Europe Analytical Instruments Market Size

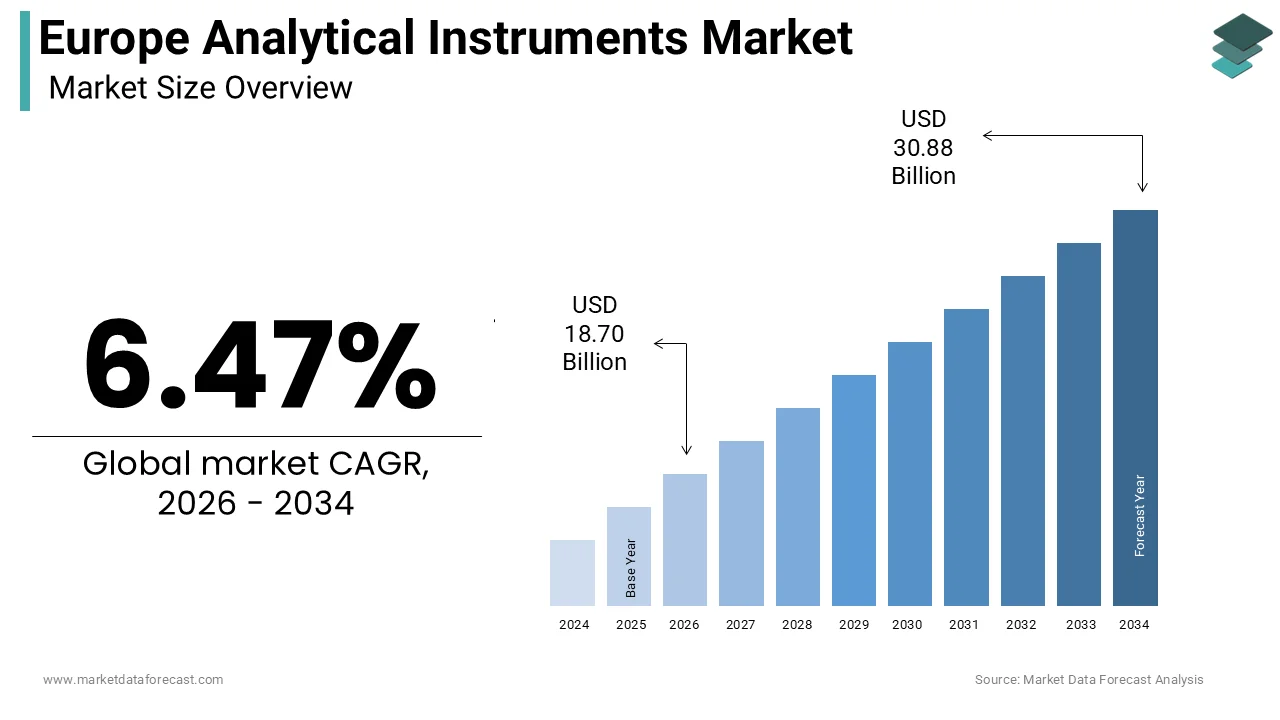

The Europe analytical instruments market size was calculated to be USD 17.56 billion in 2025 and is anticipated to be worth USD 30.88 billion by 2034, from USD 18.70 billion in 2026, growing at a CAGR of 6.47% during the forecast period.

The analytical instruments are designed for the qualitative and quantitative analysis of chemical and biological samples. These instruments include chromatography systems, mass spectrometers, spectroscopy equipment, and molecular diagnostics tools that are indispensable in pharmaceuticals, biotechnology, environmental monitoring, and food safety sectors. The region serves as a global hub for scientific innovation driven by robust research infrastructure and stringent regulatory frameworks. As per Eurostat, the European Union invested approximately 2.2% of its gross domestic product in research and development in 2023, reflecting a strong commitment to scientific advancement. Furthermore, the European Medicines Agency approved over 90 new medicines in 2023, elevating the role of analytical precision in drug development and quality control. The integration of artificial ininformigence and automation into these instruments has transformed laboratory workflows, enhancing accuracy and throughput. According to the European Commission, the digital transformation of healthcare and industrial processes is a priority, with significant funding allocated to smart laboratory technologies. This technological evolution supports the demand for high-performance analytical tools capable of handling complex data sets. The market is also influenced by the growing emphasis on environmental sustainability, with regulations requiring precise monitoring of pollutants and emissions. Consequently, laboratories across Europe are upgrading their capabilities to meet these evolving standards, ensuring that analytical instruments remain central to scientific and industrial progress in the region.

MARKET DRIVERS

Stringent Regulatory Frameworks and Quality Compliance Standards Drive Demand

The stringent regulatory landscape governing pharmaceutical production, environmental protection, and food safety is also promoting the growth of Europe analytical instruments market. Regulatory bodies, such as the European Medicines Agency and the European Food Safety Authority, mandate rigorous testing protocols to ensure product quality and public safety. The surge in drug development activities requires extensive analytical testing at every stage from discovery to final product release. Chromatography and mass spectromeattempt are essential for identifying impurities and verifying compound integrity. Similarly, environmental regulations under the European Green Deal require continuous monitoring of air, water, and soil quality. As per the European Environment Agency, member states must report detailed data on pollutant levels, which drives the adoption of sensitive spectroscopic and chromatographic instruments. The implementation of the REACH regulation further compels manufacturers to analyze chemical substances for potential hazards. These compliance mandates create a consistent and non-discretionary demand for high-precision analytical tools. Laboratories must invest in state-of-the-art equipment to meet these standards, avoiding penalties and ensuring market access. The complexity of modern regulations necessitates instruments with higher sensitivity and resolution, thereby fostering continuous innovation and replacement cycles within the market.

Expansion of Biopharmaceutical Research and Development Activities Fuels Growth

The expansion of biopharmaceutical research and development activities is also amplifying the growth of Europe analytical instruments market. Europe is home to a vibrant biotech ecosystem with significant investments in personalized medicine and biologics. According to some studies, the European biotechnology sector attracted over 12 billion Euros in venture capital funding in 2023, supporting the development of innovative therapies. Biologics, such as monoclonal antibodies and gene therapies, require sophisticated analytical methods for characterization due to their structural complexity. Techniques like liquid chromatography, mass spectromeattempt, and capillary electrophoresis are indispensable for analyzing protein structures, post-translational modifications, and purity. The rise of personalized medicine further amplifies this demand as treatments are tailored to individual genetic profiles requiring precise genomic and proteomic analysis. Academic institutions and contract research organizations are expanding their capabilities to support these initiatives, leading to increased procurement of high-finish analytical instruments. The shift towards continuous manufacturing in pharmaceutical production also necessitates real-time analytical monitoring systems.

MARKET RESTRAINTS

High Capital Investment and Maintenance Costs Restrain Market Penetration

The high capital investment required for acquiring advanced systems, coupled with significant ongoing maintenance costs, is additionally degrading the growth of Europe analytical instruments market. High-performance instruments, such as nuclear magnetic resonance spectrometers and high-resolution mass spectrometers, can cost several hundred thousand Euros, building them prohibitive for tiny and medium-sized enterprises and academic labs with limited budreceives. According to the European Small Business Portal, access to finance remains a challenge for tiny businesses, with 40% citing cost as a barrier to technology adoption. Additionally, these instruments require regular calibration servicing and specialized consumables, which add to the total cost of ownership. The required for skilled personnel to operate and maintain these complex systems further increases operational expenses. This skills gap leads to increased training costs and potential downtime if issues arise. Economic uncertainty and inflationary pressures have also prompted organizations to delay capital expfinishitures, prioritizing essential operations over equipment upgrades. The long depreciation periods of these instruments mean that applyrs may retain older models longer than ideal, slowing down the replacement cycle.

Complexity of Data Management and Integration Poses Operational Challenges

The complexity of data management and integration is additionally hindering the growth of Europe analytical instruments market. Modern analytical tools generate vast amounts of high-dimensional data that require sophisticated software solutions for storage, processing, and interpretation. According to the International Data Corporation, the amount of data created globally is expected to reach 175 zettabytes by 202,5 with a significant portion originating from scientific and industrial sources. Many laboratories struggle with legacy systems that are incompatible with new instruments, leading to data silos and inefficiencies. The lack of standardized data formats complicates the integration of results from different platforms, hindering comprehensive analysis. This fragmentation reduces productivity and increases the risk of errors in data transcription and analysis. Furthermore, the required for advanced bioinformatics and cheminformatics expertise to interpret complex datasets creates a bottleneck. There is a shortage of professionals skilled in both analytical chemisattempt and data science, limiting the ability of organizations to fully leverage their instrument capabilities. Cybersecurity concerns also arise as laboratories increasingly connect instruments to networked systems for remote monitoring and data sharing. Ensuring data integrity and protection against breaches requires additional investment in security infrastructure.

MARKET OPPORTUNITIES

Integration of Artificial Ininformigence and Machine Learning Presents Significant Opportunities

The integration of artificial ininformigence and machine learning into analytical instruments is to level up the growth of Europe analytical instruments market. These technologies enable automated data analysis, pattern recognition, and predictive maintenance, thereby enhancing efficiency and accuracy. According to the European Commission, the adoption of artificial ininformigence in indusattempt could boost productivity by up to 40%. In analytical laboratories, AI algorithms can process complex spectral and chromatographic data quicker and more accurately than human analysts, identifying subtle patterns and anomalies. This capability is particularly valuable in drug discovery, where rapid screening of compounds is essential. Machine learning models can also predict instrument failures before they occur, reducing downtime and maintenance costs. Vfinishors are increasingly embedding AI capabilities into their software platforms, offering applyrs intuitive interfaces and actionable insights. This trfinish appeals to laboratories seeking to optimize workflows and reduce operational burdens. Furthermore, AI-driven automation facilitates high-throughput screening, enabling researchers to conduct larger-scale experiments with greater precision. The ability to integrate diverse data sources and generate holistic insights opens new avenues for research and development.

Growing Demand for Point-of-Care Testing and Decentralized Diagnostics Creates New Avenues

The growing demand for point of care testing and decentralized diagnostics is also expected to enhance the growth of Europe analytical instruments market. Healthcare systems are increasingly shifting towards patient-centric models where testing is performed closer to the patient rather than in centralized laboratories. This shift is driven by the required for rapid diagnosis and treatment decisions, particularly in emergency settings and chronic disease management. According to the World Health Organization, point-of-care tests can reduce turnaround times from days to minutes, improving patient outcomes and reducing hospital stays. The COVID-19 pandemic accelerated this trfinish, highlighting the importance of rapid and accessible diagnostic tools. As per the European Centre for Disease Prevention and Control, the apply of rapid diagnostic tests increased by 50% during the pandem,ic a trfinish that continues to influence healthcare strategies. Manufacturers are responding by developing compact, portable, and simple-to-apply analytical devices that deliver laboratory-quality results. These devices often utilize microfluidics and biosensor technologies, enabling precise analysis with minimal sample volumes. The aging population in Europe further fuels demand for home-based monitoring solutions for conditions such as diabetes and cardiovascular diseases. Governments are supporting this transition through reimbursement policies and infrastructure investments.

MARKET CHALLENGES

Supply Chain Vulnerabilities and Raw Material Shortages Pose Operational Risks

The supply chain vulnerabilities and raw material shortages are affecting manufacturing consistency and delivery schedules, which are limiting the growth of Europe analytical instruments market. The production of analytical instruments relies on specialized components such as detectors, lenses, and electronic chips, which are often sourced from a limited number of global suppliers. According to the European Semiconductor Indusattempt Association, lead times for semiconductor components remained extfinished in 2023, with some items taking over 20 weeks to deliver. Geopolitical tensions and trade restrictions further exacerbate these issues, creating uncertainty in the availability of critical materials. The reliance on single-source suppliers for specific technologies increases the risk of disruption. These delays result in longer wait times for customers, potentially affecting research timelines and clinical operations. Additionally, fluctuations in raw material prices, particularly for rare earth elements applyd in magnets and sensors, impact profit margins. Companies are forced to hold higher inventory levels, tying up capital and increasing storage costs.

Shortage of Skilled Professionals and Technical Expertise Limits Utilization

The shortage of skilled professionals and technical expertise, by limiting the effective utilization of advanced technologies, is also impeding the growth of Europe analytical instruments market. Operating modern analytical instruments requires specialized knowledge in chemisattempt, physics, and data analysis, which is in short supply across the region. Many laboratories struggle to recruit qualified technicians and scientists capable of managing complex workflows and troubleshooting instrument issues. This shortage leads to underutilization of equipment, increased error rates, and longer turnaround times. The rapid evolution of technology further complicates the situation as existing staff require continuous training to keep up with new methodologies and software updates. Small and medium-sized enterprises are particularly affected as they lack resources for extensive training programs. The reliance on external service providers for maintenance and support increases operational costs and depfinishency. Addressing this challenge requires collaborative efforts between educational institutions, indusattempt, and government to enhance STEM education and vocational training.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

6.47% |

|

Segments Covered |

By Product Type, Sales Channel, End User, and Region |

|

Various Analyses Covered |

Global, Regional & Counattempt Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Thermo Fisher Scientific Inc., Agilent Technologies Inc., Danaher Corporation, PerkinElmer Inc., Bruker Corporation, Bio-Rad Laboratories Inc., Waters Corporation, Shimadzu Corporation, METTLER TOLEDO International Inc., Sartorius AG, Eppfinishorf AG, Illumina Inc., F. Hoffmann-La Roche Ltd, Tecan Group Ltd, AMETEK Inc. |

SEGMENTAL ANALYSIS

By Product Type Insights

The molecular spectroscopy segment was the largest by holding 35.4% of the Europe analytical instruments market share in 2025, with the extensive application of techniques such as nuclear magnetic resonance, infrared spectroscopy, and Raman spectroscopy in the pharmaceutical and biotechnology sectors. According to the European Federation of Pharmaceutical Industries and Associations, the pharmaceutical indusattempt in Europe invested over 36 billion Euros in research and development in 2023. A significant portion of this investment is directed towards characterizing new chemical entities and biologics, where molecular spectroscopy is indispensable for determining molecular structure and purity. The increasing complexity of drug molecules, particularly in the realm of monoclonal antibodies and gene therapies, necessitates high-resolution analytical tools that can provide detailed structural insights. Furthermore, regulatory agencies such as the European Medicines Agency require rigorous spectral data for marketing authorization applications, ensuring consistent demand for these instruments. The versatility of molecular spectroscopy allows it to be applyd across various stages of drug development, from early discovery to quality control in manufacturing. Additionally, advancements in instrumentation, such as the integration of artificial ininformigence for spectral analysis, have enhanced throughput and accuracy, building these tools even more attractive to research laboratories.

The mass spectromeattempt segment is projected to register the quickest CAGR of 7.5% from 2026 to 2034, with the expanding field of omics sciences, particularly proteomics and metabolomics, which rely heavily on mass spectromeattempt for identifying and quantifying biological molecules. Mass spectromeattempt offers unparalleled sensitivity and specificity, enabling researchers to detect low-abundance proteins and metabolites in complex biological samples. This capability is crucial for biomarker discovery and personalized medicine initiatives, which are gaining traction across Europe. The European Commission’s Horizon Europe program has allocated substantial funding for health research projects focutilizing on precision medicine, further driving the adoption of advanced mass spectromeattempt systems. Additionally, the integration of mass spectromeattempt with liquid chromatography has streamlined workflows, allowing for high-throughput analysis essential for large-scale clinical studies. The rise of contract research organizations specializing in bioanalysis has also contributed to market growth as these entities invest in state-of-the-art mass spectrometers to serve pharmaceutical clients. The continuous innovation in ionization sources and detectors further enhances the performance of these instruments, attracting a broader applyr base.

By End User Indusattempt Insights

The pharmaceuticals and biotechnology segment was the largest by holding 40.3% of the Europe analytical instruments market share in 202,5 with the region’s robust pharmaceutical indusattempt, which is a global leader in drug innovation and production. According to the European Medicines Agency, over 90 new medicines were approved in 2,023 each requiring extensive analytical testing for safety, efficacy, and quality. Analytical instruments, such as high-performance liquid chromatography, gas chromatography, and mass spectromeattempt, are essential for these processes, ensuring compliance with Good Manufacturing Practice standards. The presence of major pharmaceutical companies in countries like Germany, France, and Switzerland creates a concentrated demand for high-finish analytical equipment. Furthermore, the shift towards biologics and biosimilars has increased the required for sophisticated characterization tools capable of analyzing large and complex molecules. This activity translates into sustained procurement of analytical instruments for research and quality control purposes. The regulatory environment in Europe is among the strictest globally, mandating rigorous testing protocols that drive continuous investment in analytical capabilities. Additionally, the expansion of contract development and manufacturing organizations in the region provides further impetus to this segment as they equip their facilities with advanced analytical technologies to meet client demands.

The environmental monitoring segment is likely to grow at the quickest CAGR of 8.2% from 2026 to 2034, with the implementation of the European Green Deal, which aims to build Europe climate neutral by 2050. The deal includes stringent regulations on air, water, and soil quality, requiring continuous and precise monitoring of pollutants. Techniques, such as atomic absorption spectroscopy and inductively coupled plasma mass spectromeattempt, are widely applyd for detecting heavy metals and other contaminants in water and soil samples. The Industrial Emissions Directive further mandates regular monitoring of industrial discharges, driving demand from manufacturing facilities. Additionally, the Water Framework Directive requires a comprehensive assessment of water bodies, leading to increased investment in water quality monitoring infrastructure by municipal authorities. The growing awareness of microplastics and emerging contaminants has also spurred research and development in new analytical methods. Governments across Europe are allocating significant budreceives for environmental protection projects.

By Sales Channel Insights

The direct sales channel segment accounted in holding 55.3% of the Europe analytical instruments market share in 2025, with the complex nature of analytical instruments, which often require specialized technical knowledge for selection, installation, and maintenance. Manufacturers prefer direct engagement with customers to provide tailored solutions and ensure proper integration into laboratory workflows. According to the European Laboratory Equipment Association, over 60% of high-finish analytical instrument purchases involve direct consultation with manufacturer representatives. This approach allows for better understanding of customer requireds and facilitates the nereceivediation of service contracts and warranty agreements. Large pharmaceutical companies and research institutions often establish long-term relationships with manufacturers through direct channels, ensuring consistent support and access to the latest technologies. The high value of these transactions justifies the cost of maintaining a direct sales force. Additionally, direct sales enable manufacturers to gather valuable feedback for product development and improvement. The trfinish towards solution selling, where instruments are bundled with software and services, further strengthens the direct channel. Customers benefit from single-point accountability and streamlined communication. The ability to offer comprehensive training and after-sales support directly enhances customer satisfaction and loyalty, reinforcing the dominance of this channel.

The e-commerce marketplaces segment is swiftly emerging at a quickest CAGR of 9.5% from 2026 to 2034 with the digital transformation of laboratory procurement processes, particularly for consumables, accessories, and enattempt-level instruments. Laboratories are increasingly adopting online platforms for their convenience, transparency, and competitive pricing. E-commerce enables quick comparison of products and prices, facilitating efficient procurement decisions. The COVID-19 pandemic accelerated this trfinish as restrictions on physical interactions prompted laboratories to shift to online purchasing. Major manufacturers and distributors have enhanced their online presence, offering detailed product information, virtual demonstrations, and seamless ordering processes. The availability of standardized items such as columns, vials, and reagents on e-commerce platforms builds them ideal for online transactions. Additionally, the integration of procurement software with e-commerce platforms allows for automated reordering and inventory management, reducing administrative burdens. Small and medium-sized enterprises and academic labs particularly benefit from the accessibility and ease of apply of e-commerce channels.

REGIONAL ANALYSIS

Germany Analytical Instruments Market Analysis

Germany was the top performer of the Europe analytical instruments market by holding 22.4% of the share in 2025 with its robust manufacturing indusattempt and leading position in pharmaceutical research. The counattempt is home to major pharmaceutical companies, such as Bayer and Merck, which extensively utilize analytical instruments for drug development and quality control. According to the German Chemical Indusattempt Association, the chemical and pharmaceutical sector invested over 10 billion Euros in research and development in 2023. This substantial investment fuels demand for advanced analytical technologies, including chromatography and spectroscopy systems. Germany’s strong engineering tradition supports a vibrant domestic manufacturing base for analytical instruments, with companies like Bruker and Sartorius contributing to global supply. Environmental regulations are also strict in Germany, with the Federal Environment Agency mandating rigorous monitoring of industrial emissions. This drives demand for environmental analytical instruments.

United Kingdom Analytical Instruments Market Analysis

The United Kingdom analytical instruments market held 18.3% of the market share in 2025, with its strong pharmaceutical sector and renowned academic institutions. The UK is a global leader in life sciences, with clusters such as the Golden Triangle comprising Oxford, Cambridge, and London, driving innovation. This activity necessitates extensive apply of analytical instruments for drug discovery and clinical trials. The National Health Service also utilizes analytical tools for diagnostic purposes, further supporting market demand. The UK Research and Innovation agency allocates billions of Pounds annually to scientific projects, many of which require advanced analytical capabilities. Additionally, the counattempt has a strong presence of contract research organizations that serve global pharmaceutical clients, driving instrument procurement.

France Analytical Instruments Market Analysis

France’s analytical instruments market growth is likely to have prominent growth opportunities in the coming years, with the active government support for scientific research and a thriving cosmetics and pharmaceutical indusattempt. The French government has launched the France 2030 investment plan, which allocates 54 billion Euros to strategic sectors, including health and biotechnologies. This funding supports the acquisition of advanced analytical instruments in public laboratories and research centers. The cosmetics indusattempt centered in regions like Paris and Lyon is another key driver, with companies like L’Oreal investing heavily in product safety and efficacy testing. Analytical instruments are essential for analyzing ingredients and ensuring compliance with European regulations. The pharmaceutical sector also contributes significantly, with companies like Sanofi conducting extensive research and development activities. The National Agency for the Safety of Medicines and Health Products enforces strict quality controls, driving demand for analytical testing. Additionally, France is a hub for environmental research with initiatives focapplyd on water and air quality monitoring.

Switzerland Analytical Instruments Market Analysis

Switzerland’s analytical instruments market growth is likely to grow with the high-value pharmaceutical indusattempt and precision manufacturing capabilities. The counattempt is headquarters to global pharmaceutical giants, such as Novartis and Roche, which are among the largest investors in research and development worldwide. This intense focus on innovation drives substantial demand for cutting edge analytical instruments for drug discovery and quality assurance. Switzerland is also home to leading analytical instrument manufacturers such as Mettler Toledo and Buchi, which contribute to the domestic supply chain and export markets. The counattempt’s reputation for precision and quality attracts high-finish laboratory equipment investments. The Swiss National Science Foundation provides generous funding for research projects fostering a vibrant academic community that utilizes advanced analytical tools. Strict regulatory standards enforced by Swissmedic ensure rigorous testing protocols further supporting market demand. The presence of specialized contract research organizations and testing laboratories adds to the ecosystem.

Italy Analytical Instruments Market Analysis

Italy’s analytical instruments market growth is expected to grow with a recovering pharmaceutical indusattempt and a growing emphasis on environmental monitoring. The Italian pharmaceutical sector has revealn resilience and growth, with companies investing in modernization and expansion. The counattempt is also strengthening its environmental monitoring capabilities in response to European Union directives. Government initiatives to improve public health infrastructure have led to upgrades in hospital and diagnostic laboratories. The presence of local distributors and service providers enhances market accessibility.

COMPETITION OVERVIEW

The competition in the Europe analytical instruments market is characterized by a highly consolidated landscape dominated by a few multinational corporations alongside numerous specialized regional players. Major global entities leverage their extensive research and development capabilities, broad product portfolios, and strong brand recognition to maintain leadership positions. These companies compete intensely on the basis of technological innovation, product reliability, and after-sales service quality. The market sees significant rivalry in the development of advanced features such as automation, connectivity, and artificial ininformigence integration, which are becoming standard expectations among sophisticated European customers. Price competition is moderate in the high-finish segment, where performance and precision are prioritized over cost, but remains intense in the mid-range and enattempt-level sectors. Regional players often differentiate themselves by offering customized solutions and personalized customer support tailored to specific local regulatory requirements and indusattempt requireds. Strategic collaborations between instrument manufacturers and software developers are increasingly common as companies seek to provide integrated digital solutions. The threat of new entrants is relatively low due to high barriers to enattempt, including substantial capital requirements and complex regulatory approvals.

KEY MARKET PLAYERS

A few major players of the Europe analytical instruments market include

- Thermo Fisher Scientific Inc

- Agilent Technologies Inc

- Danaher Corporation

- PerkinElmer Inc

- Bruker Corporation

- Bio-Rad Laboratories Inc

- Waters Corporation

- Shimadzu Corporation

- METTLER TOLEDO International Inc

- Sartorius AG

- Eppfinishorf AG

- Illumina Inc

- F. Hoffmann-La Roche Ltd

- Tecan Group Ltd

- AMETEK Inc

Top Strategies Used by Key Market Participants

Key players in the Europe analytical instruments market primarily employ strategies focapplyd on continuous innovation and strategic partnerships to maintain their competitive edge. Companies are heavily investing in research and development to create next-generation instruments that offer higher sensitivity, speed, and automation capabilities. The integration of digital technologies such as artificial ininformigence and machine learning into analytical workflows is a major strategic priority, enabling smarter data analysis and predictive maintenance. Strategic acquisitions of specialized technology firms allow larger corporations to expand their product portfolios and enter new market segments rapidly. Additionally, manufacturers are focutilizing on sustainability by developing eco-frifinishly instruments that reduce energy consumption and waste, aligning with stringent European environmental regulations. Enhancing customer experience through comprehensive service contracts and training programs is another critical strategy to build long-term relationships and ensure customer retention. Companies are also expanding their direct sales forces in key European countries to provide localized support and deepen market penetration.

Leading Players in the Market

- Thermo Fisher Scientific stands as a global leader in the analytical instruments sector, providing comprehensive solutions for laboratories across Europe. The company offers a wide portfolio including mass spectromeattempt, chromatography, and spectroscopy systems that are essential for pharmaceutical, environmental, and academic research. Thermo Fisher has recently focapplyd on expanding its digital capabilities by integrating artificial ininformigence into its instrument software to enhance data analysis and workflow efficiency. They have also invested in expanding their manufacturing and service centers in Germany and Ireland to better serve European customers. Their commitment to sustainability is evident in the development of energy-efficient instruments that reduce laboratory carbon footprints. Their strategic acquisitions of niche technology firms further broaden their product offerings, ensuring they remain at the forefront of analytical technology advancements in the competitive European market landscape.

- Danaher Corporation is a prominent player in the Europe analytical instruments market known for its robust portfolio of life science and diagnostics tools. Through subsidiaries such as Beckman Coulter and Leica Biosystem,s Danaher provides advanced solutions for genomic, proteomic, and cellular analysis. The company has actively pursued growth through strategic acquisitions of innovative biotech firms to expand its technological capabilities and market reach. Recent initiatives include the integration of automation and robotics into analytical workflows to improve throughput and reproducibility for high-volume laboratories. Danaher has also emphasized digital transformation by launching cloud-based data management platforms that enable remote monitoring and collaboration. Their focus on customer-centric innovation ensures that their instruments meet the evolving requireds of researchers and clinicians.

- Agilent Technologies is a key contributor to the Europe analytical instruments market, offering a diverse range of tools for chemical analysis and life sciences. The company specializes in chromatography, mass spectromeattempt, and spectroscopy equipment that is widely applyd in pharmaceutical, food safety, and environmental testing. Agilent has recently strengthened its market position by launching new high-performance instruments designed for enhanced sensitivity and speed. They have also expanded their service and support networks across Europe to ensure timely maintenance and technical assistance for customers. The company is heavily investing in sustainable technologies, developing instruments that consume less solvent and energy, thereby aligning with European environmental regulations. Agilent’s collaborations with academic institutions and research organizations foster innovation and facilitate the adoption of new analytical methods. Their focus on providing integrated solutions that combine hardware, software, and consumables creates a seamless experience for applyrs.

MARKET SEGMENTATION

This research report on the European analytical instruments market has been segmented and sub-segmented based on product type, sales channel, finish applyr & region.

By Product Type

- Chromatography Instruments

- Molecular Spectroscopy

- Elemental Spectroscopy

- Mass Spectromeattempt

By Sales Channel

- Direct Sales

- Distributors and System Integrators

- E-commerce Marketplaces

By End User

- Food and Beverage Testing

- Environmental Testing Laboratories

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe