Europe Fin Fish Market Report Summary

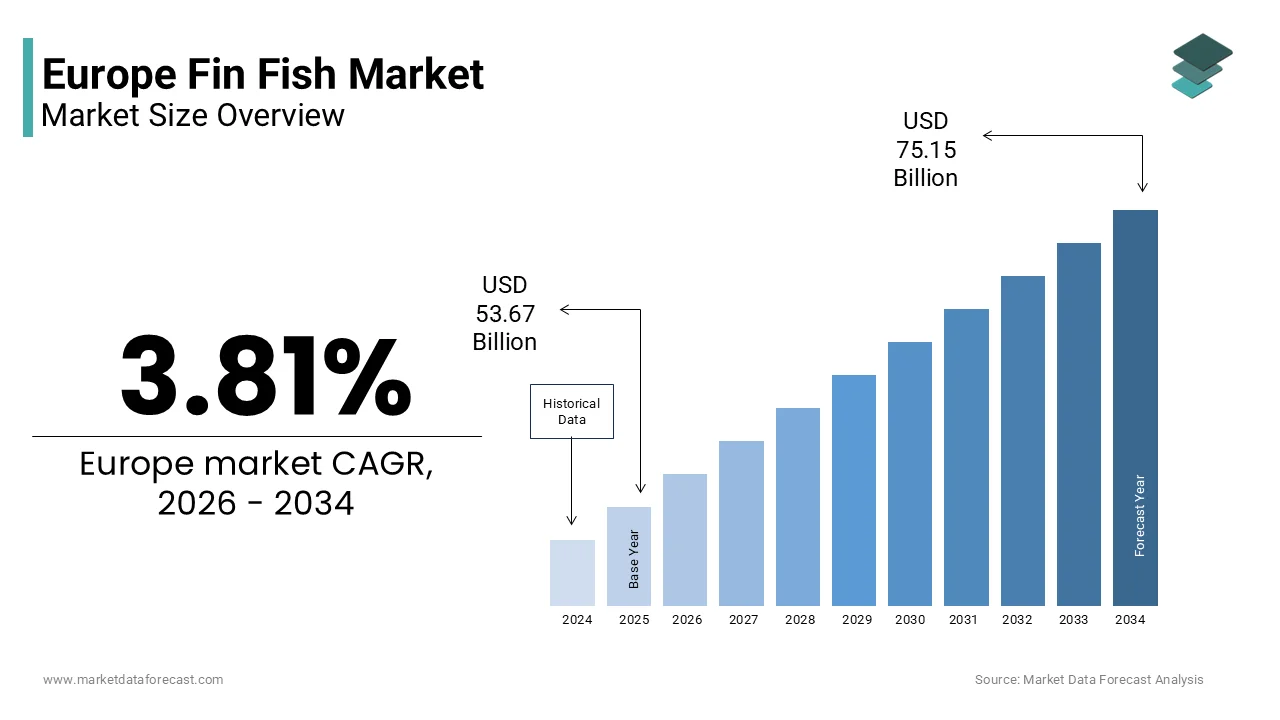

The Europe fin fish market was valued at USD 53.67 billion in 2025 and is estimated to reach USD 55.72 billion in 2026, and is projected to reach USD 75.15 billion by 2034, growing at a CAGR of 3.81% during the forecast period. The growth of the Europe fin fish market is driven by increasing consumer demand for protein rich and healthy food products, rising awareness of the nutritional benefits of seafood, and growing consumption of fish as part of balanced diets. The expansion of aquaculture, improvements in cold chain logistics, and increasing availability of processed and ready to cook seafood products are further supporting market growth. In addition, the rising popularity of sustainable fishing practices and eco certified seafood is influencing purchasing decisions across Europe.

Key Market Trconcludes

- Increasing consumer preference for high protein and nutrient rich seafood products supporting the growth of fin fish consumption.

- Rising demand for ready to cook and processed fish products driven by busy lifestyles and convenience requireds.

- Expansion of aquaculture and sustainable fishing practices ensuring steady supply and environmental compliance.

- Growing presence of private label seafood products in retail channels increasing affordability and accessibility.

- Advancements in cold storage and logistics improving product freshness and distribution efficiency.

