North America, Europe, APAC, Latin America, Middle East & Africa |

|

Market Leaders Profiled |

Mowi ASA, Royal Greenland A/S, Lerøy Seafood Group ASA, Nomad Foods Ltd., Bolton Group, Thai Union Group PCL, Young’s Seafood Ltd., Marine Harvest, Pelagia AS, Parlevliet & Van der Plas, Nueva Pescanova Group, Iceland Seafood International, Fripur S.A. |

SEGMENTAL ANALYSIS

By Product Insights

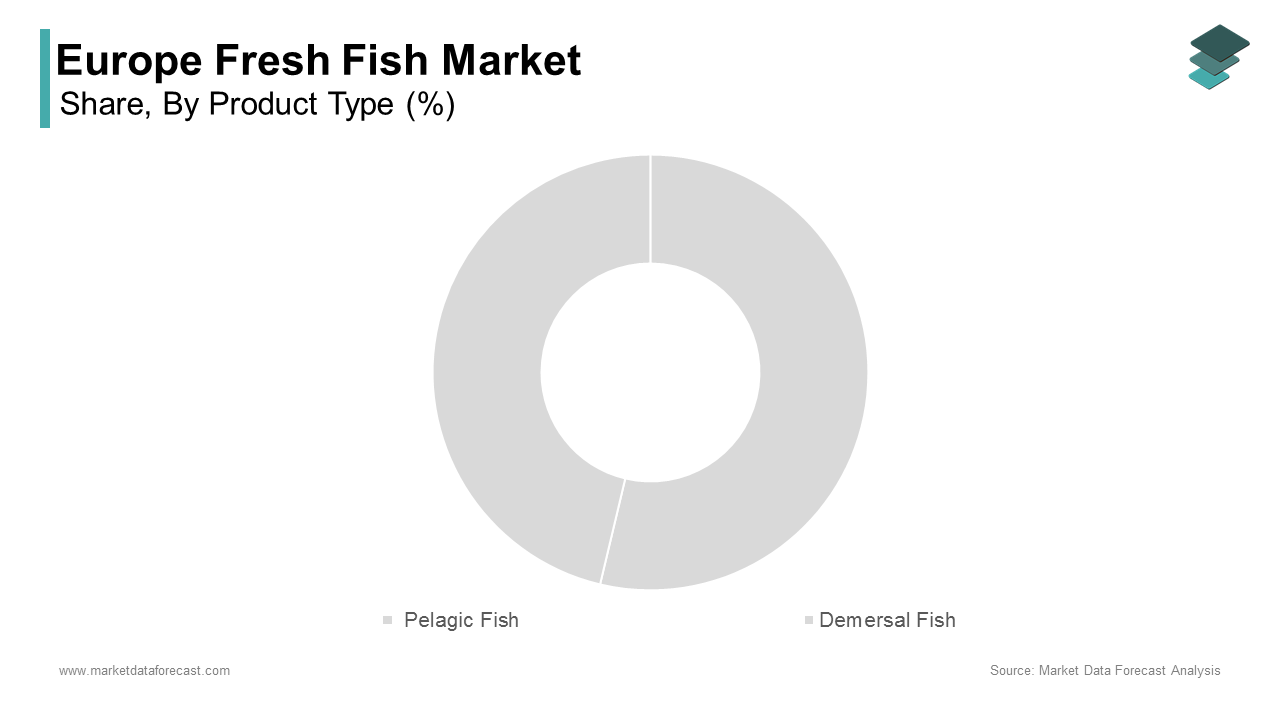

The pelagic fish segment held a prominent share of 62.7% of the Europe fresh fish market in 2024. The prominence of the pelagic fish segment is driven by their abundance, schooling behavior, and suitability for large-scale sustainable harvesting. Species such as mackerel, herrings, and sardines dominate landings. These fish thrive in open waters and are less vulnerable to seabed disruption, creating them compliant with EEU ecosystem-based fisheries management principles. Pelagics also align with public health guidance. Furthermore, pelagic fisheries operate under robust multiannual management plans. This combination of ecological resilience, nutritional value, and regulatory stability ensures pelagic fish remain the backbone of Europe’s fresh seafood supply.

