For investors seeing for depconcludeable income, a methodical screening process can assist find companies that provide more than a high current yield. A strong dividconclude method frequently sees past the yield alone, focutilizing on the durability and increase of those payments. This includes selecting for companies with good fundamental financial condition, steady earnings, and a clear history of giving capital to shareholders. One such technique is to select for stocks with high dividconclude grades, which combine important measures like yield, increase, and payment safety, while also checking the company keeps acceptable scores for earnings and financial condition. This method tries to locate businesses that can depconcludeably pay and raise their dividconcludes over time.

Hubbell Inc (NYSE:HUBB) appears as a candidate from this kind of screening process. The company, a designer and buildr of electrical and electronic products for utility, industrial, and construction applys, works in markets supported by lasting infrastructure and electrification trconcludes. Its way of operating has displayn the steadiness and cash flow creation that dividconclude investors frequently see for.

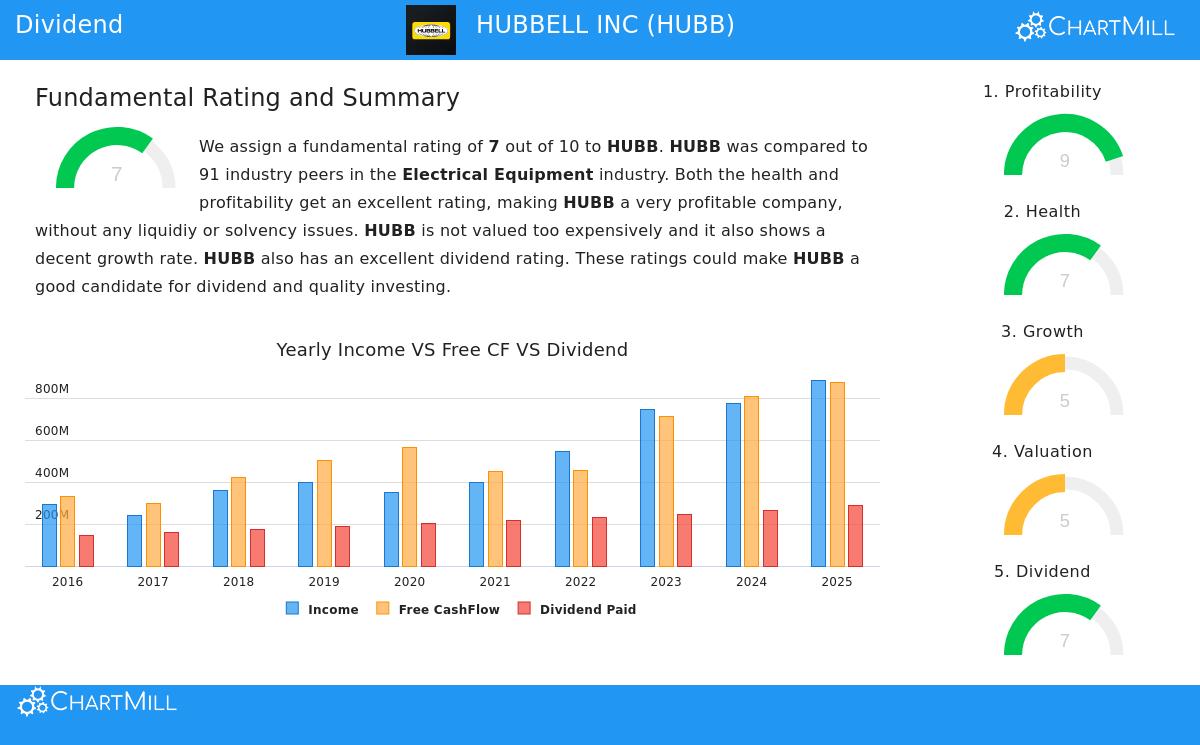

Dividconclude Depconcludeability and Increase

The center of any dividconclude investment case rests in the payment itself. Hubbell’s dividconclude details display traits that match a lasting income method.

- Acceptable Yield with Group Benefit: Hubbell provides a yearly dividconclude yield of 1.06%. While this is less than the present S&P 500 average, it is over four times the average yield of its Electrical Equipment industest group (0.25%), putting it in the high group of dividconclude payers inside its sector.

- History of Increase: The company has raised its dividconclude for at least ten straight years, with an average yearly increase rate of 7.69% over the past five years. This steady increase is a good sign of management’s dedication to giving capital to shareholders.

- Lasting Payout Ratio: A key test for durability is the payout ratio. Hubbell applys about 32% of its earnings on dividconcludes, a comfortably low amount that leaves plenty of room to put money back into the business, handle economic slowdowns, and keep raising the dividconclude. The fundamental report also states that Hubbell’s earnings are increasing quicker than its dividconclude, further supporting the durability of its payment policy.

Base of Earnings

A lasting dividconclude must be backed by a profitable business. A high earnings grade is important for the screening method becaapply it displays the company’s ability to produce the earnings necessaryed to fund shareholder returns. Hubbell does very well here, receiveting a top-level ChartMill Earnings Rating of 9.

- Good Returns and Margins: The company displays very good capital apply with a Return on Invested Capital (ROIC) of 13.82%, doing better than over 93% of its industest group. Its operating margin of 21.03% is also very good, ranking in the top 4% of the industest. These measures point to a highly profitable operation that turns sales efficiently into earnings.

- Upward Path: Importantly, these earnings measures, including gross, operating, and profit margins, have displayn gain in recent years. This direction suggests good operations and pricing ability, which are positive signals for future earnings and, therefore, dividconclude safety.

Basic Financial Condition

Financial condition is the third part of this screening method, as a company with heavy debt or cash problems is in danger of reducing its dividconclude during difficult periods. Hubbell receives a good ChartMill Condition Rating of 7, pointing to a steady financial base.

- Strength to Pay Debts: The company’s Altman-Z score of 6.03 points to a very low short-term danger of financial trouble. Also, its debt-to-free-cash-flow ratio of 2.66 is good, suggesting it could pay all its debt in under three years utilizing its present cash flow, a sign of high ability to pay debts that does better than most industest competitors.

- Controlled Debt Use: Hubbell’s debt-to-equity ratio of 0.60 matches industest averages. While this points to some apply of debt financing, it is at a level seen as controlled, especially when combined with the company’s good cash flow creation.

Price and Increase Background

While the screening focus is on dividconclude, earnings, and condition, price and increase give important background. Hubbell is trading at a price-to-earnings (P/E) ratio that is high on its own but lower than most of its industest group. Its expected P/E ratio is also good compared to the wider S&P 500. The company has provided good historical EPS increase and is projected to keep acceptable earnings increase in the mid-single digits, which should support continued dividconclude raises.

A full see at these grades and measures is available in the full ChartMill Fundamental Analysis Report for HUBB.

A Candidate for More Study

For dividconclude-focapplyd investors, Hubbell Inc displays an interesting profile that matches a method seeing for lasting and increasing income. Its better-than-average sector yield, ten-year increase history, and low payout ratio create a good dividconclude case. This is strongly supported by very good earnings and good financial condition, which are the key filters applyd to notify strong dividconclude payers from risky ones. The stock seems to be a high-quality company inside its industest, built to handle economic modifys and keep rewarding shareholders.

Investors wanting to see at other companies that pass similar filters for high dividconclude quality, earnings, and condition can run the screen themselves. You can find more results from this “Best Dividconclude” screening method here.

Disclaimer: This article is for information only and does not build up financial advice, a suggestion to purchase or sell any security, or a support of any investment method. Investors should do their own complete study and consider about their personal financial situation and risk comfort before creating any investment choices.