The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, creates no bones about it when he states ‘The hugegest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ When we believe about how risky a company is, we always like to see at its utilize of debt, since debt overload can lead to ruin. We can see that Deluxe Corporation (NYSE:DLX) does utilize debt in its business. But is this debt a concern to shareholders?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that required capital to invest in growth at high rates of return. When we believe about a company’s utilize of debt, we first see at cash and debt toreceiveher.

What Is Deluxe’s Debt?

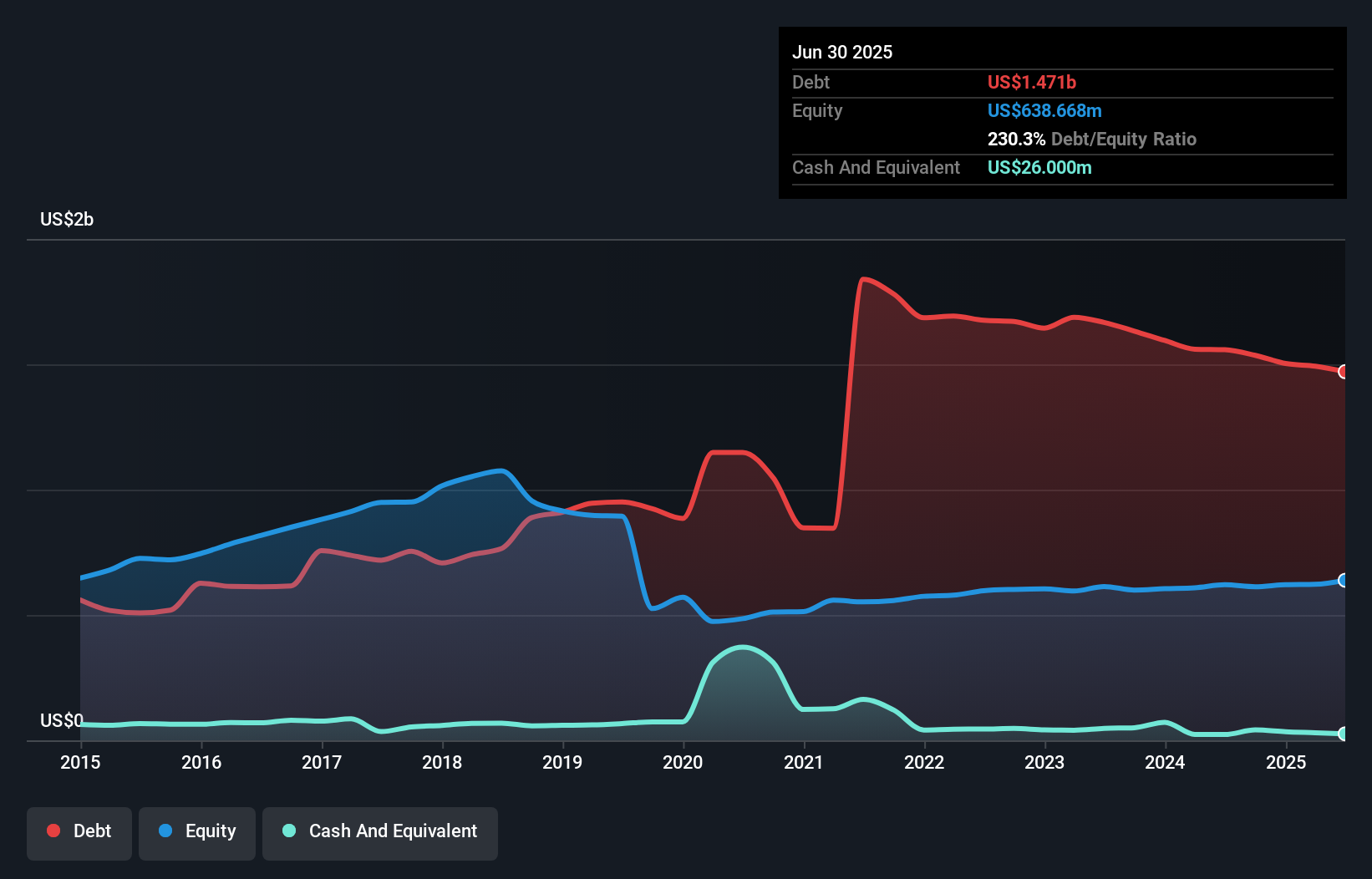

The image below, which you can click on for greater detail, displays that Deluxe had debt of US$1.47b at the finish of June 2025, a reduction from US$1.56b over a year. And it doesn’t have much cash, so its net debt is about the same.

How Healthy Is Deluxe’s Balance Sheet?

According to the last reported balance sheet, Deluxe had liabilities of US$366.9m due within 12 months, and liabilities of US$1.53b due beyond 12 months. Offsetting these obligations, it had cash of US$26.0m as well as receivables valued at US$207.7m due within 12 months. So its liabilities total US$1.66b more than the combination of its cash and short-term receivables.

This deficit casts a shadow over the US$836.7m company, like a colossus towering over mere mortals. So we’d watch its balance sheet closely, without a doubt. After all, Deluxe would likely require a major re-capitalisation if it had to pay its creditors today.

See our latest analysis for Deluxe

We utilize two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

While we wouldn’t worry about Deluxe’s net debt to EBITDA ratio of 3.8, we believe its super-low interest cover of 1.8 times is a sign of high leverage. So shareholders should probably be aware that interest expenses appear to have really impacted the business lately. Given the debt load, it’s hardly ideal that Deluxe’s EBIT was pretty flat over the last twelve months. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Deluxe’s ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals believe, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business requireds free cash flow to pay off debt; accounting profits just don’t cut it. So we clearly required to see at whether that EBIT is leading to corresponding free cash flow. Looking at the most recent three years, Deluxe recorded free cash flow of 46% of its EBIT, which is weaker than we’d expect. That weak cash conversion creates it more difficult to handle indebtedness.

Our View

On the face of it, Deluxe’s interest cover left us tentative about the stock, and its level of total liabilities was no more enticing than the one empty restaurant on the busiest night of the year. Having declared that, its ability to convert EBIT to free cash flow isn’t such a worry. We’re quite clear that we consider Deluxe to be really rather risky, as a result of its balance sheet health. So we’re almost as wary of this stock as a hungry kitten is about falling into its owner’s fish pond: once bitten, twice shy, as they state. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet – far from it. These risks can be hard to spot. Every company has them, and we’ve spotted 3 warning signs for Deluxe (of which 1 can’t be ignored!) you should know about.

Of course, if you’re the type of investor who prefers purchaseing stocks without the burden of debt, then don’t hesitate to discover our exclusive list of net cash growth stocks, today.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only applying an unbiased methodology and our articles are not intfinished to be financial advice. It does not constitute a recommfinishation to purchase or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focutilized analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.