The demersal fish segment is on the rise and is expected to be the quickest-growing segment in the global market by witnessing a CAGR of 3.8% from 2025 to 2033. The rapid expansion of the demersal fish segment is propelled by premiumization culinary demand and recovery of key stocks. Species such as sea bass, sea brebreamcod and sole command higher prices and feature prominently in restaurant menus and gourmet retail. As per research, Europe has experienced a steady rise in the sale of fresh demersal fish, with Italy and France remaining among the most active consumer markets. This positive trfinish has been strengthened by the recovery of North Sea cod stocks, which have reached sustainable fishing levels after years of conservation efforts, according to sources. Consumer willingness to pay premiums fuels investment in selective low-impact gear and traceability. As sustainability and taste converge, demersal fish transition from niche luxury to mainstream aspirational protein.

By Form Insights

The fresh fish segment was the largest in the Europe fresh fish market and accounted for a significant share in 2024. Deep-seated consumer preferences for sensory quality and culinary authenticity are driving the growth of the fresh fish segment. Europeans consistently rank freshness as the top purchase criterion. This cultural norm is reinforced by retail infrastructure, where supermarkets dedicate chilled counters with daily deliveries and ice bed displays to signal immediacy. National dietary guidelines further promote fresh fish. The short supply chains from coastal ports to urban markets preserve texture and flavor while supporting local fishers. Fresh fish benefits from ritualistic shopping habits, daily replenishment cycles, and strong emotional resonance, creating it the unequivocal core of European seafood culture, whereas frozen alternatives are often perceived as emergency or budreceive options.

The frozen fresh fish segment is expected to exhibit a noteworthy CAGR of 5.1% during the forecast period, owing to the technological advances in blast freezing, improved consumer perception, and demand for convenience without compromising quality. Modern individually quick frozen technology preserves cellular integrity, achieving sensory parity with fresh fish when thawed properly. Retailers are capitalizing on this shift with private-label frozen fillets now featuring sustainability certifications and catch date labeling. As per research, frozen fish consumption in Germany has been rising, driven by urban houtilizeholds preferring convenient, portion-controlled meals. The European Union’s quality designations ensure that fish frozen shortly after being caught maintain standards comparable to fresh produce, according to sources. Frozen products have also been recognized for supporting reduce houtilizehold food waste by supporting broader sustainability goals, as per research.

By Distribution Channel Insights

In 2024, the offline channels segment led the Europe fresh fish market and captured a substantial share 2024. The dominance of the offline channels segment is driven by the critical importance of sensory evaluation, immediate availability, and established consumer trust in physical retail. Supermarkets, fishmongers, and municipal markets allow shoppers to inspect texture, mell, nd eye clarity, key freshness indicators that cannot be conveyed digitally. Traditional fish markets remain cultural institutions in Southern Europe, with Barcelona’s La Boqueria and Lisbon’s Mercado da Ribeira drawing both locals and tourists. Offline retail also enables same-day consumption alignment M.. Moreover, cold chain integrity is more easily maintained in controlled store environments compared to last-mile delivery. This tactile and immediate shopping experience sustains offline dominance despite digital advances.

The online distribution segment is predicted to witness the highest CAGR of 12.4% from 2025 to 2033, owing to digital adoption, convenience, and over-the-counter assurance models. Platforms like Pesce Azzurro in Italy and FishFix in the Netherlands offer next-day delivery of fish caught within hours applying vacuum-sealed-sealed sealed insulated packaging that maintains temperatures below 2 degrees Celsius. Subscription boxes featuring chef-designed recipes and pre-portioned fillets have gained traction. Retailers like Carrefour and Tesco have integrated online fish counters with real-time inventory and catch data, enhancing transparency. Apart from these, municipal policies in cities like Amsterdam and Copenhagen support digital fish hubs that connect tiny-scale fishers directly to consumers, bypassing traditional auctions. Online channels redefine accessibility and build trust while improving logistics and preserving the premium promise of freshness.

REGIONAL ANALYSIS

Spain Market Analysis

Spain dominated the Europe fresh fish market in 2024 and accounted for a 24.7% share. The domination of Spain is attributed to its extensive coastline, high per capita consumption, and robust fishing fleet. Spaniards consume notable kilograms of fish per person annually, the second highest in Europe, according to Eurostat, with fresh fish central to daily meals like grilled sardines and bacalao. The counattempt operates the EU’s largest fishing fleet. Major ports like Vigo and Palma serve as key distribution hubs supplying domestic and European markets. Spain also leads iaquaculturecure producing significant metric tons of sea bass and bream yearly. Strong cultural attachment oseafood supported by gastronomic tourism and traditional fi, marke,, ts ensures sustained demand. This blfinish of supply,cu culturalmbeddedness, nd logistical infrastructure solidifies Spain’s dominance in the regional fresh fish economy.

France Market Analysis

France was the second largest region of the Europe fresh fish market by capturing 18.8% share in 2024. Factors such as diverse consumption patterns, strong retail integration, and emphasis on origin have largely contributed to the growth of France. French houtilizeholds consume kilograms of fish annually, with fresh species like sea bass and mackerel favored in both home cooking and haute cuisine as per FranceAgriMer. France has an extensive network of fish markets, including major wholesale hubs that support ensure quick distribution of seafood from both Atlantic and Mediterranean sources. The counattempt enforces detailed labeling requirements specifying catch area and fishing method, a measure designed to increase transparency and strengthen consumer confidence. This regulatory and cultural framework sustains high-quality demand and positions France as a trfinishsetter in ethical seafood consumption.

Italy Market Analysis

Italy is relocating ahead steadquickly in the Europe fresh fish market and is driven by Mediterranean dietary traditions, vibrant coastal fisheries, nd artisanal processing. Italians consume notable kilograms of fish per capita annually, with fresh anchovies, sardines, and sea bream integral to regional cuisines from Sicily to Liguria. The counattempt’s strong fishing fleet focutilizes on tiny-scale day boats, ensuring rapid landing and freshness. Italy also leads in value-added fresh preparations, such as marinated and ready-to-grill fillets account for a portion of retail sales, according to sources. Culinary tourism further amplifies demand with coastal restaurants sourcing daily from local ports. Recent EU funding under the National Recovery Plan has modernized fish markets by enhancing the cold chain and traceability. This fusion of tradition and innovation, and gastronomic identity, maintains Italy’s influential role in the European fresh fish landscape.

United Kingdom Market Analysis

The United Kingdom is growing gradually in the Europe fresh fish market marked owing to high seafood demand, post supply recalibration, and strong retail standards. Britons consume kilograms of fish annually, with salmon, cod, and haddock dominating houtilizehold purchases. Despite reduced EU access, UK ports like Peterhead and Newlyn maintain robust landings supported by domestic quotas. Supermarkets enforce stringent sustainability criteria. The rise of online fishmongers and direct boat-to-consumer schemes has grown since 2021, offering traceable premium options. Apart from these, the UK’s Food Standards Agency mandates full catch documentation under the post-Brexit Seafood Export Scheme, ensuring safety and origin integrity. This adaptive quality-focutilized market remains a key player despite geopolitical shifts.

Germany Market Analysis

Germany is predicted to expand in the Europe fresh fish market over the forecast period due to health awareness and retail innovation. Germans consume kilograms of fish annually, with fresh salmon,n tro, and pangasius leading houtilizehold purchases. Discounters like Aldi and Lidl have elevated fresh fish offerings with sustainability certifications and transparent sourcing. The “Blue Angel” eco label now covers fresh fish, ensuring low-impact fishing and fair labor practices as per the German Environment Agency. This demand-driven, import-relia, equality-conscious model defines Germany’s strategic position as Europe’s central consumption hub.

COMPETITION OVERVIEW

The Europe fresh fish market features a complex competitive landscape comprising large integrated aquaculture groups, national fishing cooperatives, and regional processors. Competition is defined less by price and more by freshness, consistency, sustainability credentials, and supply chain transparency. Nordic companies dominate the salmon and pelagic segments through scale and technological advantage, while Southern European firms excel in Mediterranean species and artisanal value addition. Retailers exert significant influence by setting certification and packaging standards, which shape supplier behaviorThehe risof e-commerce and short supply chains has enabled tiny-scale fishers to access premium urban consumers directly, challenging traditional auction models. Regulatory complexity under the Common Fisheries Policy and evolving import controls creates both barriers and strategic opportunities. Innovation, intraceability, chain integrity, and low-impact harvesting methods are critical for differentiation. Overall, the market rewards agility, ecological responsibility, and deep integration across the farm-to-fork continuum in a sector where trust and timeliness are paramount.

KEY MARKET PLAYERS

A few of the dominating players in the Europe fresh fish market include

- Mowi ASA

- Royal Greenland A/S

- Lerøy Seafood Group ASA

- Nomad Foods Ltd

- Bolton Group

- Thai Union Group PCL

- Young’s Seafood Ltd

- Marine Harvest

- Pelagia AS

- Parlevliet & Van der Plas

- Nueva Pescanova Group

- Iceland Seafood International

- Fripur S.A

Top Strategies Used by the Key Market Participants

Key players in the Europe fresh fish market prioritize traceability through digital labeling, sustainable certifications such as MSC and ASC, investment in cold chain logistics, vertical integration from harvest to retail, compliance with EU food safety and animal welfare regulations, and expansion of direct-to-consumer channels. Companies are increasingly adopting blockchain and QR code systems to provide real-time data on catch location, fishing method, and carbon footprint. Strategic partnerships with retailers for exclusive product lines and sustainability storynotifying enhance shelf presence. Apart from these, firms invest in recirculating aquaculture systems and onboard chilling technologies to extfinish freshness and reduce waste. Geographic diversification of sourcing mitigates quota risks while localized marketing addresses regional culinary preferences, ensuring resilience and relevance in a highly regulated and consumer-driven market.

Leading Players in the Market

Mowi ASA

Mowi ASA is a global leader in Atlantic salmon farming with extensive operations across Norway, Scotland, and Ireland, supplying premium fresh salmon to European retailers and food service providers. The company plays a pivotal role in meeting Europe’s demand for consistent, high-quality fresh fish through vertically integrated production from hatchery to retail. Mowi adheres to stringent EU animal welfare and environmental standards and provides full traceability via digital batch tracking. Recently, the company launched a carbon-neutral salmon line certified by indepfinishent auditors and expanded its chilled logistics network to ensure 48-hour delivery across Western Europe. These initiatives reinforce its commitment to sustainability and freshness while strengthening its position as a trusted supplier in Europe’s premium fresh fish segment.

Austevoll Seafood ASA

Austevoll Seafood ASA is a Norwegian-based integrated seafood group with significant harvesting, aquaculture, and processing assets supplying fresh pelagic and whitefish across Europe. The company operates a fleet of over 50 vessels and owns processing facilities in Norway, Spain, and the Netherlands, enabling rapid handling and distribution of fresh catches. Austevoll emphasizes responsible sourcing and holds multiple MSC and ASC certifications for its key species. In recent years, the company has invested in onboard freezing and chilled storage technology to preserve freshness during transit and introduced QR code traceability for all fresh fish lines sold in the EU. These actions enhance product integrity and align with European consumer demands for transparency and sustainability in seafood supply chains.

Pescanova S A

Pescanova S A is a Spanish multinational specializing in aquaculture and fresh fish distribution with a strong presence in Southern and Western Europe. The company is a leading producer of farmed sea bass, sea bream, and turbot applying land-based and offshore recirculating systems that minimize environmental impact. Pescanova supplies major supermarket chains and restaurants with fresh fish harvested on demand, ensuring optimal shelf life and quality. Recently,y the company upgraded its traceability platform to comply with the EU Digital Product Passport framework and expanded its direct-to-consumer e-commerce service across Italy and France. These strategic relocates strengthen its responsiveness to evolving regulatory and consumer expectations while reinforcing its reputation for innovation and reliability in the European fresh fish market.

MARKET SEGMENTATION

This research report on the Europe Fresh Fish Market has been segmented and sub-segmented based on the following categories.

By Product

- Pelagic Fish

- Demersal Fish

By Form

By Distribution Channel

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe