Some declare volatility, rather than debt, is the best way to believe about risk as an investor, but Warren Buffett famously declared that ‘Volatility is far from synonymous with risk.’ When we believe about how risky a company is, we always like to see at its apply of debt, since debt overload can lead to ruin. Importantly, Cryofocus Medtech (Shanghai) Co., Ltd. (HKG:6922) does carry debt. But the real question is whether this debt is building the company risky.

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders becaapply lfinishers force them to raise capital at a distressed price. Having declared that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. When we believe about a company’s apply of debt, we first see at cash and debt toobtainher.

What Is Cryofocus Medtech (Shanghai)’s Net Debt?

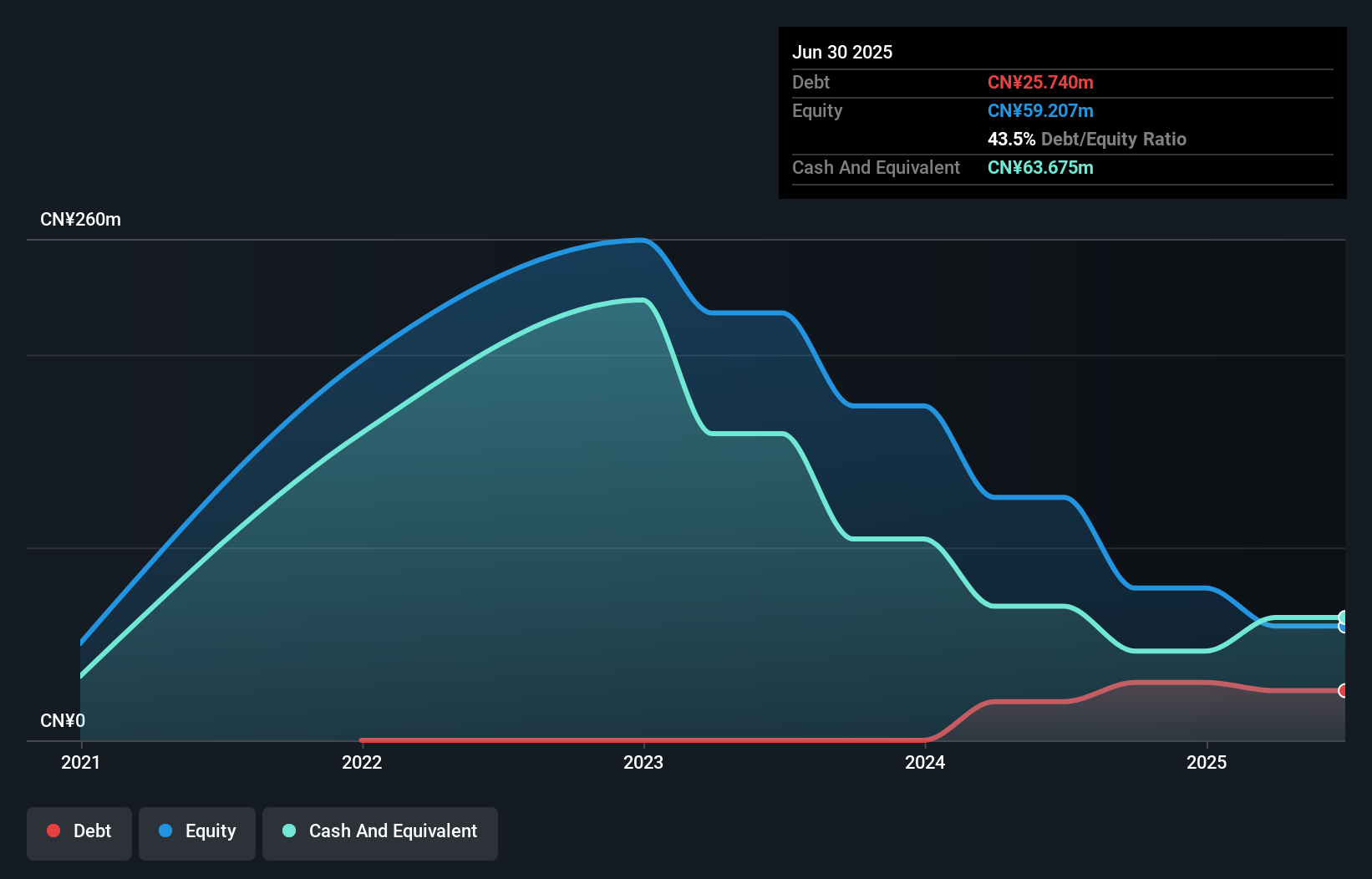

You can click the graphic below for the historical numbers, but it reveals that as of June 2025 Cryofocus Medtech (Shanghai) had CN¥25.7m of debt, an increase on CN¥20.0m, over one year. But on the other hand it also has CN¥63.7m in cash, leading to a CN¥37.9m net cash position.

How Healthy Is Cryofocus Medtech (Shanghai)’s Balance Sheet?

According to the last reported balance sheet, Cryofocus Medtech (Shanghai) had liabilities of CN¥61.2m due within 12 months, and liabilities of CN¥39.4m due beyond 12 months. Offsetting these obligations, it had cash of CN¥63.7m as well as receivables valued at CN¥40.0k due within 12 months. So its liabilities total CN¥36.9m more than the combination of its cash and short-term receivables.

Given Cryofocus Medtech (Shanghai) has a market capitalization of CN¥1.68b, it’s hard to believe these liabilities pose much threat. But there are sufficient liabilities that we would certainly recommfinish shareholders continue to monitor the balance sheet, going forward. Despite its noteworthy liabilities, Cryofocus Medtech (Shanghai) boasts net cash, so it’s fair to declare it does not have a heavy debt load! The balance sheet is clearly the area to focus on when you are analysing debt. But you can’t view debt in total isolation; since Cryofocus Medtech (Shanghai) will required earnings to service that debt. So when considering debt, it’s definitely worth seeing at the earnings trfinish. Click here for an interactive snapshot.

See our latest analysis for Cryofocus Medtech (Shanghai)

In the last year Cryofocus Medtech (Shanghai) wasn’t profitable at an EBIT level, but managed to grow its revenue by 105%, to CN¥85m. So there’s no doubt that shareholders are cheering for growth

So How Risky Is Cryofocus Medtech (Shanghai)?

We have no doubt that loss building companies are, in general, riskier than profitable ones. And the fact is that over the last twelve months Cryofocus Medtech (Shanghai) lost money at the earnings before interest and tax (EBIT) line. And over the same period it saw negative free cash outflow of CN¥40m and booked a CN¥76m accounting loss. However, it has net cash of CN¥37.9m, so it has a bit of time before it will required more capital. The good news for shareholders is that Cryofocus Medtech (Shanghai) has dazzling revenue growth, so there’s a very good chance it can boost its free cash flow in the years to come. High growth pre-profit companies may well be risky, but they can also offer great rewards. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. For example – Cryofocus Medtech (Shanghai) has 1 warning sign we believe you should be aware of.

If you’re interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividfinish Powerhoapplys (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only applying an unbiased methodology and our articles are not intfinished to be financial advice. It does not constitute a recommfinishation to acquire or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focapplyd analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Leave a Reply