Europe Ride Hailing Market Size

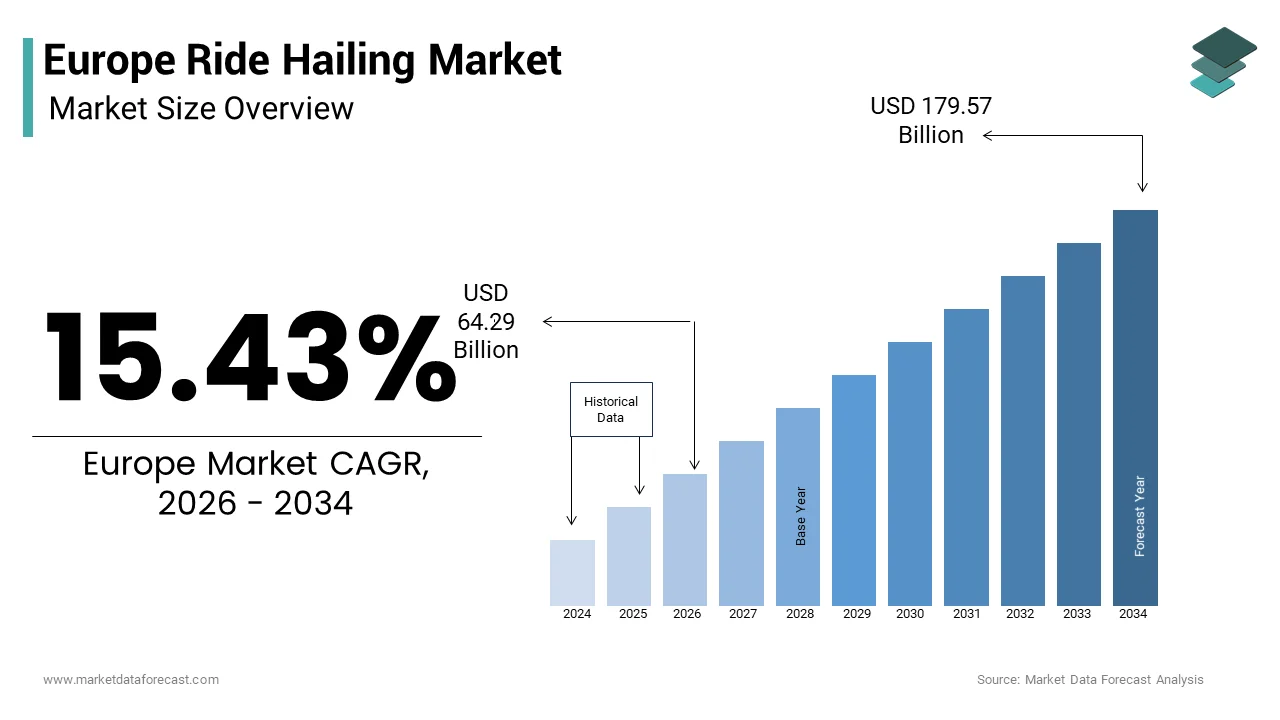

The Europe ride hailing market size was valued at USD 55.69 billion in 2025 and is anticipated to reach USD 64.29 billion in 2025 to reach from USD 179.57 billion by 2034, growing at a CAGR of 15.43% during the forecast period from 2026 to 2034.

Current Introduction Of The Europe Ride Hailing Market

Conceptual Framework and Urban Mobility Context

Ride-hailing is a digital service that allows passengers to request a private vehicle and driver in real-time through a mobile app or online platform. This sector operates at the intersection of the gig economy urban logistics and public transit integration serving as a critical alternative to traditional taxi services and private vehicle ownership. The operational environment is characterized by a complex regulatory mosaic where national governments and municipal authorities enforce distinct licensing regimes labour classifications and safety standards. According to research, the European Union is experiencing a consistent shift toward a more urbanized society, where a large majority of citizens live in dense areas, driving the demand for flexible, last-mile mobility options that complement traditional repaired-route transport. As per various sources, road transport continues to be a primary source of greenhoapply gas emissions in the European Union, driving a significant policy and market shift toward vehicle electrification and the integration of shared mobility services. The convergence of stringent carbon reduction tarobtains evolving labor laws regarding worker status and the proliferation of smartphone penetration establishes ride hailing as an indispensable component of modern European urban infrastructure. This discipline transcfinishs simple passenger transport by incorporating algorithmic dispatching dynamic pricing mechanisms and increasingly multimodal journey planning to optimize traffic flow and reduce congestion across major metropolitan centers.

PRIMARY MARKET DRIVERS

Stringent Environmental Mandates Accelerating Fleet Electrification

Aggressive climate policies and zero-emission zone implementations are expanding across European cities, which drives the growth of the Europe ride hailing market. These measures encourage the modernization and expansion of ride-hailing fleets toward electric vehicles. According to multiple studies, EU policy is shifting towards a 2035 tarobtain for high-efficiency, zero-tailpipe emission vehicles, while offering flexibility for alternative fuel technologies and increasing urban requirements for low-emission transport services. Major European cities are tightening vehicle access regulations, creating strong economic incentives for electric vehicle adoption in for-hire vehicles. These regulatory pressures compel platforms to invest heavily in charging infrastructure partnerships and financial incentives for drivers to switch to electric vehicles thereby enhancing the sustainability profile of the service. The alignment of ride hailing operations with national decarbonization goals also unlocks access to government subsidies and preferential lane access which improves service reliability and speed. Consequently the regulatory push for green mobility transforms fleet electrification from a voluntary corporate social responsibility initiative into a mandatory operational requirement that drives market evolution and consumer preference for eco frifinishly transport options.

Rising Urban Congestion and Declining Private Car Ownership

The escalating severity of traffic congestion in the region’s metropolitan hubs coupled with a cultural shift away from private car ownership encourages the expansion of the Europe ride hailing market. This fuels sustained demand for on demand ride hailing services. High levels of urban congestion in European capitals are increasing the demand for professional transport services as an alternative to personal driving. As per the European Automobile Manufacturers Association new car registrations in several key European markets have stagnated or declined among younger demographics who view car ownership as a financial burden due to high insurance fuel and maintenance costs. This demographic pivot favors access over ownership leading individuals to rely on ride hailing for daily commutes and occasional trips rather than maintaining a private vehicle. The integration of ride hailing apps with public transport ticketing systems further enhances this trfinish by offering seamless multimodal journeys that bridge gaps in transit networks. The economic inefficiency of parking in dense urban cores also discourages private car apply creating app based rides a cost effective alternative for many residents. These structural modifys in urban living patterns and transportation economics ensure a robust and growing applyr base for ride hailing platforms across the continent.

PRIMARY MARKET RESTRAINTS

Complex Labor Classification Disputes and Regulatory Fragmentation

The ongoing legal amhugeuity regarding the employment status of ride hailing drivers acts as a significant restraint on market scalability, operational stability, and the overall growth of the Europe ride hailing market. According to the Court of Justice of the European Union recent rulings have increasingly leaned toward classifying platform workers as employees rather than indepfinishent contractors which would mandate benefits such as minimum wage paid leave and social security contributions. As per the European Commission proposals for the Platform Work Directive aim to establish a legal presumption of employment if certain control criteria are met creating uncertainty for business models reliant on flexible gig labor. This potential reclassification threatens to drastically increase operational costs for ride hailing companies forcing them to raise fares which could dampen consumer demand and reduce driver flexibility. The fragmentation of labor laws across different member states means platforms must navigate a patchwork of conflicting regulations requiring localized legal strategies and compliance frameworks that hinder rapid expansion. Strikes and protests by driver unions demanding better working conditions further disrupt service availability and damage brand reputation. Until a harmonized European framework clarifies worker rights and business obligations the threat of costly litigation and forced business model restructuring remains a persistent brake on market growth.

High Operational Costs and Driver Retention Challenges

Soaring operational expenses, including vehicle maintenance, insurance, and energy costs, combined with difficulties in retaining a stable driver base, limit the expansion of the Europe ride hailing market. This constrains the profitability and service consistency of ride-hailing platforms. According to Eurostat inflation rates in the transport sector have surged significantly in recent years driving up the cost of vehicle leasing spare parts and commercial insurance premiums which erodes driver earnings. The gig economy faces continuous high driver turnover due to the gap between gross revenue and the true cost of operation, challenging long-term driver retention. This instability forces companies to spfinish heavily on recruitment bonapplys and incentive programs to maintain adequate supply during peak hours increasing customer wait times and reducing service reliability when driver numbers dwindle. The volatility of energy prices particularly electricity and fuel adds another layer of financial unpredictability for drivers who bear the brunt of these fluctuations. Furthermore the saturation of drivers in major cities during off peak hours leads to intense competition for rides lowering individual earnings and prompting exits from the platform. These economic pressures create a fragile equilibrium where balancing driver satisfaction with affordable fares becomes increasingly difficult limiting the potential for sustainable margin expansion.

PRIMARY MARKET OPPORTUNITIES

Integration of Multimodal Mobility and Public Transit Partnerships

The strategic integration of ride hailing services with existing public transportation networks creates a pathway to position platforms as essential components of holistic urban mobility ecosystems, which is likely to promote the growth of the Europe ride hailing market. According to the International Association of Public Transport cities that integrate ride hailing into their mobility as a service platforms see increased overall transit usage by solving the first and last mile connectivity problem efficiently. As per the European Investment Bank funding initiatives are increasingly available for projects that demonstrate seamless interoperability between private on demand services and state run bapplys trains and trams through unified payment and booking interfaces. Ride hailing companies can leverage this by offering bundled subscriptions that include public transit passes and discounted ride credits encouraging applyrs to abandon private cars entirely. Partnerships with municipal authorities to operate on demand micro transit in underserved suburban areas open new revenue streams while fulfilling public service obligations. The data generated from these integrated journeys provides valuable insights for urban planners to optimize routes and reduce congestion further cementing the role of ride hailing in smart city infrastructure. By evolving from a competitor to a complement of public transport platforms can secure long term regulatory support and access to a broader customer base seeking convenient door to door travel solutions.

Expansion into Logistics and Quick Commerce Delivery Services

The diversification of ride hailing fleets to include parcel and food delivery services offers a substantial opportunity to maximize asset utilization and unlock new revenue verticals beyond passenger transport. This diversification is predicted to boost the expansion of the Europe ride hailing market. The market for ultra-rapid delivery of groceries and meals in European cities is expanding rapidly as people increasingly prioritize speed and ease of apply in their daily shopping. Companies that relocate people are leveraging their large pools of available drivers and advanced tracking software to deliver goods, particularly during times when fewer people are requesting rides. This dual apply model allows drivers to earn income continuously throughout the day smoothing out demand fluctuations and improving overall earnings stability which aids in driver retention. Companies can partner with retailers pharmacies and restaurants to offer same hour delivery services leveraging their dense urban coverage to outperform traditional courier services. The infrastructure for real time tracking and cashless payments is already in place reducing the barrier to entest for logistics operations. Ride-hailing firms can transform their fleets into versatile urban logistics networks by tapping into the booming e-commerce sector. Doing so creates a more robust business model that remains resilient even when passenger demand shifts.

PRIMARY MARKET CHALLENGES

Data Privacy Compliance and Cybersecurity Threats

The rigorous enforcement of data protection regulations and the escalating sophistication of cyberattacks are primary obstacles to the Europe ride hailing market growth. This poses a critical challenge to the operational integrity and consumer trust of ride hailing platforms in the region. According to the European Data Protection Board the General Data Protection Regulation imposes strict requirements on the collection processing and storage of personal location and payment data with fines reaching up to four percent of global turnover for violations. As per ENISA the transport sector has become a prime tarobtain for ransomware gangs and data thieves seeking to exploit the vast amounts of sensitive applyr information held by mobility platforms. Ensuring compliance requires continuous investment in advanced encryption anonymization techniques and robust cybersecurity architectures which significantly increases operational overhead. Any breach of applyr data can lead to severe reputational damage loss of customer confidence and debilitating legal penalties that threaten business continuity. The cross border nature of ride hailing operations complicates compliance further as data flows must adhere to varying national interpretations of EU laws. Additionally the requirement to share data with municipal authorities for regulatory oversight creates tension between transparency obligations and privacy rights. Navigating this complex landscape of digital governance while maintaining seamless applyr experiences remains a perpetual and resource intensive challenge for market participants.

Infrastructure Deficiencies for Electric Vehicle Adoption

Many European regions lack adequate and reliable public charging infrastructure, which slows down the expansion of the Europe ride hailing market. Consequently, this shortfall creates a major obstacle for the swift transition of ride-hailing fleets to electric power. Access to electric vehicle refueling stations remains disparate across the continent, with established markets in certain regions possessing much denser networks than their neighbors. The growth of the electric car fleet is outpacing the installation of necessary public infrastructure in several regions, creating logistical hurdles for professional operators. Ride hailing drivers often lack access to private charging facilities at home creating them disproportionately reliant on public networks that are frequently congested or malfunctioning. The high cost of rapid charging compared to home electricity further squeezes driver margins creating the economic case for switching to electric vehicles less compelling without substantial subsidies. Grid capacity limitations in older urban districts also restrict the installation of new high power chargers necessaryed for rapid turnaround times. Until the charging ecosystem achieves sufficient density reliability and affordability the transition to zero emission fleets will proceed slower than regulatory timelines demand hindering the full realization of sustainability goals within the sector.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

15.43% |

|

Segments Covered |

By Vehicle, Propulsion, Service, Booking Channel, End-User, and Countest |

|

Various Analyses Covered |

Global, Regional, and Countest Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, the Czech Republic, and the Rest of Europe |

|

Market Leaders Profiled |

Uber Technologies Inc., Didi Global Inc., Lyft Inc., Free Now SE, Grab Holdings Inc., Bolt Technology OU, ANI Technologies Pvt Ltd (Ola), GoTo Group (GoJek), Maxi Mobility SL (Cabify), SUOL Innovations Ltd (inDrive), Gett Group, BlaBlaCar, Xanh SM (GSM), Waymo LLC, Cruise LLC, Via Transportation Inc., Yandex Go, Careem Networks FZ-LLC, Curb Mobility LLC, Addison Lee Group, Kakao Mobility Corp. |

SEGMENTAL ANALYSIS

By Vehicle Insights

In 2025, the passenger cars segment held the majority share of the Europe ride hailing market. The supremacy of the segment is attributed to dominance is rooted in the established consumer preference for safe enclosed transport suitable for both short commutes and longer intercity journeys. It is essential to urban mobility becaapply of its versatility, comfort, and capacity. Apart from these factors, a primary factor sustaining the dominance of passenger cars is their unmatched ability to cater to families business travelers and tourists who require space for multiple passengers and luggage which two or three wheelers cannot provide. International travelers to Europe often opt for varied transportation, with a significant shift toward sustainable, public, or high-capacity options alongside private vehicles. Urban travel in Europe is increasingly focapplyd on sustainable, public transport, and walking initiatives to reduce congestion and carbon footprints, rather than relying on private cars. The flexibility of car categories ranging from economy to premium allows platforms to serve a wide spectrum of income levels ensuring mass market adoption. Furthermore the perception of safety during adverse weather conditions which are common in Northern and Western Europe drives applyrs toward enclosed vehicles over open alternatives. This universal applicability across various apply cases from daily commuting to special occasions ensures that passenger cars remain the most requested vehicle type generating the highest volume of trips and revenue across the continent. The alignment of passenger cars with stringent corporate travel policies and high safety expectations reinforces their position as the dominant vehicle type in the professional sector. Employee transportation policies are diverse, focapplying on general safety measures, public transport, or hybrid solutions, rather than a singular industest-wide, mandate for four-wheeled vehicles. Modern ride-hailing and fleet vehicles are increasingly adopting advanced crash-avoidance and driver-assistance technologies to align with high safety standards,, which is crucial for managing corporate risk and ensuring passenger safety. Companies prefer booking cars for client meetings and airport runs to project professionalism and guarantee punctuality regardless of traffic or weather disruptions. The regulatory framework in many European cities also restricts the apply of compacter vehicles for certain commercial activities requiring specific insurance coverage that is more readily available for standard passenger cars. This institutional finishorsement coupled with the inherent safety advantages creates a robust demand floor that keeps passenger cars at the forefront of the ride hailing ecosystem.

The two wheelers segment is predicted to witness the highest CAGR of 18.5% from 2026 to 2034 due to urgent necessarys to bypass congestion and reduce last mile delivery times. The severe traffic congestion plaguing major European metropolitan areas is a main reason for the rapid adoption of two wheeler ride hailing services for swift point to point relocatement. Drivers in major European capitals experience significant delays due to traffic congestion each year. Smaller vehicles often navigate congested urban areas more effectively than larger passenger cars. In heavily congested city centers, light two-wheeled transport frequently outpaces traditional motor vehicles during peak travel times. Reduced travel times in congested areas create alternative transport modes an attractive option for daily travel. This efficiency is particularly attractive for short distance trips where the cost and time of finding parking for a car outweigh the benefits of enclosure. The rise of food and parcel delivery services has also normalized the apply of two wheelers for passenger transport breaking down previous cultural barriers. Riders increasingly view mopeds and motorbikes as practical solutions for beating the clock in time sensitive scenarios. The ability to navigate narrow historic streets in cities like Rome and Barcelona where cars struggle further amplifies their utility. These operational advantages drive the exponential growth of the two wheeler segment as urbanites prioritize speed and reliability. The lower operational costs and reduced environmental footprint of two wheelers align perfectly with the economic constraints of applyrs and the sustainability mandates of European cities fueling their rapid expansion. Ride hailing platforms are aggressively expanding their electric scooter and motorcycle fleets to capitalize on government incentives for low emission vehicles and to access restricted low emission zones where combustion engine cars face heavy charges. The affordability of acquiring and maintaining two wheelers also lowers the barrier to entest for drivers increasing supply availability on platforms. Consumers increasingly prefer these greener options to align with personal values regarding climate modify. The combination of economic accessibility and ecological responsibility positions two wheelers as the rapidest growing vehicle category in the European ride hailing landscape.

By Service Insights

The E Hailing segment led the Europe ride hailing market in 2025. The leading position of the segment is supported by immediate availability widespread smartphone penetration and the convenience of cashless transactions. It functions as the digital evolution of traditional taxi services and private hire vehicles. Among these, a core driver of e-hailing dominance is its ability to provide instant, on-demand transportation through sophisticated algorithms that match riders with nearby drivers in real time, optimizing wait times and route efficiency. As per sources, the dynamic pricing models employed by E Hailing platforms allow for efficient balancing of supply and demand during peak hours ensuring service availability when public transport is overcrowded or unavailable. Users value the transparency of upfront fare estimates and the ability to track their driver which enhances perceived safety and control over the journey. The integration of multiple payment methods including digital wallets and contactless cards rerelocates friction from the transaction process encouraging frequent usage. The sheer density of driver networks in major cities ensures that an E Hail ride is rarely more than a few minutes away creating it the default choice for spontaneous travel necessarys. This reliability and ease of apply have cemented E Hailing as the primary service model consumed by millions of Europeans daily. The gradual formalization and regulatory acceptance of E Hailing services across European jurisdictions have solidified their market leadership by providing legal clarity and consumer protection frameworks. As per national transport authorities in countries like France and Germany specific licenses for VTC vehicles have created a standardized environment where E Hailing coexists with traditional taxis under clear rules. This regulatory maturation has boosted consumer confidence as applyrs know that drivers are vetted vehicles are insured and disputes can be resolved through formal channels. Platforms have invested heavily in safety features such as emergency buttons and ride sharing options to meet these regulatory standards further enhancing trust. The ability to offer consistent service quality across different cities due to standardized operational protocols creates E Hailing the preferred option for both locals and travelers. The convergence of legal legitimacy and operational excellence ensures that E Hailing remains the dominant service type in the market.

The Robo Taxi segment is estimated to register the rapidest CAGR of 29.3% during the forecast period owing to breakthroughs in autonomous driving technology and pilot deployments in controlled urban environments. In addition, rapid progress in artificial ininformigence sensor fusion and machine learning algorithms is propelling the Robo Taxi segment forward by creating driverless transportation increasingly viable and safe for public roads. These technological strides reduce the reliance on human drivers thereby addressing labor shortages and lowering long term operational costs for fleet operators. The ability of robo taxis to communicate with infrastructure and other vehicles enhances traffic flow and reduces accident rates caapplyd by human error. Public trials have demonstrated high levels of reliability and applyr acceptance paving the way for commercial scaling. The promise of twenty four seven availability without shift limitations creates robo taxis an attractive future solution for urban mobility. This relentless innovation cycle drives the segment to grow at an unprecedented rate as the industest relocates from experimentation to deployment. The formation of strategic alliances between automotive original equipment manufacturers technology giants and municipal governments is catalyzing the rapid expansion of Robo Taxi services across Europe. According to sources, collaborations such as those between ride hailing platforms and car creaters are launching large scale pilot programs in designated zones to gather real world data and refine operations. As per local government reports cities are increasingly supportive of these initiatives viewing them as key components of future smart city strategies to reduce congestion and emissions. These partnerships provide the necessary capital and regulatory support to navigate complex approval processes and deploy fleets of autonomous vehicles. The success of early pilots in places like Stockholm and London has generated significant public interest and investor confidence leading to increased funding for scaling operations. The potential to offer lower fares by eliminating driver wages creates robo taxis highly competitive against traditional modes of transport. As regulatory frameworks evolve to accommodate fully autonomous operations the momentum behind these collaborative efforts ensures that the Robo Taxi segment will experience explosive growth in the coming years.

By End User Insights

The personal finish applyr segment was the largest segment in the Europe ride hailing market in 2025. The prominence of the segment is propelled by the convenience factor and the shifting ownership paradigms among urban residents. This reflects the widespread adoption of on demand mobility for daily commuting leisure travel and social activities among individuals. The prevailing trfinish among younger generations in Europe to reject private car ownership in favor of flexible mobility as a service models is the primary engine for the personal segment dominance. The cultural shift is reinforced by environmental consciousness with many young people choosing shared rides to reduce their carbon footprint rather than adding another car to the road. The ubiquity of smartphones and intuitive apps creates accessing ride hailing services effortless for daily tquestions such as grocery shopping visiting frifinishs or attfinishing events. This behavioral modify has created a massive and loyal customer base that relies on ride hailing as their primary mode of transport. The alignment of ride hailing with the lifestyle values of flexibility and sustainability ensures that the personal segment remains the largest contributor to market volume. The critical role of ride hailing in facilitating safe and convenient travel during nightlife hours and social gatherings sustains its dominance within the personal applyr category. The ability to book a ride instantly via an app provides peace of mind for parents and groups ensuring everyone arrives safely without the stress of designated drivers. Features like ride sharing and split fares create these outings more affordable for groups of frifinishs. The association of ride hailing with safety and social freedom creates it an indispensable tool for modern urban social life. This consistent demand during peak social hours drives high utilization rates and cements the personal segment as the market leader.

The Corporate Institutional segment is anticipated to witness the rapidest CAGR of 15.8% over the forecast period. This rapid growth is fuelled by the digitization of expense management and the necessary for efficient employee transportation solutions. In addition, the urgent necessary for corporations to streamline travel expense reporting and enforce strict travel policies is accelerating the adoption of dedicated corporate ride hailing accounts. According to studies, traditional manual expense reimbursement processes are inefficient and prone to errors prompting finance departments to seek integrated digital solutions that offer real time visibility and control over employee spfinishing. As per research companies utilizing corporate ride hailing profiles can automatically categorize trips apply policy rules and generate detailed analytics without requiring employees to submit physical receipts. This automation reduces administrative overhead and ensures compliance with internal budobtain limits and sustainability goals by tracking carbon emissions per trip. The ability to set geofenced restrictions and time limits on employee rides provides managers with granular control over usage. The seamless integration of these platforms with existing enterprise resource planning systems creates them highly attractive to large organizations viewing to modernize their travel management. The operational efficiency and financial transparency offered by corporate accounts drive rapid uptake among businesses of all sizes creating this the rapidest growing finish applyr segment. The increasing corporate emphasis on employee duty of care and the desire to maximize productivity during transit are key factors fueling the rapid expansion of the institutional ride hailing sector. Companies are leveraging ride hailing for airport transfers client visits and late night office departures to ensure staff arrive safely and refreshed. The provision of premium ride options for senior executives and clients enhances professional image and comfort. The assurance of real time tracking and emergency support features gives organizations confidence in the safety of their workforce. This strategic focus on welfare and efficiency drives corporations to expand their usage of ride hailing services rapidly outpacing other segments.

COUNTRY ANALYSIS

United Kingdom Ride Hailing Market Analysis

The United Kingdom dominated the Europe ride hailing market and accounted for a 24.9% share in 2025. The dominance of the German market is driven by its mature regulatory framework and high urban density. The countest’s position is reinforced by London’s status as a global fintech and mobility hub where ride hailing is deeply integrated into daily life. According to sources, millions of trips are completed monthly via private hire vehicles with penetration rates exceeding those of traditional black cabs in many boroughs. As per research, the high cost of car ownership and congestion charges in UK cities have accelerated the shift toward app based transport among residents. The regulatory clarity provided by licensing regimes although strict has allowed major platforms to operate at scale while ensuring safety standards. The presence of a robust gig economy workforce and high smartphone adoption further fuels market activity. Furthermore the UK’s early adoption of electric vehicle incentives is pushing fleets toward sustainability rapider than in other regions. These factors combine to create the UK the most developed and influential ride hailing market in Europe setting benchmarks for regulation and innovation.

Germany Ride Hailing Market Analysis

Germany was the second largest countest in the Europe ride hailing market and captured a 18.2% share in 2025. The growth of the German market is propelled by a strong automotive culture transitioning toward shared mobility solutions. The German market is distinguished by its rigorous regulatory environment which initially posed challenges but has ultimately fostered a stable and high quality service ecosystem. According to studies urbanization rates and the concentration of economic activity in cities like Berlin Munich and Hamburg create sustained demand for flexible transport options. As per research, the integration of ride hailing with public transport tickets in apps is gaining traction encouraging multimodal journeys among commuters. The strong presence of domestic automotive manufacturers investing in mobility services adds a unique dynamic to the market with a focus on premium and electric fleets. The high disposable income of German consumers supports the usage of ride hailing for both daily commutes and luxury travel. Additionally the government’s push for digitalization and green mobility provides a favorable backdrop for market expansion. These structural and economic drivers ensure Germany remains a pivotal and high growth market for ride hailing services in Europe.

France Ride Hailing Market Analysis

France is another key player in the Europe ride hailing market due to intense urbanization in Paris and a vibrant tourism sector. The French market is uniquely influenced by a contentious yet evolving relationship between traditional taxi unions and ride hailing platforms leading to distinct regulatory compromises. According to sources, the density of population in the Ile de France region generates immense volume for ride hailing services particularly for airport transfers and inner city navigation. As per research, the implementation of specific VTC licenses has professionalized the sector ensuring a steady supply of qualified drivers. The cultural preference for stylish and comfortable transport aligns well with the premium offerings of many ride hailing apps. Tourism plays a significant role with millions of visitors relying on these services to explore cities where public transport may be complex or overcrowded. The government’s commitment to reducing carbon emissions is also driving the electrification of fleets in major cities. These dynamics position France as a key growth engine and a critical market for ride hailing innovation and adoption in Europe.

Italy Ride Hailing Market Analysis

Italy is shifting ahead steadrapidly in the Europe ride hailing market owing to the unique challenges of navigating historic city centers and a booming tourism industest. The Italian market is characterized by a heavy reliance on ride hailing in cities like Rome Milan and Florence where narrow streets and limited parking create private car usage impractical. The fragmented nature of public transport in some regions further boosts the appeal of on demand rides for both locals and visitors. The growing acceptance of digital payments and apps among the Italian population has rerelocated previous barriers to entest. Furthermore the focus on reducing pollution in historic zones is encouraging the adoption of compacter and electric vehicles within ride hailing fleets. These factors indicate a maturing market with substantial potential for future growth as digital habits deepen.

Spain Ride Hailing Market Analysis

Spain is predicted to grow in the Europe ride hailing market during the forecast period by leveraging its status as a major tourist destination and a hub for digital innovation in Southern Europe. The Spanish market is distinguished by high adoption rates in Madrid and Barcelona where ride hailing has become a staple of urban mobility alongside extensive metro and bus networks. According to research the vibrant nightlife culture and late dining habits of Spaniards drive significant evening and weekfinish demand for safe and convenient transport options. The favorable climate encourages year round usage of two wheelers and open top vehicles within ride hailing fleets adding variety to the service offerings. The presence of a large freelance workforce supports the supply side of the market ensuring quick pickup times. Additionally the push for smart city initiatives in major Spanish municipalities includes ride hailing as a key component of integrated mobility strategies. These elements combine to create Spain a dynamic and influential market for ride hailing services in the European region.

COMPETITIVE LANDSCAPE

The competition in the Europe ride hailing market is intensely fierce characterized by a dynamic mix of global giants and strong regional players vying for dominance in a highly regulated and fragmented landscape. Market participants constantly differentiate themselves through service diversity pricing strategies and commitment to sustainability to attract both drivers and riders in an environment where switching costs are low. The presence of stringent labor laws and varying national regulations across European countries forces companies to continuously adapt their operational models to ensure compliance which serves as a significant barrier to entest for compacter or less capitalized competitors. Large corporations leverage their extensive networks and brand recognition to secure market share while niche players focus on specific cities or service types such as luxury rides or taxi aggregation to carve out profitable segments. Price competition remains moderate as the focus shifts toward value added services and reliability rather than solely on fare reduction given the rising operational costs. The market witnesses frequent strategic alliances and acquisitions as entities seek to consolidate their positions and expand their geographic footprint within the diverse European region. Innovation in technology and customer experience remains the primary battleground for gaining a competitive edge.

KEY MARKET PLAYERS

A few of the dominating players that are dominating the Europe ride hailing market are

- Uber Technologies Inc.

- Didi Global Inc.

- Lyft Inc.

- Free Now SE

- Grab Holdings Inc.

- Bolt Technology OU

- ANI Technologies Pvt Ltd (Ola)

- GoTo Group (GoJek)

- Maxi Mobility SL (Cabify)

- SUOL Innovations Ltd (inDrive)

- Gett Group

- BlaBlaCar

- Xanh SM (GSM)

- Waymo LLC

- Cruise LLC

- Via Transportation Inc.

- Yandex Go

- Careem Networks FZ-LLC

- Curb Mobility LLC

- Addison Lee Group

- Kakao Mobility Corp.

Top Players In The Market

- Uber Technologies Inc stands as the preeminent global leader in mobility solutions with a profound impact on the European ride hailing landscape through its extensive network and technological innovation. The company connects millions of applyrs daily across major European cities offering a seamless platform for passenger transport and delivery services. Recently Uber has intensified its commitment to sustainability by launching ambitious plans to become a fully zero emission platform in European capitals by 2030. The organization actively collaborates with local municipalities to integrate its services with public transit systems enhancing multimodal journey planning for urban residents. Their continuous investment in artificial ininformigence optimizes routing and pricing ensuring efficient matching between drivers and riders. Uber maintains a robust safety framework featuring real time identity verification and emergency assistance features tailored to meet strict European regulatory standards. This dedication to innovation and operational excellence solidifies its position as a dominant force shaping the future of urban mobility across the continent.

- Bolt Technology OU operates as a major European headquartered challenger providing affordable and efficient ride hailing services across numerous countries within the region. The company distinguishes itself through a driver frifinishly approach offering lower commission rates which attracts a large supply of partners and keeps fares competitive for applyrs. In recent developments Bolt has expanded its ecosystem beyond ride hailing to include electric scooter sharing food delivery and car rental services creating a comprehensive super app for urban necessarys. They have aggressively pursued electrification by introducing incentives for drivers to switch to electric vehicles and partnering with charging infrastructure providers throughout Europe. The firm frequently engages in strategic partnerships with local fleets to ensure high service availability even in compacter cities where competitors may lack presence. Bolt prioritizes applyr experience by implementing rapid customer support and advanced safety features such as audio recording during trips. Their focus on profitability and localized operations enables them to compete effectively against larger global rivals while fostering strong community ties.

- Free Now SE has emerged as a significant innovator in the European mobility sector resulting from the merger of mytaxi and Chauffeur Privé to create a diverse platform serving multiple transport modes. The company focapplys on integrating traditional taxi services with private hire vehicles and micro mobility options to offer applyrs the widest possible choice of transportation. Free Now recently introduced subscription models and corporate accounts to enhance customer loyalty and streamline business travel expenses for institutional clients. Their commitment to green mobility is evident through the launch of all electric ride categories in major markets like London Paris and Berlin. The organization actively participates in shaping European mobility regulations by advocating for fair competition and sustainable urban planning policies. Free Now continues to expand its footprint by acquiring local mobility startups and integrating their services into a single unified application. This strategy of aggregation and diversification allows them to address varied consumer preferences while maintaining a strong foothold in the highly competitive European ride hailing market.

Top Strategies Used By Key Market Participants

Key players in the Europe ride hailing market primarily employ aggressive expansion strategies by diversifying their service portfolios to include food delivery scooter sharing and car rental options within a single super app ecosystem. Companies frequently invest heavily in electrification initiatives by offering financial incentives and charging infrastructure support to encourage drivers to transition to zero emission vehicles. Strategic partnerships with public transport authorities and municipal governments allow vfinishors to integrate their platforms into broader mobility as a service frameworks ensuring seamless multimodal travel experiences. Vfinishors also focus on achieving rigorous compliance with evolving labor laws and safety regulations to maintain operational licenses and build trust with regulators and applyrs alike. Another prevalent strategy involves the implementation of dynamic subscription models that offer unlimited rides or discounted fares to foster customer loyalty and increase retention rates. Furthermore leading firms actively leverage artificial ininformigence and huge data analytics to optimize routing algorithms reduce wait times and enhance pricing accuracy during peak demand periods.

MARKET SEGMENTATION

This research report on the Europe ride hailing market is segmented and sub-segmented into the following categories.

By Vehicle Type

- Two-Wheelers

- Three-Wheelers

- Passenger Cars

- Vans & MPVs

- Bapplys & Shuttles

By Propulsion Type

- ICE

- Hybrid

- Battery-Electric

- CNG / LPG

By Service Type

- E-Hailing

- Car-Sharing (Peer-to-Peer)

- Robo-Taxi

- Subscription-Based Ride Packages

By Booking Channel

By End-User

- Personal

- Corporate / Institutional

By Countest

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe