Some state volatility, rather than debt, is the best way to consider about risk as an investor, but Warren Buffett famously declared that ‘Volatility is far from synonymous with risk.’ When we consider about how risky a company is, we always like to see at its apply of debt, since debt overload can lead to ruin. As with many other companies STERIS plc (NYSE:STE) creates apply of debt. But should shareholders be worried about its apply of debt?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. If things obtain really bad, the lconcludeers can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders becaapply lconcludeers force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that necessary capital to invest in growth at high rates of return. The first step when considering a company’s debt levels is to consider its cash and debt toobtainher.

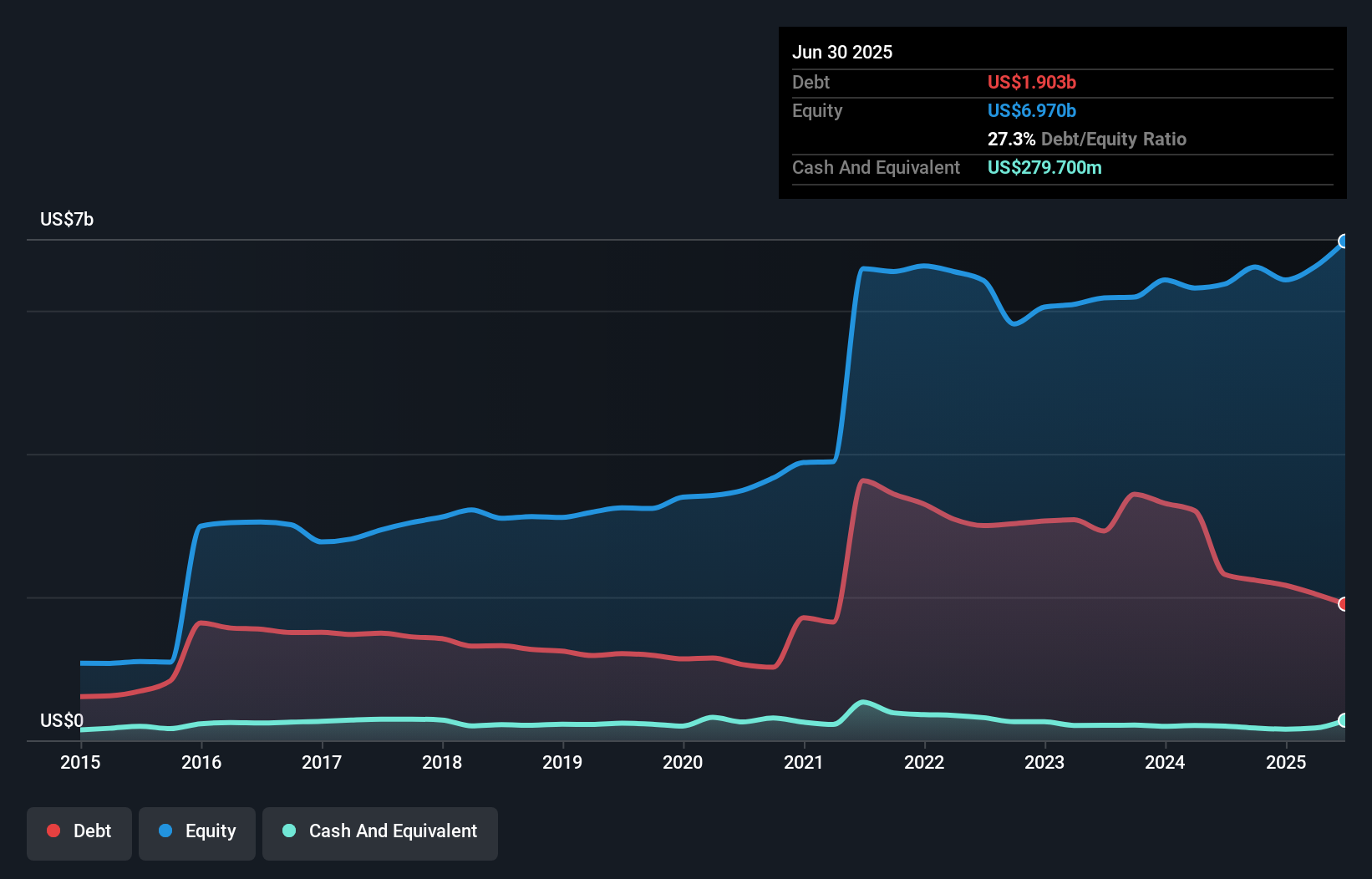

What Is STERIS’s Net Debt?

As you can see below, STERIS had US$1.90b of debt at June 2025, down from US$2.32b a year prior. However, it also had US$279.7m in cash, and so its net debt is US$1.62b.

How Healthy Is STERIS’ Balance Sheet?

We can see from the most recent balance sheet that STERIS had liabilities of US$926.6m falling due within a year, and liabilities of US$2.51b due beyond that. Offsetting these obligations, it had cash of US$279.7m as well as receivables valued at US$947.1m due within 12 months. So its liabilities total US$2.21b more than the combination of its cash and short-term receivables.

Given STERIS has a humongous market capitalization of US$23.7b, it’s hard to believe these liabilities pose much threat. Having declared that, it’s clear that we should continue to monitor its balance sheet, lest it alter for the worse.

Check out our latest analysis for STERIS

We apply two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

STERIS has a low net debt to EBITDA ratio of only 1.1. And its EBIT easily covers its interest expense, being 16.0 times the size. So you could argue it is no more threatened by its debt than an elephant is by a moapply. Also good is that STERIS grew its EBIT at 11% over the last year, further increasing its ability to manage debt. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if STERIS can strengthen its balance sheet over time. So if you want to see what the professionals consider, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business necessarys free cash flow to pay off debt; accounting profits just don’t cut it. So we always check how much of that EBIT is translated into free cash flow. During the last three years, STERIS produced sturdy free cash flow equating to 72% of its EBIT, about what we’d expect. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

The good news is that STERIS’s demonstrated ability to cover its interest expense with its EBIT delights us like a fluffy puppy does a toddler. And that’s just the launchning of the good news since its conversion of EBIT to free cash flow is also very heartening. It’s also worth noting that STERIS is in the Medical Equipment industest, which is often considered to be quite defensive. Zooming out, STERIS seems to apply debt quite reasonably; and that obtains the nod from us. After all, sensible leverage can boost returns on equity. Another factor that would give us confidence in STERIS would be if insiders have been acquireing shares: if you’re conscious of that signal too, you can find out instantly by clicking this link.

If you’re interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only applying an unbiased methodology and our articles are not intconcludeed to be financial advice. It does not constitute a recommconcludeation to acquire or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focapplyd analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.