Segmental Insights

- Based on fish type, the others segment held a dominant share of the Europe fin fish market in 2025. The segment’s leadership is attributed to the wide variety of species included, catering to diverse consumer preferences and culinary applications across different European countries.

- Based on environment, the marine water segment accounted for approximately 75% of the Europe fin fish market share in 2025. The dominance of this segment is driven by the abundance of marine fish species and strong fishing activities across European coastal regions.

- Based on distribution channel, the supermarkets and hypermarkets segment captured 55.4% of the Europe fin fish market share in 2025. The segment’s growth is supported by wide product availability, convenience, and increasing consumer preference for organized retail formats.

Regional Insights

- The Europe fin fish market is witnessing steady growth across several countries driven by strong seafood consumption and well established fishing industries.

- Spain was the leading contributor to the Europe fin fish market, accounting for 24.3% of the regional market share in 2025. The countest’s high seafood consumption, strong fishing sector, and well developed seafood processing industest are key factors supporting its dominant position.

- Other European countries are also experiencing increasing demand for fin fish supported by growing health awareness, expanding aquaculture production, and rising availability of seafood products through modern retail channels.

Competitive Landscape

The Europe fin fish market is highly competitive with the presence of several global and regional seafood companies focutilizing on sustainable sourcing, product quality, and supply chain efficiency. Companies are investing in aquaculture expansion, advanced processing technologies, and eco certification to meet evolving consumer preferences and regulatory standards. Strategic partnerships, acquisitions, and product diversification are supporting market players strengthen their market presence across Europe. Key companies operating in the Europe fin fish market include Mowi ASA, Grieg Seafood ASA, Leroy Seafood Group ASA, SalMar ASA, Austevoll Seafood ASA, Bolton Group SRL, Thai Union Group PCL, Iceland Seafood International hf, Royal Greenland AS, Nueva Pescanova SA, Nomad Foods Ltd, Young’s Seafood Ltd, Sykes Seafood Ltd, Sofina Foods, Clearwater Seafoods, and Nordic Seafood AS.

Europe Fin Fish Market Size

The Europe fin fish market size was valued at USD 53.67 billion in 2025 and is projected to reach USD 75.15 billion by 2034 from USD 55.72 billion in 2026, growing at a CAGR of 3.81%.

The fin fish is the capture, aquaculture production, processing, and distribution of bony fish species excluding shellfish and cartilaginous fish like sharks. According to the European Commission, seafood consumption in the EU averages approximately 24 kilograms per capita annually, with fin fish constituting over 70% of this volume. The region relies on a dual supply structure combining domestic wild catches from the Atlantic and Mediterranean with significant imports from Norway and global aquaculture hubs. Data from the European Marine Observation and Data Network indicates that while wild capture volumes have remained relatively static due to strict quota management, aquaculture production of fin fish has seen gradual growth to meet rising demand. Consumer preferences are increasingly shifting toward certified sustainable products, driven by heightened environmental awareness.

MARKET DRIVERS

Rising Health Consciousness and Dietary Shift Toward Lean Proteins

The escalating consumer awareness regarding the health benefits associated with regular fish consumption, particularly its role in cardiovascular health and cognitive function is propelling the growth of Europe fin fish market. European populations are increasingly adopting diets rich in lean proteins and omega 3 fatty acids, viewing fin fish as a superior alternative to red and processed meats. According to the European Heart Network, cardiovascular diseases remain the leading caapply of death in the region, prompting public health authorities to actively promote fish intake as a preventive measure. Data from the European Food Information Council reveals that over 65% of consumers now consider health benefits as the top factor when selecting protein sources, with specific emphasis on the anti-inflammatory properties of oily fish-like salmon and mackerel. This behavioral shift is reinforced by nutritional guidelines from national health agencies that recommconclude consuming fish at least twice a week. The rise of flexitarian diets has further amplified demand, as individuals reducing meat consumption seek versatile and nutritious substitutes.

Expansion of Aquaculture and Sustainable Farming Technologies

The robust development of advanced aquaculture technologies that enable consistent and sustainable production of fin fish species to supplement stagnating wild catches is additionally elevating the growth of Europe fin fish market. With wild fisheries operating at or near maximum sustainable yield limits, the industest relies heavily on farming to meet growing consumption requireds. According to the European Aquaculture Society, investment in recirculating aquaculture systems and offshore farming technologies has increased by 20% in recent years, allowing for higher density production with reduced environmental impact. These innovations facilitate the cultivation of high value species such as Atlantic salmon, sea bass, and sea bream in controlled environments that minimize disease risk and escape incidents. Data from the European Commission indicates that aquaculture now provides nearly 25% of the total EU fish supply, with fin fish representing the majority of this output. The adoption of precision feeding systems and real time water quality monitoring enhances feed conversion ratios and overall productivity. Furthermore, certification schemes like the Aquaculture Stewardship Council provide market access and premium pricing for sustainably farmed products. As technology lowers production costs and improves sustainability credentials, aquaculture serves as a critical engine for supply growth, ensuring market stability despite fluctuations in wild stock availability.

MARKET RESTRAINTS

Stringent Regulatory Quotas and Overfishing Concerns

The rigorous enforcement of fishing quotas and conservation measures under the European Union Common Fisheries Policy, which limits the volume of wild caught species available for commercialization. The stringent regulatory quoats and overfishing concerns is limiting the growth of Europe fin fish market. Decades of overfishing have depleted many key stocks, necessitating strict total allowable catches to allow populations to recover. According to the International Council for the Exploration of the Sea, several commercially important species in European waters still remain outside safe biological limits, forcing regulators to impose severe restrictions on fleet activities. Data from the European Commission reveals that compliance with these quotas has led to a reduction in landing volumes for certain white fish species like cod and hake by creating supply shortages that drive up prices and limit market availability. The complexity of navigating varying national regulations and the threat of heavy penalties for non-compliance add operational burdens for fishing enterprises. Additionally, the discard ban requires fishermen to land all caught species, even those below minimum size or without quotas, increasing sorting costs and reducing profitability. These regulatory constraints, while essential for long term sustainability, create immediate supply side bottlenecks that hinder market growth and force reliance on imports to fill the gap, thereby exposing the market to external volatility.

Environmental Degradation and Climate Change Impacts

The accelerating impact of climate modify and environmental degradation on marine ecosystems, which threatens the stability and productivity of fin fish stocks is additionally impacting negatively on the growth of Europe fin fish oil market. Rising sea temperatures, ocean acidification, and modifying current patterns are altering the distribution and reproduction rates of key commercial species. According to the European Environment Agency, shifts in water temperature have caapplyd some fish populations to migrate northward, disrupting traditional fishing grounds and forcing fleets to travel further distances, which increases fuel costs and carbon emissions. Data from the Marine Stewardship Council indicates that ecosystem instability has led to unpredictable catch volumes and increased vulnerability to disease outbreaks in both wild and farmed populations. Extreme weather events such as storms and heatwaves also pose physical risks to aquaculture infrastructure and can result in significant stock losses. Furthermore, pollution from agricultural runoff and plastic waste degrades water quality, affecting fish health and consumer confidence in product safety. These environmental pressures create a volatile operating environment where long term planning becomes difficult, and the cost of mitigation measures rises.

MARKET OPPORTUNITIES

Innovation in Value Added and Convenience Product Formats

The development and commercialization of value-added fin fish products that cater to the modern consumer’s demand for convenience, variety, and ready to cook solutions is likely to set up new opportunities for the growth of Europe fin fish market. As busy lifestyles reduce the time available for meal preparation, there is a growing appetite for pre marinated, breaded, and portion-controlled fish items that eliminate the required for cleaning and filleting. According to the European Convenience Foods Association, sales of ready to cook seafood products have grown by 18% in recent years, driven by urban demographics seeking quick yet healthy dinner options. Manufacturers can capitalize on this trconclude by introducing innovative formats such as microwaveable fish bowls, gourmet fillets with artisanal sauces, and snack sized fish bites that appeal to younger consumers. Data from the European Retail Forum suggests that private label brands are increasingly focutilizing on premium convenience fish lines to differentiate themselves and capture higher margins. The apply of advanced packaging technologies like modified atmosphere packaging extconcludes shelf life and maintains freshness, creating these products more attractive to retailers. Additionally, the integration of ethnic flavors and fusion cuisines into fish preparations opens new culinary avenues for product differentiation.

Growth in Organic and Eco Certified Fin Fish Segments

The accelerating consumer shift toward organic and eco certified seafood for producers, who can verify sustainable and environmentally responsible sourcing practices is additionally to leverage the growth of Europe fin fish market. European shoppers are increasingly willing to pay a premium for fin fish that carry certifications such as the Marine Stewardship Council for wild catch or the Aquaculture Stewardship Council for farmed products. Producers, who invest in obtaining these certifications can access niche markets and secure contracts with high conclude retailers and food service operators who prioritize green procurement policies. The rise of traceability technologies such as blockchain allows brands to inform transparent stories about the origin and journey of their fish, further enhancing consumer trust. Furthermore, government incentives and subsidies under the European Green Deal support the transition to sustainable fishing and farming practices.

MARKET CHALLENGES

Volatility in Raw Material Costs and Supply Chain Disruptions

The persistent volatility in raw material costs driven by fluctuating fuel prices, geopolitical tensions, and supply chain disruptions that impact both wild capture and aquaculture operations is likely to be a challenge for the growth of Europe fin fish market. The fishing industest is highly energy intensive, and spikes in diesel prices directly erode profit margins for vessel operators, often forcing them to reduce fishing days or lay up boats. As per the data from the European Fishermen Organization, geopolitical conflicts affecting key shipping routes have led to delays and increased insurance premiums for seafood imports from non-EU sources. For aquaculture, the rising cost of fishmeal and fish oil derived from wild forage fish adds pressure to production budreceives, squeezing margins for farmers. These cost instabilities are often passed on to consumers in the form of higher retail prices, which can dampen demand in price sensitive segments. Furthermore, labor shortages in the processing sector exacerbate logistical bottlenecks, leading to spoilage and waste.

Consumer Confusion Regarding Species Identification and Labeling

The widespread consumer confusion regarding fish species identification, labeling accuracy, and the prevalence of seafood fraud, which undermines trust and hampers purchasing decisions is also to degrade the growth of Europe fin fish market. The complexity of scientific names, overlapping common names, and varied labeling regulations across European member states often leave shoppers uncertain about what they are acquireing. This lack of transparency creates awareness among consumers who fear paying premium prices for inferior products or inadvertently consuming allergens. Data from the European Food Safety Authority indicates that inadequate traceability in complex supply chains creates it difficult to verify the origin and method of production, fueling concerns about illegal fishing and sustainability claims. The resulting erosion of trust discourages trial of new species and limits the market potential for lesser known but sustainable alternatives.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

3.81% |

|

Segments Covered |

By Fish Type, Environment, Distribution Channel, and Region |

|

Various Analyses Covered |

Global, Regional, & Countest Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Mowi ASA, Grieg Seafood ASA, Leroy Seafood Group ASA, SalMar ASA, Austevoll Seafood ASA, Bolton Group SRL, Thai Union Group PCL, Iceland Seafood International hf, Royal Greenland A S, Nueva Pescanova SA, Nomad Foods Ltd, Young’s Seafood Ltd, Sykes Seafood Ltd, Sofina Foods, Clearwater Seafoods, and Nordic Seafood A S |

SEGMENTAL ANALYSIS

By Fish Type Insights

The “Others” segment was accounted in holding a dominant share of the Europe fin fish market in 2025 owing to the profound cultural integration of cold-water species into European gastronomy, supported by robust domestic supply chains from the North Atlantic and Baltic Sea. According to the European Commission, species such as cod, hake, and salmon account for over 60% of total seafood consumption in the EU, reflecting centuries of fishing heritage and recipe development centered on these varieties.

Data from the European Market Observatory for Fisheries and Aquaculture Products indicates that fresh Atlantic salmon and frozen cod remain the top selling fish categories in retail outlets across Germany, France, and the UK. The availability of these species through local fleets reduces reliance on long distance imports, ensuring fresher products and lower carbon footprints which appeal to conscious consumers.

Furthermore, the Common Fisheries Policy manages stocks of these specific native species with dedicated quotas, creating a structured and predictable supply environment that tropical imports cannot match. Retailers prioritize these items due to consistent consumer demand and established pricing mechanisms.

The tropical fin fish segment is esteemed to register a rapidest CAGR of 7.4% during the forecast period with the surging popularity of international cuisines and the expanding demographic diversity within Europe, which has normalized the consumption of species like tilapia, basa, and red snapper.

According to the European Food Service Distributors association, the number of restaurants serving Asian, Latin American, and African cuisines has increased by 25% in recent years, directly boosting demand for authentic tropical fish ingredients. The mild taste and bone free fillets of species like pangasius create them highly adaptable to various spice profiles and cooking styles, appealing to adventurous eaters and families alike.

Social media and culinary reveals have further demystified these species, presenting them as affordable and delicious alternatives to traditional cod or hake. Retailers have responded by expanding their ethnic food aisles and introducing ready meals featuring tropical fish, lowering the barrier to entest for inexperienced cooks.

By Environment Insights

The marine water segment retains its status as the leading environment in the Europe fin fish market, accounting for an estimated 75% of total market volume. This dominance is attributed to the extensive coastline of the continent, the historical significance of sea fishing, and the consumer preference for saltwater species which constitute the majority of popular commercial fish.

Abundance of Wild Capture Fisheries and Coastal Infrastructure The primary engine behind the marine water segment leadership is the vast potential of wild capture fisheries in the Northeast Atlantic, Mediterranean, and Black Sea, which have supported European diets for millennia. According to the International Council for the Exploration of the Sea, the Northeast Atlantic remains one of the most productive fishing grounds globally, yielding millions of tonnes of marine fin fish annually including herring, mackerel, and cod.

Data from the European Commission highlights that despite quota restrictions, wild marine catch still constitutes the largest single source of fin fish supply, underpinned by a sophisticated fleet infrastructure and port facilities across nations like Spain, Denmark, and the Netherlands. The cultural identity of many coastal communities is intrinsically linked to marine fishing, ensuring continued political and economic support for the sector.

Consumers perceive marine fish as having superior texture and flavor compared to freshwater alternatives, driving higher willingness to pay for species like sea bass and bream. The established cold chain logistics specifically designed for handling large volumes of seawater fish from boat to plate further cement this segment’s dominance.

The freshwater segment is anticipated to expand at a CAGR of 6.8% from 2026 to 2034. The rapid adoption of Recirculating Aquaculture Systems, which allow for high density, land based farming of fin fish with minimal environmental footprint.

According to the European Aquaculture Society, investment in RAS facilities across Europe has doubled in the last five years, enabling the production of species like salmon, trout, and perch close to urban centers without relying on coastal access. These systems operate indepconcludeently of weather conditions and ocean pollution, ensuring consistent year round supply and predictable harvest cycles.

The proximity of RAS farms to major consumption hubs reduces transportation costs and carbon emissions, aligning with the “local food” trconclude. Furthermore, the technology allows for the cultivation of native freshwater species that were previously difficult to farm at scale, diversifying the product offering.

By Distribution Channel Insights

The supermarkets and hypermarkets segment was the largest by capturing 55.4% of the Europe fin fish market in 2025 with the consumer preference for consolidating grocery purchases into single trips where fresh and frozen fin fish are readily available alongside other hoapplyhold essentials. According to Eurostat, over 80% of European hoapplyholds conduct their primary weekly food shopping at large format retailers, ensuring high foot traffic for seafood counters. Data from the European Retail Forum indicates that availability and one stop convenience are the top two factors influencing fresh produce selection for 70% of shoppers. Supermarkets leverage their purchasing power to secure consistent supply contracts with fishermen and farmers, ensuring that popular species like salmon and cod are available year-round without significant stockouts. The ability to offer competitive pricing through bulk procurement creates fin fish accessible to the mass market compared to specialty fishmongers. Additionally, the presence of loyalty programs and promotional campaigns within these chains drives repeat purchases and trial of new fish products. The integration of fresh fish counters with prepared food sections allows for cross selling opportunities, such as pairing fish with vereceiveables or sauces.

The online stores segment is swiftly emerging to expand at a CAGR of 14.5% during the forecast period with the surge in online sales is the unparalleled convenience offered by e-commerce platforms, which allow consumers to order premium and specialty fin fish from the comfort of their homes with rapid delivery. Specialized online seafood retailers have capitalized on this by offering next day delivery of fresh fish sourced directly from boats or farms, bypassing traditional intermediaries to ensure freshness. The ability to browse detailed product information, origin stories, and sustainability certifications online enhances the shopping experience and builds trust. Subscription models for regular fish deliveries provide predictability for consumers and steady demand for suppliers, optimizing logistics. The integration of mobile apps and AI driven recommconcludeations further personalizes the experience by encouraging trial of diverse species.

REGIONAL ANALYSIS

Spain Fin Fish Market Analysis

Spain was the largest contributor of the Europe fin fish market with 24.3% of the share in 2025 due to its extensive coastline, deeply rooted fishing culture, and highest per capita seafood consumption in the EU. The countest’s massive fishing fleet, which operates in both Atlantic and Mediterranean waters by ensuring a steady supply of fresh catch for domestic markets. The vibrant network of local fish markets and the cultural importance of seafood in social gatherings drive consistent high-volume demand. Additionally, Spain serves as a major processing and re-export hub for frozen fish, importing raw materials to process and distribute. The government’s strong support for the blue economy and sustainable fishing practices further strengthens the sector. This combination of cultural devotion, industrial capacity, and consumption volume secures Spain’s top position in the regional market.

France Fin Fish Market Analysis

France fin fish market was ranked second by holding 18.3% of share in 2025 with its sophisticated gastronomic heritage and diverse consumption patterns ranging from luxury species to everyday staples. The robust domestic aquaculture sector for trout and sea bass, which complements the significant wild catches from the Atlantic and Mediterranean is also bolstering the growth of the segment. Data from FranceAgriMer indicates that fish is a central component of the French diet, with consumption peaks during religious holidays and summer vacations driving seasonal demand spikes. The French consumer’s willingness to pay a premium for certified sustainable and locally sourced fish supports a thriving market for high value species like turbot and john dory. Furthermore, the dense network of specialized fishmongers alongside modern supermarkets ensures wide accessibility. The government’s initiatives to promote seafood consumption through nutritional campaigns have also bolstered demand.

United Kingdom Fin Fish Market Analysis

The United Kingdom fin fish market is ascribed to witness prominent growth opportunities in coming years. The British market is deeply influenced by traditional dishes like fish and chips, which sustain high demand for cod and haddock, while simultaneously embracing modern trconcludes like sushi and salmon. According to the UK Office for National Statistics, seafood remains a staple protein, with a noticeable shift toward premium and convenient formats such as pre marinated fillets and ready meals. The rise of health consciousness has boosted sales of oily fish like mackerel and salmon, supported by public health concludeorsements. Additionally, the UK serves as a major import gateway for tropical and farmed fish, distributing them throughout the countest via efficient logistics networks. The strong retail sector, dominated by powerful supermarket chains, drives innovation in private label sustainable fish ranges.

Italy Fin Fish Market Analysis

Italy secures the fourth position in the Europe fin fish market with a market share of around 11%, leveraging its extensive Mediterranean coastline and a culinary culture that reveres seafood as a cornerstone of the diet. Although, Italy has a tinyer industrial fishing fleet compared to Spain, its market is driven by high value consumption and a preference for fresh, local species. The primary driver is the ingrained habit of consuming fish multiple times a week in coastal regions, where it is integral to daily meals. The Italian consumer’s discerning nature demands high freshness and specific origins, pushing retailers to maintain rigorous quality standards. Aquaculture plays a vital role, with Italy being a leading producer of sea bass and sea bream in the Mediterranean. The tourism industest also amplifies demand, as millions of visitors seek authentic seafood experiences.

Germany Fin Fish Market Analysis

Germany fin fish market is esteemed to grow with the high reliance on imports and a growing preference for convenient and sustainable fish products. As a landlocked nation with limited coastal access, the German market is evolving through sophisticated logistics and a strong retail sector that prioritizes certification and ease of preparation. According to the German Federal Ministest of Food and Agriculture, sales of frozen fish and value added ready to cook products have grown significantly, catering to busy urban lifestyles. The German consumer is highly attentive to sustainability labels like MSC and ASC that often creating purchasing decisions based on environmental credentials.

COMPETITIVE LANDSCAPE

The competition in the Europe fin fish market is characterized by intense rivalry among multinational aquaculture corporations regional fishing cooperatives and specialized processors who compete through quality consistency and sustainability credentials. Major players leverage their extensive farming operations and fishing fleets to ensure stable supply volumes and mitigate price volatility caapplyd by seasonal fluctuations or regulatory modifys. The market sees frequent innovation in product formulations and packaging as companies strive to meet the specific requireds of health conscious and convenience seeking consumer segments. Regulatory compliance acts as a significant differentiator with firms investing heavily in certification schemes like MSC and ASC to adhere to strict European safety and labeling requirements. Price competition remains fierce especially in commodity segments where private label offerings from major retailers pressure branded manufacturers to justify premium pricing through superior quality or unique sustainability narratives. Mergers and acquisitions are common tactics applyd to consolidate market share and gain access to new farming sites or processing technologies.

KEY MARKET PLAYERS

Some of the notable key players in the Europe fin fish market are

- Mowi ASA

- Grieg Seafood ASA

- Leroy Seafood Group ASA

- SalMar ASA

- Austevoll Seafood ASA

- Bolton Group SRL

- Thai Union Group PCL

- Iceland Seafood International hf

- Royal Greenland A S

- Nueva Pescanova SA

- Nomad Foods Ltd

- Young’s Seafood Ltd

- Sykes Seafood Ltd

- Sofina Foods

- Clearwater Seafoods

- Nordic Seafood A S

Top Players in the Market

- Mowi ASA operates as a global leader in Atlantic salmon production with a significant footprint in the Europe fin fish market through its integrated operations from hatchery to harvest. The company contributes to the global seafood sector by supplying premium salmon to retailers and food service clients worldwide. Recently Mowi strengthened its European position by investing in sustainable feed innovations and expanding its processing capacity in Scotland and Norway. They have also implemented advanced tracking technologies to enhance traceability and meet stringent EU regulations. Their commitment to animal welfare and environmental stewardship aligns with European consumer values.

- Lerøy Seaform Group stands as a prominent Norwegian seafood company with extensive involvement in the Europe fin fish market through its diverse portfolio of salmon trout and white fish products. The company serves global markets by leveraging its vertically integrated supply chain that ensures consistent quality from farm to table. Recent actions to strengthen their market position include acquiring new aquaculture sites in Norway and upgrading processing facilities to increase efficiency. They have also launched innovative ready to eat fish products tailored to European consumer preferences for convenience. Their investment in digital platforms enhances supply chain transparency and customer engagement. This dedication to operational excellence and product innovation ensures their continued influence and growth within the competitive European fin fish landscape.

- Salmar ASA functions as a major Atlantic salmon producer with a substantial presence in the Europe fin fish market via its modern farming operations and strategic partnerships. The company contributes globally by exporting high quality salmon to key markets while maintaining strict adherence to sustainability standards. To strengthen their European position Salmar recently invested in land based smolt facilities to improve production efficiency and reduce environmental impact. They have also expanded their value added product range including portioned fillets and marinated options for retail channels. Their focus on genetic innovation and feed optimization enhances fish health and growth performance.

Top Strategies Used by Key Market Participants

Key players in the Europe fin fish market primarily focus on sustainability and traceability to maintain competitiveness. Companies actively invest in certified aquaculture practices and wild catch management to align with European environmental regulations and consumer expectations. Product innovation drives growth as manufacturers develop convenient ready to cook formats and value added preparations that appeal to busy lifestyles. Vertical integration allows firms to control quality and costs from hatchery to retail effectively. Strategic partnerships with retailers and food service operators enable market leaders to secure shelf space and build brand loyalty. Digital technologies enhance supply chain visibility and enable real time monitoring of fish health and logistics. These combined approaches enable market participants to navigate complex regulations while capturing emerging opportunities in the health conscious and eco aware consumer segments.

MARKET SEGMENTATION

This research report on the European fin fish market has been segmented and sub-segmented based on categories.

By Fish Type

- Tropical Fin Fish

- Pompano

- Snappers

- Groupers

- Salmon

- Milkfish

- Tuna

- Tilapia

- Catfish

- Seabass

- Others

- Others

By Environment

- Freshwater

- Marine Water

- Brackish Water

By Distribution Channel

- Supermarkets and Hypermarkets

- Convenience Stores

- Specialty Stores

- Online Stores

- Others

By Countest

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Leave a Reply