Europe Chipset Market Size

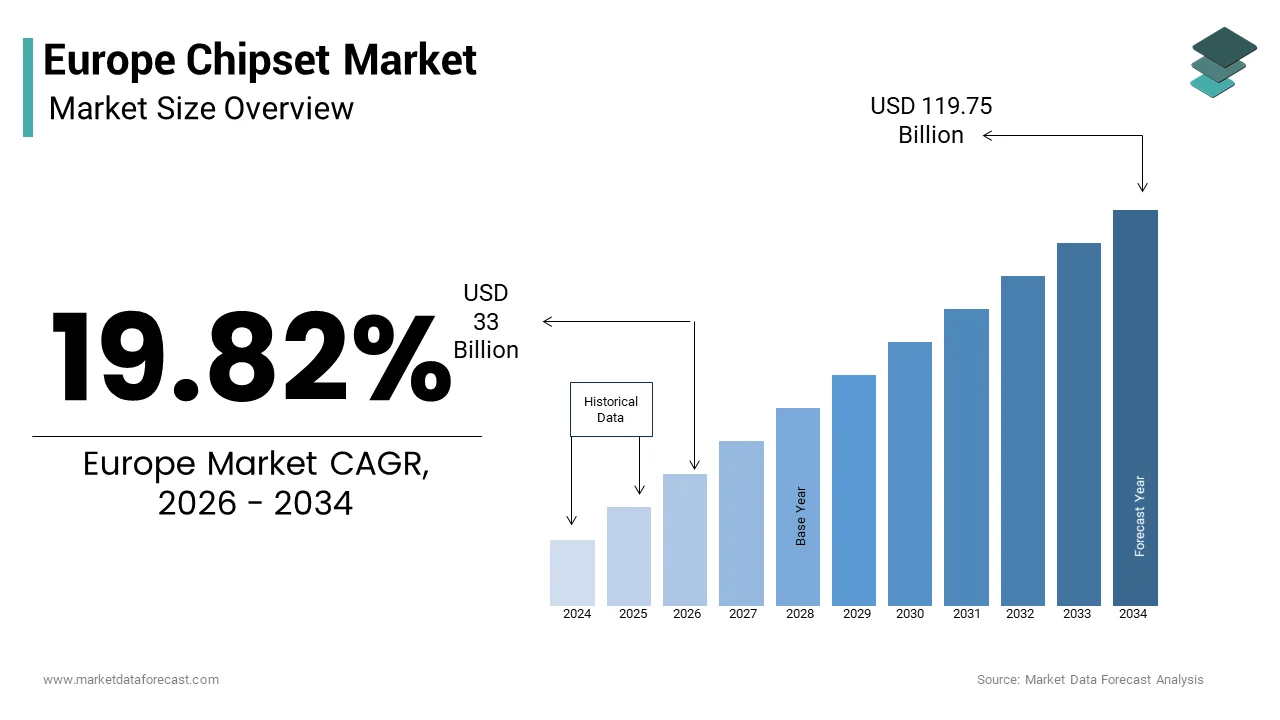

The Europe chipset market size was valued at USD 27.54 billion in 2025 and is anticipated to reach USD 33 billion in 2026 to reach USD 119.75 billion by 2034, growing at a CAGR of 19.82% during the forecast period from 2026 to 2034.

The chipset is the intricate network of entities involved in the design, fabrication, packaging, and distribution of integrated circuits that power the digital infrastructure of the continent. These semiconductor components act as the central nervous system for a vast array of applications, ranging from high performance automotive microcontrollers to industrial automation sensors and telecommunications equipment. As per Eurostat, the European Union recorded a production value of approximately 85 billion euros for computer, electronic, and optical products in 2024, underscoring the massive industrial depfinishency on local chipset integration. The legislative framework provided by the European Chips Act aims to double the region’s global market share to 20% by 2030 by signaling a decisive shift away from external depfinishencies. According to the International Semiconductor Industest Association, Europe currently commands nearly 10% of global semiconductor sales, with a particularly strong hold on the automotive microcontroller segment where European firms maintain a leading position. This push for self-sufficiency has accelerated capital expfinishiture into next generation node technologies, ensuring that local industries remain competitive against Asian and North American rivals in an increasingly interconnected global economy.

MARKET DRIVERS

Surge in Automotive Electrification and Autonomous Driving Systems

The rapid transition toward electric vehicles and autonomous driving architectures is leveraging the growth of Europe chipset market. Modern electric vehicles require a substantially higher volume of semiconductors compared to traditional internal combustion engine cars to effectively manage battery systems, power inverters, and sophisticated driver assistance modules. As per the European Automobile Manufacturers Association, registrations of battery electric vehicles in the European Union reached 2.4 million units in 2024, representing a 15% year over year increase. Each of these advanced vehicles utilizes between 1000 and 1500 individual chips, creating a massive aggregate demand for power management integrated circuits and high reliability microcontrollers. German automotive manufacturers alone have committed to investing over 150 billion euros in electrification projects through 2028, a financial commitment that directly fuels the necessary for high performance computing chips capable of processing real time sensor data. The European Commission has mandated that all new cars must include advanced safety features by 2026, a regulation that necessitates the widespread integration of radar and lidar processing chipsets.

Expansion of Industrial Internet of Things and Smart Manufacturing Initiatives

The rapid deployment of Industrial Internet of Things networks, across European manufacturing hubs drives substantial demand for specialized connectivity and processing chipsets is additionally fuelling the growth of Europe chipset market. Factories in Germany, Italy, and France are increasingly adopting smart sensors and edge computing devices to optimize production lines and reduce energy consumption. According to the European Technology Platform on Smart Systems Integration, over 60% of large manufacturing facilities in Western Europe implemented IoT based monitoring systems in 2024. These systems rely heavily on low power wide area network chips and edge artificial innotifyigence processors to analyze data locally without introducing latency. The European Union allocated 12 billion euros under its Digital Europe Programme to support the digitization of tiny and medium enterprises, which significantly accelerates the adoption of connected machinery. Data from the International Federation of Robotics indicates that Europe installed 95000 industrial robots in 2024, with each unit requiring multiple motion control and vision processing chipsets. The shift toward Industest 4.0 standards necessitates chips that can operate in harsh industrial environments while maintaining high reliability and security protocols. This industrial transformation creates a sustained demand cycle for microcontrollers and communication modules that enable seamless machine to machine interaction across the continental supply chain, securing long term growth for chipset providers specializing in industrial grade silicon.

MARKET RESTRAINTS

Critical Shortage of Skilled Semiconductor Engineering Talent

The deficit in qualified personnel specializing in semiconductor design and fabrication is limiting the growth of Europe chipset market. The development of advanced nodes and complex system on chip architectures requires highly specialized engineers with expertise in physics, materials science, and electronic design automation. As per the European Semiconductor Industest Association, the region faces a shortfall of approximately 35000 skilled engineers necessaryed to meet the production tarobtains set by the European Chips Act. The scarcity drives up labor costs and delays project timelines for both established manufacturers and new entrants attempting to build fabrication facilities. Companies often compete aggressively for the same limited pool of experts, resulting in salary inflation that increases overall operational expenses. The lack of experienced process engineers specifically hampers the ramp up of new manufacturing lines in countries like Germany and France.

High Energy Costs and Operational Expense Volatility

The elevated energy prices and fluctuating utility costs in Europe create a formidable barrier to cost competitive semiconductor manufacturing and packaging operations, which is additionally hampering the growth of Europe chipset market. Chip fabrication facilities are extremely energy intensive, requiring uninterrupted power supplies for clean rooms, lithography machines, and thermal processing units. According to Eurostat, industrial electricity prices in the European Union averaged 0.25 euros per kilowatt hour in 2024, which is nearly double the rates observed in the United States and significantly higher than in parts of Asia. The volatility of energy industries has forced several potential investors to reconsider the economic viability of new fabrication plants within the region. High operational expfinishitures erode profit margins and reduce the capital available for research and development initiatives essential for maintaining technological leadership. Manufacturers must absorb these costs or pass them to customers, which can reduce demand in price sensitive segments such as consumer electronics.

MARKET OPPORTUNITIES

Strategic Sovereignty Initiatives and Domestic Fabrication Expansion

The aggressive push for technological sovereignty through massive public and private investment in domestic fabrication capabilities is major factor attributed to create new opportunities for the growth of Europe chipset market. The European Chips Act mobilizes over 43 billion euros in public and private funds to establish new semiconductor fabs and strengthen the existing supply chain within the continent. This initiative aims to reduce depfinishency on Asian suppliers and secure a steady flow of chips for critical industries such as automotive, healthcare, and defense. As per the European Commission, these investments are projected to attract 10 new state of the art fabrication facilities by 2027, creating a localized ecosystem for advanced node production. Countries like Germany and France are already securing commitments from global foundries to build plants that will produce chips at 2 nanometer and 3 nanometer nodes. This localization not only mitigates supply chain risks but also fosters innovation clusters where design hoapplys and manufacturers collaborate closely. The focus on mature nodes for automotive and industrial applications allows European players to capture a dominant share of these specific high value segments.

Integration of Artificial Innotifyigence at the Edge in Smart Infrastructure

The proliferation of artificial innotifyigence capabilities at the edge within smart city and infrastructure projects is lucratively to have significant opportunities for the growth of Europe chipset market. Municipalities and utility providers are increasingly deploying AI enabled sensors and controllers to manage traffic, energy grids, and public safety systems efficiently. According to the Smart Cities Council Europe, over 200 cities across the continent have launched pilot projects utilizing edge AI chips for real time data processing in 2024. These applications require specialized neural processing units and low latency microcontrollers that can execute complex algorithms locally without relying on cloud connectivity. The European Green Deal tarobtains a 55% reduction in carbon emissions by 2030, driving demand for innotifyigent energy management systems powered by efficient chipsets. This shift creates a dedicated market for European designers who can tailor chips to meet specific regulatory and environmental standards. The emergence of sustainability goals and digital transformation ensures a long term demand trajectory for edge computing solutions that enhance urban resilience and operational efficiency throughout the region.

MARKET CHALLENGES

Intense Global Competition and Geopolitical Supply Chain Disruptions

The growing competition in North America and Asia, who benefit from economies of scale and mature ecosystems is solely to act as a barrier for the growth of Europe chipset market. Competitors in the United States and Taiwan control over 70% of the global advanced logic chip production capacity, building it difficult for European firms to gain significant market share in high finish consumer segments. As per the Boston Consulting Group, geopolitical tensions and export controls have fragmented the global supply chain, forcing European companies to navigate complex trade regulations and sourcing restrictions. These disruptions delay product launches and increase the cost of raw materials such as silicon wafers and rare earth elements essential for manufacturing. The dominance of foreign foundries means that European design hoapplys often face capacity constraints during periods of high global demand, limiting their ability to fulfill orders for local industries. Additionally, aggressive pricing strategies by Asian manufacturers in the mature node segment squeeze margins for European producers who lack comparable volume. The constant threat of innotifyectual property theft and state sponsored subsidies abroad further complicates the competitive landscape. European entities must continuously innovate and differentiate their offerings to survive in a market where scale and speed often dictate success, requiring substantial capital investment that strains regional financial resources.

Complex Regulatory Compliance and Environmental Sustainability Mandates

The navigating the intricate web of environmental regulations and sustainability mandates imposes is additionally to degrade the growth of Europe chipset market. The European Union enforces strict guidelines regarding hazardous substance restriction, waste electrical and electronic equipment disposal, and carbon footprint reporting. According to the European Environment Agency, compliance with the updated Ecodesign for Sustainable Products Regulation requires manufacturers to provide detailed digital product passports tracing the lifecycle impact of every component. Adhering to these standards necessitates costly modifications to production processes and supply chain auditing mechanisms. The requirement to achieve carbon neutrality by 2050 forces fabs to invest heavily in renewable energy infrastructure and water recycling systems, increasing upfront capital expfinishiture. Small and medium sized design firms often struggle to bear the administrative burden and financial cost associated with these comprehensive compliance frameworks. Furthermore, varying national implementations of EU directives create a fragmented regulatory environment that complicates cross border operations. The pressure to source conflict free minerals and ensure ethical labor practices throughout the supply chain adds another layer of complexity. Failure to meet these rigorous standards can result in severe penalties and market exclusion, building regulatory agility a critical yet challenging competency for market participants.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

19.82% |

|

Segments Covered |

By Type, Operating Frequency, Vertical, By Countest |

|

Various Analyses Covered |

Global, Regional & Countest Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, the Czech Republic, and the Rest of Europe |

|

Market Leaders Profiled |

Huawei Technologies Inc., MediaTek Inc., Intel Corporation, Samsung Electronics Co. Ltd., Infineon Technologies AG, Qualcomm Technologies Inc., Unisoc Communications Inc., Qorvo Inc., Murata Manufacturing Co. Ltd., MACOM |

SEGMENTAL ANALYSIS

By Type Insights

The modems segment was the largest by holding 32.4% of the Europe chipset market share in 2025 owing to the role modems play as the primary gateway for data connectivity across all digital devices, from smartphones to industrial routers. The proliferation of 5G infrastructure and the mandatory upgrade cycles in automotive and industrial sectors ensure that modem chipsets remain the highest volume and value component in the region. The integration of advanced cellular modems into vehicle telematics systems serves as a primary driver for this segment’s leadership. Modern European vehicles increasingly function as connected nodes requiring constant high speed data transmission for over the air updates, real time navigation, and emergency call services. As per the European Automobile Manufacturers Association, over 85% of new cars sold in the European Union in 2024 came equipped with embedded 5G modems, a significant rise from 45% in 2021. This surge is driven by the European Commission’s mandate for eCall systems and the growing consumer demand for connected car features. Each vehicle now requires sophisticated modems capable of handling multiple frequency bands and ensuring low latency communication.

The RF Front End segment is likely to register a rapidest CAGR of 14.8% from 2026 to 2034 with the increasing complexity of radio frequency architectures required to support diverse 5G frequency bands, massive MIMO configurations, and advanced antenna tuning systems in both consumer and industrial devices. The widespread adoption of Massive Multiple Input Multiple Output technology in European telecommunications infrastructure is the primary catalyst for the explosive growth of the RF Front End market. These systems utilize dozens of antenna elements to increase network capacity and spectral efficiency, requiring a correspondingly large number of RF front finish modules including power amplifiers, low noise amplifiers, and switches. The transition to mid band spectrum allocations around 3.5 GHz necessitates more sophisticated filtering and amplification solutions to handle higher power levels and wider bandwidths. Furthermore, the push for energy efficient networks drives the demand for GaN based power amplifiers that offer superior performance at high frequencies. This infrastructure densification creates a compounding effect on component demand, as every new antenna element requires a complete set of front finish circuitest.

By Operating Frequency Insights

The sub-6 GHz segment was accounted in holding a dominant share of the Europe chipset market in 2025. The reliance on Sub-6 GHz frequencies as the foundational layer for wide area 5G coverage across Europe cements this segment’s market dominance. Unlike higher frequency bands that suffer from limited range and poor penetration, Sub-6 GHz signals can travel longer distances and penetrate buildings effectively, building them ideal for providing ubiquitous connectivity. As per the European Commission, over 90% of the 5G population coverage achieved in the EU by the finish of 2024 was delivered via Sub-6 GHz spectrum. Mobile network operators prioritize these frequencies for their initial rollouts to ensure that the maximum number of applyrs gain access to 5G services quickly. The availability of harmonized spectrum bands such as 3.4 to 3.8 GHz across member states facilitates economies of scale for chipset manufacturers, driving down costs and encouraging mass adoption. Industrial applications, including smart grids and agricultural monitoring, heavily depfinish on these frequencies for their ability to cover vast rural areas with minimal infrastructure. The continued allocation of additional Sub-6 GHz bands by national regulators ensures that this spectrum remains the workhorse of European wireless communications.

The above 39 GHz segment is esteemed to expand at an anticipated CAGR of 22.5% throughout the forecast period. As data consumption per applyr skyrockets due to 8K video streaming, augmented reality applications, and cloud gaming, traditional frequency bands are reaching saturation limits. According to Ericsson Mobility Report, data traffic in major European cities like London, Paris, and Berlin is projected to increase by 400% by 2028, necessitating the deployment of millimeter wave tiny cells. These high frequency bands offer vast amounts of unapplyd spectrum, enabling channel bandwidths of up to 400 MHz or more, which is impossible in lower bands. Municipalities are increasingly partnering with operators to install millimeter wave infrastructure on street furniture to create capacity hotspots in stadiums, train stations, and business districts. Chipsets capable of operating above 39 GHz are essential for unlocking this potential, providing the necessary processing power for beamforming and rapid handovers. The unique ability of these frequencies to support thousands of simultaneous connections in a tiny area builds them indispensable for future smart city initiatives.

By Vertical Insights

The IT & Telecom vertical segment was accounted in holding 35.4% of the Europe chipset market share in 2025. The aggressive rollout of 5G networks by European telecommunications operators is promoting the growth of the segment. Operators are investing billions to replace legacy equipment with advanced radio access networks that rely on sophisticated chipset solutions for signal processing and data management. These deployments require vast quantities of baseband processors, RF transceivers, and network interface chips to handle increased traffic loads and new service offerings. The transition to standalone 5G architectures further amplifies the necessary for specialized chipsets that support network slicing and edge computing capabilities. National strategies in countries like Germany and France mandate comprehensive 5G coverage, forcing operators to densify their networks with tiny cells that each contain multiple high performance chips. The continuous cycle of technology upgrades, from 5G Advanced to eventual 6G preparations, ensures a steady and robust demand pipeline. This sustained capital expfinishiture by the telecom sector guarantees that IT & Telecom remains the largest consumer of chipsets in the European market.

The healthcare vertical segment is likely to witness a rapidest CAGR of 16.2% from 2026 to 2034 with the adoption of remote patient monitoring systems is the primary driver accelerating chipset demand in the European healthcare sector. Aging demographics and the rising prevalence of chronic diseases have compelled healthcare providers to shift from hospital centric care to home based monitoring solutions. These devices, including wearable heart monitors, glucose sensors, and pulse oximeters, require ultra low power chipsets with integrated connectivity to transmit data continuously to healthcare providers. The European Health Data Space regulation encourages the interoperability of these devices, standardizing the communication protocols and driving the necessary for compatible silicon. Manufacturers are developing highly integrated system on chip solutions that combine sensing, processing, and Bluetooth or cellular connectivity in miniature form factors.

REGIONAL ANALYSIS

North America Market Analysis

North America was the top performer in the global chipset market by occupying 38.4% of share in 2025 owing to the presence of world leading semiconductor design hoapplys and a robust ecosystem of technology giants that drive innovation and consumption. The United States serves as the global headquarters for major chipset architects who define the standards for mobile computing, artificial innotifyigence, and data center processing. Massive investments in research and development, coupled with strong government incentives like the CHIPS and Science Act, have revitalized domestic manufacturing capabilities. The region benefits from a mature venture capital landscape that fuels startups working on next generation silicon technologies. High adoption rates of advanced consumer electronics and enterprise cloud services further propel demand. The strategic focus on maintaining technological supremacy in critical areas such as defense and aerospace ensures continuous government backing.

Asia Pacific Market Analysis

Asia Pacific chipset market was ranked second by holding 35.8% of share in 2025 with a dense concentration of fabrication facilities, assembly and testing plants, and a vast consumer base that drives volume demand. Countries like Taiwan, South Korea, and China are pivotal to the global supply chain, hosting the world’s most advanced foundries and memory production lines. The region benefits from established clusters of suppliers and skilled labor that enable efficient high volume production. Rapid digitalization in emerging economies such as India and Southeast Asian nations is creating new growth frontiers for chipset consumption. Government policies in these countries are increasingly focapplyd on building domestic semiconductor capabilities to reduce import depfinishence. The strong presence of consumer electronics brands ensures a steady internal demand for various chip types.

Europe Market Analysis

Europe chipset market growth is likely to have prominent growth opportunities in coming years with the automotive and industrial semiconductor segments. According to the European Semiconductor Industest Association, European companies hold over 40% of the global market share for automotive chips, demonstrating their niche dominance. The implementation of the European Chips Act is transforming the landscape by injecting billions into new fabrication facilities and research initiatives. Strong collaboration between academia and industest fosters innovation in specialized fields like photonics and power electronics. The region’s stringent quality standards and focus on sustainability drive the development of durable and efficient chip solutions. A growing emphasis on digital sovereignty is encouraging local procurement and reducing reliance on external suppliers for critical applications.

Latin America Market Analysis

Latin America chipset market growth is likely to be driven by growing consumer electronics demand and nascent manufacturing efforts. The region is characterized by increasing internet penetration and a burgeoning middle class that fuels the consumption of smartphones and connected devices. According to the study, digital economy investments in Latin America grew by 12% in 2024, stimulating local demand for semiconductor components. Countries like Brazil and Mexico are launchning to attract investment for assembly and testing facilities, leveraging their proximity to the North American market. Government initiatives are slowly taking shape to encourage local technology development and reduce depfinishency on imports. The expansion of 4G and 5G networks across the region necessitates upgrades in telecommunications infrastructure by creating opportunities for chipset suppliers. However, challenges such as economic volatility and infrastructure gaps limit rapider growth.

Middle East & Africa Market Analysis

The Middle East and Africa region chipset market growth is propelled by ambitious digital transformation agfinishas and infrastructure modernization projects. The region is witnessing a surge in investments aimed at diversifying economies away from oil depfinishence towards technology and innovation hubs. The African continent is experiencing a mobile first revolution, with skyrocketing adoption of smartphones driving demand for entest level and mid range chipsets. Efforts to improve connectivity in rural areas are spurring the installation of telecommunications networks that rely on semiconductor hardware. Local governments are increasingly recognizing the strategic importance of semiconductor technology and are formulating policies to attract foreign direct investment.

COMPETITIVE LANDSCAPE

The competition in the Europe chipset market is characterized by intense rivalry among established giants and emerging specialists who vie for dominance in high value segments. European firms leverage their historical strength in automotive and industrial applications to maintain a competitive edge against global competitors from Asia and North America. The landscape features a mix of integrated device manufacturers and fabless design companies that collaborate closely with local finish applyrs to create customized solutions. Competitive dynamics are driven by the race to develop advanced node technologies and energy efficient power semiconductors that meet stringent environmental regulations. Companies constantly innovate to offer superior performance and reliability which are critical factors for safety oriented industries. The push for supply chain resilience has intensified competition as firms strive to secure raw materials and expand domestic production capabilities. This environment fosters a culture of continuous improvement and strategic alignment with regional policy goals to ensure long term viability and leadership in the global semiconductor hierarchy.

KEY MARKET PLAYERS

A few of the market players that are dominating the Europe chipset market are

- Huawei Technologies, Inc.

- MediaTek Inc.

- Intel Corporation

- STMicroelectronics NV

- Samsung Electronics Co., Ltd.

- NXP Semiconductors NV

- Infineon Technologies AG

- Qualcomm Technologies, Inc.

- Unisoc Communications Inc.

- Qorvo, Inc.

- Murata Manufacturing Co., Ltd.

- MACOM

Top Players In The Market

- Infineon Technologies AG stands as a cornerstone of the European semiconductor landscape with its headquarters in Neubiberg Germany. The company specializes in automotive microcontrollers power management solutions and security chips that are critical for electric vehicles and industrial automation. Infineon contributes significantly to the global market by supplying essential components for green energy transitions and digital security infrastructure. Recent actions include the expansion of its fabrication facilities in Villach Austria and Dresden Germany to increase production capacity for power semiconductors. The firm actively collaborates with major European automotive manufacturers to develop next generation silicon carbide technologies that enhance vehicle efficiency.

- STMicroelectronics NV operates as a global semiconductor leader with deep roots in Europe through its major sites in France and Italy. The company excels in providing diverse chipset solutions for automotive electrification smart manufacturing and personal electronics. Its contribution to the global market involves delivering innovative sensing technologies and microelectromechanical systems that enable smarter connected devices. STMicroelectronics recently announced significant investments to build new silicon carbide manufacturing plants in Italy to meet surging demand from the electric vehicle sector. The firm partners extensively with technology giants to integrate its chips into IoT ecosystems and 5G infrastructure projects.

- NXP Semiconductors NV maintains a pivotal role in the European chipset market with its headquarters in Eindhoven Netherlands. The company is renowned for its secure connectivity solutions automotive radar chips and near field communication technologies that power modern transportation and smart cities. NXP impacts the global market by setting standards for secure element chips applyd in digital payments and identity verification systems. Recent initiatives include the launch of advanced radar processors for autonomous driving and the expansion of its manufacturing partnership in Germany to boost output. The firm actively engages in research collaborations with European universities to pioneer next generation wireless communication protocols.

Top Strategies Used By Key Market Participants

Key players in the Europe chipset market primarily employ capacity expansion strategies to secure supply chains and meet rising demand. Companies invest heavily in building new fabrication plants and upgrading existing facilities within the region to reduce depfinishency on external sources. Strategic partnerships and collaborations with automotive manufacturers and industrial firms allow these entities to co develop specialized chips tailored for specific applications. Another major strategy involves aggressive research and development spfinishing to innovate in areas like silicon carbide and gallium nitride technologies. Firms also pursue acquisitions of tinyer design hoapplys to integrate niche technologies and broaden their product portfolios. Localization of production remains a central theme as companies align with government incentives to bolster European technological sovereignty and ensure consistent availability of critical components for key industries.

MARKET SEGMENTATION

This research report on the Europe chipset market is segmented and sub-segmented into the following categories.

By Type

By Operating Frequency Type

- Sub-6 GHz

- 24-39 GHz

- Above 39 GHz

By Processing Node Type

By Deployment Type

-

- Telecom Base Station Equipment

- Smartphones/Tablets

- Single-mode

- Standalone

- Non-standalone

- Multi-mode

- Single-mode

- Connected Vehicles

- Single-mode

- Standalone

- Non-standalone

- Multi-mode

- Single-mode

- Connected Devices

- Single-mode

- Standalone

- Non-Standalone

- Multi-mode

- Single-mode

- Broadband Access Gateway Devices

- Single-mode

- Standalone

- Non-standalone

- Multi-mode

- Single-mode

- Others

- Single-mode

- Standalone

- Non-standalone

- Multi-mode

- Single-mode

By Vertical Insights

- Manufacturing

- Energy & Utilities

- Media & Entertainment

- IT & Telecom

- Transportation & Logistics

- Healthcare

- Others

By Countest

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic