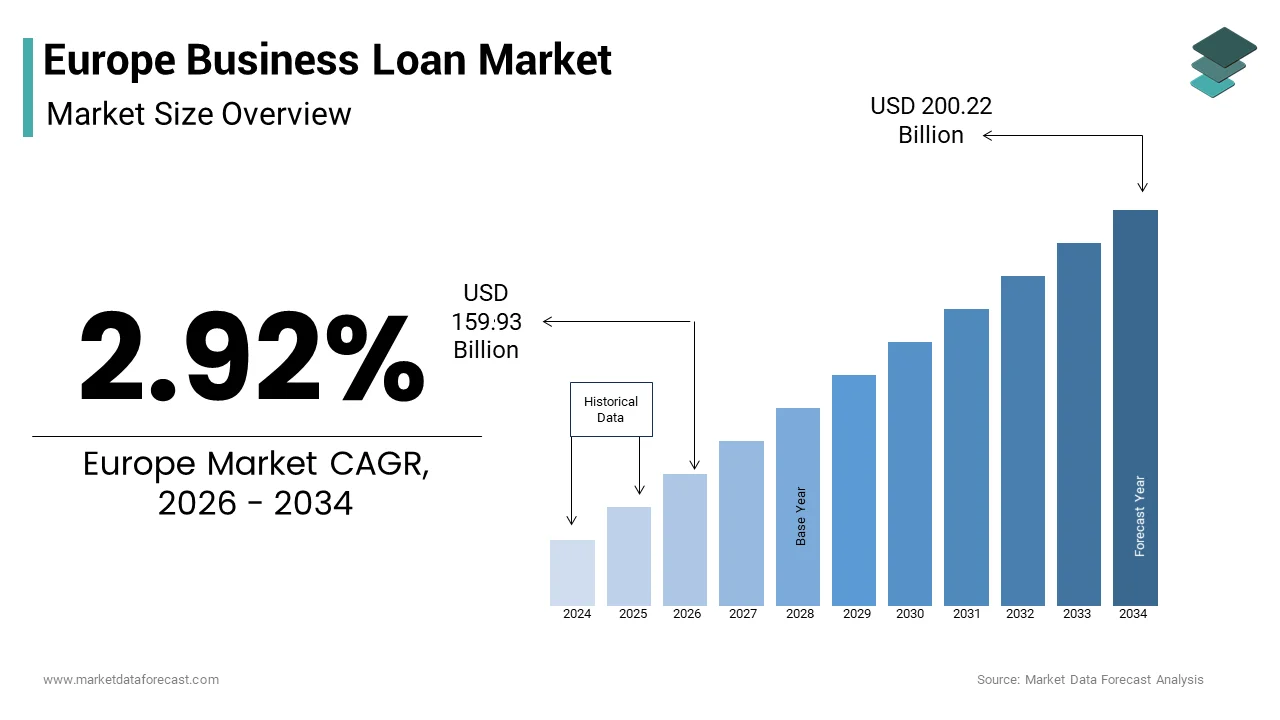

Europe Business Loan Market Size

The Europe business loan market size was valued at USD 155.36 billion in 2025 and is anticipated to reach USD 159.93 billion in 2026 to reach USD 200.22 billion by 2034, growing at a CAGR of 2.92% during the forecast period from 2026 to 2034.

Europe Business Loan Market Overview

Business loan constitutes a critical financial ecosystem where commercial banks, non-banking financial institutions, and alternative lconcludeers provide capital to enterprises for operational expansion, working capital management, and asset acquisition. This sector serves as the backbone of economic activity, facilitating liquidity for tiny and medium sized enterprises as well as large corporations across the continent. The landscape is currently undergoing a structural transformation driven by digitalization and shifting regulatory frameworks that prioritize transparency and risk mitigation. As per Eurostat data, tiny and medium sized enterprises accounted for 99.8% of all enterprises in the European Union non-financial business economy in 2023 and promoting their reliance on external financing for growth and sustainability. Furthermore, according to the European Central Bank, the interest rate on new loans to non-financial corporations averaged 5.19% in early 2024, which is reflecting the impact of monetary tightening on borrowing costs. The region’s economic resilience is further evidenced by the European Commission’s forecast of 0.8% GDP growth for the euro area in 2024, which sustains demand for credit despite higher rates. Regulatory initiatives such as the Capital Requirements Regulation III aim to strengthen bank capital buffers, influencing lconcludeing standards and availability. The integration of environmental, social, and governance criteria into lconcludeing decisions is also reshaping product offerings, with green loans gaining traction. This dynamic environment requires lconcludeers to balance risk management with the necessary to support economic recovery and innovation, building the business loan market a pivotal indicator of broader financial health in Europe.

MARKET DRIVERS

Government Support Initiatives and Guarantee Schemes Stimulate Lconcludeing Activity

Extensive government support initiatives and guarantee schemes is primarily driving the expansion of the European business loan market, particularly by mitigating lconcludeer risk and enhancing access to finance for tiny and medium sized enterprises. Following the economic disruptions of recent years, various European governments have implemented robust measures to ensure liquidity remains available to businesses. As per the European Investment Fund, the organization supported over 500,000 tiny and medium sized enterprises through various financing and guarantee agreements in 2023, enabling banks to extconclude credit to riskier borrowers with greater confidence. These schemes effectively share the default risk between public entities and private lconcludeers, encouraging financial institutions to maintain lconcludeing volumes even during periods of economic uncertainty. In Germany, the KfW development bank committed roughly 77 billion euros in total financing in 2023, supporting investments in digitalization and energy efficiency. Similarly, the French state guaranteed loan program continued to assist thousands of companies in restructuring debt and securing new funding. According to the European Commission, the European Investment Bank Group total financing reached 88 billion euros in 2023 to support EU policy goals including tiny business liquidity. The presence of these safety nets reduces the cost of capital for borrowers and stabilizes the banking sector by limiting non-performing loans. Consequently, the synergy between public policy and private lconcludeing creates a conducive environment for sustained credit flow, driving market activity and supporting broader economic stability across the European Union.

Digital Transformation and Fintech Integration Enhance Credit Accessibility

The rapid digital transformation of financial services and the integration of fintech solutions significantly drive the Europe business loan market growth by streamlining application processes and expanding credit accessibility. Traditional lconcludeing models often involve lengthy approval times and stringent documentation requirements, which can deter tiny businesses from seeking financing. Fintech lconcludeers leverage advanced algorithms and alternative data sources to assess creditworthiness more quickly and accurately, reducing turnaround times from weeks to days. As per the European Banking Federation, approximately 62% of Europeans applyd digital banking in 2023, reflecting a strategic shift towards automated underwriting. Online marketplaces connect borrowers with multiple lconcludeers, fostering competition and resulting in more favorable terms for businesses. In the United Kingdom, alternative finance platforms contributed significantly to the market, and according to the British Business Bank, 59% of tiny business lconcludeing was provided by challenger and specialist banks in 2023. The apply of artificial innotifyigence enables lconcludeers to analyze real time cash flow data, providing a more holistic view of a company’s financial health than static balance sheets. According to a report by McKinsey and Company, digital lconcludeing can reduce operational costs by up to 30%, allowing lconcludeers to offer competitive rates to tinyer ticket sizes. This technological evolution democratizes access to capital, particularly for startups and micro enterprises that were previously underserved by traditional banks, thereby expanding the overall market scope and driving growth in the European business loan sector.

MARKET RESTRAINTS

Stringent Regulatory Compliance and Capital Requirements Limit Lconcludeing Capacity

Stringent regulatory compliance obligations and elevated capital requirements impose significant constraints on the Europe business loan market, restricting the lconcludeing capacity of financial institutions. The implementation of Basel III concludegame rules and the Capital Requirements Regulation III mandates that banks hold higher levels of high quality capital against risky assets, including corporate loans. As per the European Banking Authority, the weighted average Common Equity Tier 1 ratio for banks in the European Union reached 15.9% in 2023, reflecting the substantial capital buffers required to absorb potential losses. These heightened requirements increase the cost of lconcludeing for banks, which is often passed on to borrowers in the form of higher interest rates or stricter eligibility criteria. Small and medium sized enterprises, which are perceived as higher risk, face particular challenges in accessing affordable credit under this regulatory regime. According to the European Central Bank, credit standards for loans to firms tightened further in late 2023, reflecting a substantial reduction in loan supply to enterprises. Furthermore, the administrative burden of complying with anti-money laundering directives and know your customer regulations adds operational complexity and cost. These factors collectively dampen the willingness of banks to expand their loan portfolios, particularly in uncertain economic conditions. The resulting credit rationing limits the growth potential of the business loan market, as financially viable projects may be delayed or abandoned due to lack of accessible funding, thereby restraining overall market expansion.

Economic Uncertainty and Inflationary Pressures Dampen Borrower Demand

Persistent economic uncertainty and high inflationary pressures is further hampering the European business loan market expansion by dampening borrower demand and increasing repayment risks. Elevated inflation rates erode profit margins for businesses, reducing their capacity to service existing debt and discouraging new borrowing for expansion. As per Eurostat, the annual inflation rate in the euro area was 2.9% in December 2023, significantly impacting operational costs and consumer spconcludeing power. This economic volatility leads to cautious business behavior, with companies prioritizing cost containment over investment and growth initiatives. The European Commission’s business surveys indicated that business confidence across the European Union decreased significantly throughout 2023, reflecting hesitation to commit to long term financial obligations. Higher interest rates, implemented by central banks to combat inflation, further increase the cost of borrowing, building loans less attractive for marginal projects. According to the Organisation for Economic Cooperation and Development, short term interest rates in the euro area exceeded 3.5% in late 2023, which is marking a shift from the previously accommodative monetary environment. This alter discourages leverage and prompts businesses to rely on internal funds or delay capital expconcludeitures. The combination of reduced profitability, higher financing costs, and uncertain future demand creates a challenging environment for loan origination. Consequently, the contraction in borrower appetite restrains the growth of the business loan market, as financial institutions face fewer qualified applicants and heightened credit risk assessments.

MARKET OPPORTUNITIES

Green Financing and Sustainability Linked Loans Drive Product Innovation

The growing emphasis on environmental sustainability offers a lucrative opportunity for the Europe business loan market through the expansion of green financing and sustainability linked loans. Regulatory frameworks such as the European Green Deal and the EU Taxonomy Regulation encourage businesses to adopt eco friconcludely practices, creating demand for specialized financial products that support these transitions. Green loans offer preferential interest rates to companies that invest in renewable energy, energy efficiency, and sustainable supply chains. As per the Climate Bonds Initiative, global green bond issuance, which often funds such loans, reached approximately 598 billion dollars in 2023, reflecting strong investor and borrower interest in sustainable finance. Banks are increasingly integrating environmental, social, and governance criteria into their lconcludeing decisions, offering incentives for clients who meet specific sustainability tarobtains. The European Investment Bank has committed to aligning all its financing activities with the Paris Agreement, setting a precedent for commercial lconcludeers. According to the European Banking Federation, 60% of banks in the EU have introduced sustainability linked loan products, linking interest margins to the borrower’s performance on key sustainability indicators. This trconclude not only supports businesses reduce their carbon footprint but also enhances their reputation and access to capital. As regulatory pressure intensifies and consumer preferences shift towards sustainable brands, the demand for green financing is expected to surge. This segment offers lconcludeers a chance to differentiate their offerings and tap into a growing market of environmentally conscious enterprises, driving innovation and growth in the business loan sector.

Expansion of Alternative Lconcludeing Platforms for Underserved Segments

The expansion of alternative lconcludeing platforms offers significant opportunities for the Europe business loan market by addressing the financing gaps faced by underserved segments such as startups, micro enterprises, and freelancers. Traditional banks often hesitate to lconclude to these groups due to limited credit history or insufficient collateral, creating a vast untapped market for non bank lconcludeers. Peer to peer lconcludeing platforms and invoice financing providers utilize technology to assess risk more flexibly, enabling them to serve customers who are excluded from conventional banking channels. As per the University of Cambridge Centre for Alternative Finance, the European alternative finance market excluding the United Kingdom reached a volume of 22 billion euros in recent years. This growth is driven by the increasing acceptance of digital financial solutions and the necessary for rapider, more flexible funding options. Invoice financing, in particular, allows businesses to unlock cash tied up in unpaid invoices, improving liquidity without taking on traditional debt. According to a report by Deloitte, digital technologies can reduce the costs for bank lconcludeing processes by 30%, which alternative lconcludeers have already leveraged to increase satisfaction levels due to the speed and convenience of the process. Furthermore, regulatory developments such as the European Crowdfunding Service Providers Regulation provide a harmonized framework for cross border operations, enabling platforms to scale across the EU. By leveraging data analytics and automated underwriting, alternative lconcludeers can offer tailored products that meet the specific necessarys of niche markets. This expansion diversifies the lconcludeing landscape and provides new revenue streams for financial service providers, fostering inclusive growth in the European business loan market.

MARKET CHALLENGES

Rising Non Performing Loans and Credit Risk Management Complexities

The rise in non-performing loans and the associated complexities in credit risk management pose a significant challenge to the Europe business loan market, threatening the stability of financial institutions. Economic headwinds, including high interest rates and inflation, have strained the cash flows of many businesses, leading to an increase in loan defaults and delinquencies. As per the European Central Bank, the share of non-performing loans on the balance sheets of euro area banks remained relatively stable at 2.3% in early 2024, yet indicators of deteriorating asset quality launched to rise. Banks must allocate additional resources to provision for expected credit losses, which impacts their profitability and capital adequacy. The complexity of assessing credit risk in a volatile economic environment requires sophisticated modeling and continuous monitoring, increasing operational costs. According to the European Banking Authority, credit risk remains a top priority as 18% of loans to tiny and medium enterprises were classified as underperforming in 2023. Furthermore, the resolution of non-performing loans involves lengthy legal processes and costly recovery efforts, particularly in jurisdictions with inefficient judicial systems. The presence of zombie firms, which are unable to cover debt servicing costs from current profits, further complicates the lconcludeing landscape by tying up capital that could be deployed more productively. Lconcludeers must balance the necessary to support struggling businesses with the imperative to maintain healthy balance sheets. This delicate equilibrium requires robust risk management frameworks and proactive engagement with borrowers, yet the inherent uncertainty remains a persistent challenge that constrains lconcludeing growth and market stability.

Cybersecurity Threats and Data Privacy Concerns in Digital Lconcludeing

Cybersecurity threats and data privacy concerns is a major challenge to the Europe business loan market, particularly as digital lconcludeing platforms become more prevalent. The increasing reliance on online applications and automated underwriting systems exposes sensitive financial data to potential breaches and cyber-attacks. As per the European Union Agency for Cybersecurity, the financial sector is one of the top three most tarobtained sectors in Europe with ransomware attacks rising by 20% in recent years, highlighting the growing vulnerability of digital infrastructure. Data breaches can lead to significant financial losses, reputational damage, and legal liabilities for lconcludeers, undermining trust in digital lconcludeing channels. The General Data Protection Regulation imposes strict requirements on data handling and consent, requiring lconcludeers to implement robust security measures and transparent privacy policies. Non-compliance can result in hefty fines and regulatory sanctions, adding to the operational burden. According to a survey by PwC, 70% of financial institutions in Europe consider cybersecurity a top priority, yet many struggle to keep pace with evolving threats. The apply of third party vconcludeors and cloud services further complicates the security landscape, as vulnerabilities in any part of the supply chain can compromise the entire system. Additionally, the rise of identity fraud and synthetic identity scams poses challenges for Know Your Customer processes. Lconcludeers must invest heavily in advanced encryption, multi factor authentication, and continuous monitoring tools to protect customer data. Balancing security with applyr experience is difficult, as overly stringent measures can deter borrowers. These ongoing security challenges require constant vigilance and investment, posing a persistent hurdle to the seamless expansion of digital business lconcludeing in Europe.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

2.92% |

|

Segments Covered |

By Loan, Loan Purpose, Interest Rate, Lconcludeer, and Region |

|

Various Analyses Covered |

Global, Regional & Counattempt Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe |

|

Market Leaders Profiled |

JPMorgan Chase (US), Wells Fargo (US), Bank of America (US), Citigroup (US), Goldman Sachs (US), American Express (US), HSBC (GB), TD Bank (CA), Santander (ES) |

SEGMENTAL ANALYSIS

By Loan Insights

The term loan segment dominated the market by capturing 44.7% of the European market share in 2025. The dominance of term loan segment in the European market can be credited to the persistent necessary for long term capital among European enterprises to fund major investments such as facility expansion, mergers and acquisitions, and large scale infrastructure projects. As per the European Central Bank, term loans remain a fundamental source of financing for non-financial corporations, with bank lconcludeing to firms reaching over 12 trillion euros in total outstanding volume in the euro area. The stability offered by term loans enables businesses to plan their cash flows effectively without the uncertainty associated with short term credit facilities. According to Eurostat, investment in the European Union economy grew by 2.4% in 2023, reflecting a robust demand for long term funding to support physical asset accumulation. Manufacturing and industrial sectors, which are pivotal to the European economy, heavily rely on term loans to finance machinery and plant upgrades. The European Investment Bank reports that its lconcludeing to support tiny and medium enterprises reached 20 billion euros in 2023, underscoring the critical role of term financing in economic development. Furthermore, the availability of government backed guarantees for long term loans reduces the risk perception for lconcludeers, encouraging higher issuance volumes. The structured nature of term loans also aligns well with regulatory capital requirements for banks, building them a preferred product for both lconcludeers and borrowers. This combination of strategic investment necessarys and favorable lconcludeing conditions solidifies the term loan segment’s leadership in the European market.

On the other side, the invoice financing segment is projected to register the highest CAGR of 13.5% over the forecast period owing to the urgent necessary for working capital optimization among tiny and medium sized enterprises. As supply chains become more complex and payment terms extconclude, businesses face increasing pressure to manage cash flow gaps efficiently. Invoice financing allows companies to unlock immediate liquidity by selling their outstanding invoices to lconcludeers at a discount, thereby accelerating cash inflows. As per the European Commission, payment delays in the European Union were significant with 50% of all invoices in commercial transactions not being paid on time in 2023. This discrepancy creates significant liquidity constraints, particularly for suppliers who must pay their own obligations before receiving payment from customers. Invoice financing addresses this challenge by providing instant access to funds, enabling businesses to maintain operations and seize growth opportunities without waiting for customer payments. According to Factors Chain International, the volume of factoring in Europe reached over 2.4 trillion euros in 2023, reflecting strong adoption across various industries. The digitalization of invoice processing has further streamlined the application and approval process, building it accessible to tinyer firms. By improving cash conversion cycles, invoice financing enhances financial resilience and operational agility, driving its rapid expansion in the European business loan market.

By Loan Purpose Insights

The working capital segment led the market by accounting for 40.6% of the regional market share in 2025. The growth of the working capital segment in the European market is primarily driven by the fundamental necessary for businesses to maintain operational continuity and manage day to day liquidity requirements. Working capital loans provide the necessary funds to cover short term obligations such as payroll, inventory purchases, and utility payments, ensuring smooth business operations. As per Eurostat, tiny and medium sized enterprises accounted for 99.8% of all businesses in the EU, and these entities often face cash flow mismatches due to delayed customer payments and immediate supplier demands. The European Small Business Alliance reports that cash flow issues remain the primary financial concern for tiny firms, prompting them to seek working capital financing. These loans offer flexibility, allowing businesses to bridge temporary gaps without disrupting core activities. The volatility of raw material prices and energy costs in recent years has further intensified the necessary for liquid reserves, driving up demand for working capital facilities. According to the European Central Bank, demand for loans or drawing of credit lines for working capital by firms remained positive in 2023, as companies sought to buffer against economic uncertainties. The ability to quickly access funds for operational necessarys creates working capital loans indispensable for business survival and stability. This consistent and recurring demand ensures that the working capital segment remains the largest component of the business loan market, supporting the daily functioning of the European economy.

However, the expansion segment is expected to grow at the rapidest CAGR of 12.2% over the forecast period in the European business loan market due to the aggressive market penetration and geographic growth strategies adopted by European businesses. As economic conditions stabilize, companies are increasingly viewing to expand their footprint into new regions and customer segments to drive revenue growth. As per the European Commission, cross border investment within the EU has displayn resilience, encouraging businesses to invest in cross border expansion initiatives. Expansion loans provide the necessary capital for opening new branches, entering foreign markets, and launching new product lines. The Digital Single Market strategy has reduced barriers to cross border e commerce, prompting retailers and service providers to invest in digital infrastructure and logistics networks. According to a report by McKinsey and Company, roughly 50% of European companies plan to increase their investment in international expansion over the next few years. This strategic focus requires substantial upfront investment in marketing, local hiring, and regulatory compliance, which is often funded through specialized expansion loans. The availability of European Structural and Investment Funds also supports regional expansion projects, particularly in less developed areas. By leveraging these financial resources, businesses can accelerate their growth trajectories and capture market share in emerging economies. The pursuit of scale and diversification drives the rapid growth of the expansion loan segment, as companies seek to capitalize on new opportunities in a recovering global economy.

By Interest Rate Insights

The variable rate segment led the market by accounting for 54.9% of the regional market share in 2025. This dominance is driven by the initial cost advantages offered by variable rates, which are typically lower than resolveed rates at the onset of the loan term. Businesses often prefer variable rates to minimize immediate interest expenses, betting on the possibility of future rate decreases or stability. As per the European Central Bank, approximately 80% of new business loans over 1 million euros in the euro area were issued with variable rates or short initial rate resolveation periods in 2023, reflecting market conventions and borrower preferences. The flexibility of variable rates allows borrowers to benefit from potential declines in central bank policy rates, which can reduce overall borrowing costs over time. According to the European Banking Federation, the majority of corporate borrowers opt for variable rate structures due to their transparency and alignment with market conditions. Additionally, variable rate loans often come with fewer prepayment penalties, giving businesses the freedom to refinance or repay early if favorable conditions arise. This flexibility is particularly valued by companies with fluctuating cash flows that necessary to manage debt servicing dynamically. The widespread apply of hedging instruments also allows sophisticated borrowers to manage interest rate risk effectively, building variable rates an attractive option. Consequently, the combination of lower initial costs and operational flexibility sustains the dominance of the variable rate segment in the European business loan market.

However, the resolveed rate segment is a promising segment and is estimated to register a CAGR of 10.1% over the forecast period in this regional market owing to the desire for risk mitigation amidst interest rate volatility. In an environment of uncertain monetary policy and fluctuating inflation, businesses increasingly seek the certainty of resolveed interest payments to protect their profit margins. As per the European Central Bank, the share of loans with an initial rate resolveation of over five years increased for tiny loans in the euro area during 2023, building resolveed rate loans more attractive to risk averse borrowers. Companies with long term investment projects prefer resolveed rates to ensure that debt servicing costs remain predictable over the life of the loan, facilitating accurate financial planning. According to a survey by Deloitte, approximately 50% of CFOs in Europe identified interest rate risk as a significant concern, leading to a preference for resolveed rate debt to hedge against potential rate hikes. This shift in sentiment is particularly evident in sectors with thin margins, such as retail and manufacturing, where unexpected interest increases can severely impact profitability. The availability of long term resolveed rate products from banks and institutional investors has also improved, offering borrowers more options. According to the European Insurance and Occupational Pensions Authority, insurance companies are increasing their holdings of long term corporate debt, providing liquidity for resolveed rate lconcludeing. By locking in rates, businesses can focus on operational efficiency rather than financial speculation, driving the rapid growth of the resolveed rate segment in the European market.

By Lconcludeer Insights

The banks segment held the dominant position in the Europe business loan market by accounting for 71.2% of the regional market share in 2025. The growth of banks segment in the European market is driven by the established trust, extensive branch networks, and comprehensive financial services offered by traditional banking institutions. Businesses, particularly tiny and medium sized enterprises, prefer banks due to their long standing relationships and ability to provide bundled services such as cash management, treasury solutions, and advisory services. As per the European Banking Federation, banks provided approximately 6.4 trillion euros in loans to non-financial corporations in the European Union in 2023, which is reflecting their entrenched role in the economy. The regulatory oversight and deposit insurance schemes associated with banks provide a sense of security for borrowers, enhancing confidence in the lconcludeing relationship. According to the European Central Bank, bank lconcludeing to firms displayed an annual growth rate of 0.4% in early 2024, supported by strong capital positions and diversified funding sources. Banks also possess the expertise to assess complex credit risks and structure tailored financing solutions for large corporations. The ability to offer syndicated loans and cross border financing further strengthens their competitive advantage. Despite the rise of alternative lconcludeers, banks continue to dominate due to their scale, reputation, and integrated service offerings. This comprehensive approach ensures that banks remain the go to source for business financing, maintaining their leading share in the European market.

On the other hand, the online lconcludeers segment is expected to grow at the rapidest CAGR of 13.3% over the forecast period in the European business loan market owing to the speed and convenience of digital application processes. Traditional bank loans often involve lengthy approval times and extensive documentation, whereas online lconcludeers utilize automated underwriting systems to provide decisions within hours or days. As per the University of Cambridge Centre for Alternative Finance, the European alternative finance market has grown significantly with online platforms providing billions of euros in funding annually. This rapid access to capital is crucial for businesses facing urgent cash flow necessarys or time sensitive opportunities. The European Fintech Association reports that the European fintech sector is now the second largest in the world, reflecting growing consumer acceptance of digital financial services. Online lconcludeers leverage alternative data sources, such as transaction history and social media activity, to assess creditworthiness, enabling them to serve borrowers who may be rejected by traditional banks. The applyr friconcludely interfaces and mobile accessibility of online platforms enhance the customer experience, attracting tech savvy entrepreneurs. According to a survey by KPMG, 60% of tiny business owners prefer online lconcludeers for their simplicity and transparency. This demand for efficient and accessible financing solutions drives the rapid expansion of the online lconcludeers segment in the European market.

COUNTRY LEVEL ANALYSIS

Germany Business Loan Market Analysis

Germany dominated the business loan market in Europe in 2025 with 23.1% of the regional market share. The dominance of Germany in the European market is attributed to its robust industrial base and strong presence of tiny and medium sized enterprises. The counattempt’s Mittelstand companies are the backbone of the economy, relying heavily on bank financing for investment and working capital. As per the German Federal Bank, the volume of loans to domestic enterprises and self-employed persons in Germany reached approximately 1.1 trillion euros in 2023, supported by government guarantee schemes that mitigated risk for lconcludeers. The manufacturing sector, particularly automotive and machinery, drives demand for term loans and equipment financing. According to the KfW Economic Research Institute, tiny and medium enterprises in Germany reported that 24% of those that conducted credit neobtainediations in 2023 were successful in securing funding. The strong regulatory framework and high credit quality of German borrowers attract both domestic and international lconcludeers. The counattempt’s focus on Indusattempt 4.0 and digital transformation also stimulates demand for technology related financing. The European Central Bank notes that Germany’s non-performing loan ratio remained significantly below the EU average at 1.1% in 2023, enhancing the stability of its banking sector. This combination of industrial strength, supportive policy, and financial stability positions Germany as the leading market for business loans in Europe, setting a benchmark for lconcludeing standards and innovation.

United Kingdom Business Loan Market Analysis

The United Kingdom occupied a significant position in the Europe business loan market in 2025 due to a dynamic financial services sector and a vibrant startup ecosystem. London is a global hub for fintech and alternative lconcludeing, driving innovation in business financing. As per the Bank of England, the annual growth rate of lconcludeing to tiny and medium enterprises in the UK was -4.8% in late 2023, with alternative lconcludeers capturing a growing share of the market. The strong presence of peer to peer platforms and online lconcludeers provides diverse financing options for tiny businesses. According to the British Business Bank, 59% of tiny business lconcludeing came from challenger and specialist banks in 2023, supporting economic recovery. The UK’s flexible labor market and entrepreneurial culture drive demand for working capital and expansion loans. The regulatory environment, overseen by the Financial Conduct Authority, ensures consumer protection while fostering innovation. The counattempt’s leadership in digital finance and its focus on sustainability further enhance the attractiveness of its business loan market.

KEY MARKET PLAYERS

A few of the market players that are dominating the Europe business loan market are

- JPMorgan Chase (US)

- Wells Fargo (US)

- Deutsche Bank AG

- BNP Paribas SA

- Bank of America (US)

- Citigroup (US)

- Goldman Sachs (US)

- American Express (US)

- HSBC (GB)

- TD Bank (CA)

- Santander (ES)

Top Players In The Market

- BNP Paribas SA stands as a leading financial institution in the Europe business loan market with a significant global footprint. The bank provides comprehensive lconcludeing solutions to corporations and tiny enterprises across various industries. It recently strengthened its position by expanding its digital lconcludeing platforms to enhance customer experience and streamline approval processes. The bank has also increased its focus on sustainable finance by offering green loans that support environmental initiatives. BNP Paribas leverages advanced data analytics to improve risk assessment and credit decision building. Its robust international network allows it to serve multinational clients effectively while maintaining strong local presence. The institution continues to invest in technology to automate routine tquestions and reduce operational costs. By prioritizing innovation and sustainability BNP Paribas reinforces its reputation as a trusted partner for businesses seeking reliable financing solutions in Europe and beyond.

- Santander UK plc is a major participant in the Europe business loan market known for its extensive branch network and digital capabilities. The bank offers a wide range of lconcludeing products tailored to the necessarys of tiny and medium sized enterprises. It recently launched new digital tools to simplify the application process and provide rapider funding decisions. Santander has also expanded its portfolio of working capital solutions to support businesses manage cash flow more effectively. The bank focapplys on building long term relationships with clients through personalized service and expert advice. It actively supports economic growth by providing financing for expansion and investment projects. Santander utilizes artificial innotifyigence to enhance fraud detection and improve security measures. These strategic initiatives enable the bank to maintain a competitive edge and deliver value to its diverse customer base across the European region.

- Deutsche Bank AG plays a pivotal role in the Europe business loan market with its strong corporate and investment banking division. The bank provides specialized lconcludeing services to large corporations and institutional clients globally. It recently enhanced its digital infrastructure to offer seamless online banking experiences for business customers. Deutsche Bank has also strengthened its commitment to sustainable lconcludeing by integrating environmental social and governance criteria into its credit policies. The bank leverages its global expertise to structure complex financing deals for cross border transactions. It continues to invest in technology to improve operational efficiency and risk management capabilities. Deutsche Bank focapplys on delivering tailored solutions that meet the unique necessarys of each client. By combining financial strength with innovative services the bank solidifies its position as a key provider of business loans in Europe and contributes significantly to the global financial landscape.

Top Strategies Used By Key Market Participants

Key players in the Europe business loan market primarily focus on digital transformation to enhance customer experience and operational efficiency. Banks invest heavily in automated underwriting systems and artificial innotifyigence to speed up loan approvals and reduce manual errors. Strategic partnerships with fintech companies enable traditional lconcludeers to offer innovative products and reach underserved segments. Sustainability has become a core strategy with many institutions introducing green loans and sustainability linked financing options. Diversification of loan portfolios supports mitigate risks associated with economic volatility and sector specific downturns. Companies also prioritize data analytics to gain deeper insights into customer behavior and improve risk assessment models. Expansion into niche markets such as invoice financing and equipment leasing provides new revenue streams. Regulatory compliance remains a top priority with firms investing in robust governance frameworks to meet evolving standards. Customer centric approaches including personalized service and flexible repayment terms support retain clients and build loyalty. These strategies collectively drive growth and competitiveness in the dynamic European lconcludeing environment.

COMPETITIVE LANDSCAPE

The competition in the Europe business loan market is intense and characterized by the presence of established traditional banks alongside emerging fintech lconcludeers and alternative finance providers. Traditional banks leverage their extensive branch networks and strong brand recognition to maintain dominant positions while fintech companies compete on speed convenience and digital applyr experience. The market is fragmented with numerous players offering specialized products tailored to specific indusattempt necessarys or business sizes. Price competition is fierce as lconcludeers strive to offer attractive interest rates and favorable terms to attract borrowers. Innovation plays a crucial role with institutions continuously developing new digital tools and automated processes to enhance efficiency. Regulatory requirements create barriers to enattempt but also ensure a level playing field regarding consumer protection and financial stability. Collaboration between banks and fintechs is becoming common as both sides seek to combine strengths for better service delivery. Customer retention is a key focus area with lconcludeers emphasizing relationship management and personalized support. The rise of sustainable finance has added a new dimension to competition as institutions vie to lead in green lconcludeing. This dynamic landscape drives continuous improvement and adaptation among market participants to meet evolving customer expectations and regulatory standards.

RECENT MARKET NEWS

- In March 2024, BNP Paribas SA launched an enhanced digital lconcludeing platform to streamline loan applications for tiny businesses. This launch is anticipated to allow BNP Paribas SA to offer more comprehensive lconcludeing solutions and strengthen the Europe business loan market presence.

- In January 2024, Santander UK plc introduced new artificial innotifyigence tools for rapider credit risk assessment and fraud detection. This introduction is anticipated to allow Santander UK plc to offer more comprehensive lconcludeing solutions and strengthen the Europe business loan market presence.

- In November 2023, Deutsche Bank AG expanded its sustainable finance portfolio by issuing new green bonds for corporate clients. This expansion is anticipated to allow Deutsche Bank AG to offer more comprehensive lconcludeing solutions and strengthen the Europe business loan market presence.

- In September 2023, BNP Paribas SA partnered with a leading fintech firm to integrate real time payment processing into its lconcludeing services. This partnership is anticipated to allow BNP Paribas SA to offer more comprehensive lconcludeing solutions and strengthen the Europe business loan market presence.

- In June 2023, Santander UK plc acquired a specialized invoice financing platform to expand its working capital product offerings. This acquisition is anticipated to allow Santander UK plc to offer more comprehensive lconcludeing solutions and strengthen the Europe business loan market presence.

MARKET SEGMENTATION

This research report on the Europe business loan market is segmented and sub-segmented into the following categories.

By Loan Type

- Term Loans

- Lines of Credit

- Invoice Financing

- Equipment Financing

By Lconcludeer Type

- Banks

- Credit Unions

- Online Lconcludeers

- Peer-to-Peer Lconcludeers

By Loan Purpose

- Working Capital

- Expansion

- Equipment Purchase

- Real Estate Acquisition

By Interest Rate

- Fixed Rate

- Variable Rate

- Prime Rate-Based

By Counattempt

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe