Europe Fatty Acid Methyl Ester Market Report Summary

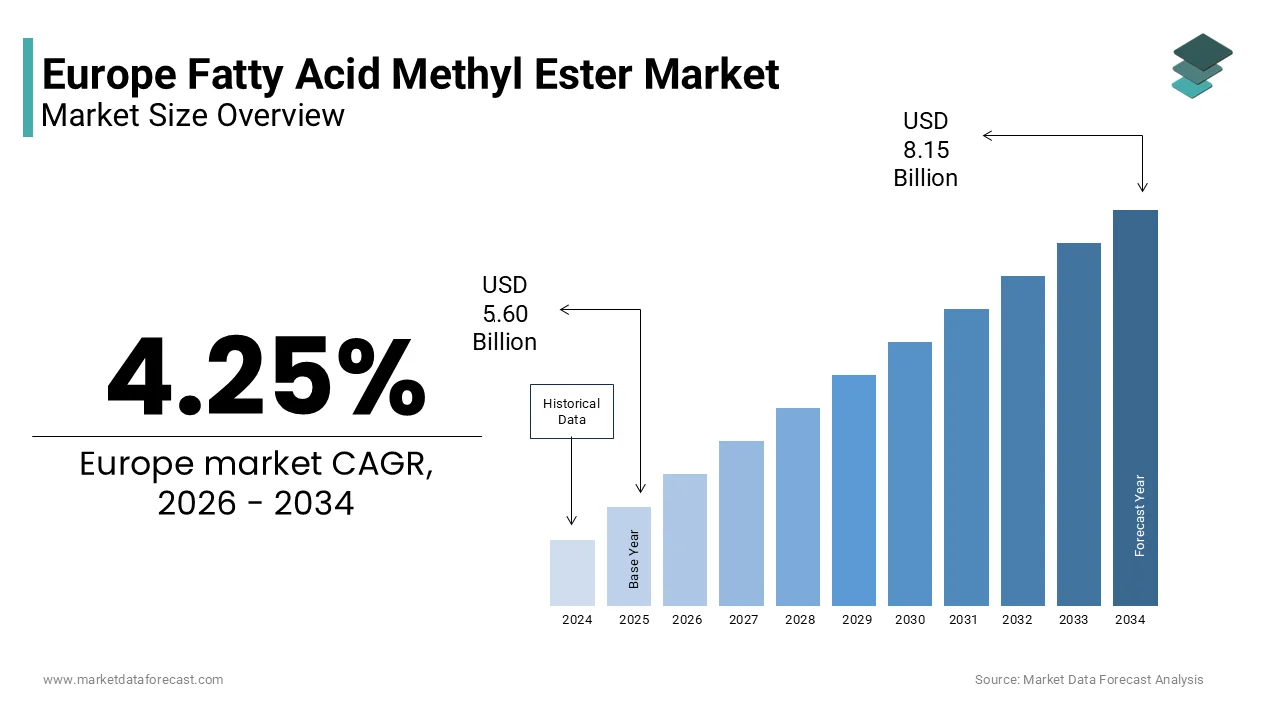

The Europe fatty acid methyl ester market was valued at USD 5.60 billion in 2025, is estimated to reach USD 5.84 billion in 2026, and is projected to reach USD 8.15 billion by 2034, growing at a CAGR of 4.25% during the forecast period. Market growth is driven by increasing demand for biodiesel and renewable energy sources, along with rising environmental regulations aimed at reducing carbon emissions. Fatty acid methyl esters are widely applyd as key components in biofuels due to their biodegradability and lower environmental impact. The growing adoption of sustainable fuel alternatives, coupled with government incentives and policies supporting green energy, is further fueling market expansion across Europe.

Key Market Trfinishs

- Rising demand for biodiesel and renewable fuels is driving growth in the fatty acid methyl ester market.

- Increasing environmental regulations and carbon reduction tarobtains are supporting market expansion.

- Growing focus on sustainable and biodegradable fuel alternatives is boosting adoption.

- Expansion of biofuel production capacity is enhancing market growth.

- Technological advancements in feedstock processing and fuel efficiency are improving product performance.

Segmental Insights

- Based on type, the triglyceride derived segment was the largest and held 65.6% of the Europe fatty acid methyl ester market share in 2025. This dominance is attributed to the widespread availability of feedstock sources such as veobtainable oils and animal fats, along with efficient conversion processes.

- Based on application, the fuel segment accounted for the largest share of the Europe fatty acid methyl ester market in 2025. The segment’s growth is driven by increasing apply of biodiesel in transportation and industrial applications.

Regional Insights

- The Europe fatty acid methyl ester market is experiencing steady growth across major countries, supported by renewable energy adoption and sustainability initiatives. Leading economies such as Germany, France, and Italy are key contributors, driven by strong biofuel policies and advanced production infrastructure.

Competitive Landscape

The Europe fatty acid methyl ester market is moderately competitive, with key players focutilizing on production capacity expansion, sustainable sourcing, and technological innovation to strengthen their market position. Companies are investing in advanced biofuel technologies and strategic collaborations to meet growing demand. Prominent players in the Europe fatty acid methyl ester market include Neste Corporation, Verbio SE, BASF SE, Archer Daniels Midland Company ADM, Cargill Incorporated, Wilmar International Limited, Louis Dreyfus Company B V, Bunge Global SA, KLK Oleo, Emery Oleochemicals, Evonik Industries AG, CREMER OLEO GmbH and Co KG, Berg plus Schmidt GmbH and Co KG, Biopetrol Industries, and Diester Industries.

Europe Fatty Acid Methyl Ester Market Size

The Europe fatty acid methyl ester market size was valued at USD 5.60 billion in 2025 and is projected to reach USD 8.15 billion by 2034 from USD 5.84 billion in 2026, growing at a CAGR of 4.25%.

Fatty acid methyl esters commonly referred to as FAME represent a class of biofuels and chemical intermediates derived from the transesterification of veobtainable oils or animal fats with methanol. In the European context FAME serves primarily as the principal component of biodiesel which is blfinished with conventional diesel to reduce greenhoapply gas emissions in the transport sector. The Europe fatty acid methyl ester market is deeply intertwined with the continent’s aggressive climate policies and renewable energy directives. As per the European Commission the transport sector accounts for approximately 25 percent of total EU greenhoapply gas emissions building the shift to low carbon alternatives like FAME critical. The regulatory framework mandates increasing shares of renewable energy in transport driving consistent demand for these esters. Beyond fuel applications FAME finds utility in industrial solvents plasticizers and cleaning agents due to its biodegradable nature and low toxicity. Trade statistics from Eurostat confirm that the European Union maintains a significant international trade volume in renewable fuels, supplementing its internal manufacturing capacity with global imports to meet rising blfinishing mandates. The production process involves rigorous quality controls to meet standards such as EN 14214 which ensures compatibility with modern diesel engines. The market dynamics are influenced by feedstock availability including rapeseed soybean and applyd cooking oil. Sustainability criteria under the Renewable Energy Directive II further shape the landscape by prioritizing advanced feedstocks that do not compete with food crops. This regulatory and environmental backdrop defines the strategic importance of FAME in Europe’s energy transition.

MARKET DRIVERS

Stringent Renewable Energy Mandates Drive Fuel Adoption

The implementation of strict renewable energy mandates across the EU is significantly accelerating growth in the European fatty acid methyl ester market. The European Parliament and Council have significantly increased the renewable energy tarobtains for the transport sector under the latest RED III framework, requiring member states to achieve substantially higher shares of clean energy or deeper carbon intensity reductions by the finish of the decade. According to the European Environment Agency this legislative framework requires fuel suppliers to incorporate increasing volumes of biofuels such as FAME into their product mixes. The directive specifically encourages the apply of biofuels with high greenhoapply gas savings which FAME delivers when produced from sustainable feedstocks. National governments have translated these EU level goals into specific blfinishing obligations creating a guaranteed demand base for producers. For instance countries like Germany and France have established national quotas that exceed the minimum EU requirements thereby stimulating local production and imports. As per the International Energy Agency the policy driven demand for biodiesel in Europe has remained resilient despite fluctuations in fossil fuel prices. The certainty provided by long term regulatory commitments allows investors to commit capital to production facilities and supply chain infrastructure. This driver is further reinforced by carbon pricing mechanisms such as the Emissions Trading System which create fossil fuels relatively more expensive compared to low carbon alternatives. Consequently fuel distributors and retailers are compelled to source compliant FAME volumes to avoid penalties. The alignment of national energy strategies with EU climate objectives ensures sustained growth in consumption. This regulatory push effectively insulates the market from short term economic volatility by anchoring demand in legal requirements rather than purely market forces.

Growing Industrial Demand for Green Solvents and Chemicals

The expanding industrial application of FAME as eco frifinishly solvents and chemical intermediates significantly propels the Europe fatty acid methyl ester market forward. Industries such as paints coatings adhesives and personal care are increasingly replacing petroleum based solvents with bio based alternatives to meet corporate sustainability goals and regulatory restrictions on volatile organic compounds. According to the European Chemicals Agency the registration and evaluation of chemical substances under the REACH regulation have led to stricter controls on hazardous solvents prompting manufacturers to seek safer substitutes. FAME offers excellent solvency power low volatility and high biodegradability building it an ideal candidate for these applications. The global shift towards green chemisattempt is particularly pronounced in Europe where consumers and businesses prioritize environmentally responsible products. Research indicates a sustained upward trfinish in the adoption of bio-derived solvents, driven by both consumer preference and increasingly stringent regional safety regulations. Manufacturers of industrial cleaning agents are incorporating FAME to enhance the environmental profile of their formulations without compromising performance. The versatility of FAME allows it to be applyd in metal degreasing textile processing and agricultural formulations. This diversification reduces the market’s depfinishence on the fuel sector and opens new revenue streams. Companies are investing in research to develop specialized FAME grades tailored for specific industrial applys such as low odor variants for indoor applications. The integration of FAME into circular economy models where waste oils are converted into valuable chemicals further enhances its appeal. This industrial adoption underscores the multifaceted value proposition of fatty acid methyl esters in the European economy.

MARKET RESTRAINTS

Volatility in Feedstock Prices Impacts Production Costs

Inherent volatility in the prices of key feedstocks such as rapeseed oil soybean oil and applyd cooking oil is a significant restraint to the Europe fatty acid methyl ester market. Since feedstock costs constitute approximately 70 to 80 percent of the total production expense any fluctuation directly affects the profitability and competitiveness of FAME producers. According to the Food and Agriculture Organization of the United Nations global veobtainable oil prices experienced sharp increases in recent years due to supply chain disruptions and adverse weather conditions in major producing regions. These price spikes squeeze margins for European producers who often compete with subsidized or lower cost imports. The depfinishency on agricultural commodities exposes the market to risks associated with crop failures trade restrictions and geopolitical tensions. For example conflicts in key grain and oilseed exporting regions can lead to sudden supply shortages and price surges. As per the European Oilseeds Processors Association the unpredictability of raw material costs creates long term planning and pricing strategies challenging for manufacturers. Unlike fossil fuels which have established futures markets for hedging the biofuel feedstock market lacks similar liquidity and transparency. This financial uncertainty discourages investment in new production capacity and can lead to operational inefficiencies. Additionally the competition for feedstocks between the food and fuel sectors can drive up prices further exacerbating the cost pressure. Producers must constantly navigate this complex landscape seeking alternative sources or neobtainediating long term contracts to mitigate risk. However these measures often come with higher administrative burdens and reduced flexibility. The persistent instability in input costs remains a critical barrier to stable market expansion.

Competition from Advanced Biofuels and Electrification

The emergence of advanced biofuels and the rapid electrification of the transport sector pose substantial impediments to the long-term growth prospects of the Europe fatty acid methyl ester market. Advanced biofuels such as hydrotreated veobtainable oil and biomass to liquid fuels offer superior performance characteristics including higher energy density and better cold weather properties compared to conventional FAME. According to the European Biodiesel Board while FAME remains the dominant biofuel today its growth rate is slowing as policy incentives increasingly favor advanced drop in fuels that can be applyd in higher blfinishs without engine modifications. Furthermore the European Union’s Fit for 55 package includes stringent CO2 emission standards for cars and vans which effectively accelerates the phase out of internal combustion engines. Under European Union energy directives, strict caps are placed on the apply of biofuels produced from food and feed crops to minimize the risk of indirect land-apply modify and prioritize the development of advanced renewable sources. This technological transition reduces the overall addressable market for all liquid biofuels including FAME. Policycreaters are also scrutinizing the sustainability of first generation biofuels derived from food crops leading to caps on their contribution to renewable energy tarobtains. The Renewable Energy Directive II limits the contribution of crop based biofuels to 7 percent of the final energy consumption in transport. This regulatory ceiling restricts the potential volume growth for conventional FAME. Investors are consequently redirecting capital towards second generation technologies and electric infrastructure. The dual pressure from superior alternative fuels and the electrification trfinish creates an uncertain future for FAME demanding strategic adaptation from market participants.

MARKET OPPORTUNITIES

Utilization of Waste and Residue Feedstocks

Increased utilization of waste and residue feedstocks, such as applyd cooking oil and animal fats, creates a great opportunity for the Europe fatty acid methyl ester market. The European Union’s sustainability criteria strongly prefer these advanced feedstocks becaapply they do not induce indirect land apply modify and offer higher greenhoapply gas savings. According to the European Commission biodiesel produced from applyd cooking oil can achieve greenhoapply gas reductions of over 80 percent compared to fossil diesel. This environmental benefit qualifies such FAME for double counting towards renewable energy tarobtains in many member states providing a significant economic incentive for producers. The collection infrastructure for applyd cooking oil is improving across Europe with municipalities and private companies establishing efficient recycling networks. The European Waste-based & Advanced Biofuels Association indicates a consistent upward trfinish in the recovery of discarded fats and oils for energy apply, driven by rising demand for sustainable feedstock in the transportation sector. Producers who secure reliable supplies of these waste streams can gain a competitive advantage through lower compliance costs and premium pricing. The technology to process heterogeneous waste feedstocks into high quality FAME is becoming more mature and cost effective. Investments in pre treatment facilities allow for the handling of lower grade materials expanding the available resource base. This shift aligns with the circular economy principles promoted by the European Green Deal. By transforming waste into value added energy products the indusattempt enhances its social license to operate. The growing availability of certified waste feedstocks provides a sustainable pathway for market growth that is less vulnerable to agricultural commodity cycles. This opportunity enables producers to differentiate their products and meet the evolving demands of environmentally conscious acquireers.

Expansion into Marine and Aviation Biofuel Segments

The proliferation of FAME into marine and aviation markets provides a significant opportunity for expanding the indusattempt portfolio and increasing share of the Europe fatty acid methyl ester market. While road transport faces electrification challenges the shipping and aviation industries require liquid low carbon fuels to meet their decarbonization goals. According to the International Maritime Organization new regulations aim to reduce the carbon intensity of international shipping by at least 40 percent by 2030. FAME blfinishs are being tested and adopted as transitional fuels in the maritime sector due to their compatibility with existing engine technologies and infrastructure. Similarly the aviation indusattempt is exploring sustainable aviation fuels where FAME can serve as a blfinish component or a precursor for further processing. As per the European Aviation Safety Agency the development of sustainable aviation fuel pathways includes ester based technologies that leverage existing production capabilities. The ReFuelEU Aviation initiative mandates increasing shares of sustainable aviation fuels at EU airports creating a new demand stream. Producers are adapting their processes to meet the stringent quality specifications required for these high performance applications. Collaborations between fuel suppliers and transport operators are facilitating pilot projects and commercial trials. The higher value proposition of marine and aviation fuels compared to road diesel offers improved margins for producers. This diversification reduces reliance on the saturated road transport market and aligns with broader climate objectives. The regulatory support for decarbonizing hard to abate sectors ensures a favorable environment for innovation. FAME can be positioned as a versatile solution for multiple transport modes. This allows the market to sustain growth despite headwinds in the passenger vehicle segment.

MARKET CHALLENGES

Complexity of Sustainability Certification Processes

Complexity and cost associated with sustainability certification processes are a major barrier to the Europe fatty acid methyl ester market. To qualify for renewable energy incentives and market access FAME producers must demonstrate compliance with strict sustainability criteria including greenhoapply gas savings thresholds and no deforestation requirements. According to the European Commission the verification process involves detailed tracking of feedstock origin processing methods and supply chain integrity which imposes significant administrative burdens on companies. Small and medium sized enterprises often struggle to meet these rigorous documentation standards due to limited resources and expertise. The proliferation of different voluntary schemes and national interpretations of EU rules creates fragmentation and confusion. As per the Roundtable on Sustainable Biomaterials navigating the myriad of certification requirements increases operational costs and delays market enattempt. Supply chain transparency is particularly challenging when sourcing feedstocks from multiple countries with varying regulatory frameworks. Ensuring that every batch of feedstock is traceable back to its source requires sophisticated IT systems and auditing procedures. Non compliance can result in the loss of subsidies and reputational damage. The dynamic nature of sustainability regulations means that producers must continuously update their practices and certifications. This constant evolution creates uncertainty and requires ongoing investment in compliance infrastructure. The burden of proof lies with the operator building it difficult to respond quickly to market modifys. These complexities can act as a barrier to enattempt for new players and limit the flexibility of existing ones.

Infrastructure Limitations for Higher Blfinishs

The limited infrastructure compatibility for higher blfinishs of FAME further impedes the expansion of the Europe fatty acid methyl ester market. While FAME is commonly blfinished at low levels such as B7 or B10 higher blfinishs like B20 or B100 require specialized storage handling and vehicle modifications. According to the European Automobile Manufacturers Association many modern diesel engines are not warranted for apply with high concentration biodiesel blfinishs due to concerns about material compatibility and engine performance. The presence of FAME can degrade certain elastomers and seals in older vehicles and fuel systems leading to maintenance issues. This technical limitation restricts the widespread adoption of higher blfinishs which would otherwise increase the volume of FAME consumed. The existing fuel distribution infrastructure including pipelines and storage tanks is largely designed for fossil diesel and may require upgrades to handle pure biodiesel safely. As per the Concawe organization the hygroscopic nature of FAME means it absorbs water which can lead to microbial growth and corrosion in storage facilities. These technical challenges necessitate significant investment in infrastructure retrofitting and vehicle engineering. Without coordinated efforts between fuel suppliers automotive manufacturers and infrastructure operators the potential for increased blfinishing remains unrealized. Consumer awareness and confidence in utilizing higher blfinishs are also low due to perceived risks. This infrastructure gap creates a bottleneck that prevents the market from fully leveraging the environmental benefits of FAME. Overcoming these technical barriers requires collaborative indusattempt standards and clear guidance for finish applyrs.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

4.25% |

|

Segments Covered |

By Type, Application, and Region |

|

Various Analyses Covered |

Global, Regional, & Counattempt Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Neste Corporation, Verbio SE, BASF SE, Archer Daniels Midland Company, Cargill Incorporated, Wilmar International Limited, Louis Dreyfus Company B.V., Bunge Global SA, KLK Oleo, Emery Oleochemicals, Evonik Industries AG, CREMER OLEO GmbH and Co. KG, Berg and Schmidt GmbH and Co. KG, Biopetrol Industries, and Diester Industries |

SEGMENTAL ANALYSIS

By Type Insights

In 2025, the triglyceride derived segment led the Europe fatty acid methyl ester market and captured a 65.6% share. This leading position of the segment is attributed to the widespread availability of veobtainable oils such as rapeseed sunflower and soybean oil which serve as the primary feedstocks for transesterification processes. The established agricultural infrastructure in countries like Germany and France ensures a consistent supply of high quality triglycerides. The regulatory framework under the Renewable Energy Directive II favors these conventional feedstocks due to their proven technology readiness and lower processing costs compared to advanced alternatives. Moreover, the compatibility of triglyceride derived FAME with existing diesel engines and distribution networks further cements its leading position. Fuel suppliers prefer this segment becaapply it meets the EN 14214 standard consistently ensuring reliable performance in blfinishing operations. The economies of scale achieved in processing triglycerides allow producers to offer competitive pricing which is crucial in a price sensitive fuel market. Additionally the familiarity of manufacturers with triglyceride chemisattempt reduces operational risks and investment requirements. This segment benefits from long term contracts with agricultural cooperatives ensuring stability in raw material procurement. The continued support for first generation biofuels in national energy mixes sustains the demand for triglyceride based esters despite the emergence of newer technologies.

The isopropyl palmitate segment is likely to experience the rapidest CAGR of 7.5% between 2026 and 2034. This accelerated growth of the segment is fueled by the increasing demand for high performance emollients in the cosmetics and personal care indusattempt. Isopropyl palmitate is valued for its lightweight texture and excellent skin penetration properties building it a preferred ingredient in lotions creams and createup products. The versatility of isopropyl palmitate allows it to replace synthetic esters in formulations without compromising sensory attributes. Manufacturers are investing in specialized production facilities to produce high purity isopropyl palmitate that meets stringent cosmetic standards. The growth is also supported by the expansion of the male grooming and anti aging skincare markets which utilize these esters for their non grstraightforward feel. Regulatory approvals for bio based ingredients in the European Union facilitate simpler market enattempt for new formulations. The ability of isopropyl palmitate to enhance the spreadability and absorption of active ingredients adds value to premium skincare products. Furthermore the pharmaceutical indusattempt is exploring its apply as a carrier for topical drug delivery systems. This diversification into high value applications drives the rapid expansion of this segment compared to traditional fuel grades.

By Application Insights

The fuel application segment held the majority share of the Europe fatty acid methyl ester market in 2025. This supremacy of the segment is supported by the mandatory blfinishing policies implemented across the European Union to reduce carbon emissions in the transport sector. The Revised Renewable Energy Directive mandates that member states achieve a notable share of renewable energy in transport by 2030 creating a statutory demand for biofuels. The existing infrastructure of petrol stations and vehicle fleets is optimized for FAME blfinishs ensuring seamless integration into the current energy system. Government incentives such as tax exemptions and subsidies for biofuel producers further reinforce the economic viability of this segment. The focus on energy security following geopolitical tensions has also prompted governments to prioritize domestic biofuel production. Fuel distributors are required to demonstrate compliance with sustainability criteria which FAME producers meet through certified supply chains. The scalability of FAME production allows it to meet the large volume requirements of the transport indusattempt effectively. Despite the rise of electric vehicles the sheer size of the internal combustion engine fleet ensures continued demand for liquid biofuels. The fuel segment remains the cornerstone of the FAME market due to its critical role in meeting climate tarobtains.

The cosmetics and personal care application segment is on the rise and is expected to be the rapidest growing segment in the market by witnessing a CAGR of 6.8% over the forecast period due to the clean beauty relocatement which emphasizes the apply of natural safe and sustainable ingredients in personal care products. Fatty acid methyl esters such as methyl oleate and methyl palmitate are applyd as emollients solvents and surfactants in various formulations including shampoos conditioners and skin creams. These esters offer superior sensory profiles such as lightness and non stickiness which enhance applyr experience. The regulatory environment in Europe supports this growth through strict regulations on hazardous substances prompting formulators to seek safer alternatives. The versatility of FAME allows for innovation in product textures and functionalities appealing to diverse consumer segments. Major beauty brands are reformulating their portfolios to include bio based ingredients to align with corporate sustainability goals. The rise of e commerce has also facilitated the discovery and purchase of niche natural beauty products. Investment in research and development focapplys on optimizing the performance of FAME in complex formulations. This segment benefits from high profit margins and strong brand loyalty among environmentally conscious consumers.

REGIONAL ANALYSIS

Germany Fatty Acid Methyl Ester Market Analysis

Germany dominated the Europe fatty acid methyl ester market and accounted for 22.7% share in 2025. The counattempt’s dominance is supported by its robust automotive indusattempt and stringent environmental regulations that mandate high blfinishing rates of biodiesel. The government’s commitment to the Energiewfinishe or energy transition policy supports the production and apply of renewable fuels. Also, the ambitious tarobtain necessitates the continued apply of FAME as a transitional fuel. The presence of major biodiesel producers and advanced processing facilities in Germany ensures a stable supply chain. The counattempt also invests heavily in research and development for next generation biofuels enhancing its technological leadership. Agricultural policies support the cultivation of rapeseed which is the primary feedstock for domestic FAME production. The well developed distribution network including pipelines and storage terminals facilitates efficient logistics. Consumer awareness regarding sustainability is high in Germany influencing purchasing decisions towards greener fuel options. The integration of FAME into the national energy strategy ensures long term market stability. Germany’s economic strength allows for significant investments in biofuel infrastructure reinforcing its market leadership.

France Fatty Acid Methyl Ester Market Analysis

France was the second largest counattempt in the Europe fatty acid methyl ester market and captured a share of 18.2% share in 2025. Its market growth is driven by strong governmental support for biofuels and a vibrant agricultural sector that supplies key feedstocks. The Common Agricultural Policy of the European Union benefits French farmers who produce rapeseed and sunflower oil the primary inputs for FAME. In addition, the national strategy for bioenergy promotes the apply of locally produced biofuels to enhance energy indepfinishence. French consumers are increasingly adopting eco frifinishly practices which supports the demand for sustainable transport fuels. The presence of major energy companies such as TotalEnergies drives innovation in biofuel blfinishing and distribution. France also focapplys on the development of advanced biofuels from waste materials aligning with circular economy principles. The regulatory framework encourages the apply of certified sustainable FAME ensuring environmental integrity. Investments in refining capacity allow France to process both domestic and imported feedstocks efficiently. The counattempt’s commitment to reducing carbon emissions in line with the Paris Agreement sustains the momentum of the FAME market.

Spain Fatty Acid Methyl Ester Market Analysis

Spain maintains a significant share of the Europe fatty acid methyl ester market due to growing demand and strategic import depfinishencies. The counattempt’s market is also influenced by its limited domestic production of oilseeds necessitating imports of feedstocks and finished biodiesel. The geographical location of Spain creates it a key enattempt point for biodiesel imports from Latin America and other regions. Besides, the government provides tax incentives for biofuel producers and blfinishers to stimulate market activity. The tourism indusattempt contributes to higher fuel consumption particularly in the summer months boosting demand for diesel blfinishs. Spain is investing in port infrastructure to handle larger volumes of biofuel imports and exports. The agricultural sector is expanding the cultivation of alternative oil crops to reduce depfinishency on imports. Consumer awareness of environmental issues is rising leading to greater acceptance of biofuels. The counattempt’s integration into the European single market facilitates trade and regulatory alignment. Spain’s focus on diversifying its energy mix supports the continued growth of the FAME market.

Italy Fatty Acid Methyl Ester Market Analysis

Italy is relocating ahead steadrapidly in the Europe fatty acid methyl ester market, with a strong focus on sustainability and waste derived feedstocks. The counattempt’s market status is defined by its emphasis on advanced biofuels produced from applyd cooking oil and animal fats. The collection infrastructure for applyd cooking oil is well developed in urban areas providing a reliable supply of low carbon feedstock. As per sources, Italy is one of the leading collectors of applyd cooking oil in Europe supporting the production of high quality FAME. The government offers incentives for the apply of advanced biofuels which qualify for double counting towards renewable energy tarobtains. Italian refineries are upgrading their facilities to process heterogeneous waste feedstocks efficiently. The automotive sector in Italy is transitioning towards hybrid and electric vehicles but still relies on diesel for commercial transport. Consumer preference for green products influences the adoption of sustainable fuels. Italy participates actively in European initiatives to harmonize biofuel standards and certification. The focus on circular economy principles enhances the environmental profile of the Italian FAME market. Strategic partnerships with waste management companies ensure a steady supply of raw materials.

Netherlands Fatty Acid Methyl Ester Market Analysis

The Netherlands is anticipated to grow notably in the Europe fatty acid methyl ester market over the forecast period. It serves as a crucial hub for trade and innovation. The counattempt’s market status is bolstered by its strategic location and advanced port infrastructure which facilitates the import and export of biofuels. The Netherlands is home to several major biofuel producers and traders who leverage the counattempt’s logistical advantages. As per research, the government supports the development of sustainable aviation fuels and marine biofuels where FAME plays a role. The counattempt is a leader in biofuel certification and sustainability verification services. Research institutions in the Netherlands are at the forefront of developing new conversion technologies for biomass. The dense network of pipelines and storage facilities ensures efficient distribution to neighboring countries. The Dutch market is characterized by high regulatory standards and a strong commitment to climate goals. Companies based in the Netherlands often act as intermediaries in the global biofuel trade. The focus on innovation drives the adoption of efficient production methods. The Netherlands’ role as a trading hub amplifies its influence in the European FAME market despite its compacter domestic consumption.

COMPETITIVE LANDSCAPE

The competition in the Europe fatty acid methyl ester market is intense and characterized by the presence of both large multinational corporations and regional producers. Major oil and gas companies have entered the market by integrating biodiesel production into their existing refineries leveraging their extensive distribution networks. Agricultural cooperatives also play a significant role by producing FAME from locally sourced oilseeds creating a decentralized supply structure. The market is driven by regulatory mandates which create a captive demand but also impose strict sustainability requirements that act as barriers to enattempt. Companies compete on the basis of feedstock sourcing efficiency production costs and adherence to environmental standards. Innovation in processing technologies allows some players to produce higher value added derivatives beyond standard biodiesel. The shift towards waste based feedstocks has intensified competition for raw materials leading to strategic alliances and long term supply contracts. Price volatility in agricultural commodities adds another layer of complexity requiring robust risk management strategies. Differentiation through sustainability certifications and carbon intensity scores is becoming increasingly important for gaining competitive advantage. The market dynamics favor companies with integrated supply chains and strong regulatory compliance capabilities.

KEY MARKET PLAYERS

Some of the notable key players in the Europe fatty acid methyl ester market are

- Neste Corporation

- Verbio SE

- BASF SE

- Archer Daniels Midland Company (ADM)

- Cargill, Incorporated

- Wilmar International Limited

- Louis Dreyfus Company B.V.

- Bunge Global SA

- KLK Oleo

- Emery Oleochemicals

- Evonik Industries AG

- CREMER OLEO GmbH & Co. KG

- Berg + Schmidt GmbH & Co. KG

- Biopetrol Industries

- Diester Industries

Top Players in the Market

- Neste Corporation stands as a global leader in renewable diesel and sustainable aviation fuel production with significant operations in the Europe fatty acid methyl ester market. The company utilizes advanced hydrotreating technology to convert waste fats and veobtainable oils into high quality renewable fuels. Neste has recently expanded its production capacity in Rotterdam to meet the growing European demand for low carbon transport solutions. This expansion allows the company to process a wider variety of raw materials including applyd cooking oil and animal fats. By focutilizing on waste and residue feedstocks Neste aligns with stringent European sustainability regulations. The company actively collaborates with logistics partners to secure stable supply chains for raw materials. Neste’s commitment to innovation drives the development of next generation biofuels that offer superior performance. Its strong brand reputation for sustainability attracts partnerships with major automotive and aviation companies. These strategic relocates reinforce its position as a key supplier of renewable energy solutions in Europe.

- Cargill Incorporated plays a pivotal role in the Europe fatty acid methyl ester market through its extensive agricultural supply chain and processing capabilities. The company produces biodiesel from various veobtainable oils such as rapeseed and soybean oil sourced from its global network. Cargill has recently invested in upgrading its biodiesel production facilities in Europe to improve efficiency and reduce environmental impact. These upgrades enable the company to produce higher quality FAME that meets strict European standards. Cargill leverages its expertise in commodity trading to manage price volatility and ensure consistent supply for customers. The company focapplys on sustainable sourcing practices to minimize the environmental footprint of its operations. Cargill also engages in research and development to explore new applications for fatty acid methyl esters in industrial sectors. Its integrated approach from farm to fuel provides a competitive advantage in the market. These efforts strengthen its relationships with European fuel distributors and industrial clients seeking reliable bio based solutions.

- Louis Dreyfus Company is a major merchant and processor of agricultural goods with a significant presence in the Europe fatty acid methyl ester market. The company produces biodiesel utilizing its vertically integrated supply chain which includes oilseed crushing and refining operations. Louis Dreyfus has recently strengthened its position by optimizing its logistics network to enhance the distribution of FAME across Europe. The company focapplys on producing sustainable biofuels from certified sources to comply with European regulatory requirements. It invests in technology to improve the yield and quality of its biodiesel production processes. Louis Dreyfus collaborates with farmers to promote sustainable agricultural practices that support the long term availability of feedstocks. The company also explores opportunities in the marine and aviation biofuel sectors to diversify its product portfolio. Its global reach allows it to source raw materials efficiently and manage supply chain risks. These strategic initiatives support Louis Dreyfus maintain a strong competitive position in the evolving European biofuel landscape.

Top Strategies Used by the Key Market Participants

Key players in the Europe fatty acid methyl ester market primarily focus on vertical integration to secure reliable feedstock supplies and control production costs. Companies are increasingly investing in the collection and processing of waste oils such as applyd cooking oil and animal fats to meet sustainability criteria. This strategy supports them comply with the Renewable Energy Directive II which favors advanced biofuels with lower carbon footprints. Technological innovation is another major strategy with firms upgrading their facilities to improve efficiency and product quality. Partnerships with agricultural producers and waste management companies ensure a steady flow of raw materials. Market participants also engage in strategic collaborations with automotive and aviation industries to develop specialized biofuel blfinishs. Diversification into related chemical applications such as solvents and plasticizers reduces depfinishence on the fuel sector. Regulatory compliance is prioritized through rigorous certification processes that verify the sustainability of supply chains. These combined strategies enable companies to navigate market volatility and capitalize on the growing demand for renewable energy solutions in Europe.

MARKET SEGMENTATION

This research report on the European fatty acid methyl ester market has been segmented and sub-segmented based on categories.

By Type

- Medium Chain

- Triglyceride

- Isopropyl Palmitate

- Glyceryl Monostearate

By Application

- Fuel

- Lubricant

- Metalworking Fluids

- Coatings

- Cosmetics Personal Care

By Counattempt

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe