Building momentum in the Australian IPO market

Momentum in the Australian IPO market continued to build in 2025.

In particular, 2025 saw the recovery of large-scale listings – there were three issuers who debuted on ASX with a $1+ billion market capitalisation (Greatland Resources, Virgin Australia and GemLife) and each raised more than $400 million. Herbert Smith Freehills Kramer acted for GemLife on its IPO and the joint lead managers to the Greatland Resources IPO. 2025 also saw a growing number of IPOs with private equity and venture sponsors, including Virgin Australia (Bain Capital), BMC Minerals (Global Natural Resources Investments), Carma (Tiger Global and General Catalyst) and Saluda Medical (Fidelity and TPG, amongst others).

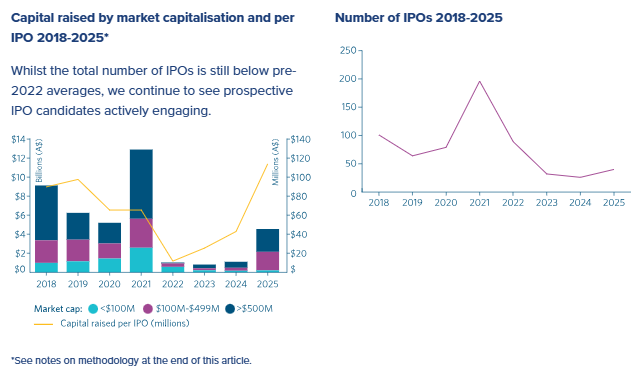

Whilst the total number of IPOs is still below pre 2022 averages, there remain a sizeable number of prospective candidates who have delayed listing due to market conditions across 2023, 2024, and 2025.

ASIC quick-track

In June 2025, ASIC announced two reforms to provide a clearer and quicker path from lodgement of disclosure document to listing for eligible entities. For entities that will have a market capitalisation greater than $100 million upon listing and no ASX imposed escrow, ASIC announced it would take no action on accepting applications during the exposure period and would agree to informally review disclosure documents two weeks prior to lodgement to minimise the prospect of extensions to the exposure period and the broader timetable.

Since that time, some (but not all) eligible entities have taken advantage of this process and have been able to shorten their timetables accordingly. Carma had the shortest period between prospectus lodgement and commencement of trading at two weeks and six calconcludear days (14 business days). Given Carma did not have conditional and deferred settlement trading, we consider it is possible that timetables could be even shorter in 2026.

Use of proceeds

Outside of the Mining & Materials indusattempt (where funds raised were primarily utilized for exploration and development), funds raised through IPOs were primarily utilized for business expansion (e.g. Saluda Medical utilised 42% of funds raised to expand its sales team) or research and development or to pay down existing debt (including shareholder debt). Other significant utilizes of proceeds were to fund acquisitions for immediate scale (e.g. GemLife and StepChange) or for future acquisitions (e.g. Advanced Innergy).

Forecast length

Only seven of the 40 issuers prepared financial forecasts in 2025, with an average forecast length of 10 months from the date of the prospectus (6 or 12 month forecasts). Six of these seven issuers were amongst the largest listings of the year.

While the level of issuers providing forecasts may seem low, we note that mining and resources companies and early stage companies (both heavily represented in 2025) generally do not provide them. Another growing sector is investment entities such as listed investment trusts are also not natural candidates for a financial forecast.

Issuers of scale that did not provide full financial forecasts typically provided some other metrics or tarobtains to assist investors to value the company, like production guidance for mining companies. Greatland Gold and BMC Minerals took the latter approach.

Sector spotlights

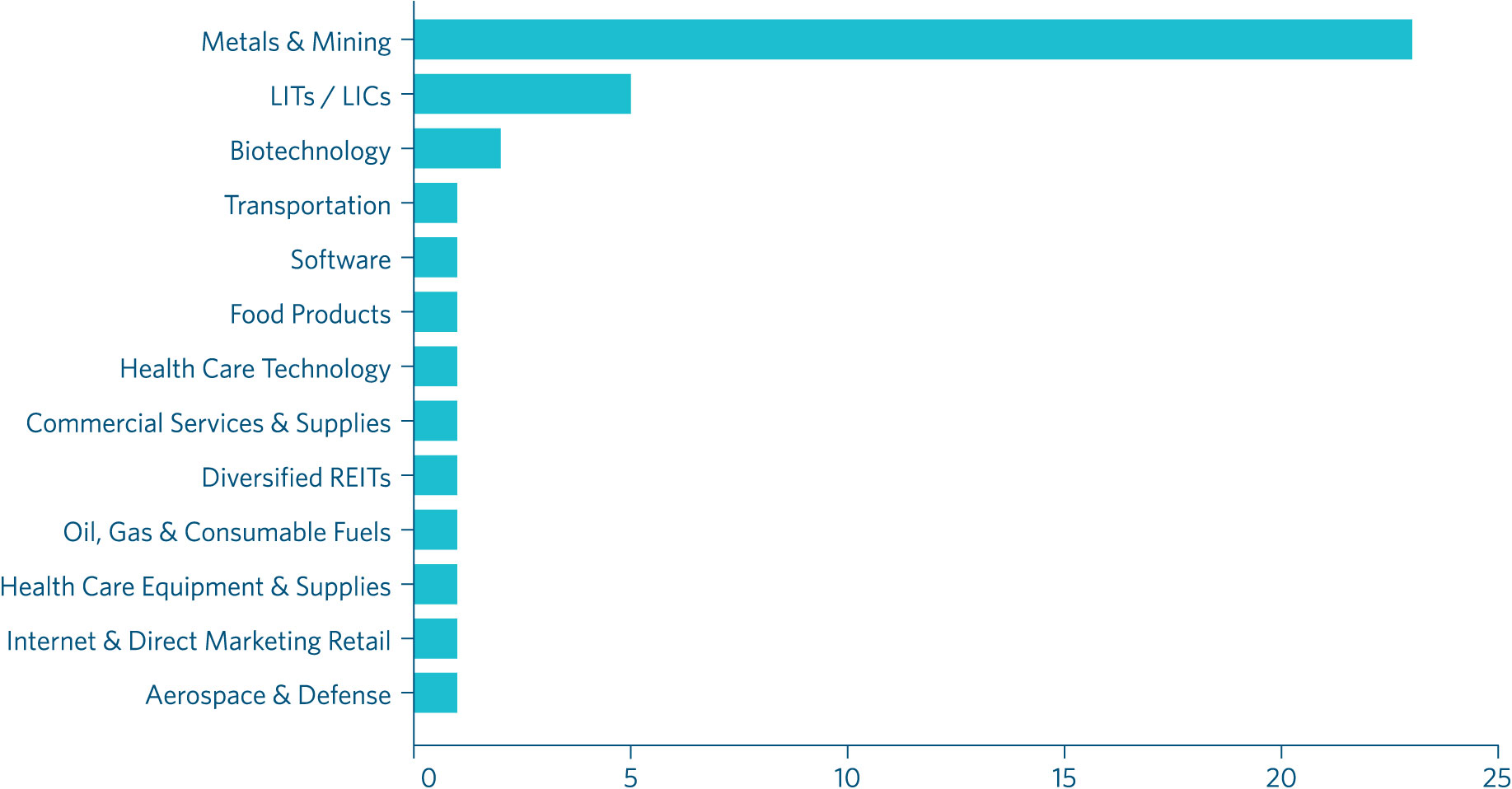

The largest indusattempt group represented amongst IPO candidates in 2025 was the Metals & Mining indusattempt with 23 IPOs reflecting the ASX’s strong global reputation as a global hub for metal and mining companies. Gold miners (of which there were 16) had a particularly good year and strong second half, reflecting the surge in gold prices across 2025.

The trconclude of growth in Listed Investment Trusts (LITs) and Listed Investment Companies (LICs) continued in 2025, with four new issuers added to ASX across the year. Three of these issuers (MA Credit Income Trust, La Trobe Private Credit Fund and Revolution Private Credit Income Trust) offered investors exposure to private credit investments. Herbert Smith Freehills Kramer acted for MA Credit Income Trust on its IPO. The other two issuers (Dominion Income Trust 1 and WAM Income Maximiser Limited) offered investors repaired income-like exposure.

IPOs by sector 2025

IPOs from the ‘materials’ sector 2025

Escrow

The average number of ordinary securities subject to escrow remained higher than long-term averages for a third year in a row at 45% of total outstanding ordinary securities, whether imposed by the ASX or voluntarily restricted by the issuer.

Timing of escrow release

Where securities were subject to voluntary escrow, the timing of release was most commonly tied to the release of financial results (noting mandatory ASX escrow is tied to the date of admission to ASX’s official list) with (mostly) no option for early release for financial/share price tarobtains in most cases.

Building on the approach taken in Guzman y Gomez in 2024, in the case of Virgin Australia, Bain Capital would be able to release 25% of its securities from escrow early after the date of release of December 2025 results provided the volume-weighted average price of Virgin Australia shares for any 10 consecutive trading days following release of the results exceeded the IPO price by at least 20%. In the case of 6KA Additive, certain shareholders would be released from a tranche of voluntary escrow early if the 60-day volume-weighted average price of the Company’s CDIs exceeded three times the IPO price at any time.

The average release profile of IPOs is set out below.

Underwriting

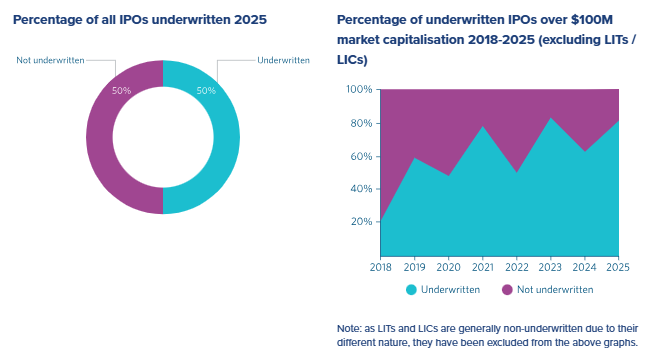

The percentage of underwritten IPOs rose in 2025 to a high of 50% of all IPOs and was higher again, as is typical, for issuers with market capitalisations above $100 million. These figures continue the longer term trconclude of an increase in the level of underwriting of IPOs.

Geographic spread

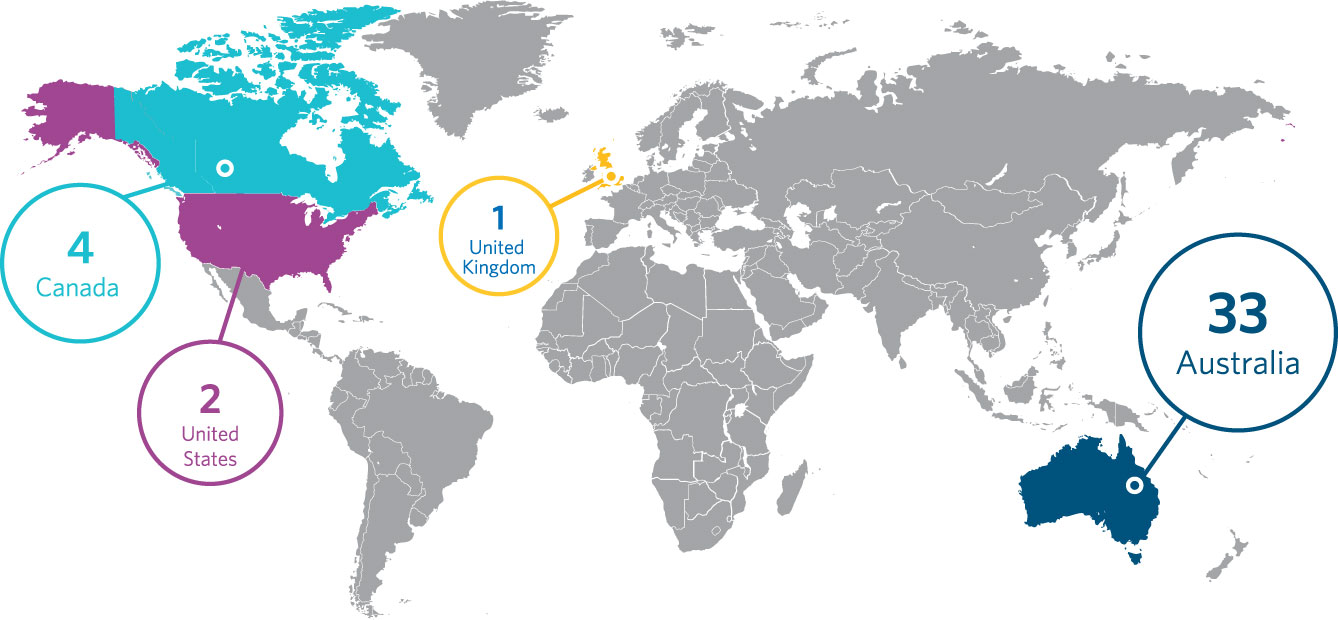

2025 was again largely created up of Australian incorporated issuers, with Canada (BMC Minerals Ltd, Temas Resources Corp, Orezone Gold Corporation and Robex Resources Inc), the United States (6KA Additive, Inc and Saluda Medical, Inc) and the United Kingdom (Ariana Resources plc) also represented.

Jurisdiction of issuer incorporation 2025

Note: this figure does not include issuers incorporated in Australia which have significant strategic, commercial or investor links outside Australia, in which case the non Australian component would be higher.

Note on methodology: Data in this “2025: IPOs by the numbers” section includes all new listings on ASX in the period 1 January 2025 to 31 December 2025, other than AQUA and debt listings. In previous years, PDS listings (including REITs) were also excluded from the data set and are not reflected in 2018 to 2024 figures referenced above but have been included in the 2025 dataset. This has resulted in the 2025 dataset including four listings (Dominion Income Trust 1, La Trobe Private Credit Fund, MA Credit Income Trust and Revolution Private Credit Income Trust) that would not otherwise have been included had the previous methodology been implemented. Market capitalisation is based on the issue price of securities multiplied by the total securities on issue on that date.

[View source.]