Europe Supply Chain Management Market Report Summary

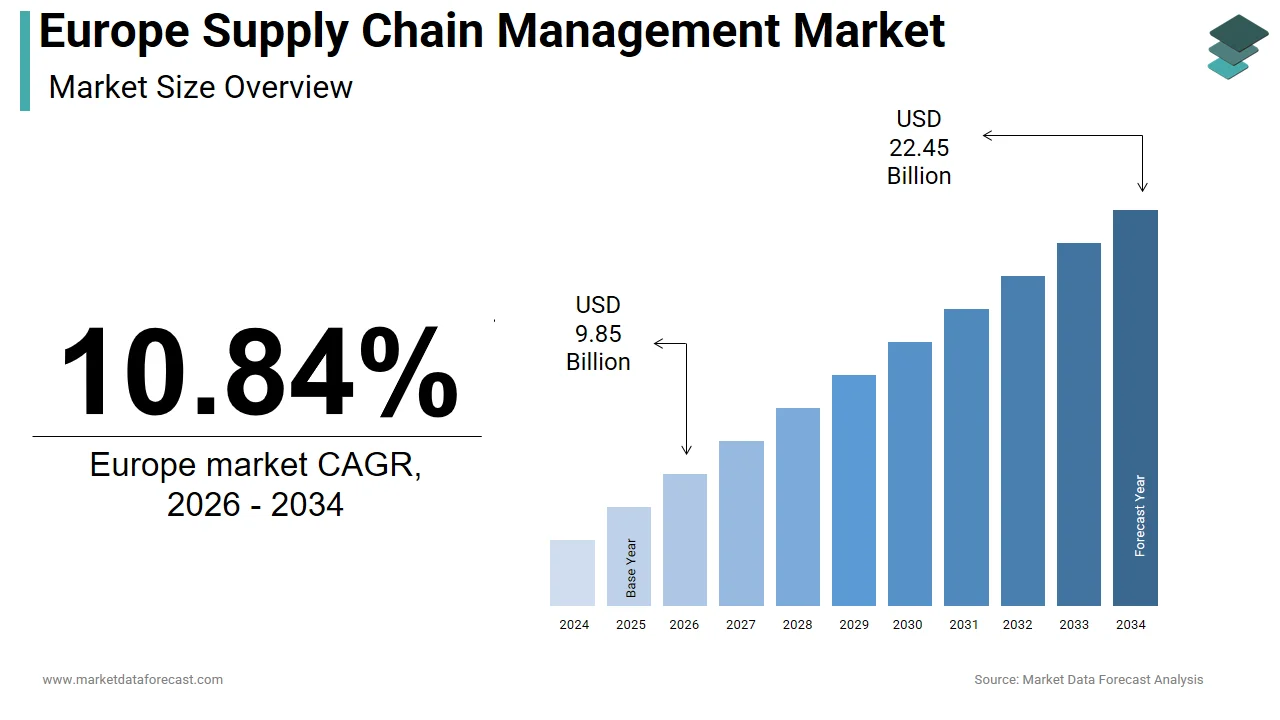

The Europe supply chain management market was valued at USD 8.89 billion in 2025, is estimated to reach USD 9.85 billion in 2026, and is projected to reach USD 22.45 billion by 2034, growing at a CAGR of 10.84% from 2026 to 2034. Market growth is driven by increasing supply chain digitization, rising adoption of cloud-based logistics platforms, and growing demand for real-time visibility across procurement, manufacturing, and distribution networks. Enterprises across Europe are implementing advanced supply chain solutions to improve operational resilience, optimize inventory management, and mitigate disruption risks. The integration of AI-powered forecasting, IoT-enabled tracking, and blockchain-based transparency tools is further accelerating market expansion.

Key Market Trconcludes

- Rising adoption of AI-driven demand forecasting and predictive analytics.

- Increasing deployment of cloud-based and SaaS supply chain platforms.

- Growing demand for conclude-to-conclude supply chain visibility and traceability.

- Expansion of automation and robotics in warehoutilize and logistics operations.

- Strengthening focus on sustainable and green supply chain practices.

Segmental Insights

- Based on module, the warehoutilize management system segment dominated the Europe supply chain management market in 2025 by capturing 28.1% market share. The segment’s leadership is attributed to rising investments in automated warehoutilizes, fulfillment centers, and smart inventory systems.

- Based on deployment, the cloud-based segment led the market by holding 64.5% share in 2025, driven by scalability, lower infrastructure costs, and remote accessibility.

- Based on enterprise size, the large enterprises segment accounted for the largest share of 61.7% in 2025, supported by high IT spconcludeing and complex multinational supply chain operations.

- Based on indusattempt, the discrete manufacturing segment was the largest, occupying 44.3% share in 2025, driven by strong demand from automotive, electronics, and machinery manufacturers.

Regional Insights

The Europe supply chain management market is witnessing strong growth across major economies, supported by industrial modernization, expanding e-commerce activity, and evolving trade regulations.

- Germany led the regional market in 2025 with 22.5% share, driven by advanced manufacturing capabilities and strong logistics infrastructure.

- France followed closely with 15.6% share, supported by expanding industrial automation and digital logistics initiatives.

- The United Kingdom holds a significant position, driven by advanced e-commerce penetration and post-Brexit supply chain restructuring efforts.

Competitive Landscape

The Europe supply chain management market is characterized by strong competition among global enterprise software providers and specialized supply chain solution vconcludeors. Market players are focutilizing on developing AI-enabled planning platforms, enhancing cloud-native architectures, and expanding real-time analytics capabilities. Strategic partnerships, platform upgrades, and continuous innovation are shaping competitive dynamics across the region.

Prominent companies operating in the Europe supply chain management market include Oracle Corporation, IBM Corporation, Kinaxis, SAP SE, Wolters Kluwer N.V., Blue Yonder Group, Inc., Infor, o9 Solutions, Inc., Logility, and GainSystems, Inc.

Europe Supply Chain Management Market Size

The Europe supply chain management market reached USD 8.89 billion in 2025, is expected to grow to USD 9.85 billion in 2026, and is anticipated to touch USD 22.45 billion by 2034, at a CAGR of 10.84% from 2026 to 2034.

Supply Chain Management (SCM) is the centralized management of the entire flow of goods, services, data, and finances, from raw material sourcing to final product delivery. As of 2024, the European Union remains the primary driver of freight transport on the continent, with road transport maintaining its position as the dominant inland mode, while maritime shipping handles the largest volume overall. European seaports experienced a decrease in container traffic throughout 2023, reflecting a weaker economic environment and shifting trade routes, yet these ports remain crucial nodes requiring intense coordination for international trade. The integration of environmental mandates such as the Corporate Sustainability Reporting Directive has further compelled enterprises to embed transparency and traceability into their logistics ecosystems. The proliferation of EU enterprises and the high volume of cross-border trade have created resilient, adaptive, and data-driven supply chain solutions a strategic necessity. This operational reality defines the contemporary scope of the Europe supply chain management market, distinguishing it through regulatory rigor, operational complexity, and sustainability-driven transformation.

MARKET DRIVERS

Accelerated Adoption of Artificial Ininformigence and Predictive Analytics

European enterprises are increasingly deploying artificial ininformigence and predictive analytics to enhance supply chain visibility, resilience, and responsiveness, which acts as a major driver of the Europe supply chain management market. Large European enterprises are increasingly incorporating artificial ininformigence into their operational processes, with supply chain management emerging as a key application area. The integration of these technologies is contributing to enhanced precision in forecasting demand, while manufacturing companies are adopting machine learning models to better anticipate potential disruptions and refine inventory management. Substantial funding is being directed toward accelerating the deployment of artificial ininformigence within crucial industrial and logistics networks. This strategic emphasis is reinforced by rising consumer expectations for delivery speed and product availability, with a notable share of European online shoppers expecting same-day or next-day delivery, as per a study. These dynamics collectively drive demand for ininformigent supply chain platforms capable of synthesizing real-time data from disparate sources to support proactive decision-building.

Stringent Regulatory Compliance and Sustainability Mandates

Regulatory imperatives across the region, particularly those related to environmental accountability and labour ethics, are compelling organizations to overhaul traditional supply chain models, which contributes to the expansion of the Europe supply chain management market. New regulatory frameworks in Europe require companies to extconclude risk management deep into supply networks, focutilizing on environmental and social impacts. Observations indicate that a large portion of a company’s environmental impact originates within supply chains rather than direct operations, driving a necessary for broader visibility. Upcoming waste management regulations incentivize increased supplier cooperation to improve material recyclability and traceability. Organizations operating within the European market are intensifying their focus on supply chain transparency to align with stricter compliance requirements. France’s Anti-Waste for a Circular Economy Law further illustrates national-level stringency requiring detailed disclosure of product repairability and material origin. These regulatory currents are not merely administrative burdens but active market shapers that elevate the strategic importance of integrated supply chain management systems capable of real-time compliance monitoring and sustainability reporting.

MARKET RESTRAINTS

Fragmented Cross-Border Regulatory and Customs Frameworks

Persistent disparities in national customs, procedures, tax regimes, and documentation requirements continue to impede seamless supply chain operations, despite the European Union’s single market vision, and the growth of the Europe supply chain management market. Variations in administrative procedures at internal borders contribute to delays in road freight, particularly impacting routes through specific regions. Diverse interpretations of customs regulations across member states have created numerous procedural differences. These regulatory inconsistencies result in operational stoppages during cross-border transits. Moreover, the departure of the United Kingdom from the European Union has added complexity to trade, leading to increased documentation requirements for shipments. Such fragmentation escalates operational costs, increases error rates, and discourages tiny and medium enterprises from engaging in cross-border commerce, thereby constraining market fluidity and scalability for supply chain management solutions.

Persistent Shortage of Skilled Logistics and Digital Integration Talent

The effective implementation of advanced SCM systems across the region is increasingly constrained by a critical deficit of professionals skilled in both logistics operations and digital integration. This poses a serious restraint to the Europe supply chain management market. The logistics sector is experiencing a shortage of workers possessing necessary digital competencies, including data analytics, IoT configuration, and enterprise resource planning. Logistics managers are encountering challenges in recruiting personnel capable of navigating and operating modern cloud-based supply chain platforms. An aging workforce, with a substantial portion nearing retirement age, is creating a looming talent shortage, as the influx of new personnel is not keeping pace with departing employees. Positions requiring specialized analytical skills in the supply chain sector are remaining vacant for extconcludeed periods compared to other industrial roles. Educational institutions are gradually adapting, with specialized degrees in digital supply chain management still being a limited offering. Consequently, organizations delay or scale back technology deployments not due to lack of capital or strategy but due to the absence of human capacity to operationalize these systems effectively.

MARKET OPPORTUNITIES

Integration of Circular Supply Chain Models

The transition toward circular economy principles provides a major opening for the Europe supply chain management market. This shift is achieved by redefining product lifecycles and value recovery mechanisms. The European Commission’s Circular Economy Action Plan tarreceives a reduction in municipal waste by 2030 and a doubling of circular material utilize by 2035, creating systemic demand for reverse logistics infrastructure and closed-loop coordination. Transitioning toward a circular economy holds the potential to reduce material expconcludeitures for businesses by reconfiguring supply chains. Digital tracking technologies are facilitating increased product returns and component reutilize, allowing for certified take-back programs to become more common among electronics retailers in specific markets. Extconcludeed producer responsibility frameworks, which require coordination between retailers, recyclers, and material suppliers, are enabling higher rates of packaging recovery and reutilize in manufacturing processes. These developments necessitate supply chain platforms that manage bidirectional flows, coordinate with third-party refurbishers, and validate material provenance, all of which expand the functional scope and market potential of next-generation supply chain management solutions.

Expansion of Regionalized and Nearshored Manufacturing Networks

Geopolitical volatility and pandemic-induced disruptions have enabled a strategic shift toward regionalized production hubs within the region by reducing depconcludeency on distant suppliers and enhancing supply chain agility, which offers fresh prospects for the Europe supply chain management market. Many European manufacturers are transitioning production closer to their final markets, with notable activity in sectors such as automotive, electronics, and pharmaceuticals. Specific countries in Central and Eastern Europe are becoming key industrial hubs, attracting significant foreign investment for new facilities. This shift toward regional sourcing is prompting companies to increase their investments in localized logistics, including warehoutilize automation and supplier collaboration tools. Regional policy initiatives are encouraging the development of localized microelectronics manufacturing, fostering more integrated supply ecosystems. Such regional networks require granular demand sensing, localized inventory optimization, and multi-tier supplier visibility, all of which elevate the strategic relevance and functional complexity of supply chain management systems tailored to European industrial geography.

MARKET CHALLENGES

Cybersecurity Vulnerabilities in Digitally Integrated Logistics Networks

The deep digitization of European supply chains has significantly expanded the attack surface for cyber threats, with logistics platforms now serving as high-value tarreceives for data theft and operational sabotage, which inhibits the growth of the Europe supply chain management market. Logistics organizations across Europe are experiencing a high frequency of significant cybersecurity incidents, resulting in considerable financial impact. The integration of cloud-based management systems and connected warehoutilize infrastructure increases systemic risk and operational interdepconcludeencies, often cautilizing significant disruptions to cargo flows. Third-party software providers, including API integrations and supplier portals, represent a significant vector for breaches, while a substantial portion of tinyer firms have not fully implemented mandated security protocols. These vulnerabilities undermine stakeholder trust, delay digital adoption, and necessitate costly security retrofitting, thereby constraining the scalability of integrated supply chain management architectures.

Energy Price Volatility and Decarbonization Pressures on Logistics Operations

The ongoing energy transition in the region has introduced acute cost instability and operational complexity into transportation and warehoutilizing functions, which directly impacts the supply chain economics and the expansion of the Europe supply chain management market. Elevated energy costs in certain regions, in contrast to lower-priced areas, are cautilizing logistics operators to re-examine their warehoutilize placement and transportation routes. Mandated emissions reductions in transport are pushing companies to accelerate the adoption of electric vehicles, even while supporting infrastructure remains underdeveloped. A limited number of operational charging stations for heavy-duty electric vehicles, particularly along major transport networks, is creating operational bottlenecks and concerns regarding range limitations. The increased energy demands of refrigeration systems, combined with current grid conditions, are placing additional pressure on cold chain operators. These intersecting pressures force trade-offs between cost control, sustainability compliance, and service reliability, presenting a multifaceted operational challenge that conventional supply chain models are ill-equipped to resolve.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Segments Covered |

By Module, Deployment, Enterprise Size, Indusattempt, and Counattempt. |

|

Various Analyses Covered |

Global, Regional, and Counattempt-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

|

Market Leaders Profiled |

Oracle Corporation, IBM Corporation, Kinaxis, SAP SE, Wolters Kluwer N.V., Blue Yonder Group, Inc., Infor, o9 Solutions, Inc., Logility, GainSystems, Inc., and Others. |

SEGMENTAL ANALYSIS

By Module Insights

The warehoutilize management system segment captured the majority share of 28.1% of the Europe supply chain management market in 2025. The prominence of the warehoutilize management system segment is primarily attributed to the escalating complexity of inventory handling within e-commerce fulfillment centers and industrial distribution hubs. European retailers are increasingly adopting unified commerce strategies that require integrated, real-time inventory visibility, driving reliance on advanced warehoutilize management platforms. Logistics hubs are experiencing a surge in automated fulfillment solutions to meet demand for error-free order processing, while new sustainability mandates are pushing operators to adopt ininformigent management systems that track energy consumption on a per-unit basis. These systems reduce picking errors and improve space utilization, according to a study. As urban last-mile delivery pressures intensify, particularly in cities like Paris and Amsterdam, warehoutilize efficiency has become a strategic linchpin, building WMS the cornerstone of modern European supply chain architecture.

The transportation management system segment is likely to experience the rapidest CAGR of 13.2% from 2026 to 2034 due to intensifying regulatory and cost pressures on freight shiftment across the continent. The significant contribution of road freight to regional transport emissions is driving logistics providers to adopt transportation management systems that feature carbon calculation and route optimization capabilities. Regulatory mandates for real-time load matching across borders are accelerating the adoption of these systems among mid-sized carriers, while fluctuating fuel costs are increasing the importance of dynamic carrier selection and shipment consolidation. Additionally, the inclusion of cross-border documentation modules has transformed these systems from a tactical tool into a compliance necessity, with utilizers experiencing notable reductions in freight costs. France’s Ecotaxe revision and Germany’s nationwide tolling system for commercial vehicles have also necessitated granular cost tracking functionalities that only advanced TMS platforms can deliver, building this segment the most dynamically evolving in the European landscape.

By Deployment Insights

The cloud-based deployment segment led the Europe supply chain management market by holding a 64.5% share in 2025. The supremacy of the cloud-based deployment segment is credited to scalability, cost efficiency, and rapid integration capabilities. European enterprises are increasingly adopting a cloud-first approach for operational software, with supply chain platforms frequently leading this transition. Initiatives promoting secure, federated infrastructure have enhanced trust in regional cloud providers while addressing data sovereignty concerns. Cloud-based supply chain solutions often achieve operational readiness rapider than on-premise alternatives, allowing companies to respond more rapidly to sudden disruptions. Furthermore, cloud platforms facilitate improved collaboration across multi-tier supplier networks, enabling closer coordination within unified ecosystems. The subscription-based model aligns with capital conservation efforts, as financial leaders prioritize operational expconcludeiture flexibility.

The cloud deployment segment is also the rapidest-growing segment, with a projected CAGR of 14.1% during the forecast period, owing to converging technological policy and behavioral shifts across European businesses. New regulatory requirements in Europe are compelling critical infrastructure providers to adopt advanced monitoring and data protection measures, often leading them toward specialized cloud solutions. Data management providers are increasingly offering localized storage options, which assist organizations align with both stringent privacy regulations and cybersecurity mandates simultaneously. Logistics and supply chain companies are shifting toward modular, API-driven architectures, allowing them to integrate various specialized software applications. The trconclude toward composable, flexible systems is driving adoption of cloud-based supply chain tools, enabling firms to customize their operational technology. The war in Ukraine and subsequent energy disruptions further exposed the fragility of legacy on-premises systems, prompting governments like Sweden and the Netherlands to allocate national digital resilience grants specifically for cloud migration in logistics. These structural tailwinds ensure cloud deployment remains both the present standard and future trajectory of supply chain digitization in Europe.

By Enterprise Size Insights

The large enterprises segment dominated the Europe supply chain management market by accounting for a 61.7% share in 2025. The dominance of the large enterprises segment is driven by its complex multi-tier global operations and compliance obligations. Large-scale European enterprises represent a tiny fraction of businesses yet generate a significant portion of non-financial sector value, driving the necessary for advanced supply chain management investments. These multinational corporations manage expansive, global networks requiring integrated platforms to align procurement, production, logistics, and sustainability. In response to ongoing disruptions, many of these firms have implemented comprehensive, real-time, conclude-to-conclude supply chain monitoring systems. Furthermore, regulatory requirements compel large organizations to adopt traceability tools that monitor labor practices, emissions, and material flows throughout their supplier networks. The significant investment in supply chain software by these firms reflects the high cost of managing complex, large-scale operations and meeting regulatory demands that differ from those of tinyer companies.

The tiny and medium enterprises (SMEs) segment is expected to exhibit a noteworthy CAGR of 15.3% from 2026 to 2034. The rapid expansion of the SMEs segment is propelled by digital accessibility policy support and competitive necessity. Public funding initiatives in Europe are actively supporting the integration of digital tools within tinyer enterprises, with a notable focus on supply chain management technologies. The market for supply chain software has adjusted to offer more affordable, enattempt-level, cloud-based options, allowing tinyer businesses to access advanced functional capabilities that were previously associated with larger corporations. The adoption of digital supply chain tools by manufacturing and retail businesses is increasingly driven by the necessary to meet the visibility and operational requirements set by major purchasing partners. National initiatives in certain European regions are actively facilitating access to training and software for tinyer enterprises, accelerating the adoption of digital tools. SMEs face rising sales losses in cross-border e-commerce due to manual processes, with many struggling with shipping delays and stockouts before adopting SCM, finds a European Retail Roundtable study. This operational urgency, combined with financial and technical support, is fueling unprecedented SME engagement in supply chain digitization.

By Indusattempt Insights

The discrete manufacturing indusattempt segment was the largest segment in the Europe supply chain management market by occupying a 44.3% share in 2025. The leading position of the discrete manufacturing indusattempt segment is supported by its intricate bill of materials, complex assembly lines, and high customization demands. Automotive, aerospace, and industrial machinery sectors, core components of discrete manufacturing, require real-time synchronization between engineering, procurement, and logistics functions. The high volume of individual components within European passenger vehicles requires sophisticated supply chain management systems to facilitate just-in-time delivery. German automotive manufacturers rely on an extensive number of certified supply chain platforms to manage supplier lead times and integrate with Tier 1 and Tier 2 networks. New European regulations concerning battery components necessitate that manufacturers adopt blockchain-enabled traceability to track the provenance of raw materials. The utilize of integrated supply chain suites in manufacturing is associated with reduced production downtime and improved on-time delivery. The shift toward electric and connected vehicles further intensifies data exmodify necessarys, building SCM not just operational infrastructure but a strategic enabler of industrial transformation.

The process indusattempt segment is predicted to witness the highest CAGR of 12.8% over the forecast period. The swift growth of the process indusattempt segment is fuelled by stringent product integrity regulations and batch traceability requirements. Pharmaceuticals, food and beverage, and specialty chemicals, key verticals within process manufacturing, are subject to rigorous EU mandates, including the Falsified Medicines Directive and Novel Foods Regulation, which demand conclude-to-conclude digital batch records. European pharmaceutical manufacturers are updating supply chain management systems to meet regulatory tracking requirements. Major food producers are investing in real-time monitoring technologies to address document-related gaps and enhance the safety of perishable goods. In the chemical sector, REACH compliance requires detailed substance disclosure across hundreds of formulations, building SCM systems essential for regulatory submission automation. Non-neobtainediable demands for safety and green practices are pushing industries to digitize their operations, triggering an unprecedented wave of SCM adoption.

COUNTRY-LEVEL ANALYSIS

Germany Supply Chain Management Market Analysis

Germany outperformed other countries in the Europe supply chain management market by holding a 22.5% share in 2025. The prominence of the German market is credited to a dense industrial base, advanced logistics infrastructure, and early adoption of Indusattempt 4.0 principles. The national logistics landscape is characterized by a high volume of service providers operating within the market. Software expconcludeitures for supply chain management are notably concentrated within specific industrial sectors, particularly automotive and mechanical engineering. Government-sponsored digital initiatives have encouraged the adoption of internet-connected technologies and artificial ininformigence in supply chain operations. The counattempt’s geographical position serves as a central hub for cross-border freight shiftment, emphasizing the importance of logistics efficiency. Large-scale manufacturing firms display a high adoption rate for real-time tracking systems, supported by broader national initiatives aimed at digitizing tiny and medium-sized enterprise supply chains.

France Supply Chain Management Market Analysis

France followed closely in the Europe supply chain management market by capturing a 15.6% share in 2025. The expansion of the French market is driven by its strategic investments in green logistics and digital sovereignty. National industrial modernization initiatives are channeling funding toward upgrading logistics infrastructure, focutilizing on smart storage facilities and reduced-emission transport routes. The concentration of high-conclude consumer goods companies in the capital region necessitates advanced supply chain management techniques, including secure tracking systems for authenticity and specialized inventory management. The domestic logistics indusattempt has demonstrated resilience and growth, driven by the rapid adoption of new supply chain technologies across key sectors like retail and aerospace. A government certification program for digital service providers is increasing trust and security for enterprises integrating advanced logistics software. Key maritime, port, and rail infrastructure developments are facilitating a shift toward more sustainable and digitized logistical operations.

United Kingdom Supply Chain Management Market Analysis

The United Kingdom is another key player in the Europe supply chain management market due to its advanced e-commerce penetration and post Brexit supply chain restructuring. The high proportion of online shopping in the UK retail market highlights a necessary for adaptable supply chain systems that can handle fluctuating inventory levels and efficient last-mile delivery. Increased border documentation following the departure from the EU has prompted UK businesses to adopt supply chain management platforms with built-in customs compliance capabilities. London functions as a central hub for supply chain technology, with numerous specialized firms providing embedded trade finance and risk analytics. Centralized purchasing of medical supplies within the public health sector has driven the modernization of supply chain management through the utilize of AI-powered demand forecasting. Despite economic volatility, the UK’s market is characterized by high digital maturity and regulatory adaptation, building it a key innovation laboratory for next-generation SCM.

Italy Supply Chain Management Market Analysis

Italy grew steadily in the Europe supply chain management market owing to its strong manufacturing heritage and recent national digitization push. The Italian supply chain landscape is dominated by tiny family-owned enterprises in fashion machinery and food processing, which are now rapidly adopting cloud SCM under the Impresa 4.0 tax credit scheme that reimburses a notable share of software. The high volume of seasonal collections in major fashion hubs necessitates supply chain management systems capable of handling rapid shifts in demand and tight production schedules. While national logistics productivity has historically lagged behind regional averages, the adoption of digital supply chain tools has demonstrably enhanced warehoutilize efficiency in specific test regions. The substantial activity at major Mediterranean transshipment hubs drives the necessary for integrated digital systems connecting port operations. The prevalence of tiny and medium-sized enterprises dictates that market growth depconcludes on the availability of scalable, cost-effective supply chain solutions tailored to artisanal and mid-scale production models.

Netherlands Supply Chain Management Market Analysis

The Netherlands is predicted to expand in the Europe supply chain management market from 2026 to 2034 due to its role as Europe’s logistics gateway and digital innovation leader. The port in Rotterdam serves as a major European logistics hub that actively tests advanced, automated, and digital supply chain management technologies. Amsterdam’s airport functions as a significant cargo center, specializing in the secure and temperature-controlled handling of high-value goods like pharmaceuticals and electronics. National initiatives in the Netherlands have established shared, standardized data exmodify systems, improving connectivity across a large number of companies involved in logistics. A substantial portion of Dutch logistics firms have adopted real-time tracking dashboards to monitor operations. Logistics companies in the region are increasingly utilizing shared inventory systems to optimize resource efficiency. The counattempt’s flat geography, high rail freight usage, and dense distribution networks create it an ideal environment for SCM optimization with sustainability KPIs embedded into every tier of the supply chain ecosystem.

COMPETITIVE LANDSCAPE

Competition in the Europe supply chain management market is intense and multidimensional, characterized by rapid technological differentiation, regulatory adaptation, and strategic ecosystem building. Vconcludeors compete not only on functionality but also on compliance readiness, sustainability integration, and deployment agility. The presence of both global software giants and specialized European providers creates a dynamic where scalability meets local regulatory nuance. Innovation cycles have accelerated with quarterly AI feature rollouts now common. Customer loyalty hinges on a provider’s ability to deliver real-time risk mitigation, carbon tracking, and seamless cross-border data exmodify. Mergers and partnerships are frequent as companies seek to consolidate capabilities in warehoutilizing, transportation, and ethical sourcing. This environment favors players that combine deep indusattempt expertise with modular cloud architectures, enabling tailored yet future-proof supply chain solutions across diverse European economies.

KEY MARKET PLAYERS

The leading companies operating in the Europe supply chain management market include:

- Oracle Corporation

- IBM Corporation

- Kinaxis

- SAP SE

- Wolters Kluwer N.V.

- Blue Yonder Group, Inc.

- Infor

- o9 Solutions, Inc.

- Logility

- GainSystems, Inc.

TOP PLAYERS IN THE MARKET

- SAP SE is a pivotal force in the Europe supply chain management market, offering integrated solutions that span procurement, logistics, and sustainability tracking. Headquartered in Germany, the company leverages its deep roots in European industrial ecosystems to deliver tailored SCM suites aligned with EU regulatory frameworks. In recent years, SAP has intensified its focus on ininformigent automation, launching the SAP Integrated Business Planning platform with embedded AI for real-time demand sensing. The company also expanded its partnership with Deutsche Bahn to digitize rail-based freight coordination, enhancing multimodal logistics capabilities across Central Europe. These initiatives reinforce SAP’s strategic alignment with Europe’s decarbonization and resilience priorities.

- Oracle Corporation plays a critical role in shaping digital supply networks across Europe through its cloud native SCM applications. The company’s Fusion Cloud Supply Chain Planning suite is widely adopted by pharmaceutical and automotive enterprises for its advanced scenario modeling and risk analytics. Oracle recently strengthened its European footprint by opening a dedicated supply chain innovation lab in Paris focutilized on circular economy integrations and regulatory compliance automation. It also deepened collaboration with major retailers to embed ESG metrics into procurement workflows. These actions position Oracle as a key enabler of sustainable and responsive supply chains tailored to Europe’s evolving policy landscape.

- Infor delivers indusattempt-specific supply chain solutions that address the nuanced requirements of European discrete and process manufacturers. Its CloudSuite Industrial and CloudSuite Fashion platforms are engineered for complex production environments and rapid-paced consumer cycles prevalent in Italy, Germany, and the Benelux region. Infor recently enhanced its Coleman AI engine to support dynamic rerouting during geopolitical disruptions and launched a carbon footprint module compliant with the EU Corporate Sustainability Reporting Directive. The company also forged a strategic alliance with PostNL to optimize last-mile delivery data flows. These shifts demonstrate Infor’s commitment to embedding agility and compliance into European supply chain operations.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe supply chain management market primarily pursue product innovation through artificial ininformigence and machine learning integration to enhance predictive capabilities. They actively form strategic alliances with logistics providers, national rail operators, and port authorities to enable conclude-to-conclude visibility across multimodal networks. Expansion of cloud-based offerings tailored to European data sovereignty and sustainability regulations is another core strategy. Companies also invest in regional innovation hubs to co-develop solutions with local enterprises and public agencies. Additionally, they embed environmental, social, and governance metrics directly into procurement and logistics workflows to align with EU mandates and customer expectations. These approaches collectively strengthen market relevance, resilience, and regulatory alignment.

MARKET SEGMENTATION

This research report on the Europe supply chain management market has been segmented and sub-segmented into the following categories.

By Module

- Transportation Management System

- Warehoutilize Management System

- Sourcing and Procurement

- Manufacturing

- Inventory Management Software

- Others (Order Management)

By Deployment

By Enterprise Size

- Small & Medium-sized Enterprises (SMEs)

- Large Enterprise

By Indusattempt

By Counattempt

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe