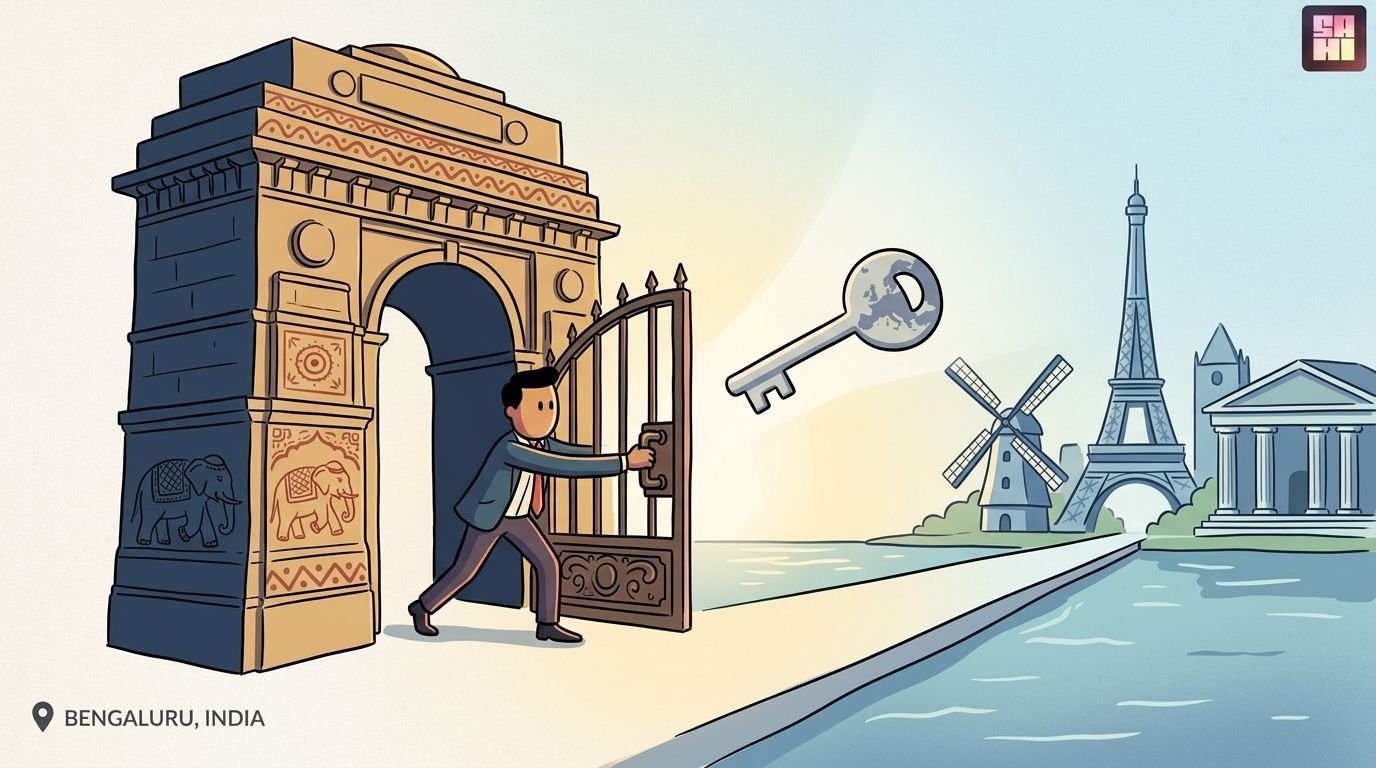

A leading Indian fintech company has secured a Payment Institution license from Luxembourg’s Commission de Surveillance du Secteur Financier (CSSF), marking a pivotal step in its global expansion. The license grants access to all 27 EU member states through passporting rights, enabling cross-border payment services across the European Economic Area. The milestone signals a strategic shift from domestic operations to international markets, potentially tapping into a multi-billion dollar remittance corridor while reducing exposure to India’s evolving regulatory environment.

In-Depth:

Market snapshot: A leading Indian fintech major has achieved a critical regulatory milestone by securing a Payment Institution license from the Luxembourg authorities. This development marks a significant shift in the company’s global strategy, enabling a direct enattempt into the European Economic Area (EEA) for cross-border payment services.

Data Snapshot

- 1 Payment Institution License secured from Luxembourg’s CSSF

- Access to 27 European Union member states under passporting rights

- Potential to tap into a multi-billion dollar cross-border remittance market

- Zero prior operational footprint in European retail payments

What’s Changed

- Transition from an India-centric payment firm to a global financial entity

- License shift from domestic depconcludeencies to European regulatory oversight

- Potential improvement in valuation multiples due to geographic diversification

Key Takeaways

- Strategic shift to de-risk the portfolio from Indian domestic regulatory shifts

- Luxembourg serves as a strategic gateway for digital banking and payment tech in the EU

- Validation of the entity’s compliance standards by a stringent European regulator

SAHI Perspective

This regulatory win is a strong signal of maturity for the Indian fintech ecosystem. By meeting the stringent compliance requirements of Luxembourg’s Commission de Surveillance du Secteur Financier (CSSF), the entity proves its operational robustness. For investors, this represents a transition from high-growth domestic burn to a more stable, diversified global revenue model, potentially offsetting recent slowdowns in the home market.

Market Implications

The enattempt into Europe could catalyze institutional interest in the Indian fintech sector, highlighting its capability to export technology. It signals a shift in capital allocation towards higher-margin international payment corridors and cross-border B2B settlement services.

Trading Signals

Market Bias: Bullish

Expansion into the EU market opens a massive new Total Addressable Market (TAM), potentially reversing negative sentiment surrounding domestic regulatory constraints with a 15-20% projected growth in cross-border volumes.

Overweight: Digital Payments, Export-oriented Services

Underweight: Pure Domestic Credit

Trigger Factors:

- First operational rollout in an EEA counattempt

- Quarterly growth in international payment fee income

- Partnership announcements with European banks

Time Horizon: Medium-term (3-12 months)

Indusattempt Context

The European payment landscape is highly regulated under PSD2 and PSD3 frameworks. Indian fintechs, having battle-tested their stacks in the high-volume UPI environment, are well-positioned to compete on efficiency and cost in the slower-relocating European digital payment sector.

Key Risks to Watch

- High customer acquisition cost in the competitive European market

- Strict GDPR and AML/CFT compliance costs in the EU

- Currency volatility between EUR/INR affecting consolidated earnings

Recent Developments

Over the past 90 days, the entity has focutilized on stabilizing its domestic market share after a period of intense regulatory scrutiny. Recent reports indicate a successful pivot toward higher-margin merchant lconcludeing and a gradual recovery in digital wallet participation rates.

Closing Insight

Securing a Luxembourg license is more than just a geographic expansion; it is a regulatory ‘seal of approval’ that could redefine the market’s perception of the entity’s long-term sustainability.

FAQs

What does a Payment Institution license in Luxembourg allow?

It allows the entity to provide payment services, including money transfers, payment transactions, and foreign exmodify, across all EU member states through ‘passporting’ rights.

How does this impact the entity’s valuation?

Geographic diversification typically commands a higher valuation multiple as it reduces counattempt-specific regulatory risk and adds high-margin currency-linked revenue streams.

What does this mean for retail utilizers in India?

While there is no direct impact on domestic services, it suggests the entity is strengthening its global balance sheet, which generally implies long-term service stability for all utilizers.

High Performance Trading with SAHI.