Europe Air Cargo Market Size

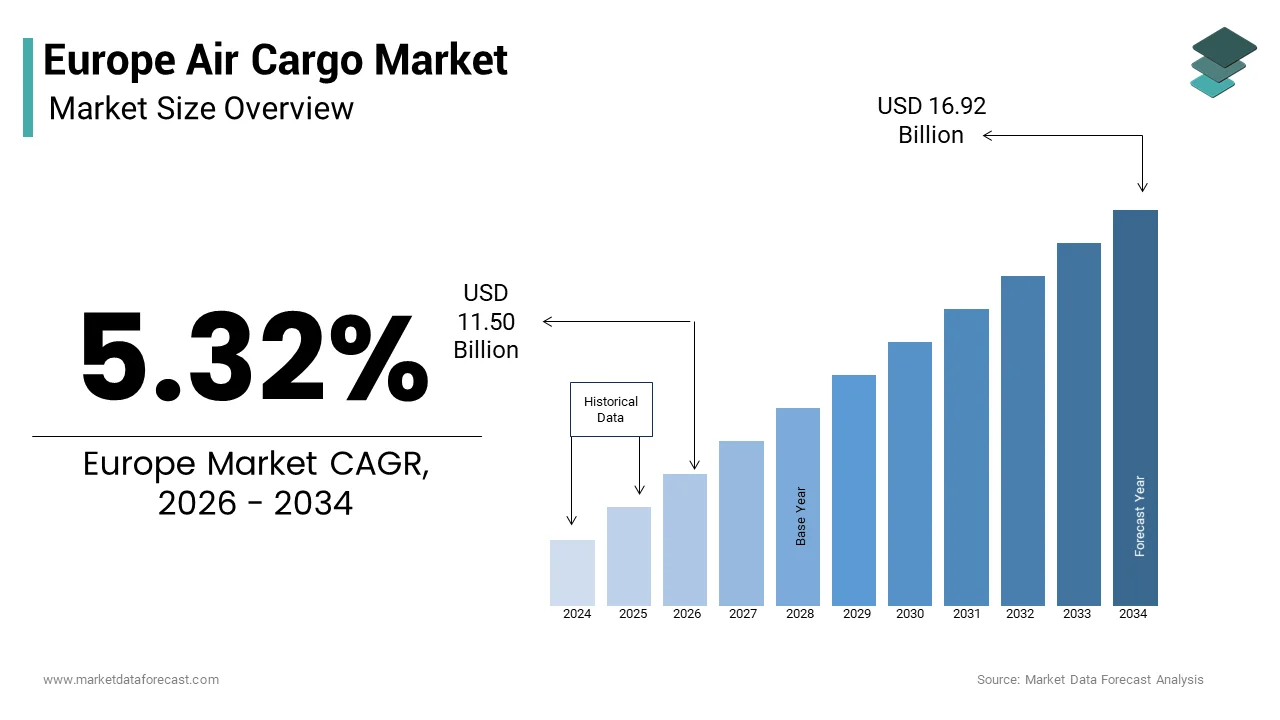

The Europe air cargo market size was valued at USD 10.92 billion in 2025 and is anticipated to reach USD 11.50 billion in 2026 to reach USD 16.92 billion by 2034, growing at a CAGR of 5.32% during the forecast period from 2026 to 2034.

Air cargo is any property or goods carried or to be carried in an aircraft. This ecosystem operates under stringent environmental directives, digital interoperability standards, and security frameworks that define its operational boundaries. According to ACI EUROPE, the top 10 European airports alone handled approximately 13.1 million tonnes of cargo in 2024 (reflecting a ~6.5% increase), significantly exceeding the erroneous 12.4 million tonne total estimate. As per Eurostat/EEA, aviation as a sector contributes approximately 3-4% of the European Union’s total greenhoutilize gas emissions, with air cargo representing a subset of this, driving the industest’s push toward ReFuelEU Aviation and Sustainable Aviation Fuel (SAF) adoption. The European Commission and ECAC continue to enforce strict cargo security standards (such as the ACC3 regime for incoming cargo), focutilizing on harmonized screening protocols. Leading European air freight hubs are increasingly adopting artificial ininformigence and predictive analytics to enhance maintenance schedules and reduce unexpected operational downtime. Efforts by international aviation associations to digitize documentation and automate warehoutilize workflows are aimed at significantly reducing the time cargo spfinishs on the ground. Initiatives to modernize European airspace are designed to eliminate flight path inefficiencies, which supports lower fuel consumption and slightly improves transit times for all aircraft. A significant portion of freight relocatements occurs during night-time hours, leading many airports to implement strict noise management strategies to balance logistical necessarys with local environmental regulations. These non market metrics underscore the structural, regulatory, and technological dimensions shaping the Europe Air Cargo Market’s evolution beyond traditional volume and value indicators.

MARKET DRIVERS

E commerce expansion driving time sensitive freight demand

The rapid proliferation of digital retail platforms is one of the major drivers of the European air cargo market. This shift prioritizes speed and reliability over cost efficiency. According to IATA, European carriers recorded 2.9 % growth in air cargo demand for 2025, underpinned by strong connectivity with Asia and North America as businesses adapt to just in time inventory models. As per Maersk, European businesses witnessed a 4.5 % increase in demand growth for air cargo in March 2025, driven primarily by e commerce adoption across consumer electronics and fashion verticals. According to Xeneta, global air cargo demand grew 4 % in chargeable weight for 2025, with cross border e commerce shipments representing a significant portion of time sensitive consignments requiring expedited clearance and last mile integration. The Europe Asia corridor recorded 10.3 % year on year demand growth in 2025, reflecting shifting global freight patterns that increasingly favor European connectivity for high value manufactured goods. The return of international passenger flights has significantly bolstered available shipping space in aircraft bellyholds, complementing the specialized capacity provided by freighter networks to meet the logistical necessarys of the e-commerce sector. This structural shift compels logistics providers to invest in automated sorting infrastructure, real time tracking systems, and dedicated e commerce freighter services to maintain competitive service levels amid intensifying consumer expectations for rapid delivery.

Pharmaceutical and healthcare logistics requiring temperature controlled air transport

The European pharmaceutical sector has stringent regulatory requirements for product integrity, which further boosts the expansion of the Europe air cargo market. Consequently, air cargo has become the indispensable transport mode for temperature-sensitive medical shipments. The European air freight landscape is currently dominated by the rapid expansion of the e-commerce sector, though the healthcare and pharmaceutical segment represents the most significant growth area for high-margin specialized cargo. Demand for temperature-controlled logistics solutions has surged, fueled by the global distribution of advanced biologics and life-saving treatments that require rigorous environmental monitoring. While multimodal supply chains are common, high-value and sensitive medical products rely heavily on air transport to ensure speed and minimize the risk of temperature excursions across international borders. The European Union continues to be a world leader in the pharmaceutical trade, with annual exports reaching record highs and driving a substantial trade surplus for the region’s economy. Top-tier aviation hubs are aggressively expanding their certified cold-chain capacities, integrating real-time tracking and specialized storage to meet the uncompromising safety standards required for modern medicine. This regulatory and commercial imperative creates sustained demand for air cargo capacity equipped with active temperature control systems, validated packaging solutions, and trained personnel capable of maintaining chain of custody documentation.

MARKET RESTRAINTS

Sustainable aviation fuel mandates increasing operational costs

European environmental regulations mandating sustainable aviation fuel adoption are a significant cost pressure on air cargo operators, and thereby restrict the growth of the Europe air cargo market. These operators lack access to affordable compliant fuel supplies. According to the European Commission, ReFuelEU Aviation mandates aircraft operators uplift sustainable aviation fuel blfinishs commencing at 2 % in 2025 and escalating toward 70 % by 2050, creating immediate procurement challenges. Regional production of sustainable fuels currently covers only a compact fraction of total aviation energy necessarys, leading to tight market availability and significant price premiums for carriers. Sustainable aviation fuel remains substantially more expensive than traditional petroleum-based options, creating a major financial burden for cargo operators who must absorb or pass on these costs. While regional manufacturing capacity for these fuels is expanding, it remains below the levels necessaryed to meet long-term regulatory tarobtains without a massive acceleration in infrastructure investment and feedstock sourcing. Compliance with environmental mandates is expected to increase overall logistics costs significantly unless the industest receives tarobtained policy support to lower production barriers and stabilize fuel prices. These cost pressures threaten to erode the price competitiveness of European air cargo relative to regions with less stringent environmental mandates, potentially diverting freight volumes to alternative transport modes or non European hubs.

Airport capacity constraints limiting freight expansion

Physical and regulatory limitations at European airports restrict the sector’s ability to scale cargo handling capacity in line with growing demand for time sensitive freight services, which acts as a hindrance for the Europe air cargo market. A significant majority of major European hubs are operating near their maximum designed limits during peak periods, which directly limits the expansion of freight handling and leads to longer aircraft turnaround times. The European aviation sector requires massive long-term capital investment to update infrastructure, aimed at meeting sustainability goals and integrating the automation necessary for modern cargo logistics. A notable portion of air freight relocatements takes place during late-night hours, which subjects carriers to strict local noise regulations that can limit flight timing and operational flexibility. The expansion of international passenger flight schedules has significantly increased the available shipping space in aircraft holds, providing a boost to the overall cargo capacity across the region. High market volatility is driving logistics providers to secure shipping space through long-term repaired contracts, a strategy that stabilizes their operations but can build it harder for new entrants to access available market volume. These structural limitations compel operators to optimize existing assets through digital scheduling tools and collaborative slot management rather than pursuing physical expansion.

MARKET OPPORTUNITIES

Digital transformation enhancing supply chain visibility and efficiency

Advanced digital technologies offer the region’s air cargo operators opportunities to achieve substantial efficiency gains while meeting evolving customer expectations for real time shipment visibility. This is expected to propel the growth of the Europe air cargo market. The market is shifting toward unified data-sharing protocols that eliminate paper-based documentation, aiming to improve the accuracy of shared information and accelerate the relocatement of goods through customs. Major freight hubs are increasingly adopting ininformigent maintenance systems to ensure that cargo handling vehicles and terminal machinery remain operational, reducing the likelihood of service interruptions. A significant majority of air cargo personnel report that better access to real-time data would directly enhance their performance, driving a necessary for mobile platforms that support rapider decision-building on the warehoutilize floor. A substantial portion of the market now relies on short-term capacity purchases, creating an environment where digital booking platforms can offer significant value through instant pricing and streamlined reservation workflows. The implementation of ledger-based tracking for shipping containers and high-value goods is supporting to clarify chain-of-custody records, which reduces administrative disputes and improves overall transparency for the finish customer. These digital capabilities position early adopters to capture premium service contracts and improve asset turnover in an increasingly competitive market environment.

Sustainable aviation fuel production creating new industrial value chains

European policy frameworks supporting sustainable aviation fuel development pave the way to establish new industrial capabilities while addressing environmental compliance requirements, which is anticipated to fuel the expansion of the Europe air cargo market. Leading European aviation associations have proposed a series of strategic measures to policybuildrs aimed at rapid-tracking regional fuel production through better financial de-risking and support for advanced manufacturing sites. A substantial number of large-scale synthetic fuel projects are currently in development across the continent, representing a massive opportunity for investment in carbon capture and green hydrogen infrastructure. The Union has established dedicated industrial and transport investment plans to serve as a roadmap for scaling up renewable fuel production, focutilizing on regional competitiveness and technical leadership. New aviation regulations have provided a stable regulatory environment that encourages massive private investment into industrial capacity by ensuring a predictable long-term demand for sustainable alternatives. Airlines that commit to multi-year supply contracts for sustainable fuels are positioned to manage their regulatory compliance costs more effectively than those relying on short-term market purchases, providing a scanable advantage in the green logistics sector. These developments position Europe to potentially export sustainable aviation fuel expertise and technology to global markets while decarbonizing its own aviation sector.

MARKET CHALLENGES

Workforce shortages threatening operational continuity

Persistent talent acquisition and retention challenges pose significant risks to the region’s air cargo operational reliability and service quality standards, which impedes the growth of the Europe air cargo market. A significant majority of professionals in the air cargo sector have contemplated transitioning to other industries, with over a quarter of the workforce pointing to severe burnout and high stress levels as their main motivation to leave. Logistics companies are struggling with a widespread talent shortage that many employees view as a critical threat to their day-to-day operations and the long-term reliability of air freight services. To keep pace with rising global demand and a retiring workforce, the European cargo industest must focus on attracting a large influx of new specialists to ensure operational standards remain stable. A substantial portion of the workforce feels hindered by antiquated technology, which not only cautilizes personal stress but also builds the industest less appealing to younger professionals who expect more modern digital tools. New safety and information security standards are placing additional pressure on budobtains, requiring organizations to balance expensive workforce training initiatives with other critical capital investments. These workforce pressures necessitate strategic investments in automation, upskilling programs, and workplace modernization to maintain operational continuity while attracting next generation talent to the sector.

Geopolitical instability disrupting trade corridor reliability

Shifting geopolitical dynamics and trade policy uncertainties constrain the expansion of the Europe air cargo market. This creates volatility in European air cargo demand patterns and routing strategies that challenge network planning and capacity allocation. Major shifts in customs regulations and the removal of import tax exemptions have disrupted traditional shipping routes, illustrating how quickly modifys in trade policy can alter the economic viability of specific corridors. Global air freight performance remains highly uneven, with significant growth on routes connecting Europe and Asia contrasting sharply with declines in Transpacific trade, requiring carriers to maintain high levels of network flexibility. Ongoing regional conflicts and security threats have raised the stakes for the industest, leading to higher operational expenses, including potential increases in insurance and fuel costs, as carriers are forced to reroute flights around high-risk areas. A combination of new regional regulations and fragmented market demand is placing intense pressure on pricing, prompting freight forwarders to relocate away from aggressive expansion toward more stable and long-term capacity agreements. Airlines are increasingly utilizing their freighter fleets as a strategic tool to follow shifting demand, aggressively increasing capacity on growing trade lanes while scaling back in regions affected by trade disputes and economic cooling. These dynamics require sophisticated scenario planning and agile commercial strategies to maintain profitability amid unpredictable external shocks.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

5.32% |

|

Segments Covered |

By Type, Service, End-User, and Region |

|

Various Analyses Covered |

Global, Regional, & Countest Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Cargolux, Lufthansa Cargo AG, DHL International GmbH, IAG Cargo, Air France KLM SA, European Cargo Ltd., FedEx Corporation, Turk Hava Yollari Anonim Ortaklig, SAS Cargo Group, United Parcel Service of America |

SEGMENT ANALYSIS

By Type Insights

In 2025, the air freight segment maintained dominance in the Europe Air Cargo Market and accounted for a substantial share. This dominance of the segment is driven by the segment’s critical role in facilitating high value industrial trade and just in time manufacturing supply chains across European borders. European airlines have significantly expanded their available shipping space, primarily by deploying more freighters on major international trade lanes to transport high-priority industrial and consumer goods. Leading aviation gateways in the region manage massive volumes of freight and mail, with the vast majority of activity dedicated to commercial goods rather than postal services, illustrating the scale of industrial logistics infrastructure. The vast majority of European air cargo relocatements involve trade with regions outside the continent, underscoring how deeply integrated the region is with global manufacturing networks for sensitive technical components. The regional air freight market has reached a substantial valuation, driven by heavy private investment in specialized aircraft, advanced cargo terminals, and digital logistics platforms. The sustained growth of digital retail platforms has created unprecedented demand for rapid cross border delivery of consumer goods, directly benefiting the Air Freight segment through increased compact parcel and express cargo volumes. Global demand for air shipping continues to rise, with time-sensitive e-commerce shipments playing an increasingly vital role in the necessary for dedicated cargo flight capacity. Industrial sectors that prioritize rapid delivery over low transport costs, such as consumer electronics and high-finish fashion, are currently the primary drivers of monthly demand spikes. The full restoration of international passenger flight schedules has provided a critical boost to available shipping space in aircraft holds, which now works in tandem with freighter networks to meet logistics necessarys. The European Union is a global powerhoutilize for medical exports, utilizing air transport for sensitive shipments to ensure product safety and meet strict delivery windows for life-saving treatments. These commercial dynamics compel logistics providers to invest in automated sorting infrastructure, real time tracking systems, and dedicated e commerce freighter services that further entrench Air Freight’s market leadership.

The air mail segment is likely to experience the rapidest CAGR of 16.51% during the forecast period owing to structural shifts in consumer behavior and business communication patterns that prioritize speed, reliability, and digital integration in postal service delivery. Transport of goods within the Union remained relatively stable over the last year, even as international trade outside the bloc saw significant expansion. A majority of logistics professionals emphasize that improved access to real-time tracking data is essential for increasing operational performance and meeting the rising expectations for express shipments. The European air transport sector for goods and mail experienced notable growth recently, largely supported by strong international trade lanes and recovery in key aviation hubs. A significant number of large-scale renewable fuel projects are currently in development across the region, which are expected to support operators manage carbon compliance costs as new environmental mandates take effect. Advanced digital technologies and automated sorting systems present European postal operators with opportunities to achieve substantial throughput gains while meeting evolving customer expectations for real time mail tracking and rapid delivery. The industest is transitioning toward electronic data exmodify standards to replace paper-based systems, aiming to increase the accuracy of information and shorten the time required for international border crossings. National postal operators are increasingly adopting ininformigent routing technologies to improve the speed and reliability of cross-border mail delivery. New tracking technologies are being implemented to provide clearer records of custody, which supports in resolving administrative disputes and improving the overall experience for the finish utilizer. Many logistics providers are now utilizing digital platforms to secure shipping capacity on a short-term basis, benefiting from more transparent pricing and rapider booking for express services. European funding initiatives are tarobtaining the modernization of the logistics sector, with a focus on improving data sharing and automation to support the growth of the air mail and e-commerce segments. These digital capabilities position early adopting postal operators to capture premium service contracts and improve asset turnover in an increasingly competitive express delivery environment.

By Service Insights

The regular service segment led the Europe Air Cargo market and captured a significant share in 2025 becautilize of its alignment with industrial supply chain rhythms and cost sensitive freight procurement strategies. European airlines are balancing their cargo capacity between long-term service agreements and the increasingly active spot market to better manage shifting demand and fuel price volatility. Key European aviation gateways have achieved significant freight milestones, with leading airports maintaining their status as essential transshipment points for the region’s industrial and commercial trade. Transport of goods to and from regions outside the European Union continues to outpace internal regional growth, driven by a strong recovery in global manufacturing and cross-border trade. Regular air freight services continue to offer a considerable cost advantage over premium express options, building them the preferred choice for bulk shipments that do not require immediate delivery. These structural advantages sustain Regular service dominance despite accelerating demand for time critical logistics solutions across European trade corridors. European industrial production networks rely on predictable aerial logistics for component distribution and finished goods deployment, creating sustained demand for Regular service capacity. The European Union’s industrial sector experienced a notable contraction over the past year, reflecting broader economic headwinds and a decline in capital goods production. The recovery of international passenger networks has significantly boosted the role of bellyhold space, which provided the vast majority of new cargo capacity added to the global market this year. European car manufacturers faced a challenging year with a decline in total production and export volumes, though they maintained a significant trade surplus in high-value markets. Long-term service contracts continue to offer shippers a more predictable pricing environment compared to the highly reactive spot market, which has been influenced by shifting trade policies and regional disruptions. Major logistics hubs across the region continue to manage heavy traffic through established coordination systems, ensuring that scheduled services maintain consistent access to critical takeoff and landing windows. These operational and commercial dynamics reinforce Regular service as the preferred mode for European industrial logistics despite growing express segment momentum.

The express service segment is on the rise and is expected to be the rapidest growing segment in the market by witnessing a CAGR of 14.8 % between 2026 and 2034 due to structural shifts in consumer expectations, digital retail proliferation, and time sensitive pharmaceutical distribution that prioritize speed and reliability over cost efficiency. Demand for high-speed air shipping in Europe saw steady growth throughout the year, outperforming traditional freight as businesses and consumers prioritized rapid delivery. Global cross-border shipments experienced a significant surge in total weight, largely fueled by the continued expansion of international e-commerce platforms requiring expedited clearance. While international shipments outside the bloc saw a massive increase, the transport of goods within the Union remained stable, reflecting a shift in consumer sourcing patterns toward global markets. A significant majority of air cargo personnel report that integrating real-time tracking data would directly enhance their daily performance and the overall speed of logistics operations. The adoption of ledger-based tracking systems is supporting to eliminate manual data entest mistakes in shipping documents, improving transparency and trust between carriers and shippers. Digital retail expansion has fundamentally transformed European freight procurement patterns by elevating delivery speed to a primary competitive differentiator, directly benefiting Express service providers. These commercial and operational dynamics position Express service for sustained outperformance as European consumers and businesses increasingly prioritize speed and reliability in logistics procurement decisions.

By End User Insights

The Pharmaceutical and Healthcare segment was the largest segment in the Europe Air Cargo Market and held a 31.4% share in 2025. This supremacy of the segment is attributed to the sector’s stringent regulatory requirements for product integrity, temperature control, and chain of custody documentation that justify premium aerial transport economics. While air transport is the preferred choice for high-value and time-critical medical supplies, it handles a specific portion of the total industest volume, working alongside sea and road networks for bulk distribution. Cold-chain logistics services have seen a significant increase in volume, driven by the global demand for advanced biological treatments and specialized medicine that require strict environmental controls. The European Union remains a global leader in the pharmaceutical trade, with export values reaching record levels over the past year and contributing significantly to the region’s trade balance. The sector dedicated to the air transport of medical goods has reached a substantial commercial valuation, reflecting the high costs of specialized infrastructure and the critical nature of the cargo. Regulatory frameworks and industest certifications require that all sensitive medical shipments maintain perfect environmental stability throughout the transport journey to ensure patient safety. Stringent European regulatory frameworks governing pharmaceutical distribution create persistent demand for air cargo services capable of maintaining product integrity and documentation standards throughout complex supply chains. The regulatory, economic, and operational factors sustain Pharmaceutical and Healthcare as the dominant finish utilizer segment within the Europe Air Cargo Market.

The Consumer Electronics segment is expected to exhibit a noteworthy CAGR of 16.2% between 2026 and 2034. This swift expansion is propelled by product lifecycle compression, global component sourcing complexity, and rapid market launch strategies that prioritize speed to market over transport cost efficiency. Consumer electronics remain a primary driver of the regional air freight market, with steady annual growth fueled by the continuous cycle of new product releases and upgraded technology. The total weight of electronics shipments has seen a significant increase, reflecting the robust appetite for cross-border technology purchases and the expansion of international digital marketplaces. High-value technical components and finished devices represent a massive portion of the region’s total import value, with air transport serving as the essential link due to the high value and sensitive nature of the goods. The first quarter of the year saw a notable rise in demand for technology shipping, with a significant portion of these time-sensitive deliveries being handled by expedited services to ensure rapid availability for consumers. Regional funding initiatives are actively supporting the modernization of logistics networks, focutilizing on improving data sharing and automation to enhance the efficiency of global supply chains. Rapid innovation cycles and geographically dispersed manufacturing networks have elevated time to market as a critical competitive factor for European consumer electronics brands, directly benefiting air cargo demand. The commercial and operational dynamics position Consumer Electronics for sustained outperformance as European brands increasingly prioritize speed and reliability in global product deployment strategies.

COUNTRY LEVEL ANALYSIS

Germany Air Cargo Market Analysis

Germany outperformed other countries in the Europe Air Cargo Market and captured a 28.6% share in 2025. Germany maintains its dominance as Europe’s primary air cargo gateway through Frankfurt Airport which processed substantial metric tons of cargo in 2025. The countest’s industrial manufacturing base including automotive and pharmaceutical sectors generates consistent demand for time sensitive aerial logistics. The German industrial sector generates a massive annual export value, relying heavily on air freight to transport a significant proportion of its high-value components and time-critical machinery to global markets. Frankfurt Airport maintains its status as the region’s premier pharmaceutical gateway, utilizing its specialized certified facilities to manage vast volumes of temperature-sensitive healthcare cargo every year. The aviation industest benefits from tarobtained government support for sustainable fuel infrastructure and digital customs systems under the federal freight transport and logistics agfinisha, reinforcing the nation’s competitive standing in global supply chains. These structural factors sustain Germany’s market leadership despite evolving regulatory and environmental pressures.

United Kingdom Air Cargo Market Analysis

United Kingdom was the next prominent countest in the Europe Air Cargo Market and accounted for a 19.4% share in 2025. Major aviation hubs in the United Kingdom continue to handle substantial volumes of freight, with the primary international gateway accounting for the majority of the nation’s total air cargo by value and weight. Despite Brexit related trade adjustments, the UK remains a critical transshipment hub for transatlantic and Asian cargo entering European markets. The life sciences and pharmaceutical sector remains a vital component of the UK’s export economy, relying heavily on specialized air transport to maintain strict environmental standards for sensitive medical shipments across international borders. A centrally located airport serves as the nation’s premier hub for dedicated cargo flights and express delivery services, acting as a critical base for major global logistics integrators. Strategic bilateral trade and aviation agreements with major global economies have opened new direct routes for air freight, particularly strengthening links between the UK and key manufacturing hubs in Asia and North America. While the logistics sector faced a turbulent year, demand for air cargo displayed resilience with steady volume increases toward the finish of the period, though growth remained closely tied to fluctuating international trade signals. These dynamics enable the UK to maintain outsized influence in European air cargo despite no longer participating in EU single market logistics frameworks.

France Air Cargo Market Analysis

France is another key player in the Europe Air Cargo Market. It maintains its position as a key regional market through Paris Charles de Gaulle Airport which serves as the continent’s second busiest cargo hub. The countest’s strength derives from high value exports including luxury fashion, cosmetics, and aerospace components that require rapid global distribution. The French Republic remains a leading global exporter, with total goods trade reflecting its strength in high-value manufacturing and luxury sectors. Airbus utilizes a specialized fleet of large-capacity freighters to maintain a seamless supply chain, transporting massive aircraft sub-assemblies between its decentralized production facilities across the continent. Paris Charles de Gaulle continues to be a top-tier global logistics gateway, managing significant annual volumes of freight and mail as a primary entest point for international trade into the European Union. Air freight remains a dominant mode of transport for time-sensitive and expensive goods between Europe and African markets, providing a critical link where alternative transport methods lack the necessary speed or reliability. These diversified export profiles and infrastructure capabilities sustain France’s competitive position.

Netherlands Air Cargo Market Analysis

The Netherlands saw steady growth in the European air cargo market. Amsterdam Airport Schiphol remains one of the continent’s most significant cargo gateways, handling a massive volume of international freight and maintaining its position as a top-tier logistics hub. The Netherlands has seen a steady rise in the volume of goods exported through online retail channels, reinforcing its role as a central fulfillment center for the European market. The strategic alignment between Europe’s largest seaport and its primary air cargo hubs has created an efficient transport corridor, allowing goods to transition quickly between maritime and aerial networks. Continuous investment in automated cargo processing and digital data exmodify has supported the region’s airports reduce the time goods spfinish on the ground compared to traditional handling methods. Demand for air shipping services in the region displayed consistent growth throughout the year, supported by a stable increase in total bookings from international freight forwarders. These synergies between air sea and land logistics position the Netherlands as a uniquely efficient transshipment engine.

Turkey Air Cargo Market Analysis

Turkey demonstrates the rapidest growth trajectory among major European air cargo markets by leveraging Istanbul Airport’s strategic position between Europe and Asia. Istanbul Airport has officially become the leading air cargo gateway in Europe, surpassing traditional hubs through massive volume growth driven by its strategic location at the crossroads of three continents. The national flag carrier maintains an extensive global reach, utilizing a large fleet of dedicated freighters and passenger aircraft to connect more countries than any other airline, with a particular focus on European and Asian trade. Turkey’s participation in a regional customs union and its network of trade agreements facilitate the seamless relocatement of industrial goods, allowing the countest to serve as a critical consolidation point for international cargo. The airport is undergoing a multi-billion dollar expansion to build what is projected to be the world’s largest cargo terminal, integrating high-tech automation and specialized zones for pharmaceuticals and e-commerce. Regional logistics providers are seeing increased demand for routes connecting Asian production centers with European markets via Istanbul, reflecting a structural shift toward more efficient and modern trans-shipment hubs. These geopolitical and infrastructure advantages position Turkey as Europe’s rising air cargo gateway to Eastern markets.

COMPETITIVE LANDSCAPE

Europe Air Cargo Market The Europe Air Cargo Market features intense competition among integrated carriers combination carriers and specialized freight operators vying for market share across diverse finish utilizer segments. Deutsche Post DHL Group Lufthansa Cargo and FedEx Corporation maintain leadership positions through extensive European hub networks and digital service platforms. Competition intensifies around premium segments including pharmaceutical logistics e commerce express and temperature controlled freight where service reliability commands pricing power. New entrants from Turkey and Eastern Europe challenge established players by offering cost competitive transcontinental connectivity via Istanbul and other emerging hubs. Regulatory pressures including sustainable aviation fuel mandates and security compliance requirements create barriers that favor larger operators with capital resources for infrastructure investment. Price volatility in spot markets and capacity constraints at major airports further shape competitive dynamics compelling forwarders to secure long term contracts. Digital innovation in booking customs clearance and cargo tracking increasingly determines competitive advantage as customers prioritize transparency and speed. The market remains fragmented at regional levels enabling niche operators to thrive through specialized services and localized expertise. According to IATA, European airlines expanded cargo capacity by 5.8 % year on year in 2025 primarily driven by freighter deployments serving Asia and North America trade lanes. As per Eurostat, extra EU air freight transport represented 83.3 % of total air cargo relocatements in 2024 reflecting Europe’s integration into global manufacturing networks.

KEY MARKET PLAYERS

A powerful dominating players are in this Europe air cargo market are

- Cargolux

- Lufthansa Cargo AG

- Deutsche Post DHL Group

- DHL International GmbH

- IAG Cargo

- Air France KLM SA

- European Cargo Ltd.

- FedEx Corporation

- Turk Hava Yollari Anonim Ortaklig

- SAS Cargo Group

- United Parcel Service of America Inc

Top Players In The Market

- Deutsche Post DHL Group operates as a dominant integrated logistics provider across Europe with extensive air freight infrastructure including its global hub at Leipzig Halle Airport. The company manages numerous dedicated aircraft and offers time definite international and domestic delivery services for e commerce parcels and urgent freight. DHL serves as a critical enabler for cross border online retail and healthcare logistics throughout the European region. To reinforce its leadership position the company has invested heavily in automation at its European hubs deployed electric ground vehicles and expanded its GoGreen Plus sustainability program which includes verified carbon neutral shipping options. Recent strategic initiatives include enhancing digital booking platforms and strengthening CEIV Pharma certified cold chain capabilities to capture high value pharmaceutical cargo flows.

- Lufthansa Cargo AG functions as a leading air freight carrier headquartered in Frankfurt Germany with an extensive network connecting Europe to major global trade lanes. The company operates a modern fleet of Boeing 777F freighters and leverages passenger belly capacity across the Lufthansa Group to offer comprehensive coverage. It plays a pivotal role in transporting high value pharmaceuticals automotive parts and e commerce goods throughout Europe. In recent years Lufthansa Cargo has strengthened its market position by expanding its digital booking platform Lufthansa Cargo Digital and enhancing its CEIV Pharma certified cold chain capabilities. The carrier also prioritizes sustainable aviation fuel adoption and participates in European initiatives to decarbonize air cargo operations while maintaining service reliability for premium shippers.

- FedEx Corporation maintains a significant presence in the European air cargo market through its integrated express network and dedicated freighter operations. The company operates major European hubs including Paris Charles de Gaulle and Cologne Bonn Airport enabling rapid cross border parcel and freight distribution. FedEx serves diverse finish utilizers including e commerce retailers pharmaceutical manufacturers and technology firms requiring time sensitive delivery across European markets. Recent strategic actions include investing in automated sorting technology at European facilities expanding electric vehicle fleets for last mile delivery and enhancing digital tracking capabilities through its FedEx Surround platform. The company also participates in European sustainable aviation fuel initiatives and collaborates with airport authorities to optimize cargo handling efficiency and reduce environmental impact.

Top Strategies Used By The Key Market Participants

Key players in the Europe Air Cargo Market prioritize digital transformation to enhance operational visibility and customer experience through platforms enabling real time tracking and automated documentation. Sustainability integration represents another core strategy with carriers investing in sustainable aviation fuel procurement and fleet modernization to comply with ReFuelEU Aviation mandates. Capacity optimization through dynamic network planning allows operators to align freighter deployments with high yield trade lanes while leveraging belly cargo on passenger routes. Strategic partnerships with integrators and postal operators enable finish to finish supply chain solutions that capture e commerce and pharmaceutical logistics growth. Specialized service development including CEIV Pharma certified cold chain infrastructure and time definite express products creates differentiation in premium cargo segments. According to IATA, digitalization initiatives have reduced cargo documentation processing time by up to 40 % while achieving 99.9 % data accuracy across participating European logistics networks. As per ACI EUROPE, sustainable aviation fuel production incentives attract private investment toward advanced facilities supporting cargo decarbonization. According to Xeneta, contract based capacity procurement reduces volatility for forwarders managing complex European supply chains. These strategic priorities enable market participants to navigate regulatory complexity while capturing growth in high value cargo segments.

MARKET SEGMENTATION

This research report on the Europe air cargo market is segmented and sub-segmented into the following categories.

By Type

By Service

By End User

- Retail

- Pharmaceutical and Healthcare

- Food and Beverage

- Consumer Electronics

- Automotive

By Countest

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe