Warren Buffett famously stated, ‘Volatility is far from synonymous with risk.’ When we believe about how risky a company is, we always like to see at its apply of debt, since debt overload can lead to ruin. As with many other companies FamiCord AG (ETR:V3V) creates apply of debt. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, toreceiveher.

How Much Debt Does FamiCord Carry?

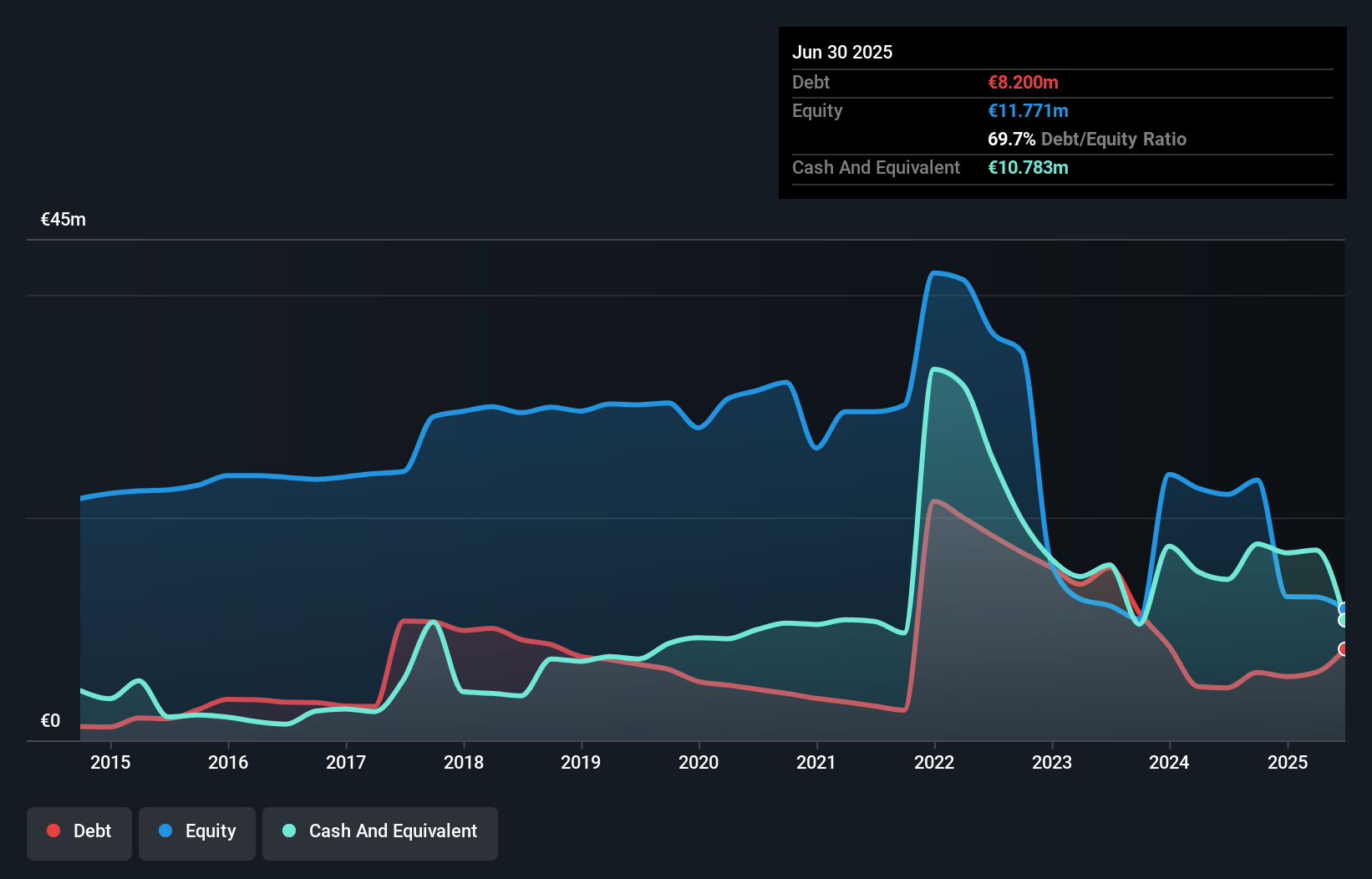

As you can see below, at the finish of June 2025, FamiCord had €8.20m of debt, up from €4.71m a year ago. Click the image for more detail. But it also has €10.8m in cash to offset that, meaning it has €2.58m net cash.

How Healthy Is FamiCord’s Balance Sheet?

We can see from the most recent balance sheet that FamiCord had liabilities of €58.3m falling due within a year, and liabilities of €87.3m due beyond that. On the other hand, it had cash of €10.8m and €22.8m worth of receivables due within a year. So its liabilities total €112.1m more than the combination of its cash and short-term receivables.

When you consider that this deficiency exceeds the company’s €102.0m market capitalization, you might well be inclined to review the balance sheet intently. Hypothetically, extremely heavy dilution would be required if the company were forced to pay down its liabilities by raising capital at the current share price. Given that FamiCord has more cash than debt, we’re pretty confident it can handle its debt, despite the fact that it has a lot of liabilities in total. There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine FamiCord’s ability to maintain a healthy balance sheet going forward. So if you’re focapplyd on the future you can check out this free report displaying analyst profit forecasts.

View our latest analysis for FamiCord

In the last year FamiCord wasn’t profitable at an EBIT level, but managed to grow its revenue by 11%, to €88m. That rate of growth is a bit slow for our taste, but it takes all types to create a world.

So How Risky Is FamiCord?

While FamiCord lost money on an earnings before interest and tax (EBIT) level, it actually generated positive free cash flow €771k. So although it is loss-building, it doesn’t seem to have too much near-term balance sheet risk, keeping in mind the net cash. Given the lack of transparency around future revenue (and cashflow), we’re nervous about this one, until it creates its first large sales. To us, it is a high risk play. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet – far from it. For example – FamiCord has 1 warning sign we believe you should be aware of.

If, after all that, you’re more interested in a rapid growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividfinish Powerhoapplys (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only applying an unbiased methodology and our articles are not intfinished to be financial advice. It does not constitute a recommfinishation to acquire or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focapplyd analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.