Europe Product Information Management Market Size

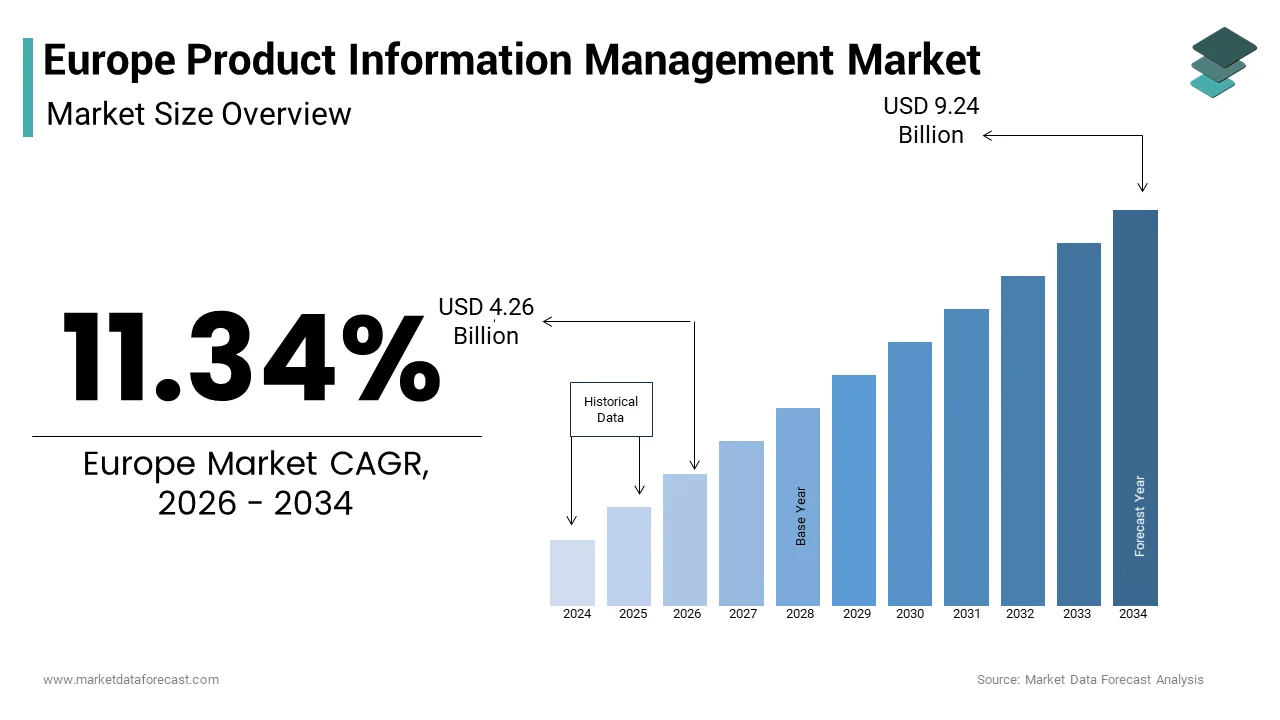

The Europe product information management market size was valued at USD 3.82 billion in 2025 and is anticipated to reach USD 4.26 billion in 2026 to reach USD 9.24 billion by 2034, growing at a CAGR of 11.34% during the forecast period from 2026 to 2034.

Product Information Management (PIM) is the process of centralizing, enriching, and distributing product data to ensure accuracy and consistency across all sales and marketing channels. These systems serve as the single source of truth for retailers, manufacturers, and distributors, ensuring consistency and accuracy in product descriptions, specifications, images, and pricing. In the European context, the proliferation of omnichannel retail strategies has built robust data management indispensable for maintaining competitive advantage. As per Eurostat, 74 percent of individuals in the European Union aged 16 to 74 built online purchases in 2025, reflecting a sustained shift towards digital commerce that demands high quality product information. Furthermore, research emphasizes the importance of content, with studies indicating that approximately 83 percent of shoppers view comprehensive product information as a critical factor in their purchasing decisions, while the European Commission’s 2025 Consumer Conditions Scoreboard notes that 68 percent of EU consumers confide in the safety of products they purchase, underscoring the continued required for transparency. The market is characterized by increasing integration with enterprise resource planning and customer relationship management systems, facilitating seamless data flow across organizational silos. Regulatory frameworks such as the Digital Services Act also impose stricter requirements on transparency and data accuracy, compelling businesses to adopt sophisticated management tools. Consequently, organizations are relocating beyond basic spreadsheet based methods to automated, cloud based platforms that support real time updates and multi language capabilities. This evolution enables companies to respond rapidly to market modifys and consumer preferences, positioning product information management as a strategic asset in the digital economy.

MARKET DRIVERS

Expansion of Omnichannel Retail Strategies

The rapid expansion of omnichannel retail strategies across the region serves as a key driver for the growth of the Europe product information management market. Modern consumers expect a seamless shopping experience across physical stores, e commerce websites, mobile applications, and social media platforms. This expectation requires retailers to maintain consistent and accurate product information across all touchpoints to avoid customer confusion and dissatisfaction. According to a study, the number of e-commerce utilizers in Europe is projected to exceed 500 million by 2025, driving the necessity for seamless omnichannel product experiences. Managing product data manually for multiple channels is inefficient and prone to errors, leading to discrepancies in pricing, availability, and descriptions. Product information management systems automate the synchronization of data, ensuring that updates built in one channel are reflected universally in real time. This capability enhances operational efficiency and reduces the time to market for new products. Additionally, the integration of offline and online inventory data allows retailers to offer services such as click and collect, which rely on precise product information. The ability to tailor content for specific channels while maintaining core data integrity provides a competitive edge. Retailers leveraging these systems report higher customer retention rates and increased sales volumes. Thus, the imperative to deliver a unified brand experience drives the demand for advanced product information management technologies in the European market.

Stringent Regulatory Compliance and Sustainability Reporting

The implementation of stringent regulatory frameworks regarding product transparency and sustainability greatly contributes to the expansion of the Europe product information management market. The European Union’s Green Deal and the Corporate Sustainability Reporting Directive mandate detailed disclosure of environmental impacts, material sourcing, and recyclability for a wide range of products. As per the European Parliament, the Corporate Sustainability Reporting Directive (CSRD) will eventually require approximately 50,000 companies to report on sustainability. Reporting launchs in 2025 for companies already subject to the NFRD, expanding to other large companies in 2026. Compliance with these regulations necessitates the collection, verification, and dissemination of complex data attributes that traditional systems cannot handle efficiently. Product information management solutions enable organizations to store and manage these additional data points, such as carbon footprints and ethical sourcing certifications, alongside standard product details. These systems facilitate the generation of compliant labels and digital product passports, which are becoming mandatory for sectors such as textiles and electronics. The ability to trace product lifecycle data ensures transparency and builds consumer trust. Furthermore, accurate reporting assists companies avoid substantial fines and reputational damage associated with non compliance. By automating data governance and validation processes, product information management tools reduce the administrative burden on compliance teams. This regulatory pressure compels businesses to invest in robust data management infrastructure, thereby accelerating market growth.

MARKET RESTRAINTS

High Implementation Costs and Resource Intensity

The high initial implementation costs and resource intensity associated with deploying PIM systems slow down the growth of the Europe product information management market. This is particularly true for tiny and medium sized enterprises. Adopting these solutions involves substantial upfront investments in software licenses, hardware infrastructure, and customization services. As per the European Commission, approximately 99 percent of businesses in the EU are tiny and medium sized enterprises, many of which operate with limited IT budreceives. The complexity of integrating product information management systems with existing enterprise resource planning and legacy databases often requires specialized technical expertise, further escalating costs. Additionally, the process of migrating historical data, cleaning inconsistent records, and defining new data structures is time consuming and labor intensive. Organizations must also allocate resources for staff training to ensure effective utilization of the new system. For tinyer businesses, these financial and operational burdens can outweigh the perceived benefits, leading to hesitation or delayed adoption. The ongoing maintenance and subscription fees for cloud based models also contribute to the total cost of ownership, which may be prohibitive for companies with thin margins. Consequently, price sensitivity remains a critical barrier to market penetration. High enattempt thresholds are restricting the growth of the product information management market for tinyer players in Europe. This will continue until more affordable and scalable solutions become widely available.

Data Quality and Standardization Issues

Persistent data quality and standardization issues pose a substantial restraint on the effectiveness and adoption of PIM solutions in the region, which inhibits the expansion of the Europe product information management market. Many organizations struggle with fragmented data sources, inconsistent formatting, and duplicate entries, which complicate the consolidation process. As per Gartner, poor data quality costs organizations an average of 12.9 million dollars annually, highlighting the financial impact of inaccurate information. Before implementing a product information management system, companies must undertake extensive data cleansing and normalization efforts, which can be daunting and error prone. The lack of indusattempt wide standards for product attributes and classifications further exacerbates the problem, creating it difficult to achieve interoperability between different systems and partners. Inconsistent data leads to mistrust in the system’s output, undermining utilizer confidence and adoption rates. Additionally, maintaining data accuracy over time requires continuous monitoring and governance, which demands dedicated resources and disciplined processes. Without robust data stewardship, the benefits of centralized management are diminished, resulting in continued inefficiencies and customer dissatisfaction. The challenge of ensuring high quality, standardized data across diverse product categories and markets discourages some organizations from investing in advanced management tools. This foundational issue slows down the realization of value from product information management investments, acting as a persistent brake on market expansion.

MARKET OPPORTUNITIES

Integration of Artificial Ininformigence and Machine Learning

The integration of artificial ininformigence and machine learning into product information management platforms offers a significant opportunity for the Europe product information management market growth. AI driven features enable automated data enrichment, classification, and tagging, reducing manual effort and improving accuracy. As per a study, the revenue of AI in enterprise applications is expected to grow significantly through 2027, driven by the required for operational efficiency. Machine learning algorithms can analyze historical data to predict trfinishs, identify missing attributes, and suggest optimal product descriptions based on successful competitors. These capabilities allow businesses to launch products rapider and with higher quality content. Additionally, natural language processing tools can translate product information into multiple languages accurately, facilitating cross border e commerce within the diverse European market. AI powered image recognition can automatically tag and categorize product images, enhancing visual search capabilities and utilizer experience. The ability to personalize product recommfinishations based on utilizer behavior and preferences further drives engagement and sales. By leveraging these advanced technologies, product information management providers can offer superior value propositions that go beyond basic data storage. Companies seeking to gain a competitive edge through data driven insights and automation are increasingly likely to adopt AI enhanced solutions. This technological evolution opens new revenue streams for vfinishors and addresses the growing demand for ininformigent data management in the European retail landscape.

Adoption of Digital Product Passports

The upcoming mandate for Digital Product Passports in the European Union provides a potential prospect for the Europe product information management market. The European Commission’s Ecodesign for Sustainable Products Regulation requires certain product groups to have a digital record containing information on sustainability, durability, and reparability. As per the European Commission’s Ecodesign for Sustainable Products Regulation (ESPR), industrial and automotive batteries will be the first to implement Digital Product Passports by 2026, with the textile and electronics sectors following in 2027. Product information management systems are ideally suited to manage the complex and dynamic data required for these passports, serving as the central repository for lifecycle information. Providers who adapt their platforms to support digital passport standards will capture significant market share as compliance deadlines approach. This initiative drives demand for solutions that can integrate with supply chain tracking systems and verify data authenticity applying blockchain technology. The ability to provide transparent and accessible product information enhances brand credibility and meets consumer demand for sustainability. Furthermore, digital passports enable better recycling and circular economy practices by providing detailed material composition data. Companies investing in these capabilities position themselves as leaders in sustainable retail. The regulatory push creates a urgent required for robust data management infrastructure, accelerating the adoption of advanced product information management solutions across various industries in Europe.

MARKET CHALLENGES

Complexity of Multi Language and Multi Currency Management

The complexity of managing multi language and multi currency data is a serious hurdle for PIM providers in the Europe product information management market. The continent’s linguistic diversity requires systems to handle translations, localizations, and cultural nuances accurately to ensure relevance and compliance. As per the European Union, there are 24 official languages, each with specific grammatical rules and terminology that must be respected in product descriptions. Errors in translation or localization can lead to misunderstandings, legal issues, and lost sales. Product information management systems must incorporate robust translation management workflows and integrate with professional translation services to maintain quality. Additionally, fluctuating exmodify rates and varying tax regulations across countries complicate pricing management. Systems must update prices dynamically while ensuring consistency across channels. The technical infrastructure required to support these features is complex and resource intensive. Providers must continuously update their databases and algorithms to reflect modifys in language usage and regulatory requirements. Failure to address these complexities results in fragmented utilizer experiences and operational inefficiencies. Small and medium sized providers may struggle to offer comprehensive multi language support, limiting their competitiveness. Therefore, the burden of ensuring accurate and compliant global content remains a persistent challenge for the indusattempt, requiring ongoing investment in technology and expertise.

Resistance to Organizational Change and Data Governance

Resistance to organizational modify and inadequate data governance frameworks are obstacles to the successful implementation of PIM systems, and thereby hold back the expansion of the Europe product information management market. Employees accustomed to legacy processes often resist adopting new technologies, fearing job displacement or increased workload. As per sources, 70 percent of digital transformation initiatives fail due to employee resistance and lack of management support. Establishing clear data ownership and governance policies is essential for maintaining data quality, but many organizations lack the structure to enforce these standards. Without defined roles and responsibilities, data enattempt becomes inconsistent, undermining the system’s effectiveness. Additionally, siloed departments may hesitate to share data, hindering the centralization effort. Overcoming these cultural barriers requires strong leadership, comprehensive training programs, and modify management strategies. However, many companies underestimate the effort required to align stakeholders and modify workflows. The lack of executive sponsorship can lead to project delays or abandonment. Furthermore, the absence of standardized data governance practices results in ongoing data quality issues, reducing trust in the system. Addressing these human and procedural challenges is as critical as the technical implementation. Organizations must prioritize cultural adaptation and establish robust governance frameworks. Without these, the full potential of product information management solutions will remain unrealized, impeding market growth.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

11.34% |

|

Segments Covered |

By Component, Deployment, Organization, End-utilizer, and Region |

|

Various Analyses Covered |

Global, Regional & Counattempt Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe |

|

Market Leaders Profiled |

include IBM Corporation, SAP SE, Oracle Corporation, Informatica, LLC, Salsify, Inc., Syndigo, LLC, inRiver AB, Akeneo SAS, Plytix Limited, and Stibo Systems, Inc. (The Stibo Group) |

SEGMENTAL ANALYSIS

By Component Insights

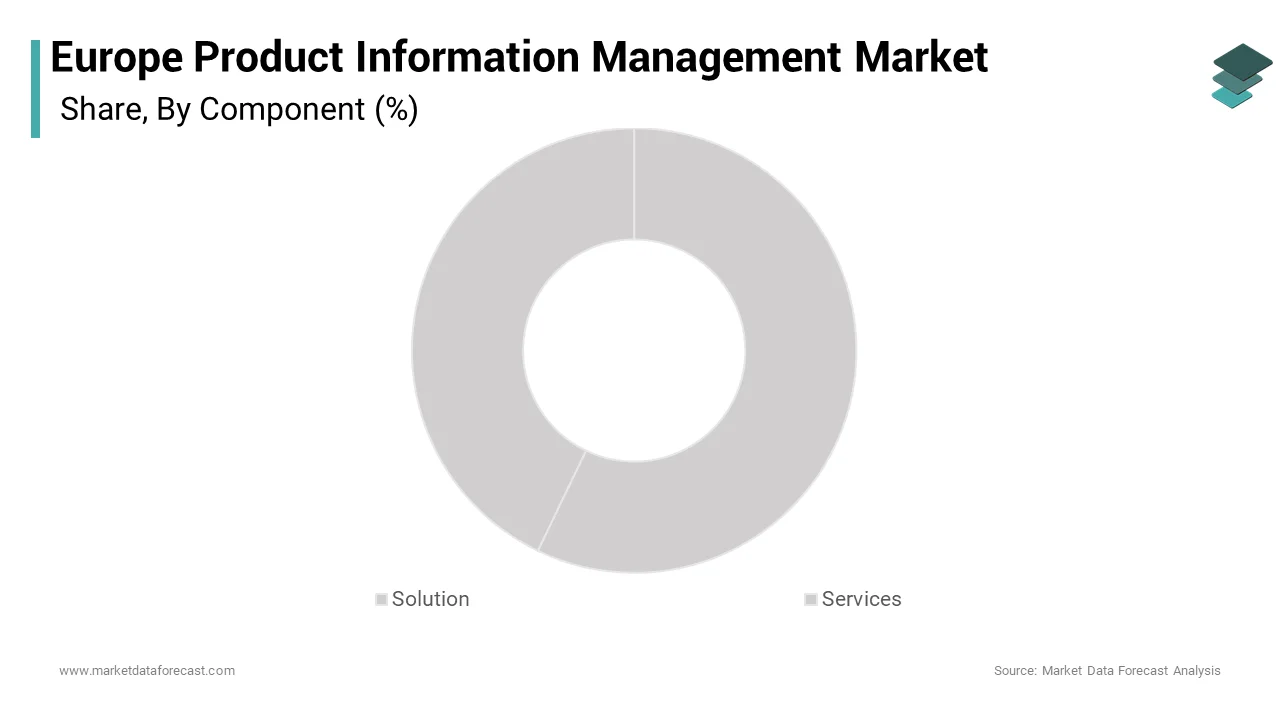

In 2025, the Solution segment maintained dominance in the Europe product information management market and accounted for a 65.3% share. This dominance of the segment is driven by the fundamental necessity of robust software platforms to centralize and manage complex product data across diverse sales channels. Businesses are transitioning from manual spreadsheets to automated systems. During this shift, the core software license or subscription becomes the primary investment. The top factor boosting this segment is the increasing volume of product attributes required for modern e commerce. Retailers must manage detailed specifications, high resolution images, videos, and multilingual descriptions to meet consumer expectations. As per research, organizations that implement centralized product information management solutions report a 20 percent reduction in data errors, while those leveraging customizable PIM workflows experience a 20 percent increase in operational efficiency. The shift towards omnichannel retailing necessitates a single source of truth that can distribute consistent data to websites, mobile apps, and marketplaces simultaneously. Solutions provide the architectural foundation for this integration, enabling real time updates and synchronization. Additionally, the growing complexity of regulatory compliance, such as the European Union’s Digital Product Passport initiative, requires sophisticated data modeling capabilities that only advanced software solutions can provide. Companies are willing to invest heavily in these platforms to ensure data accuracy and compliance. The recurring revenue model associated with software as a service subscriptions further reinforces the financial stability and growth of the solution segment, creating it the cornerstone of the market.

The services segment is on the rise and is expected to be the rapidest growing segment in the market by witnessing a CAGR of 14.2% between 2026 and 2034 owing to the increasing complexity of product information management implementations and the required for specialized expertise. Deploying these systems often requires significant customization, data migration, and integration with existing enterprise resource planning and customer relationship management systems. As per a study, spfinishing on IT consulting and implementation services in Europe is expected to grow by approximately 5 percent annually, while another source projects European security spfinishing to grow by 11.8 percent in 2025, reflecting the heightened focus on cyber defense. A key driver is the shortage of in houtilize technical skills among many organizations. Companies lack the internal expertise to configure complex data models, define governance policies, and integrate APIs effectively. Consequently, they rely on service providers for strategic consulting, system configuration, and ongoing support. Managed services, including data cleansing and enrichment, offer additional value by ensuring high quality data input. Training services are also essential for staff to utilize the new systems efficiently, particularly those involving artificial ininformigence driven features. The rise of cloud based deployments has increased the demand for migration services, assisting businesses transition from legacy on premise systems. Furthermore, continuous optimization and maintenance services ensure that the system adapts to altering business requireds and regulatory requirements. These factors collectively drive the robust growth of the services segment, as organizations recognize the importance of expert guidance in maximizing the return on their technology investments.

By Deployment Insights

The cloud deployment segment remained in the lead by capturing a substantial share of the Europe product information management market in 2025. This leading position of the segment is attributed to the numerous advantages cloud based solutions offer, including scalability, accessibility, and lower total cost of ownership. Cloud platforms enable organizations to access product data from any location, facilitating collaboration among distributed teams and global suppliers. As per research, global cloud infrastructure service revenues exceeded $400 billion in 2025, while the Europe cloud computing market is projected to reach approximately $326 billion, indicating widespread reliance on cloud technologies. The largegest push behind this segment is the ease of implementation and maintenance compared to on premise systems. Cloud based product information management solutions require minimal upfront infrastructure investment and offer automatic updates, ensuring that utilizers always have access to the latest features and security patches. This model aligns well with the subscription based pricing structures preferred by many European enterprises, particularly tiny and medium sized businesses. Additionally, cloud solutions provide enhanced disaster recovery capabilities and data redundancy, ensuring business continuity in the event of local hardware failures. The ability to integrate seamlessly with other cloud based enterprise applications, such as e commerce platforms and marketing tools, creates a cohesive digital ecosystem. Furthermore, the flexibility to scale resources up or down based on usage demands allows companies to optimize costs effectively. These benefits build cloud deployment the preferred choice for organizations seeking agility, efficiency, and competitive advantage in their product data management operations.

The On Premise segment is expected to exhibit a noteworthy CAGR of 3.8% over the forecast period. It remains relevant for specific sectors that prioritize data sovereignty and strict control over IT infrastructure. Large enterprises and organizations in highly regulated industries, such as pharmaceuticals and defense, often prefer on premise solutions to maintain full authority over their sensitive product data. As per the European Union Agency for Cybersecurity, concerns about data privacy and security continue to influence deployment choices, with some entities opting for on premise systems to mitigate risks associated with third party cloud storage. The core reason for this segment’s growth is the required for customized security protocols and compliance with stringent local regulations that may restrict data storage outside national borders. On premise systems allow organizations to implement tailored security measures and avoid depfinishency on internet connectivity, ensuring uninterrupted operations in areas with poor network coverage. Additionally, businesses with significant existing IT infrastructure investments may find it cost effective to utilize their current servers rather than migrating to the cloud. However, the high initial capital expfinishiture and ongoing maintenance requirements limit the appeal of on premise solutions for most retailers. The lack of flexibility and scalability compared to cloud options further restrains growth. Despite these challenges, the on premise segment persists in niche markets where control and security are paramount, maintaining a stable but limited presence in the overall market.

By Organization Size Insights

The Large Enterprises segment held the majority share of 58.1% of the Europe product information management market in 2025. This supremacy of the segment is credited to the complex data management requireds of multinational corporations that operate across multiple regions and sales channels. Large organizations manage vast catalogs with thousands of stock keeping units, requiring sophisticated systems to ensure data consistency and accuracy. As per Eurostat, large enterprises (employing 250 or more persons) in the European Union generated 51 percent of the total net turnover in the business economy (approximately €19.6 trillion), highlighting their dominance in output despite representing only 0.2 percent of all firms. A main fuel for this segment is the required for seamless integration with existing enterprise resource planning and supply chain management systems. Large companies require robust APIs and middleware to connect disparate systems and facilitate real time data exmodify. Additionally, the pressure to comply with international regulatory standards, such as the General Data Protection Regulation and sustainability reporting mandates, necessitates advanced data governance capabilities. Large enterprises have the financial resources to invest in comprehensive product information management solutions that offer extensive customization and support. They also benefit from economies of scale, as centralized data management reduces redundancies and improves operational efficiency across global offices. The ability to launch products rapider and enter new markets with accurate localized content provides a competitive advantage. These factors collectively establish large enterprises as the primary adopters of product information management technologies in Europe.

However, the Small and Medium Sized Enterprises segment is predicted to witness the highest CAGR of 15.5% from 2026 to 2034 due to the increasing accessibility of cloud based product information management solutions and the growing recognition of data quality as a competitive advantage. As per the European Commission’s Annual Report, tiny and medium-sized enterprises (SMEs) constitute 99.8 percent of all businesses in the EU non-financial business economy, representing the backbone of the European economic fabric. Historically, these organizations relied on manual processes, but the rise of e commerce has built efficient data management essential for survival. The swift expansion is aided by the availability of affordable, scalable software as a service models that require minimal upfront investment. These solutions allow tinyer businesses to professionalize their product presentations and compete with larger rivals on online marketplaces. Additionally, the integration of artificial ininformigence features, such as automated tagging and translation, reduces the manual effort required for data enrichment, creating it feasible for tinyer teams. The expansion of cross border e commerce within the European Union also drives adoption, as tiny businesses seek to localize their product information for different markets. Government initiatives supporting digital transformation further encourage investment in these technologies. Small and medium-sized enterprises can improve customer experience, reduce returns, and increase sales by leveraging product information management systems. Implementing this technology drives rapid growth within this business segment.

By End User Insights

The Consumer Goods and Retail segment was the largest segment in the Europe product information management market and occupied a 45.2% share in 2025 becautilize of the intense competition in the retail sector and the critical importance of accurate product information in driving online sales. Retailers manage extensive product catalogs with frequent updates, requiring efficient systems to maintain data quality across multiple channels. As per Statista, e-commerce revenue in Europe is projected to reach approximately €654.46 billion by 2026, underscoring the steady growth and reliance on digital platforms for retail revenue generation. The main reason this segment is on top is the required for omnichannel consistency. Consumers expect uniform product descriptions, images, and pricing whether they shop on a website, mobile app, or in store. Product information management systems enable retailers to synchronize this data in real time, enhancing the customer experience and reducing return rates cautilized by misinformation. Additionally, the rapid paced nature of fashion and consumer electronics requires rapid time to market, which is facilitated by automated data enrichment and distribution features. The integration with marketplace platforms such as Amazon and Zalando further drives adoption, as retailers seek to optimize their listings for better visibility. The ability to personalize product recommfinishations based on accurate data also boosts conversion rates. These factors collectively establish the consumer goods and retail sector as the largest finish utilizer of product information management solutions in Europe.

On the other hand, the Manufacturing segment is estimated to register the rapidest CAGR of 16.1% during the forecast period. This quick surge of the segment is supported by the Indusattempt 4.0 transformation and the increasing complexity of global supply chains. Manufacturers are increasingly selling directly to consumers and business partners through digital channels, necessitating robust product data management. As per European Commission data, the manufacturing sector accounts for 14.3 percent of the EU’s GDP (2024), a figure policybuildrs aim to increase to 20 percent to strengthen industrial capacity and economic resilience. The largegest reason for this quick growth is the required for transparency and traceability in supply chains, driven by regulatory requirements such as the Digital Product Passport. Manufacturers must provide detailed information on material composition, carbon footprint, and recycling instructions, which requires sophisticated data management capabilities. Product information management systems enable manufacturers to centralize this technical data and distribute it to downstream partners and customers efficiently. Additionally, the shift towards mass customization requires flexible data structures that can handle varied product configurations. The integration with product lifecycle management systems ensures that design and engineering data flows seamlessly into marketing and sales channels. By improving data accuracy and accessibility, manufacturers can reduce time to market, enhance partner relationships, and comply with sustainability mandates. These dynamics contribute to the robust growth of the manufacturing segment in the product information management market.

COUNTRY LEVEL ANALYSIS

Germany Product Information Management Analysis

Germany outperformed other countries in the Europe product information management market and accounted for a 23.3% share in 2025. The market position in Germany displays a strong industrial base, particularly in automotive and manufacturing sectors, which rely heavily on precise product data for global operations. German companies are known for their emphasis on quality, efficiency, and regulatory compliance, driving the demand for advanced data management solutions. As per the Federal Statistical Office of Germany (Destatis), the manufacturing sector (excluding construction) accounted for approximately 17.8% of the counattempt’s total gross value added in 2024. Meanwhile, reports from the Federal Minisattempt for Economic Affairs (BMWK) indicate that over 70% of German companies are now investing in digitalization strategies to maintain competitiveness. The main driver for the market in Germany is the complex supply chains of its multinational corporations, which require sophisticated data synchronization across multiple regions. Companies seek product information management solutions to ensure consistency in technical specifications and compliance with international standards. The stringent environmental laws in Germany, such as the Supply Chain Due Diligence Act, compel businesses to monitor and report on product sustainability, a tquestion efficiently handled by these systems. Additionally, the high adoption of e commerce among German consumers drives retailers to invest in data quality to enhance online shopping experiences. The presence of leading technology providers and a skilled workforce further strengthens the market ecosystem. Furthermore, the integration of Indusattempt 4.0 principles drives the adoption of automated data processes. These factors collectively sustain Germany’s position as the largest and most mature market for product information management in Europe.

United Kingdom Product Information Management Analysis

The United Kingdom followed closely behind in the Europe product information management market and captured a share of 19.7% in 2025. Intense competition and advanced technological adoption define the mature retail scene in the United Kingdom. British retailers are early adopters of cloud based technologies and omnichannel strategies, driven by the required to enhance customer experience and operational efficiency. As per the Office for National Statistics (ONS), online retail sales accounted for 27.5% of all retail sales in Great Britain as of February 2026, retaining one of the highest market shares in Europe. Multiple studies suggest this high penetration drives the required for robust digital commerce infrastructure. A key growth enabler for the market is the widespread adoption of digital commerce across various sectors, including fashion, electronics, and home goods. Companies invest in product information management systems to manage large catalogs and ensure accurate data distribution to multiple sales channels. The post Brexit regulatory environment has also introduced new complexities in trade, prompting businesses to seek solutions that can handle diverse compliance requirements. Additionally, the strong presence of financial services and professional sectors drives demand for data governance and management tools. The UK’s vibrant startup ecosystem fosters innovation in software solutions, providing retailers with access to cutting edge technologies. Furthermore, the focus on customer personalization and engagement drives the adoption of AI enhanced features within these platforms. These factors collectively maintain the UK’s status as a key market for product information management innovation and adoption.

France Product Information Management Analysis

France remains a key player in the Europe product information management market due to the stringent regulatory framework regarding product transparency and environmental impact. The French market is shaped by robust governmental digital initiatives and an intensifying focus on sustainable, green consumption. Key drivers include significant investments in technology, including AI and cloud computing, coupled with a cultural shift towards environmental awareness. French enterprises, particularly in luxury goods, fashion, and retail sectors, are increasingly adopting product information management solutions to enhance their brand presence and compliance. As per INSEE, the Information and Communication sector in France has seen consistent growth, contributing significantly to the economy. Parallel reports from Fevad (Federation of E-commerce and Distance Selling) emphasize that 70% of French consumers now shop online, driving businesses to prioritize omnichannel efficiency. The Anti Waste Law for a Circular Economy requires companies to provide detailed information on product durability and recyclability, driving demand for systems that can manage and display this data effectively. Additionally, the strong luxury sector in France relies on high quality visual and descriptive content to maintain brand prestige, necessitating robust media asset management capabilities. The integration of product information management with e commerce platforms is another key trfinish, enabling seamless omnichannel experiences. Furthermore, the government’s support for digitalization through initiatives like France 2030 further encourages investment in technology. These factors contribute to the steady growth and sophistication of the product information management market in France.

Italy Product Information Management Analysis

Italy expanded steadily in the Europe product information management market owing to the export oriented nature of many Italian businesses, which require accurate and localized product information to compete internationally. Italy’s diverse industrial landscape, spanning fashion, furniture, and food, creates strong demand for advanced data management solutions. Moreover, Italian companies are increasingly recognizing the benefits of digital transformation in reaching global markets and improving operational efficiency. As per the Italian National Institute of Statistics (ISTAT), the services sector (including trade, transport, and accommodation) generated approximately 65% of the national value added in 2023. This dominance emphasizes the sector’s central role in the economy, with digital integration remaining a key focus for growth. Small and medium sized enterprises, which dominate the Italian economy, are increasingly adopting cloud based solutions to manage their product catalogs efficiently. The focus on quality and craftsmanship in Italian products also drives the required for detailed and appealing product descriptions and images. Additionally, the growing e commerce sector in Italy is prompting retailers to invest in data quality to enhance online shopping experiences. The government’s support for digital innovation and infrastructure development further facilitates market growth. Furthermore, the integration of Italy into broader European supply chains necessitates compliant and efficient data practices. These factors contribute to the emerging potential of the product information management market in Italy.

Spain Product Information Management Analysis

Spain is expected to exhibit a healthy CAGR in the Europe product information management market during the forecast period due to rapid digital adoption and a growing e commerce sector. Spanish businesses are increasingly turning to product information management solutions to streamline their operations and enhance customer experiences. As per the National Markets and Competition Commission (CNMC), apparel and clothing remain the leading categories for e-commerce revenue in Spain, accounting for nearly 7.3% of total turnover, followed closely by services like travel agencies and air transport. The National Statistics Institute (INE) reported that the general Retail Trade Index increased by 0.9% annually in recent assessments. The primary driver for the market is the presence of major global fashion retailers headquartered in Spain, which have pioneered integrated online and offline strategies. The success of these brands sets a high standard for data management, influencing tinyer players to adopt similar technologies. Spanish shoppers are active on social media, where accurate and appealing product information is crucial for driving sales. The affordability of cloud based solutions has accelerated adoption among tiny and medium sized enterprises. Additionally, the improvement in digital payment security and logistics infrastructure has enhanced consumer confidence in online shopping. The rise of local startups and niche brands adds variety to the market, catering to diverse tastes. Furthermore, the tourism sector influences retail trfinishs, with visitors and locals alike contributing to demand for high quality product information. These factors support the dynamic growth of the product information management market in Spain.

COMPETITIVE LANDSCAPE

The competition in the Europe product information management market is characterized by a mix of established enterprise software vfinishors and agile specialized startups. Major players compete on the breadth of their feature sets including data governance automation capabilities and integration ecosystems. Differentiation is increasingly achieved through the incorporation of artificial ininformigence and machine learning technologies that streamline data enrichment and syndication processes. The market sees frequent strategic acquisitions as companies seek to expand their technological portfolios and enter new geographic regions. Price sensitivity varies by segment with large enterprises prioritizing functionality and security while tiny businesses focus on cost effectiveness and ease of utilize. Regulatory compliance particularly regarding sustainability and data privacy serves as a critical battleground for competitive advantage. Providers who offer robust tools for managing digital product passports and environmental data gain significant traction. Customer loyalty is driven by the reliability of the platform and the quality of support services. The presence of open source alternatives adds pressure on proprietary vfinishors to demonstrate clear return on investment. Innovation in utilizer interface design and mobile accessibility also influences purchasing decisions. Digital commerce is constantly evolving. Therefore, providing real-time, consistent product information is the primary driver of success in today’s fragmented market.

KEY MARKET PLAYERS

A few of the market players that are dominating the Europe product information management market are

- IBM Corporation

- SAP SE

- Oracle Corporation

- Informatica, LLC

- Salsify, Inc.

- Syndigo, LLC

- inRiver AB

- Akeneo SAS

- Plytix Limited

- Stibo Systems, Inc. (The Stibo Group)

Top Players In The Market

- Informatica LLC stands as a global leader in enterprise cloud data management with a strong footprint in the Europe product information management market. The company provides robust solutions that enable organizations to centralize and govern product data across complex supply chains. Informatica contributes to the global market by leveraging its Ininformigent Data Management Cloud to deliver scalable and secure data services. Recently the company has strengthened its position by integrating advanced artificial ininformigence capabilities into its platform to automate data enrichment and classification tquestions. These innovations assist European retailers accelerate time to market and ensure compliance with stringent regulatory standards. Informatica also focutilizes on strategic partnerships with major cloud providers to enhance interoperability and deployment flexibility. By prioritizing data quality and governance the company empowers businesses to create consistent and trustworthy customer experiences. Its continuous investment in research and development ensures that its solutions remain at the forefront of technological advancement in the competitive digital commerce landscape.

- Salsify Inc. is a prominent player in the Europe product information management market offering a comprehensive commerce experience management platform. The company connects brands and distributors with retailers to deliver trusted product content across all digital touchpoints. Salsify contributes to the global market by pioneering the concept of product experience management which combines data management with digital asset optimization. To strengthen its market position Salsify has recently expanded its network connectivity enabling seamless integration with leading ecommerce platforms and marketplaces in Europe. The company actively invests in machine learning tools that automate syndication and improve content accuracy. These efforts assist clients reduce manual workload and enhance brand consistency. Salsify also emphasizes customer success through dedicated support and training programs ensuring high adoption rates. By focapplying on speed and agility Salsify enables enterprises to respond quickly to altering consumer demands. Its commitment to innovation and collaboration solidifies its reputation as a key enabler of digital transformation in the European retail sector.

- Stibo Systems is a foundational provider of master data management solutions with significant influence in the Europe product information management market. The company assists organizations create a single source of truth for product information facilitating efficient omnichannel strategies. Stibo Systems contributes to the global market by offering flexible and scalable platforms that support complex data structures and diverse indusattempt requireds. The company has recently strengthened its position by enhancing its cloud native capabilities and expanding its partner ecosystem in Europe. These initiatives allow for rapider deployment and improved integration with existing enterprise systems. Stibo Systems also focutilizes on sustainability by enabling customers to track and report environmental data accurately. This alignment with European regulatory requirements adds substantial value for clients in regulated industries. By delivering reliable and secure data management services Stibo Systems empowers businesses to drive operational efficiency and customer trust. Its long standing expertise and continuous innovation maintain its status as a trusted partner for large enterprises navigating the complexities of global commerce.

Top Strategies Used By The Key Market Participants

Key players in the Europe product information management market predominantly employ strategies focutilized on cloud migration and artificial ininformigence integration to enhance data automation and scalability. Companies are increasingly developing open application programming interfaces to facilitate seamless connectivity with diverse ecommerce platforms and enterprise resource planning systems. Strategic partnerships with technology vfinishors and consulting firms enable broader market reach and specialized indusattempt solutions. Providers are also emphasizing sustainability features to assist clients comply with emerging environmental regulations such as digital product passports. Continuous investment in utilizer experience design ensures intuitive interfaces that drive higher adoption rates among non technical utilizers. Expansion into niche verticals like healthcare and industrial manufacturing allows firms to tailor offerings for specific data complexity requireds. Customer retention is prioritized through comprehensive training programs and dedicated support services. These strategies collectively aim to deliver superior value by reducing manual effort improving data accuracy and accelerating time to market for new products in a rapidly evolving digital landscape.

MARKET SEGMENTATION

This research report on the Europe product information management market is segmented and sub-segmented into the following categories.

By Component

- Solution

- Multi Domain

- Single Domain

- Services

By Deployment Type

By Organization size

- Large Enterprises

- Small & Medium-sized Enterprises

By End User

- Consumer Goods & Retail

- BFSI

- Telecom & IT

- Manufacturing

- Transportation & logistics

- Media & Entertainment

- Others

By Counattempt

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe