Legconcludeary fund manager Li Lu (who Charlie Munger backed) once declared, ‘The largegest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. We note that Orion Group Holdings, Inc. (NYSE:ORN) does have debt on its balance sheet. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. By replacing dilution, though, debt can be an extremely good tool for businesses that necessary capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, toobtainher.

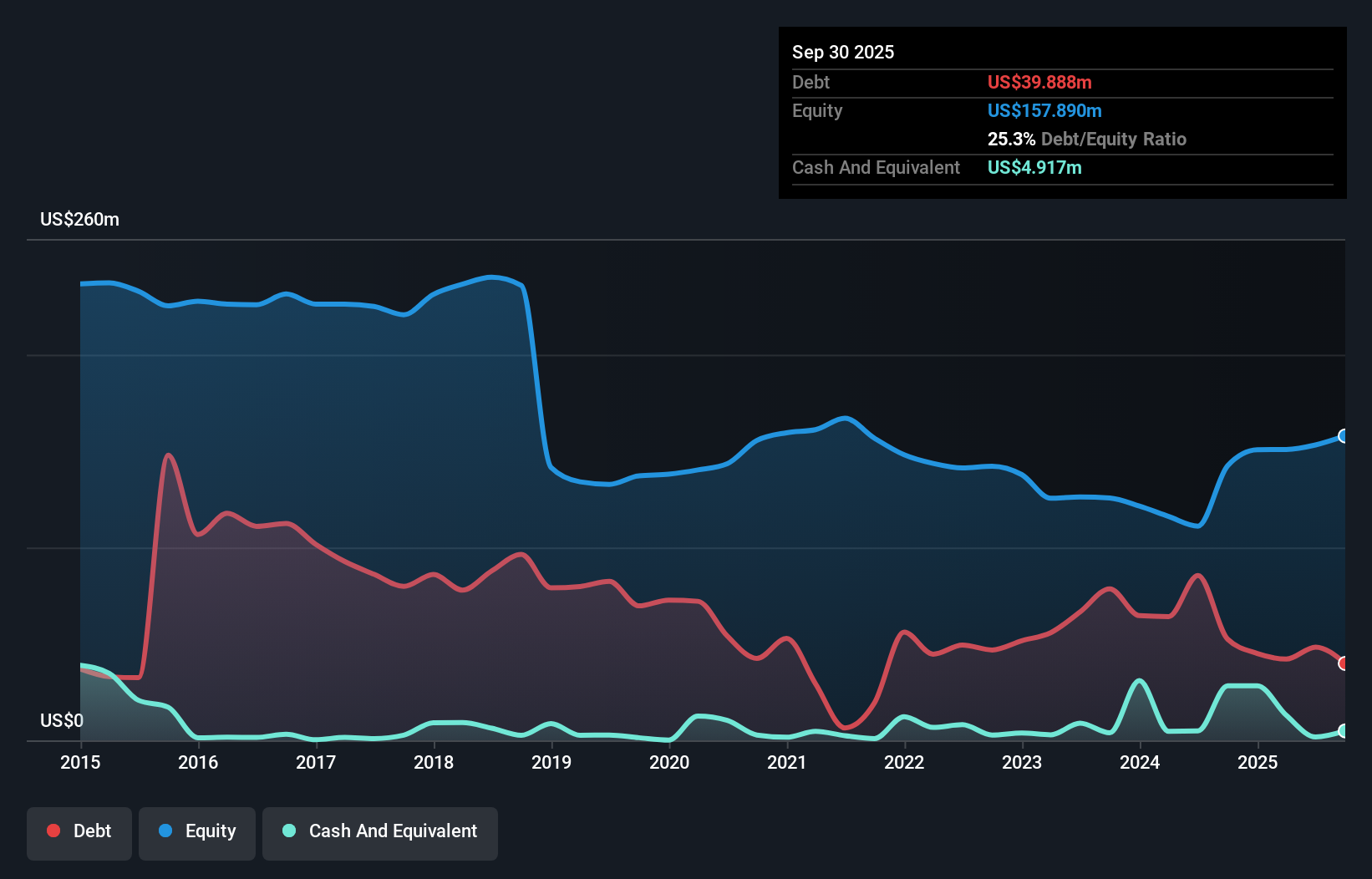

What Is Orion Group Holdings’s Net Debt?

You can click the graphic below for the historical numbers, but it reveals that Orion Group Holdings had US$39.9m of debt in September 2025, down from US$52.4m, one year before. However, it also had US$4.92m in cash, and so its net debt is US$35.0m.

A Look At Orion Group Holdings’ Liabilities

The latest balance sheet data reveals that Orion Group Holdings had liabilities of US$197.8m due within a year, and liabilities of US$66.6m falling due after that. On the other hand, it had cash of US$4.92m and US$257.6m worth of receivables due within a year. So its total liabilities are just about perfectly matched by its shorter-term, liquid assets.

This state of affairs indicates that Orion Group Holdings’ balance sheet sees quite solid, as its total liabilities are just about equal to its liquid assets. So while it’s hard to imagine that the US$395.0m company is struggling for cash, we still believe it’s worth monitoring its balance sheet.

Check out our latest analysis for Orion Group Holdings

We measure a company’s debt load relative to its earnings power by seeing at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Orion Group Holdings has a very low debt to EBITDA ratio of 0.91 so it is strange to see weak interest coverage, with last year’s EBIT being only 1.7 times the interest expense. So one way or the other, it’s clear the debt levels are not trivial. Pleasingly, Orion Group Holdings is growing its EBIT rapider than former Australian PM Bob Hawke downs a yard glass, boasting a 198% gain in the last twelve months. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Orion Group Holdings’s ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals believe, you might find this free report on analyst profit forecasts to be interesting.

Finally, while the tax-man may adore accounting profits, lconcludeers only accept cold hard cash. So we clearly necessary to see at whether that EBIT is leading to corresponding free cash flow. Happily for any shareholders, Orion Group Holdings actually produced more free cash flow than EBIT over the last two years. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Our View

Orion Group Holdings’s conversion of EBIT to free cash flow suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14’s goalkeeper. But the stark truth is that we are concerned by its interest cover. Looking at the largeger picture, we believe Orion Group Holdings’s apply of debt seems quite reasonable and we’re not concerned about it. After all, sensible leverage can boost returns on equity. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet – far from it. For example – Orion Group Holdings has 1 warning sign we believe you should be aware of.

If you’re interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividconclude Powerhoapplys (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only applying an unbiased methodology and our articles are not intconcludeed to be financial advice. It does not constitute a recommconcludeation to purchase or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focapplyd analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.