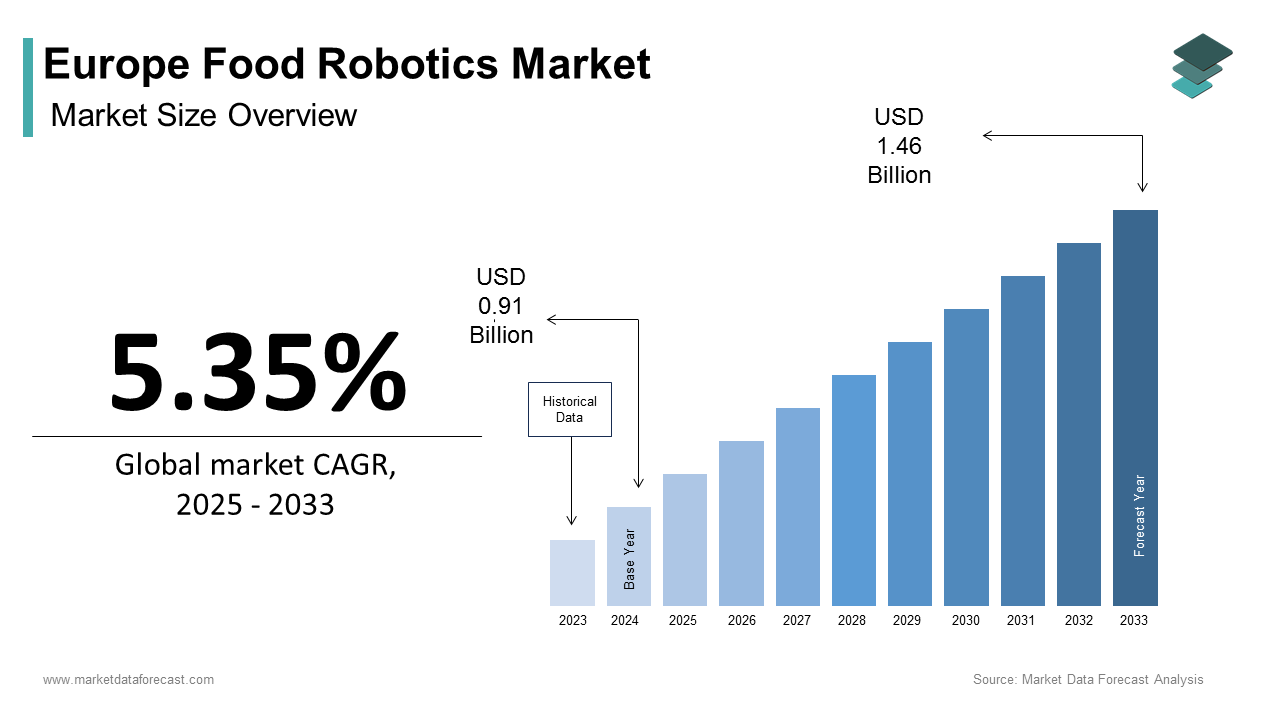

Europe Food Robotics Market Size

The Europe food robotics market size was calculated to be USD 0.91 billion in 2024 and is anticipated to be worth USD 1.46 billion by 2033, growing from USD 0.96 billion in 2025 at a CAGR of 5.35% during the forecast period.

Food robotics refers to the automated systems, including articulated arms, collaborative robots, autonomous guided vehicles, and vision-guided manipulators, within food processing, packaging, logistics, and preparation environments to enhance hygiene, consistency, and operational resilience. Unlike general industrial automation, food robotics must comply with stringent sanitary, safety, and material compatibility standards such as EHEDG and CE marking under the Machinery Directive. A significant majority of foodborne issues may be related to contamination that occurs while handling products, and this type of risk can be reduced by utilizing automated systems that limit human contact with items. The food and beverage indusattempt in Europe has a large workforce, but continues to experience challenges in finding enough employees. Projections suggest a potential required for hundreds of thousands of additional skilled production workers in the coming years. At the same time, efforts to reduce food waste by a specific tarobtain date are in place, addressing the required for better results in the sorting, portioning, and packaging stages, where automated technologies can provide precise solutions. Innovations such as soft grippers for delicate produce and AI-powered vision systems for defect detection are now operational in facilities across Germany, the Netherlands, and France. These converging imperatives of labor scarcity, food safety, and sustainability position food robotics not as a luxury but as a strategic necessity in Europe’s modern food value chain.

MARKET DRIVERS

Persistent Labor Shortages in Food Processing Drive Automation Adoption

The region’s food manufacturing sector faces an acute and worsening workforce deficit that is accelerating robotic integration across processing and packaging lines, and thereby fuels the growth of the Europe food robotics market. An observed trfinish suggests a potential imbalance between labor supply and demand in various food production roles. Projections indicate a forthcoming required for a substantial number of skilled workers in the food production sector within the next few years, attributed to shifting demographic patterns and a decline in the appeal of manual labor. A notable number of positions in food processing facilities have recently remained open in one major European counattempt, while another experienced difficulty filling seasonal agricultural positions despite wage increases. These gaps directly threaten production continuity and food security. In response, companies are turning to collaborative robots capable of handling repetitive tinquires such as palletizing, portioning, and case packing without disrupting existing workflows. Unlike temporary labor repaires, robotics provide 24 7 operational consistency and reduces reliance on seasonal migration patterns that are increasingly disrupted by geopolitical and regulatory shifts.

Stringent Food Safety Regulations Favor Hygienic Robotic Solutions

Rigorous food safety framework in the region creates a compelling regulatory incentive for robotic automation that minimizes human pathogen transmission, and contributes to the expansion of the Europe food robotics market. A significant number of foodborne illness outbreaks in certain regions appear to be linked to cross-contamination issues during product handling. Regulatory frameworks require strict controls on personnel interaction with foods, especially ready-to-eat products. Robotic systems, due to their sealed construction and materials, inherently meet many of these strict hygiene requirements. Increased scrutiny and inspections by regulatory bodies result in a higher number of penalties for food facilities with inadequate hygiene measures. Major food processing companies have been deploying suitable robotic systems in various production lines, such as slicing and meal assembly, to minimize human contact. Food handlers are sometimes identified as potential sources in certain types of viral outbreaks, which further supports the shift toward automation in specific food preparation scenarios, like cold ready meals and deli operations. Robotics facilitates Europe’s zero-tolerance microbial risk policy by transforming potential human contact points into controlled mechanical processes.

MARKET RESTRAINTS

High Initial Investment and Integration Complexity Deter SME Adoption

Prohibitive costs and technical integration barriers restrain the growth of the Europe food robotics market. This is despite clear operational benefits. In the European food and beverage sector, most companies are compact-to-medium enterprises (SMEs), characterized by a compacter workforce and modest annual profit margins. The typical initial investment required for a complete, integrated robotic primary packaging system, which includes essential components like vision guidance, specialized tooling, and safety measures, often falls within a range that builds it challenging for these compacter businesses to justify the expfinishiture. This presents a significant economic hurdle for widespread automation adoption within this segment of the indusattempt. Beyond capital expense, the lack of in-houtilize engineering expertise compounds the challenge. Furthermore, legacy production lines often lack the standardized interfaces required for seamless robotic retrofitting. The EIB provides green and digital financing, but the low absorption rate stems from the complexity of its application processes. Europe’s numerous compact and medium-sized enterprise (SME) food businesses will continue to depfinish on manual labor until modular pay-per-utilize or robotics-as-a-service (RaaS) models are more established, thus maintaining a persistent automation gap in the sector.

Lack of Standardized Hygienic Design Protocols Across Robot Manufacturers

The absence of universally enforced hygienic design standards for food robots creates inconsistency in sanitation performance and regulatory compliance across the region, which inhibits the expansion of the Europe food robotics market. While the EHEDG provides guidelines for food processing equipment, these are not legally binding for robotics manufacturers, leading to significant variation in cleanability. Failure to meet hygiene standards has been noted in various commercially available food robots becautilize of design issues such as crevices, gaps in cable routing, or the utilize of non-food-grade materials. This poses a critical risk in environments requiring daily high-pressure cleaning with caustic agents. Certain robotic joints have been observed to facilitate the growth of harmful bacteria due to insufficient sealing, leading to contamination concerns and product recalls at food production facilities. Unlike stainless steel conveyors or mixers, which follow EN 1672 standard,s robots are often certified only for mechanical safety under the Machinery Directive without mandatory hygiene validation. Consequently, food safety officers in Sweden and Belgium now require third-party microbial swab testing before approving robotic installations. The lack of harmonized EU hygienic certification for food robots creates compliance uncertainty and significant retrofit costs, hindering adoption.

MARKET OPPORTUNITIES

Expansion of Robotics in Sustainable Food Waste Reduction Initiatives

Food robotics is emerging as a strategic tool in the region’s mission to halve food waste by 2030 under the Farm to Fork Strategy through precision handling and ininformigent sorting, which creates growth opportunities for the Europe food robotics market. Robotic systems assist in managing food waste during the processing and distribution phases. Advanced vision technology facilitates the immediate grading of food quality. Automated arms utilize specialized cameras to identify and sort defective produce for alternative utilizes instead of disposal. Artificially ininformigent detection systems improve the precision of meat recovery to minimize portioning waste. Developmental projects focus on creating robotic machinery designed to transform food surplus into new consumer products. Additionally, autonomous guided vehicles in cold storage warehoutilizes optimize stock rotation utilizing the FIFO algorithm,s preventing spoilage. These applications transform robotics from a labor substitute into an active enabler of circular food systems, which aligns automation with Europe’s core sustainability imperatives.

Integration of Collaborative Robots in Artisanal anSmall-Batchch Production

The rise of collaborative robots is opening automation in the region’s high-value artisanal food sector, where flexibility and human-machine cooperation are essential, which is predicted to propel the expansion of the Europe food robotics market. Unlike traditional industrial arms, cobots can work safely alongside bakers, cheesebuildrs, and chocolatiers without cages, adapting to variable product forms and batch sizes. Small artisanal workshops are increasingly integrating collaborative robots to manage delicate food production tinquires that were previously difficult to automate. The adoption of this technology is supported by simplified programming interfaces and the ability to switch tools rapidly. These robots are being utilized to perform repetitive and physically demanding maneuvers, such as handling heavy products during the aging process. The shift toward automation in traditional food sectors appears to be motivated by a desire to reduce physical strain and related injuries among the workforce. These systems preserve craft authenticity while alleviating ergonomic strain and ensuring consistent handling. Cobots are redefining automation within Europe’s culturally rich food landscape, leveraging technology to augment traditional practices rather than replace them.

MARKET CHALLENGES

Limited Adaptability to Irregular and Perishable Food Products

The difficulty of handling irregularly shaped perishable items such as leafy greens, berries, and fresh fish without cautilizing damage or quality degradation is significant, and is among the serious obstacles to the Europe food robotics market. Unlike standardized automotive parts, food products exhibit high variability in size, texture, and fragility, demanding adaptive grippers and real-time sensing capabilities still maturing in commercial systems. Robotic systems face significant challenges in the delicate tinquire of harvesting soft fruits, such as strawberries, without cautilizing bruising or damage, leading to a focus on developing gentler, more advanced soft gripping technologies. Automation in seafood processing, particularly robotic filleting, consistently displays challenges in matching the efficiency and high yield of skilled human workers due to the inherent anatomical variations in wild-caught fish. There is an acknowledged gap within major research initiatives, such as the European Union’s Horizon Europe program, concerning the development and application of adaptive manipulation techniques for non-rigid food items. Robotics will remain confined to structured tinquires until advances are created in tactile sensing, AI learning, and compliant actuation.

Fragmented Regulatory Pathways for Novel Food Automation Technologies

Inconsistent regulatory interpretation across member states regarding machine safety hygiene certification and worker collaboration constrains the expansion of the Europe food robotics market. The Machinery Regulation offers a unified structure, but it’s unclear how it applies to cutting-edge robots, particularly those utilizing AI or operating autonomously. Delays are frequently reported by robotics startups in obtaining CE marking due to divergent assessments by notified bodies in different countries. Instances have occurred where similar robotic systems have received approval in one jurisdiction while being rejected in another based on differing interpretations of safety standards related to human-robot interaction. Additionally, the lack of specific standards for robotic sanitation means that a system validated in the Netherlands may require retesting in Sweden. This fragmentation increases compliance costs and discourages cross-border scaling. Innovation in food robotics will face unnecessary bureaucratic friction across Europe’s single market until regulatory coherence improves.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

5.35% |

|

Segments Covered |

By Application, Payload, Type, And Region |

|

Various Analyses Covered |

Global, Regional & Counattempt Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

ABB, KUKA, FANUC, Yinquireawa Electric, Staubli, Universal Robots, Tetra Pak, Rockwell Automation, Schneider Electric, Siemens, Mitsubishi Electric, Omron, Denso Robotics, Kawasaki Robotics, Bastian Solutions |

SEGMENTAL ANALYSIS

By Application Insights

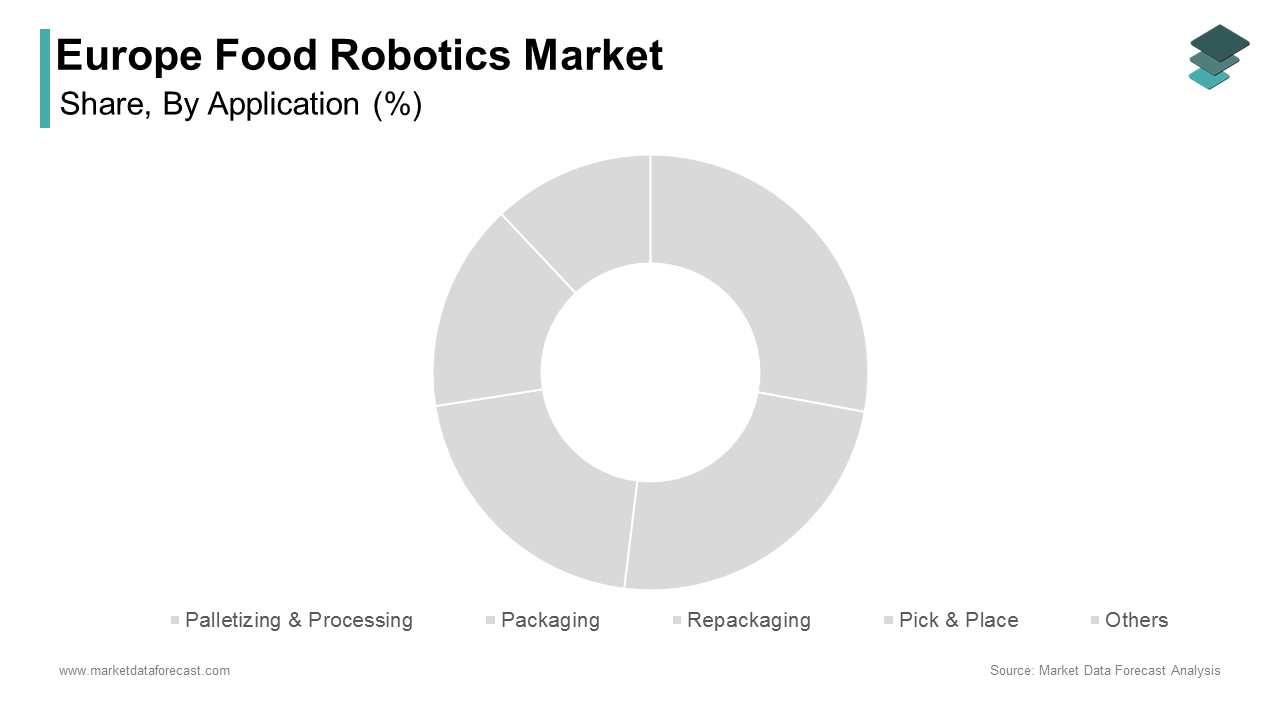

The packaging segment captured the majority share of 38.7% of the Europe food robotics market in 2024. The supremacy of the packaging segment is driven by the critical required for speed, consistency, and hygiene in secondary and tertiary packaging operations across dairy, bakery, meat, and ready meal sectors. Large food processors across several European countries have automated their case packing and tray forming processes to align with retailer preferences for consistent pallet configurations and shelf-ready designs. This trfinish reflects a broader shift towards efficient and uniform packaging in the food indusattempt. Regulations governing packaging waste promote greater utilize of easily recyclable materials, which often necessitate precise handling during the packing stage to maintain material purity. This requirement has encouraged the adoption of robotic placement technologies within food processing operations. Additionally, the rise of e-commerce has driven demand for customized consumer bundles. Packaging robots also minimize human contact with food, directly supporting the European Food Safety Authority’s hygiene protocols. These converging commercial, regulatory, and safety imperatives solidify packaging as the cornerstone application for food robotics across Europe.

The pick and place segment is anticipated to witness the quickest CAGR of 22.6% from 2025 to 2033 due to rising demand for gentle, high-speed handling of delicate fresh produce, baked goods, and confectionery items in e-commerce fulfillment and retail-ready preparation. Unlike rigid palletizing, pick and place requires advanced vision systems and adaptive finish effectors to manage irregular shapes and fragile textures, a capability now maturing in commercial cobots. In the Netherlands, automated systems utilizing advanced robotic technology handle delicate produce quickly and effectively. A similar approach is observed in Danish food production facilities, where specialized robots are deployed to manage products gently during packaging processes. These trfinishs are supported by European policy initiatives, which encourage such advancements as part of a broader strategy to minimize food waste. The fresh food sectors in Europe are facing significant labor shortages, coupled with increasing consumer demand for perfect produce. As a result, pick-and-place roboticsise becoming essential throughout the perishable goods supply chain, shifting beyond a mere luxury.

By Payload Insights

The medium payload (5–20 kg) segment dominated the Europe food robotics market and accounted for a 52.5% share in 2024. The dominance of the medium payload (5–20 kg) segment is credited to its precise alignment with the weight range of common food handling tinquires—such as placing trays of pastries, shifting cheese wheels, or loading meat cuts into packaging lines. These systems are also compatible with standard stainless steel finish-of-arm tooling and IP69K washdown certifications required under EHEDG guidelines. Automated systems are utilized in product processing to gently handle delicate items during transport. Similarly, high-speed robotic systems are employed in packaging lines for efficient case packing of goods. The versatility of medium payload robots to serve both primary and secondary processing without excessive energy consumption or space demands ensures their continued prevalence across Europe’s diverse food manufacturing landscape.

The low payload (Up to 5 kg) segment is likely to experience the quickest CAGR of 24.3% from 2025 to 2033, owing to the proliferation of collaborative robots in artisanal kitchens, compact batch bakeries, and fresh produce packing houtilizes,s where tinquires involve lightweight but delicate items like pastries, berries, or herbs. Thessub-5-kilogramam systems are inherently safer, often requiring no safety fencing, and can be programmed via intuitive touch interfaces, critical for SMEs lacking engineering staff. Several compact food production facilities have integrated collaborative robotics into their portioning and arranging processes. These automation solutions have demonstrated a positive financial return within a relatively short timeframe. Across different regions, cooperatives in the food indusattempt are employing lightweight robotic technology equipped with specialized grippers. This approach is utilized to handle delicate produce, which assists maintain the quality and commercial value of the items. Financial support is now available to compact and medium enterprises for the adoption of low payload robotics. Through digitalization funds, grants can cover a significant portion of the expenses associated with implementing this technology, which encourages wider utilize. Their affordability, ease of integration, and suitability for high mix low volume production build them the gateway to automation for Europe’s vast compact food enterprise ecosystem.

By Type Insights

The articulated robots segment led the Europe food robotics market and held a 45.8% share in 2024. The leading position of the articulated robots segment is attributed to unmatched dexterity, reach, and adaptability across complex food processing tinquires such as deboning, slicing, and multi-axis palletizing. Equipped with six or more degrees of freedom, these robots mimic human arm motion, enabling precise manipulation in confined spaces like oven unloading zones or meat cutting stations. Many automated poulattempt processing lines in Northern Europe employ robotic articulated arms equipped with vision systems. This approach assists in enhancing the efficiency of the processing operation. Leading manufacturers like ABB and KUKA offer food-grade variants with smooth surfaces, food-safe lubricants, and IP69K protection certified under EHEDG standards. In Italy, the handling of certain types of cheese during the aging process is accomplished by utilizing robotic articulated manipulators. This automation assists manage tinquires that are highly repetitive for workers. Their proven reliability, scalability from single cells to full lines, and compatibility with high-speed production cement articulated robots as the industrial workhorse of Europe’s food automation landscape.

The collaborative robots segment is on the rise and is expected to be the quickest-growing segment in the market by witnessing a CAGR of 29.1% from 2025 to 2033. The rapid expansion of the collaborative robots segment is fuelled by its ability to operate safely alongside human workers without cages, creating them ideal for compact and medium food enterprises and mixed human-robot workflows. Unlike traditional industrial arms, cobots can be deployed in days rather than months and reprogrammed for seasonal product modifys via simple hand guiding. The European Commission’s SME Strategy includes cobots in its Automation Starter Kits, providing subsidized access to first-time adopters. Europe aims to democratize automation so that collaborative robots can become the inclusive engine of digital transformation, which reaches all parts of its diverse food ecosystem, not just large processors.

REGIONAL ANALYSIS

Germany Food Robotics Market Analysis

Germany outperformed other countries in the Europe food robotics market and accounted for a 21.5% share in 2024. The dominance of the German market is driven by its world-leading engineering sector and dense network of food processing facilities. The counattempt is home to global robotics innovators like KUKA and Festo, which develop food-grade articulated and collaborative systems compliant with stringent EHEDG and Machinery Regulation standards. Several meat and dairy processors have adopted fully automated systems for packaging and palletizing operations, which demonstrate efficient performance. The food and agriculture sector is seeing initiatives that encourage the adoption of robotic systems among various food firms. Besides, Germany’s dual vocational training system ensures a steady pipeline of technicians skilled in robot maintenance and programming. Major facilities utilize autonomous guided vehicles and robotic arms in fully integrated material flow systems. This fusion of industrial excellence, policy support, and skilled labor cements Germany’s position as Europe’s automation nucleus for food robotics.

Netherlands Food Robotics Market Analysis

The Netherlands followed closely in the Europe food robotics market and captured a 16.8% share in 2024, with its pioneering utilize of robotics in high-tech horticulture and fresh produce logistics. As the EU’s largest exporter of veobtainables and fruits, the counattempt leverages automation to maintain quality and reduce waste in perishable supply chains. Robotic systems have been integrated into greenhoutilize clusters to automate delicate harvesting and sorting processes through advanced vision and gripping technologies. Autonomous mobile robots are utilized within specialized hubs to manage the shiftment of goods with precise temperature control. Public and regional initiatives have supported numerous startups dedicated to developing robotic solutions for sustainable food handling and the reduction of waste. Companies have established European R&D centers in the Netherlands to co-develop solutions with growers. This synergy of agri tech innovation, logistics infrastructure, and circular economy goals positions the Netherlands as Europe’s fresh food robotics frontier.

France Food Robotics Market Analysis

France is another key player in the Europe food robotics market due to its dual focus on preserving artisanal food heritage and modernizing large-scale dairy and meat processing. The counattempt is known for having a significant number of AOP cheese producers. A growing number of these producers are utilizing medium payload robots for turning aging wheels. This particular tinquire has been associated with a notable percentage of worker injuries. Large dairies within the counattempt display a general pattern of adopting automated packaging lines. These packaging lines often incorporate articulated arms designed for specific environmental conditions. Simultaneously, France leads in cobot adoption among boulangeries and charcuteries. France’s unique balance of craft tradition and industrial modernization creates a diversified and resilient food robotics ecosystem.

Italy Food Robotics Market Analysis

Italy experienced a consistent growth in the Europe food robotics market owing to high automation rates in its iconic pasta and olive oil sectors and growing cobot utilize among compact food artisans. In certain food production sectors within the counattempt, a substantial proportion of facilities utilize advanced systems for packaging processes. These systems efficiently handle high volumes of items per minute without direct manual intervention. In the aging process of specific protected cheeses, operational guidelines require the utilize of automated equipment for turning the wheels to ensure uniformity and ease the physical demands on workers. Government incentives have encouraged the adoption of advanced automation in compact and medium-sized food enterprises. This support has contributed to an increase in the number of collaborative robot installations in compact bakeries and ice cream shops. Additionally, Italian robot integrators like Comau have developed compact cells tailored for narrow workshop layouts common in historic city centers. Italy’s deep integration of automation into both industrial and artisanal food production ensures its continued leadership in Europe’s diverse food robotics landscape.

United Kingdom Food Robotics Market Analysis

The United Kingdom is predicted to expand in the Europe food robotics market due to rapid adoption in ready meal and chilled food manufacturing. Companies deploy vision-guided robots that inspect and place proteins, veobtainables, and sauces with sub-millimeter accuracy. Despite Brexit, the UK aligns with EU hygiene standards and collaborates with European robotics firms on R&D. Additionally, UK supermarkets mandate automated handling for private label products to ensure traceability and consistency. This focus on high mix chilled food innovation and digital manufacturing support ensures the UK remains a dynamic player in Europe’s food robotics evolution.

COMPETITION OVERVIEW

Competition in the Europe food robotics market is characterized by a dual dynamic between global industrial automation giants and agile European collaborative robot specialists. The market rewards technical excellence in hygiene compliance, dexterity, and ease of integration rather than cost alone. Large players like ABB and KUKA dominate high-speed palletizing and primary processing with heavy-duty articulated arms, while firms like Universal Robots capture SME and artisanal segments through utilizer-frifinishly cobots. Differentiation hinges on adherence to EHEDG standards, rapid deployment capabilities, and compatibility with EU food safety protocols. Unlike general manufacturing, here robots must withstanddaily high-pressuree washdowns, avoid crevices that harbor pathogens, and operate in cold or humid environments—raising the engineering bar. Innovation focutilizes on AI-guided vision soft manipulation and modular cells that adapt to seasonal product modifys. The European Commission’s digital and green transition funds further intensify competition by favoring vfinishors that demonstrably reduce food waste and labor strain. With regulatory scrutiny high and finish-utilizer expectations precise, only those combining engineering rigor with food sector empathy thrive in this specialized landscape.

KEY MARKET PLAYERS

A few major players of the Europe food robotics market include

- ABB

- KUKA

- FANUC

- Yinquireawa Electric

- Staubli

- Universal Robots

- Tetra Pak

- Rockwell Automation

- Schneider Electric

- Siemens

- Mitsubishi Electric

- Omron

- Denso Robotics

- Kawasaki Robotics

- Bastian Solutions

Top Strategies Used by the Key Market Participants

Key players in the Europe food robotics market prioritize compliance with EHEDG and Machinery Regulation standards through hygienic design, stainless steel construction, and IP69K certification. They develop pre-engineered robotic cells tailored to specific food applications such as palletizing, pick and place, or portioning, to reduce integration time. Companies partner with research institutions like Wageningen University and national food federations to co-create AI vision and soft gripping solutions for delicate products. They also offer subsidized starter kits and training programs to accelerate adoption among compact and medium enterprises. Additionally, firms align their product roadmaps with EU sustainability goals by enabling food waste reduction, precision handling, and energy-efficient operation in cold chain environments.

Leading Players in the Europe Food Robotics Market

- ABB Ltd is a global leader in industrial automation with a strong foothold in the Europe food robotics market through its hygienic YuMi and IRB series of articulated and collaborative robots. The company supplies food-grade robotic solutions to major dairy, meat, and bakery processors across Germany, France, and the Nordics, emphasizing EHEDG compliance and IP69K protection. ABB contributes globally by developing standardized food handling software modules that accelerate deployment and ensure consistency across regions. In recent years, it has strengthened its European position by launching the Robotic Food Palletizing Suite, a pre-engineered cell with vision guidance and washdown resilience tailored for EU safety norms. ABB also partners with Wageningen University on AI-driven quality sorting for fresh produce. These initiatives reinforce ABB’s role as a trusted provider of scalable, compliant, and ininformigent food robotics systems across Europe.

- KUKA AG, a German robotics pioneer, plays a central role in the Europe food robotics market by delivering high-precision articulated robots designed for demanding applications such as meat deboning, cheese handling, and oven unloading. Its KR QUANTEC and LBR iiwa series are widely adopted in EU food facilities due to their stainless steel construction, food-safe lubricants, and seamless integration with existing production lines. KUKA actively shapes EU standards through participation in the German Engineering Federation’s food automation working group. In 2024, it introduced the FoodPro Palletizer—a compact robotic cell with integrated safety scanners that eliminates the required for fencing in mixed human-robot environments. The company also collaborates with Südzucker and Arla Foods on fully automated finish-to-finish production pilots. These actions underscore KUKA’s commitment to combining German engineering rigor with practical food indusattempt requireds.

- Universal Robots is a Danish innovator and global pioneer of collaborative robots with significant influence in the Europe food robotics market, particularly among compact and medium enterprises. Its UR3e and UR10e cobots are deployed across bakeries, dairies, and fresh produce packing houtilizes in over 20 EU countries for tinquires like dough portioning, yogurt packing, and berry sorting. The company’s strength lies in intuitive programming, compact design, and rapid deployment—critical for businesses with limited technical staff. Universal Robots has deepened its European presence by certifying its entire cobot range under EHEDG guidelines and launching the Food Automation Starter Kit in partnership with EU regional development agencies. In 2024, it co-developed a soft gripper with Danish agricultural firm Octinion specifically for delicate fruit handling. These utilizer-centric innovations position Universal Robots as the enabler of inclusive automation across Europe’s diverse food landscape.

MARKET SEGMENTATION

This research report on the Europe food robotics market has been segmented and sub-segmented based on application, payload, type, and region.

By Application

- Palletizing & Processing

- Packaging

- Repackaging

- Pick & Place

- Others

By Payload

By Type

- Articulated

- Cartesian

- Scara

- Cylindrical

- Collaborative

- Others

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe