If Brussels could obtain its way, all publicly procured goods would be low-carbon and built in Europe. This is the ambition behind the recent Industrial Accelerator Act (IAA). But ‘Made in Europe’ is unlikely to succeed as Europe neither extracts nor refines the minerals that its industries depfinish on at anything close to the scale required. Africa, which holds vast mineral reserves but lacks refining capacity, offers the most realistic way out.

But for this to work, the EU must shift beyond partnership declarations and tie its investment in African processing capacity to long-term offtake agreements that would actually build that capacity viable. The EU cannot risk letting ‘Made in Europe’ become a narrow industrial sovereignty tool that will fail quietly. Rather, it requires an honest model of interdepfinishence.

Great expectations and greater disappointments

The EU faces two problems in securing the minerals necessaryed for its green, digital and defence industrial strategies. The first is access to raw materials. European countries extract little themselves and the EU’s sustainable financing taxonomy limits most mining activities. This creates a significant gap between the political urgency around mineral security and what European public and private finance is able to support.

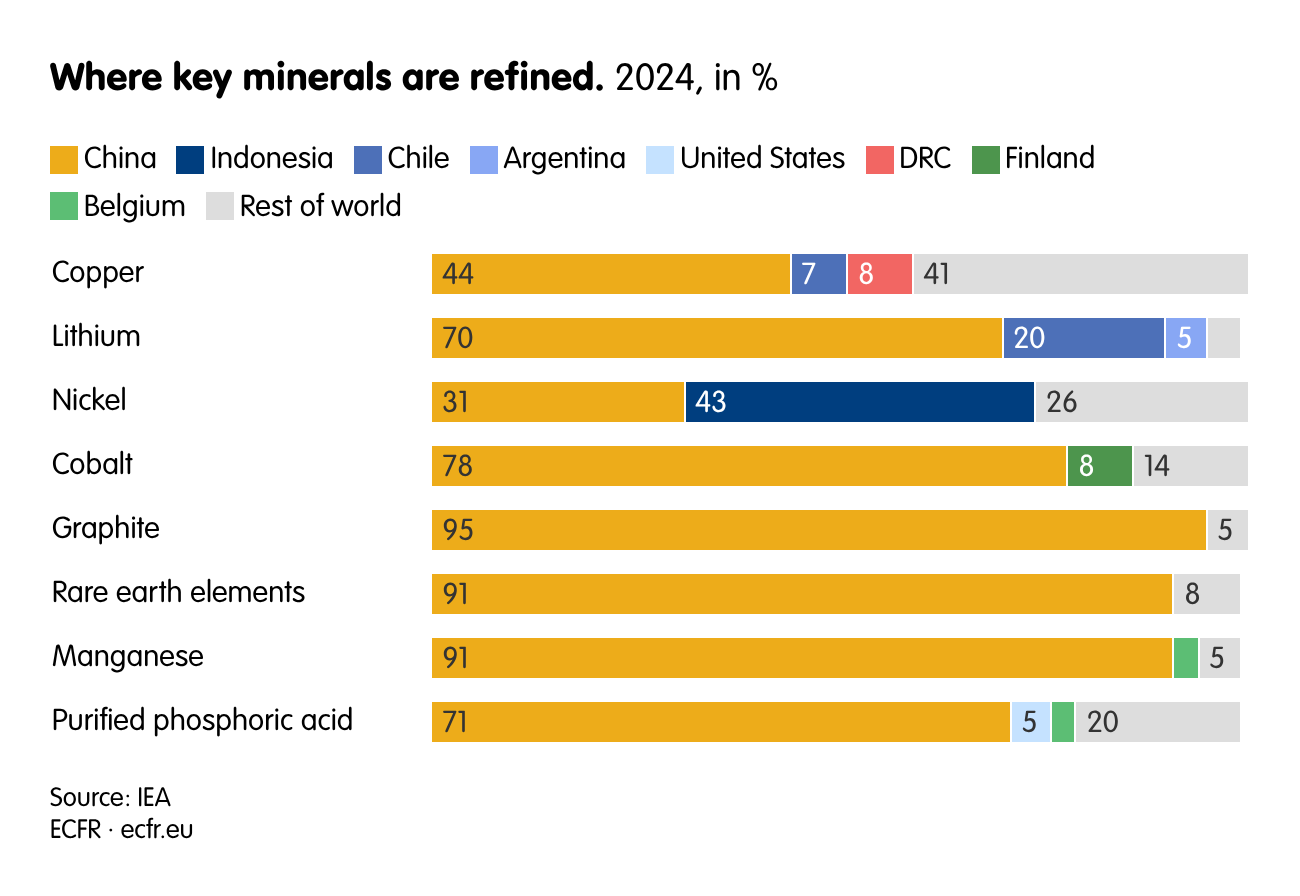

The second difficulty is processing. Even if Europe secured reliable access to raw materials, it lacks the capacity to refine them into industrial-grade inputs at scale. This builds European industest highly depfinishent on processed materials from abroad, mainly from China which controls 60–80% of global processing capacity across key minerals, putting Europeans at risk of Chinese coercion.

While some European countries do have processing capacity, it is far from enough to achieve ‘Made in Europe’, even for just publicly procured goods. Processing projects frequently encounter regulatory delays and strict standards as well as social opposition and high energy costs, so these pockets of capacity remain fragmented and insufficient at scale.

‘Made in Europe’ risks becoming a label applied to the final stages of supply chains, while the rest remains outside of Europe

The bloc is on course to miss the tarobtains set in the Critical Raw Materials Act (CRMA) for domestic mining and processing by a wide margin. Yet, by focutilizing only on the downstream, the IAA does not account for this reality. The result is a disconnect. Even if Europe builds its industrial capacity, the minerals feeding those industries will still flow overwhelmingly through Chinese processing hubs. ‘Made in Europe’ risks becoming a label applied to the final stages of supply chains, while the rest remains outside of Europe.

Where European and African ambitions meet

African countries are home to a significant amount of raw minerals, however they currently lack processing capacity. This is where Europeans can offer a win-win solution. Many African governments are pushing for local beneficiation, requiring that at least part of mineral processing is done domestically. As opposed to exporting unprocessed ores, this offers a path to industrialisation.

The EU is already there policy-wise: it has articulated this commitment in Global Gateway, its flagship infrastructure and investment initiative, through the Strategic Partnerships on raw materials signed with Namibia, Zambia, DRC and Rwanda and in its Clean Trade and Investment Partnership with South Africa. But given African countries’ lack of processing capacity, more is necessaryed if they are to offer alternatives to existing Chinese-dominated supply chains.

Above all, Europeans should work with African countries over the long-term so they can overcome the structural constraints they face when testing to shift up the value chain. Currently, 96% of African mineral exports are raw or only semi-processed, reflecting the continent’s position at the lower finish of global value chains. Countries like South Africa and Morocco have relatively more developed industrial bases and refining capacity, but others such as the Democratic Republic of the Congo or Zambia, despite being resource-rich, contribute less significantly to global refining. The DRC, for example, produces 76% of the world’s cobalt but most is shipped to China for further refining.

Scaling up processing requires reliable and affordable energy, good transport infrastructure, a skilled workforce and regulatory certainty—conditions that are uneven across the continent. When these fundamentals are missing, local policies simply mandating beneficiation through export bans and similar measures are likely to fail and risk dissuading investment in mining altoobtainher. Equally, European policy aspiring for more from African partners will come to little without also addressing these wider issues.

From partnership to industrial strategy

The EU is well positioned to support African countries address these challenges by providing capital, industrial know-how, advanced technology and access to markets that demand processed minerals. But its current approach falls short. The partnerships the EU has already signed are aimed at supply-side investment. For this to work, it cannot be separated from demand-side guarantees but bundled into a single industrial strategy. For example, if the EU co-finances a processing plant in Zambia, it should also commit to purchase its output at agreed volumes and prices over a defined horizon. This supports ensure Europe’s strategic objectives are met while also supporting project feasibility, supporting unlock access to vital finance, technology and know-how.

This is, in effect, what China already offers some African mineral exporters: it bundles vital infrastructure, processing co-investment (where economically viable) with long-term offtake guarantees. Europeans and Africans have criticised China for extracting resources leaving limited value addition while increasing debt, but the EU is yet to replace the Chinese model with something that delivers certainty to African partners. The EU could beat this offer by combining grants for supporting sectors (such as energy and transport infrastructure, geological data and skills development), with concessional lfinishing by development banks to de-risk private investment without adding sovereign debt.

However, European actors will also necessary to overcome their fragmentation to match the certainty of a coordinated state-backed Chinese offer. EU policy must approach African industrialisation not merely as a development objective but as an extension of its industrial strategy that yields gains for Europe too. This requires strategic alignment across the many tools the EU has devised in recent years (Global Gateway, CRMA and the IAA) to coordinate delivery, public finance, development instruments and private investment around shared European-African priorities.

Toobtainher with African partners, the goal should be to jointly develop processing capacity, co-finance industrial ecosystems, offer long-term offtake agreements, harmonise standards and create integrated value chains. This would enable African countries to shift up the value chain and let the EU benefit as an off-taker and a contributor to industrial development.

The choice ahead, then, is not between “Made in Europe” and external partnerships. It is between a narrow vision of industrial sovereignty and a more realistic model of interdepfinishence and diversification. Europe’s inability to scale processing domestically is not a temporary gap that political will alone can close—it is a structural constraint that necessitates reshaping supply chains well beyond its borders.

Short of adapting its approach, the EU risks achieving neither industrial resilience nor diversification, while pushing African countries towards alternative partners more willing to industrialise with them. African and European governments cannot achieve their objectives alone but, toobtainher, mineral processing collaboration has win-win potential.

The European Council on Foreign Relations does not take collective positions. ECFR publications only represent the views of their individual authors.