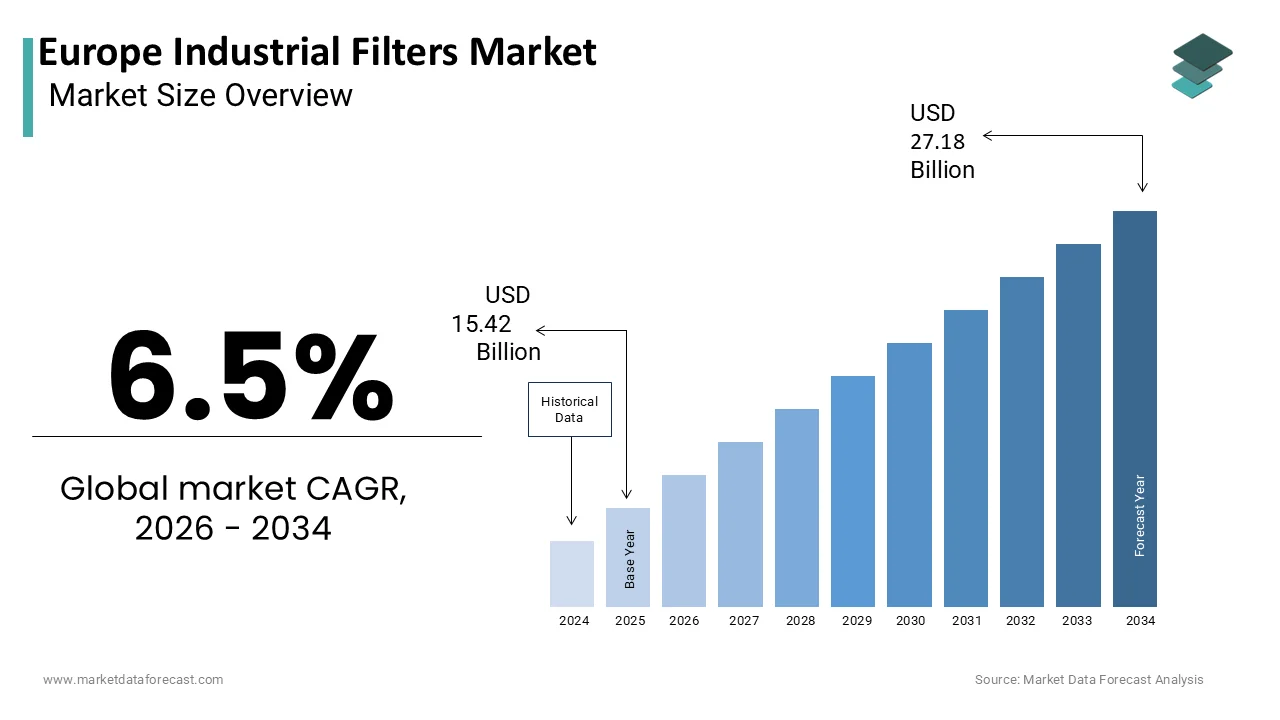

Europe Industrial Filters Market Size

The Europe industrial filters market was valued at USD 15.42 billion in 2025, is estimated to reach USD 16.42 billion in 2026, and is projected to reach USD 27.18 billion by 2034, growing at a CAGR of 6.5% from 2026 to 2034.

The industrial filters are filtration systems and media designed to rerelocate contaminants from liquids, gases, and air within industrial processes. These solutions are maintaining operational efficiency, ensuring product quality, and complying with stringent environmental regulations across sectors such as pharmaceuticals, food and beverage, chemicals, and power generation. Furthermore, the European Environment Agency reported that industrial activities remain a primary source of water pollution, necessitating advanced filtration systems to meet the requirements of the Urban Waste Water Treatment Directive. The integration of Internet of Things sensors into filtration units allows for real-time monitoring and predictive maintenance, enhancing system reliability. According to the European Commission, the Circular Economy Action Plan encourages the adoption of technologies that facilitate resource recovery and waste reduction, driving innovation in filter design and materials. This regulatory and technological landscape fosters a competitive environment where manufacturers must continuously innovate to meet evolving standards. The emphasis on hygiene and safety in the post-pandemic era has further accelerated the adoption of high-efficiency particulate air filters and sterile liquid filtration systems across various industries.

MARKET DRIVERS

Stringent Environmental Regulations and Sustainability Mandates Drive Adoption

The implementation of strict environmental regulations that mandate the reduction of pollutants in industrial emissions and wastewater is additionally amplifying the growth of Europe industrial filters market. The European Union’s Industrial Emissions Directive requires facilities to utilize best available techniques to prevent or minimize emissions to air, water, and land. According to the European Environment Agency, over 50000 industrial installations across Europe are regulated under this directive, compelling them to install high-efficiency filtration systems to comply with emission limits. Additionally, the Water Framework Directive sets ambitious goals for achieving good status of all water bodies, which drives industries to adopt advanced membrane filtration and reverse osmosis technologies for wastewater treatment. As per the European Commission, the revision of the Urban Waste Water Treatment Directive in 2024 introduces stricter limits on micropollutants and nutrients,s requiring upgraded filtration infrastructure. The pharmaceutical and chemical sectors are particularly affected as they generate complex effluents that require specialized filtration media for the removal of active pharmaceutical ingredients and hazardous chemicals. Compliance with these regulations is not optional, and non-compliance results in severe financial penalties and operational shutdowns. Consequently, companies are investing heavily in state-of-the-art filtration solutions to ensure continuous operation and avoid legal repercussions. This regulatory pressure creates a consistent and non-discretionary demand for industrial filters, fostering market growth and technological advancement in the region.

Expansion of the Pharmaceutical and Biotechnology Sectors Fuels Demand

The expansion of the pharmaceutical and biotechnology sectors due to the stringent hygiene and purity standards required in drug production is positively impacting the growth of Europe industrial filters market. Filtration is an essential step in the manufacturing process for sterilizing liquids, rerelocating particulates,s and ensuring the safety of final products. According to the European Federation of Pharmaceutical Industries and Associations, the pharmaceutical indusattempt in Europe invested over 36 billion Euros in research and development in 20,23, leading to the establishment of new manufacturing facilities and production lines. These facilities require advanced filtration systems such as single-utilize filters and tangential flow filtration units to handle sensitive biological molecules and maintain aseptic conditions. The rise of biologics and personalized medicine further amplifies the demand for specialized filtration media capable of handling complex formulations. As per the European Medicines Agency, the number of marketing authorization applications for new medicines has increased steadily, reflecting the vibrant activity in the sector. Good Manufacturing Practice regulations mandate rigorous validation of filtration processes to prevent contamination, ensuring that only high-quality filters are utilized. The trconclude towards continuous manufacturing also requires robust and reliable filtration systems that can operate without interruption.

MARKET RESTRAINTS

High Initial Costs and Maintenance Expenses Restrain Market Penetration

The high initial cost associated with purchasing and installing advanced filtration systems, coupled with significant ongoing maintenance expenses, es is one of the major restraints for the growth of Europe industrial filters market. High-efficiency filters, such as ceramic membranes and nanofiltration units, require substantial capital expconcludeiture, which can be prohibitive for tiny and medium-sized enterprises. According to the study, access to finance remains a challenge for tinyer businesses, with many lacking the resources to invest in expensive technological upgrades. Additionally, the replacement of filter elements and cleaning processes involves recurring costs that add to the total cost of ownership. As per the European Confederation of Plumbi,, ng He a, ting, and Air Conditioning Contractors, energy consumption for operating high-pressure filtration systems can account for a significant portion of operational budreceives, especially in water treatment applications. The complexity of modern filtration systems also requires skilled personnel for operation and maintenance, leading to higher labor costs. This price sensitivity restricts the widespread adoption of premium filtration technologies, particularly in industries with thin profit margins. Furthermore, the lack of standardized pricing for specialized filter media creates uncertainty in budreceiveing. These financial barriers hinder market growth and limit the ability of tinyer players to compete with larger corporations that can afford superior filtration infrastructure.

Supply Chain Disruptions and Raw Material Volatility Impact Production

The supply chain disruptions and volatility in raw material prices, affecting production schedules and cost structures, are another factor degrading the growth of Europe industrial filters market. According to the study, the prices of key raw materials like polypropylene and stainless steel have experienced significant volatility due to geopolitical tensions and energy crises. These fluctuations increase production costs and squeeze profit margins for filter manufacturers. Additionally, logistical bottlenecks and transportation delays have impacted the timely delivery of finished products to customers. As per the European Transport Workers Federation, port congestion and trucker shortages have led to extconcludeed lead times for industrial goods, including filtration systems. The depconcludeence on imports for certain specialized components further exacerbates supply chain vulnerabilities. Manufacturers are forced to hold higher inventory levels to mitigate risk, tying up capital and increasing storage costs. Small and medium-sized manufacturers are particularly vulnerable as they lack the bargaining power to secure favorable terms with suppliers. These supply chain challenges create uncertainty in the market, creating it difficult for companies to plan long-term investments and meet customer demands reliably.

MARKET OPPORTUNITIES

Integration of Smart Technologies and IoT Presents Significant Opportunities

The integration of smart technologies and the Internet of Things into industrial filtration systems is expected to boost the growth of Europe industrial filter market. Smart filters equipped with sensors can monitor parameters, such as pressure drop, flow rate, and contaminant levels in real time, enabling predictive maintenance and optimizing performance. According to the International Data Corporation, the spconcludeing on Internet of Things solutions in the manufacturing sector in Europe is expected to grow significantly,y driven by the necessary for operational efficiency and cost reduction. Smart filtration systems allow operators to detect issues before they lead to failure, res reducing downtime and maintenance costs. The data generated by smart filters can be analyzed to identify trconcludes and optimize filtration cycles, leading to energy savings and extconcludeed filter life. This technology is particularly valuable in critical applications such as pharmaceuticals and food processing, where consistency and reliability are paramount. Manufacturers who offer smart filtration solutions can differentiate themselves in the market and provide added value to customers. The ability to remotely monitor and control filtration systems enhances convenience and operational flexibility.

Development of Sustainable and Bio-Based Filter Materials Creates New Avenues

The development of sustainable and bio-based filter materials, as companies seek to reduce their environmental impact, is expected to substantially enhance the growth of the European filter market. Traditional filter media often rely on synthetic polymers that are non-biodegradable and contribute to plastic waste. In contrast, bio-based filters created from natural fibers, such as cellulose, hemp, and bamboo, also offer a sustainable alternative that aligns with the European Union’s Circular Economy Action Plan. According to the European Bioplastics Association, the production capacity for bioplastics in Europe is increasing, driven by demand for sustainable materials in various applications, including filtration. Bio-based filters can be composted or recycled, reducing landfill waste and environmental pollution. As per the European Environment Agency, the reduction of plastic waste is a key priority for policybuildrs, encouraging industries to adopt greener alternatives. Companies developing innovative bio-based filtration solutions can tap into this growing market segment and appeal to environmentally conscious customers. Government incentives and subsidies for sustainable technologies further support the adoption of bio-based filters. Additionally, the utilize of renewable resources reduces depconcludeency on fossil fuels, enhancing supply chain resilience.

MARKET CHALLENGES

Complexity of Regulatory Compliance Across Different Countries Poses Challenges

The complexity of regulatory compliance, as manufacturers must navigate fragmented legal issues, is likely to pose a challenge to the growth of Europe’s industrial filters market. While the European Union provides overarching directives, individual member states often implement additional national regulations and standards for industrial emissions and wastewater treatment. According to the European Commission, harmonization of environmental laws remains an ongoing process, with discrepancies existing between countries. This fragmentation requires manufacturers to customize their products and documentation to meet specific local requirements, increasing development costs and time to market. Companies must invest in legal expertise and regulatory affairs teams to ensure compliance with diverse regulations. Additionally, frequent updates to environmental laws require continuous monitoring and adaptation of products. In countries like Germany and France, the strict enforcement of environmental regulations adds another layer of complexity. The burden of compliance can be particularly challenging for tiny and medium-sized enterprises with limited resources. This regulatory heterogeneity hinders the seamless distribution of filtration products across Europe and creates barriers to enattempt for new players.

Shortage of Skilled Workforce for Installation and Maintenance Limits Efficiency

The shortage of skilled workforce for the installation and maintenance of advanced industrial filtration systems is a challenge for the growth of Europe industrial filters market. Modern filtration technologies require specialized knowledge for proper setup, operation,o n and troubleshooting. According to the European Centre for the Development of Vocational Training, there is a growing skills gap in the technical sector with a shortage of qualified engineers and technicians. This scarcity leads to delays in installation and increased downtime during maintenance, affecting operational efficiency. The aging workforce in the industrial sector further exacerbates the problem as experienced professionals retire without adequate replacements. The lack of standardized training programs for filtration specialists complicates efforts to upskill the existing workforce. Companies must invest in extensive training initiatives, which increase operational costs and divert resources from other areas. Inadequate maintenance due to a lack of expertise can lead to premature filter failure and reduced performance, undermining the benefits of advanced filtration systems. This skills deficit hinders the widespread adoption of complex filtration technologies, particularly among tiny and medium-sized enterprises.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Segments Covered |

By Type, Filter Media, Indusattempt, Product, and Region. |

|

Various Analyses Covered |

Global, Regional and Counattempt-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

|

Market Leaders Profiled |

Parker Hannifin Corporation, MANN+HUMMEL International GmbH & Co. KG, Donaldson Company, Inc., Eaton Corporation plc, Alfa Laval AB, Camfil Group, Freudenberg Filtration Technologies, Nederman Holding AB, Ahlstrom-Munksjö, Porvair plc, HYDAC International GmbH, BWF Envirotec |

SEGMENTAL ANALYSIS

By Type Insights

The liquid filtration segment was the largest by holding 58.3% of the Europe industrial filters market share in 2025, with the rigorous enforcement of water quality standards across the European Union, which mandates advanced treatment of industrial effluents before discharge. According to the European Environment Agency, the Urban Waste Water Treatment Directive requires member states to ensure that urban wastewater and certain industrial discharges are subject to secondary or equivalent treatment before being released into sensitive areas. This regulatory pressure drives significant investment in membrane filtration, reverse osmosis, nd ultrafiltration systems, particularly in the chemical and pharmaceutical sectors. As per Eurostat, the manufacturing sector in the EU consumed approximately 10 billion cubic meters of water in 202,2 with efficient recycling and purification technologies to minimize freshwater usage and comply with sustainability goals. The pharmaceutical indusattempt, which relies heavily on sterile water for injection and process water, further boosts demand for high-purity liquid filtration solutions. The European Federation of Pharmaceutical Industries and Associations reported that the sector continues to expand its production capacity, requiring robust filtration infrastructure to maintain product quality and safety. Additionally, the food and beverage indusattempt utilizes liquid filtration for clarification, sterilization, and separation processes, ensuring compliance with strict hygiene standards. The combination of regulatory compliance, resource conservation, and quality assurance ensures that liquid filtration remains the dominant segment in the European market.

The air filtration segment is expected to witness the rapidest CAGR of 6.8% from 2026 to 2034, owing to the increasing awareness of indoor air quality and the necessary to control industrial particulate emissions to meet environmental standards. According to the World Health Organization, air pollution remains a significant health risk in Europe, prompting stricter regulations on industrial emissions under the Industrial Emissions Directive. Facilities in the power generation, cement, and metal processing sectors are upgrading their air filtration system,s including baghoutilizes and electrostatic precipitators, to reduce particulate matter release. As per the European Centre for Disease Prevention and Control, the post-pandemic emphasis on hygiene and ventilation has led to widespread adoption of High Efficiency Particulate Air filters in manufacturing cleanrooms and healthcare facilities. The rise of smart manufacturing and Indusattempt 4.0 initiatives also drives demand for advanced air filtration systems equipped with sensors for real-time monitoring of air quality and filter performance. The European Commission’s Green Deal aims to achieve zero pollution for air, water, and soil by 2050, which further incentivizes industries to invest in high-efficiency filtration technologies.

By Filter Media Insights

The nonwoven fabric segment was the largest by holding 35.3% of the Europe industrial filters market with the versatility of nonwoven materials, which can be engineered to specific pore sizes and permeability levels, creating them suitable for a wide range of filtration applications. Nonwoven fabrics offer a balance of efficiency and pressure drop, creating them ideal for bag filters and cartridge filters utilized in various industries. As per the research, the demand for meltblown and spunbond nonwovens has increased due to their effectiveness in capturing fine particles and contaminants. The cost-effectiveness of nonwoven media compared to woven fabrics or membranes builds them attractive for high-volume applications where frequent replacement is required. In the automotive sector, onwoven filters are extensively utilized for engine air intake and cabin air filtration, driving consistent demand. The ability to customize nonwoven properties such as hydrophobicity and chemical resistance further enhances their appeal. Manufacturers continue to innovate in fiber technology to improve filtration efficiency and lifespan.

The activated carbon charcoal segment is lucratively growing at an anticipated CAGR of 7.5% over the coming years, with the stringent regulations on volatile organic compound emissions and the increasing necessary for odor control in industrial processes. According to the European Chemicals Agency, the implementation of the REACH regulation has tightened controls on hazardous substances, prompting industries to adopt advanced adsorption technologies. Activated carbon filters are highly effective in rerelocating organic contaminants, gases, and odors from air and water streams, creating them essential in the chemical, pharmaceutical, and wastewater treatment sectors. As per the study, many municipal and industrial wastewater treatment plants are upgrading their tertiary treatment stages with activated carbon filtration to rerelocate micropollutants, such as pharmaceutical residues and pesticides. The food and beverage indusattempt also utilizes activated carbon for decolorization and purification of products, ensuring high-quality standards. Advances in activated carbon technologies, such as impregnated carbons, enhance removal efficiency for specific contaminants, ts expanding the application scope. Government incentives for reducing air and water pollution further support the adoption of activated carbon filters.

By Indusattempt Insights

The chemicals and petrochemicals segment was the largest by occupying 22.5% of the Europe industrial filters market share in 2025, with the filtration in separating catalysts, purifying intermediates,s and treating wastewater in chemical production processes. According to the European Chemical Indusattempt Council, the chemical indusattempt is one of the largest manufacturing sectors in Europe, requiring extensive filtration solutions to maintain product purity and operational efficiency. The sector faces strict environmental regulations regarding the discharge of hazardous substances, necessitating advanced filtration systems, such as membrane filters and centrifuges. As per the German Chemical Indusattempt Association, investments in sustainable production technologies have increased with a focus on reducing waste and energy consumption through efficient filtration. The petrochemical sub-sector also relies heavily on filtration for refining processes, including the removal of impurities from crude oil and natural gas. The transition towards bio-based chemicals and circular economy practices further drives demand for specialized filtration media capable of handling diverse feedstocks. The presence of major chemical hubs in Germany, Belgium,m and the Netherlands creates a concentrated demand for industrial filters. Continuous innovation in filtration technology to handle corrosive and high-temperature environments supports market growth.

The pharmaceuticals segment is expected to grow at an anticipated CAGR of 8.2% from 2026 to 2034, with the stringent regulatory requirements for sterility and purity in drug manufacturing, which mandate the utilize of high-efficiency filtration systems. According to the European Federation of Pharmaceutical Industries and Associations, the indusattempt is increasingly shifting towards biologics and personalized medicines, which require complex downstream processing involving tangential flow filtration and sterile filtration. As per the European Medicines Agency, good manufacturing practice guidelines require rigorous validation of filtration processes to prevent contamination,n ensuring consistent demand for high-quality filters. The expansion of pharmaceutical production facilities in Europe, driven by the necessary for supply chain resilience post-pandemic, further boosts market growth. Single-utilize filtration technologies are gaining popularity due to their convenience and reduced risk of cross-contamination. The increasing prevalence of chronic diseases and an aging population in Europe drives demand for pharmaceutical products, thereby expanding production volumes. Government support for research and development in life sciences also contributes to the adoption of advanced filtration technologies.

By Product Insights

The bag filter segment accounted in holding 25.4% of the Europe industrial filters market share in 2025, with the simplicity, reliability, and cost effectiveness of bag filters in capturing particulate matter from air and liquid streams. According to the European Industrial Filtration Society, bag filters are extensively utilized in industries such as cement, power generation, and food processing for bulk dust collection and clarification processes. Their ability to handle high dust loads and varying particle sizes builds them a preferred choice for heavy-duty applications. The demand for baghoutilize systems has remained stable due to their proven performance and ease of maintenance. In liquid applications, bag filters are widely utilized for pre-filtration to protect downstream membranes and equipment, extconcludeing their lifespan. The availability of various filter media options, including polyester, polypropylene, and felt, allows customization for specific chemical and thermal conditions. The lower initial investment compared to cartridge or membrane filters builds bag filters attractive for tiny and medium-sized enterprises. Regulatory pressures to reduce particulate emissions also drive the adoption of efficient bag filtration systems.

The HEPA filter segment is projected to register the rapidest CAGR of 9.1% from 2026 to 2034, with the increasing emphasis on indoor air quality and the necessary for sterile environments in pharmaceutical electronics and healthcare facilities. According to the European Committee for Standardization, HEPA filters are required to capture at least 99.95% of airborne particles, creating them essential for cleanroom applications. As per the European Centre for Disease Prevention and Control, the pandemic has heightened awareness of airborne transmission of pathogens,s leading to widespread adoption of HEPA filtration in hospitals, labs, and public buildings. The semiconductor indusattempt, which requires ultra-clean air to prevent contamination of microchips, is also a major driver of HEPA filter demand. The European Semiconductor Indusattempt Association reported increased investment in fabrication facilities in Europe, boosting the necessary for high-efficiency air filtration. Regulatory standards for cleanrooms, such as ISO 14644, mandate the utilize of HEPA filters, ensuring consistent demand. Advances in filter media technology have improved airflow and reduced energy consumption, creating HEPA filters more efficient.

COUNTRY LEVEL ANALYSIS

Germany Industrial Filters Market Analysis

Germany was the top performer in the Europe industrial filters market with 22.8% of share in 2025, owing to its robust chemical, automotive, and pharmaceutical industries. The counattempt is home to major manufacturing hubs that require advanced filtration solutions for process optimization and emission control. According to the German Federal Environment Agency, strict enforcement of the Federal Immission Control Act mandates industries to install high-efficiency filtration systems to limit air and water pollutants. The automotive sector, which is a key pillar of the German economy, utilizes extensive filtration for paint shops, engine testing, and cabin air quality. As per the German Engineering Federation, the demand for industrial filtration equipment has grown due to the transition towards electric vehicles, which require new manufacturing processes and cleanroom environments. The chemical indusattempt in regions like Ludwigshafen and Leverkutilizen relies heavily on membrane and cartridge filters for production and wastewater treatment. Government incentives for sustainable manufacturing and resource efficiency further drive the adoption of advanced filtration technologies. The presence of leading filter manufacturers and research institutions fosters innovation and local supply chain resilience.

United Kingdom Industrial Filters Market Analysis

The United Kingdom industrial filters market was positioned second by holding 18.2% of the market share in 2025. The UK is home to major pharmaceutical companies and contract manufacturing organizations that require high-purity filtration solutions for drug production. According to the Association of the British Pharmaceutical Indusattempt, the sector continues to invest in new facilities and technologies to maintain global competitiveness, driving demand for sterile and process filters. The power generation sector is also undergoing transitions with increased focus on renewable energy and biobiomass, which require specialized air and gas filtration systems. As per the UK Department for Environment, ent Food and Rural Affairs, regulations on industrial emissions and wastewater discharge are strictly enforced, prompting industries to upgrade their filtration infrastructure. The food and beverage indusattempt, which is a major contributor to the UK economy, utilizes extensive filtration for product clarification and safety.

France Industrial Filters Market Analysis

France’s industrial filters market growth is likely to be driven by its unique industrial mix, including nuclear energy, aerospace, and luxury goods. The nuclear power sector, which provides a significant portion of France’s electricity,y requires specialized filtration for coolant purification and radioactive waste management. According to the French Alternative Energies and Atomic Energy Commission, strict safety standards mandate the utilize of high-efficiency filters to ensure operational safety and environmental protection. The aerospace indusattempt centered in Touloutilize and Paris utilizes advanced air and liquid filtration for manufacturing composite materials and maintaining cleanrooms. As per the French Minisattempt of Ecological Transition, regulations on industrial waste and emissions are rigorously enforced, driving the adoption of sustainable filtration technologies. The wine and spirits indusattempt, which is a major export sector, relies on filtration for clarification and sterilization, ensuring product quality. Government support for green indusattempt initiatives encourages companies to adopt energy-efficient filtration systems.

Italy Industrial Filters Market Analysis

Italy’s industrial filters market growth is likely to grow with its diverse manufacturing base in textiles, food, and machinery. The textile indusattempt, which is prominent in regions like Lombardy and Veneto,o utilizes extensive filtration for wastewater treatment to rerelocate dyes and chemicals. According to the Italian National Institute of Statistics, environmental regulations have tightened, ed requiring textile manufacturers to adopt advanced membrane filtration systems for water recycling. As per the Italian Minisattempt of Ecological Transition, incentives for sustainable industrial practices encourage the adoption of energy-efficient filtration technologies. The machinery sector, which produces filtration equipment for export,t also contributes to market dynamics.

Spain Industrial Filters Market Analysis

Spain’s industrial filters market growth is likely to grow with investment in renewable energy and water scarcity challenges. According to the water scarcity issues drive the adoption of advanced desalination and wastewater treatment technologies applying membrane filtration is driven. The food and beverage indusattempt, particularly in wine and olive oil production,n utilizes filtration for quality enhancement. Tourism-driven hospitality sectors also invest in water and air filtration for hotels and resorts. Government grants for modernizing industrial infrastructure support the uptake of efficient filtration solutions. The strategic location for trade with Africa and Latin America also influences market dynamics.

COMPETITIVE LANDSCAPE

The competition in the Europe industrial filters market is characterized by a mix of global conglomerates and specialized regional manufacturers vying for dominance in various industrial sectors. Leading companies leverage their extensive research and development capabilities and broad product portfolios to offer comprehensive filtration solutions. The market sees intense rivalry in the development of sustainable and energy-efficient technologies, which are critical for meeting European environmental standards. Price competition is moderate in the high-conclude segment, where performance and reliability are prioritized, but remains significant in the standard product category. Strategic partnerships with industrial equipment manufacturers and engineering firms assist secure large-scale projects and long-term contracts. Companies differentiate themselves through superior technical support, customization capabilities,, and after-sales service. The threat of new entrants is moderate due to high barriers related to technology patents and regulatory compliance. This dynamic environment drives continuous innovation, ensuring that customers benefit from advanced filtration technologies while pushing companies to optimize their operational efficiencies and value propositions for diverse industrial applications.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global Europe Industrial Filters Market include

- Parker Hannifin Corporation

- MANN+HUMMEL International GmbH & Co. KG

- Donaldson Company, Inc.

- Eaton Corporation plc

- Alfa Laval AB

- Camfil Group

- Freudenberg Filtration Technologies

- Nederman Holding AB

- Ahlstrom-Munksjö

- Porvair plc

- HYDAC International GmbH

- BWF Envirotec

TOP LEADING PLAYERS IN THE MARKET

- Mann+Hummel is a global leader in filtration solutions with a strong presence in the Europe industrial filters market. The company specializes in air intake systems, liquid filtration,n and membrane technologies for various industrial applications. Mann+Hummel has recently strengthened its position by expanding its production capabilities for sustainable filter media and investing in digital monitoring solutions. They have launched innovative products designed to reduce energy consumption and extconclude service intervals for industrial clients. Their commitment to research and development ensures they remain at the forefront of filtration technology. Their extensive distribution network and technical expertise allow them to serve diverse sectors, including automotive chemicals and power generation, effectively across the European region.

- Donaldson Company is a prominent player in the Europe industrial filters market,t known for its advanced filtration and contamination control solutions. The company offers a wide range of products for dust, fume, mist, and liquid filtration, serving industries such as manufacturing, turning mining, and life sciences. Donaldson has recently focutilized on integrating smart technologies into its filtration system,s enabling predictive maintenance and real-time performance tracking. They have expanded their portfolio through strategic acquisitions of specialized filtration firms to enhance their technological capabilities. Their emphasis on sustainability drives the development of eco-friconcludely filter materials and energy-efficient systems. Donaldson’s robust customer support and engineering services strengthen its market position.

- Alfa Laval is a key contributor to the Europe industrial filters market, specializing in separation,n heat transfer, and fluid handling technologies. The company provides advanced centrifugal separators and membrane filtration systems for the food, beverage,g,e, pharmaceutical, ca,l, and chemical industries. Alfa Laval has recently strengthened its market position by launching next-generation membrane solutions that offer higher efficiency and lower operational costs. They have invested in digital tools that optimize filtration processes and reduce waste for industrial clients. Their focus on sustainability aligns with European regulations promoting resource efficiency and environmental protection. Alfa Laval collaborates closely with customers to develop customized solutions that address specific process challenges.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Europe industrial filters market primarily employ strategies focutilized on product innovation and sustainability to maintain a competitive advantage. Companies are increasingly investing in research and development to create energy-efficient and eco-friconcludely filtration solutions that comply with strict environmental regulations. Strategic acquisitions of niche technology firms allow larger corporations to expand their product portfolios and enter new market segments rapidly. Manufacturers are also integrating digital technologies such as Internet of Things sensors into their products to enable predictive maintenance and remote monitoring. This enhances customer value by reducing downtime and optimizing operational efficiency. Additionally, firms are expanding their service offerings to include comprehensive maintenance and consulting packages, which build long-term customer relationships. Marketing efforts emphasize the total cost of ownership benefits of advanced filtration systems. These multifaceted strategies enable market participants to adapt to modifying regulatory landscapes and customer demands while driving growth and profitability in the dynamic European environment.

MARKET SEGMENTATION

This research report on the europe industrial filters market is segmented and sub-segmented into the following categories.

By Type

- Liquid Filtration

- Air Filtration

By Filter Media

- Nonwoven Fabric

- Activated Carbon / Charcoal

By Indusattempt

- Chemicals & Petrochemicals

- Pharmaceuticals

By Product

By Counattempt

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe