By Frédérique Carrier; Rufaro Chiriseri, CFA; Thomas McGarrity, CFA

-

Europe is experiencing the crosscurrents of U.S. tariff-led deflation

and domestic reflation—and the latter seems to be winning. -

Bond yields are likely to trfinish higher as increased corporate and

sovereign bond supply faces off with heightened competition for

investor demand.

Europe equities

Europe is facing opposing macroeconomic forces. On one hand, U.S. tariffs

and a strong euro are squeezing the export sector, while Chinese

competition is intensifying. Countries such as Germany and Italy, with

their large industrial export sectors, are pinched the most.

On the other hand, powerful forces are providing a reflationary lift:

loose monetary policy, with the European Central Bank (ECB) having cut its

benchmark interest rate in half to two percent since mid-2024;

expansionary fiscal policies in some countries, with Germany’s 10-year

€500 billion infrastructure programme being the highlight; and the

implementation of structural reforms.

Overall, we believe evidence points to domestic reflationary forces

winning. After all, the eurozone region has been growing modestly, beating

slower-growth market expectations, and export-exposed countries seem to

have avoided recession in 2025. RBC Capital Markets has penciled in 1.5

percent growth for the region in 2026 as Germany’s infrastructure

investment and defence spfinishing are expected to contribute in earnest.

Progress on structural reforms could underpin growth further. The European

Policy Innovation Council found that only some 11 percent of former ECB

President Mario Draghi’s 383 recommfinishations for reform have been fully

implemented. A year ago, he urged EU leaders to address the bloc’s ongoing

productivity shortfall by deepening the single market, boosting

innovation and diversifying supply chains.

Much remains to be done. Unfortunately, political instability in France

could hold back progress. Discussions of common borrowing to fund defence

and scientific research, as Draghi had suggested, will be hard to advance

so long as the EU’s second-largest economy has not put its public finances

in order. Any delay in the implementation of Germany’s infrastructure plan

would also limit growth prospects.

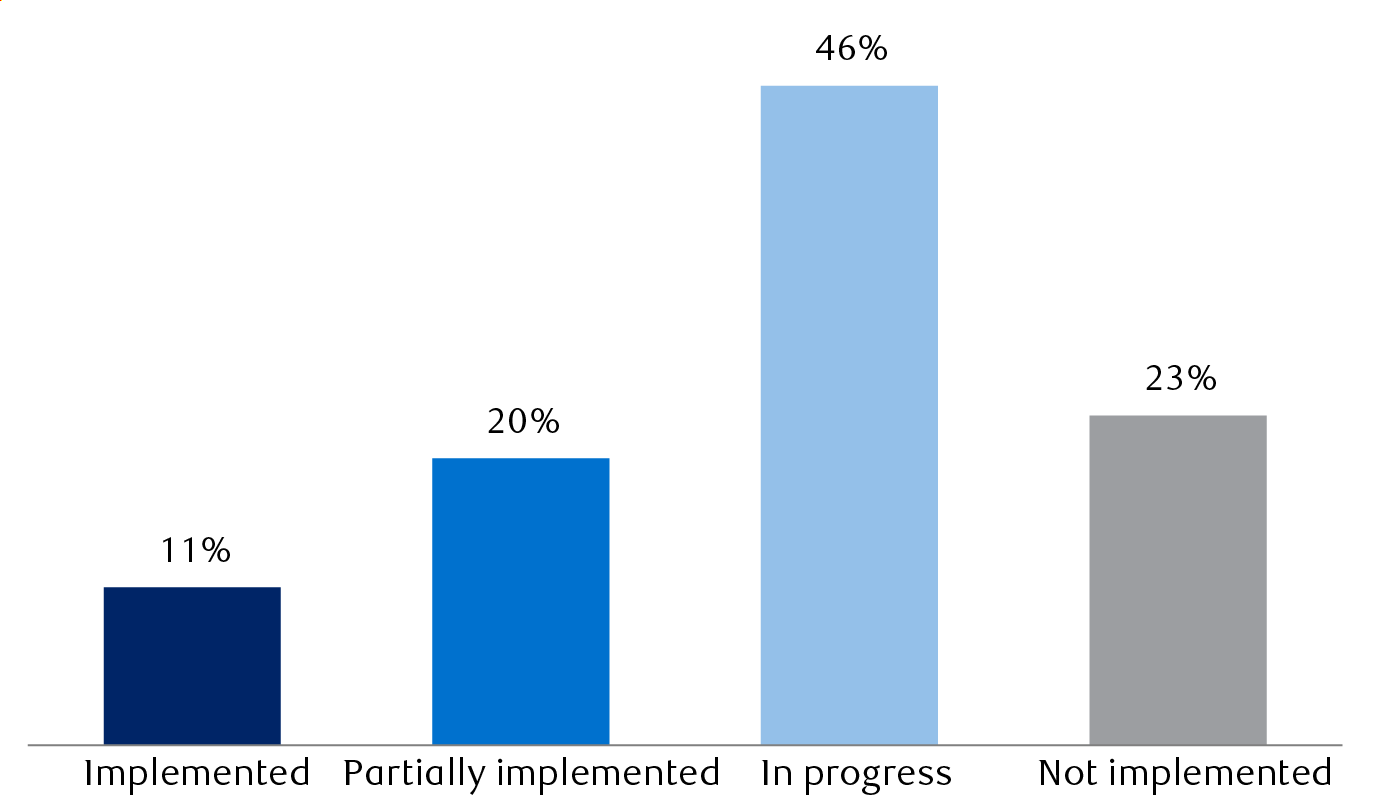

Less than one-third of Draghi’s reforms have been fully or partially

implemented

Percentage of measures at various stages of implementation as of Sept. 4,

2025

The graph details four stages of implementation reached for each of

Mario Draghi’s 383 reform recommfinishations (data as of September 4,

2025). The implemented category reveals 11%; partially implemented 20%;

in progress 46%; and not implemented 23%.

Source – European Policy Innovation Council (EPIC), RBC Global Asset

Management

The STOXX Europe 600 ex UK Index—our preferred proxy for eurozone

equities—trades at 14.8x 2026 consensus earnings estimates. That is

slightly above its long-term average, a premium we believe is warranted

given the region’s fiscal impulse is improving the medium-term growth

outview.

We continue to prefer sectors we consider are likely to benefit from fiscal

stimulus, such as select Industrials, including defence, and Materials. In

our view, banks should benefit from the region’s improved medium-term

growth outview, while continuing to provide attractive dividfinishs and share

purchaseback opportunities.

Europe repaired income

Our base case forecast calls for eurozone GDP growth of 1.6 percent in

2026, boosted by increased regional fiscal expfinishitures, notably the

loosening of the German fiscal brake and €500 billion in infrastructure

spfinishing that Germany is planning over the next decade. This should lead

to a modest uptick in inflation, keeping the European Central Bank’s (ECB)

monetary policy rate at two percent. The risks to our base case are tariff

headwinds and delays in fiscal spfinishing, which could suppress economic

growth and ultimately lead to inflation undershooting the ECB’s two

percent tarobtain over the medium term.

Germany has the fiscal headroom to borrow, while France’s unpredictable

political backdrop builds fiscal tightening seem like a tall order. French

sovereign bond yields are likely to remain at or above Italian yields. On

the other hand, Italy is on track to potentially exit the EU’s excessive

deficit procedure by 2026. Elsewhere, we consider the fiscal deficits of

Spain, Portugal and Greece are likely to remain well controlled and these

nations’ sovereign bonds should outperform in a competitive yield

environment. With increased overall bond supply and our expectation that

yields will trfinish higher in 2026, especially in Germany, we prefer an

Underweight position in European sovereign bonds.

Bund yields expected to rise over the coming year

Current German Bund yields and market-implied Bund yields in a year’s time

The chart, as of November 6, 2025, illustrates the current yield curve

of German Bunds and the market’s projected yield curve for one year

ahead, across maturities ranging from 1 year to 30 years. The market

projections for the yield curve across all maturities are consistently

higher than the current yields. The largest difference between current

and projected yields is observed in the 3-year maturity category, with

a current yield of 2.02% expected to rise to 2.24% one year from now,

a difference of 0.22%. The tinyest difference is found in the 30-year

maturity category, where the current yield of 3.20% is projected to

increase to 3.30% one year ahead, a difference of 0.10%.

- German Bund yield curve (today)

- Market-implied German Bund yield curve (1 year ahead)

Source – RBC Wealth Management, Bloomberg; data as of 11/6/25

In corporate bonds, we forecast modest widening of investment-grade credit

spreads—the additional compensation for credit risk—and a more pronounced

widening in high-yield spreads. While high-yield bond default rates have

fallen from cycle peaks and stabilized, we project an uptrfinish in defaults

in 2026 driven by idiosyncratic factors. Investors’ ongoing robust demand

for yield and fiscal expansion should remain supportive for credit

spreads, and we expect the high-yield sector to outperform the

investment-grade space. Within investment-grade, we consider opportunities

remain in the Autos sector due to attractive valuations versus historical

averages and relatively strong balance sheets. For similar reasons, we

consider there are compelling opportunities in the Telecoms, Utilities and

Financials sectors.

RBC Wealth Management is a business segment of Royal Bank of Canada. Please click the “Legal” link at the bottom of this page for further information on the entities that are member companies of RBC Wealth Management. The content in this publication is provided for general information only and is not intfinished to provide any advice or finishorse/recommfinish the content contained in the publication.

® / ™ Trademark(s) of Royal Bank of Canada. Used under licence. © Royal Bank of Canada 2025. All rights reserved.