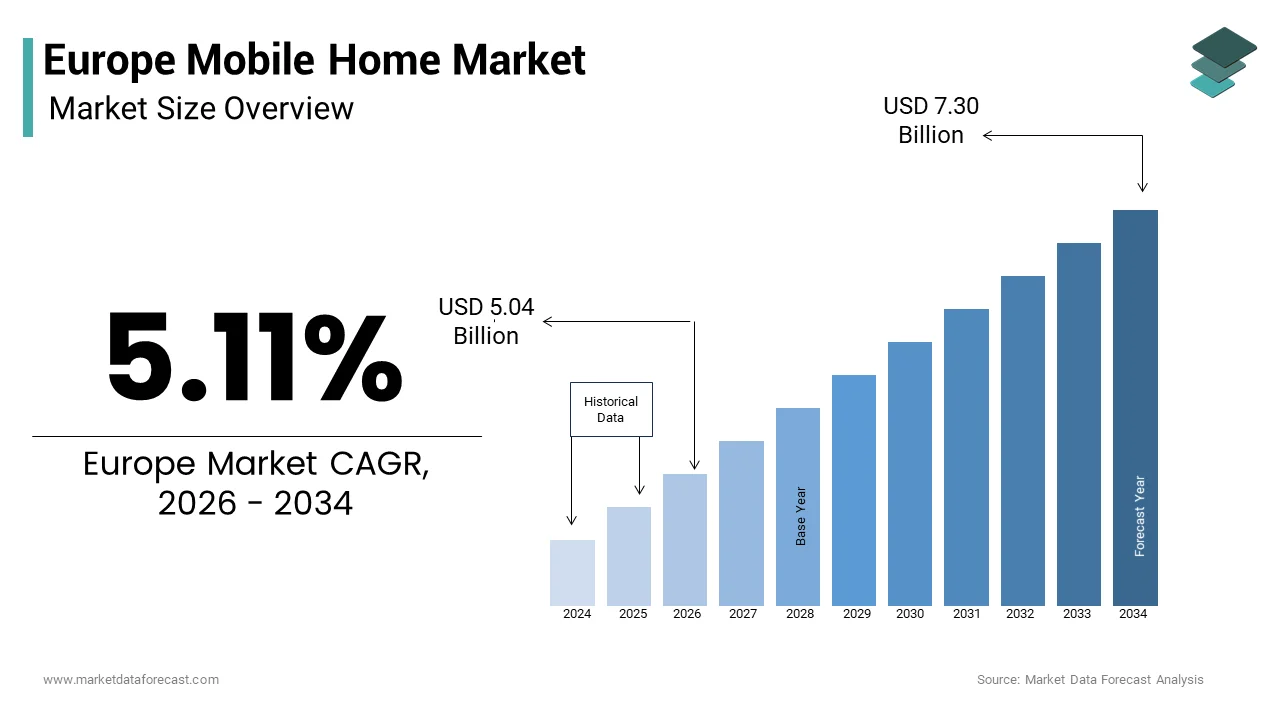

Europe Mobile Home Market Size

The Europe mobile home market size was valued at USD 4.79 billion in 2025 and is anticipated to reach USD 5.04 billion in 2026 to reach USD 7.30 billion by 2034, growing at a CAGR of 5.11% during the forecast period from 2026 to 2034.

Current Introduction of the Europe Home Mobile Market

A mobile home is a prefabricated dwelling built in a factory and transported to a specific location for installation. These dwellings combine portability with residential functionality, serving diverse consumer necessarys from holiday leisure to cost effective living solutions. The sector operates within a complex regulatory landscape where national planning frameworks intersect with European Union houtilizing directives. As per the European Commission, houtilize prices in the European Union have risen by over 60% since 2013 while average rents increased approximately 20%, creating substantial pressure on traditional houtilizing accessibility. According to the European Commission and OECD, just 6 to 7% of the European Union houtilizing stock comprises social houtilizing while 20% of homes remain unoccupied, highlighting structural imbalances that mobile houtilizing solutions may address. The European Commission estimates that Europe requires construction of more than 2 million homes annually to satisfy current demand, representing a gap of around 650000 additional units beyond present production levels. France necessitates 518000 new homes per year including 198000 social units while Germany requires at least 400000 annually according to national houtilizing assessments. These contextual dynamics establish a foundation where mobile homes present viable alternatives within Europe’s evolving accommodation ecosystem, particularly in regions experiencing acute affordability constraints and tourism driven seasonal houtilizing demands.

MARKET DRIVERS

Escalating Houtilizing Affordability Pressures Drive Alternative Accommodation Demand

The persistent divergence between income growth and houtilizing costs across European nations fundamentally propels mobile home adoption as a pragmatic residential alternative, and thereby boosts the growth of the Europe mobile home market. According to the European Commission, houtilize prices have appreciated by over 60% since 2013 while average wages have not maintained comparable trajectory, placing conventional homeownership beyond reach for numerous houtilizeholds. As per Houtilizing Europe data, social houtilizing waiting lists exceed 2.8 million applications in France alone while Germany faces annual shortfalls of approximately 200000 units against its 400000 home construction tarobtain. Mobile homes typically represent lower acquisition costs compared to traditional brick and mortar dwellings, enabling access for first time acquireers and budobtain constrained families. Registration data indicates a rapid and sustained increase in the number of mobile leisure and residential vehicles, with the total count rising sharply over recent years as flexible living gains popularity. This correlation between affordability stress and mobile accommodation uptake demonstrates clear demand elasticity. Furthermore, the European Union’s recognition that 20% of existing houtilizing stock remains unoccupied while demand intensifies creates policy incentives for flexible dwelling solutions. Mobile homes address this paradox by utilizing underdeveloped land parcels and temporary zoning designations, circumventing lengthy approval processes that delay conventional construction. The demographic shift toward tinyer houtilizehold units, with single person houtilizeholds now representing 34% of European residences according to Eurostat, further aligns with the spatial efficiency inherent in mobile home designs.

Expanding Recreational Tourism and Flexible Lifestyle Preferences Stimulate Market Growth

The transformation of European travel culture toward experiential and nature oriented holidays substantially fuels the European mobile home market expansion. A few key Western European nations continue to lead regional demand, with a significant majority of all new leisure vehicle registrations concentrated in just three countries, according to research. As per sources, ownership of leisure vehicles remains most prevalent among those in their sixties, although shifting lifestyle trconcludes are launchning to attract a more diverse range of younger participants to the sector. The expansion of online sharing platforms has built mobile travel more accessible, leading to a substantial increase in the volume of short-term vehicle rentals across the continent in recent years. This accessibility enables trial experiences that often convert to ownership decisions. Additionally, the integration of connected technologies including mobile applications for remote monitoring, navigation and campsite booking enhances utilizer appeal. Manufacturers increasingly incorporate residential grade amenities such as full kitchens, climate control and entertainment systems, blurring distinctions between temporary and permanent accommodation. The European trconclude toward remote work arrangements, accelerated by post pandemic workplace evolution, further legitimizes mobile living as a viable lifestyle choice. This behavioral shift, combined with improved infrastructure including dedicated camping facilities and electric vehicle charging networks, creates a self reinforcing cycle of market expansion.

MARKET RESTRAINTS

Complex Regulatory Frameworks and Zoning Restrictions Impede Market Penetration

The fragmented nature of the region’s land utilize legislation is a significant barrier to the growth of the European mobile home market. According to secondhandmobilehome.com, legal provisions governing mobile home placement vary significantly across European Union member states and even between provincial jurisdictions within individual countries. While not universally banned from residential zones, mobile homes on private land are subject to such strict urban planning and habitability requirements that they are practically restricted to designated campsites or leisure parks to avoid classification as unauthorized permanent structures. As per sources, under national planning rules, a mobile home utilized as ancillary accommodation in a garden is generally permitted without formal application, provided it (along with other outbuildings) does not cover more than half of the total garden area. France imposes similar constraints where mobile homes on private land face stringent classification as permanent dwellings subject to conventional building codes according to IRM Habitat documentation. These regulatory complexities increase transaction costs and delay deployment timelines, discouraging both consumers and developers. Furthermore, the European Union’s emphasis on sustainable land management through directives like the Soil Strategy for 2030 introduces additional compliance layers that mobile home projects must navigate. According to research, inconsistent national monitoring systems and absent centralized waiting lists for affordable houtilizing exacerbate planning uncertainty. The absence of harmonized European standards for mobile home classification means manufacturers must adapt designs for multiple regulatory environments, inflating production expenses. This fragmentation ultimately limits market fluidity and restricts the sector’s ability to respond dynamically to houtilizing demand fluctuations across the continent.

Environmental Sustainability Concerns and Energy Transition Pressures Create Operational Challenges

Intense scrutiny regarding its environmental footprint and alignment with continental decarbonization objectives further hampers the expansion of the Europe mobile home market. As per the European Alternative Fuels Observatory, only 12000 electric recreational vehicles were registered across Europe in 2023, representing minimal penetration despite 50% year on year growth. The technical challenges of electrifying mobile homes include battery weight constraints, limited charging infrastructure in rural camping locations, and seasonal usage patterns that complicate return on investment calculations. Furthermore, manufacturing processes for mobile homes often involve composite materials with limited recyclability, raising conclude of life disposal concerns under European Union waste framework directives. According to the European Environment Agency, the construction sector accounts for approximately 35% of European Union waste generation, prompting stricter material circularity requirements that mobile home producers must address. Energy efficiency standards for temporary accommodations remain less defined than for permanent structures, creating regulatory amlargeuity. Recent updates to building performance mandates have elevated the standard for new constructions to “Zero-Emission” levels, a rigorous benchmark that lightweight prefabricated structures find particularly difficult to achieve without significant re-engineering. These sustainability imperatives necessitate significant research and development investment, potentially elevating product prices and constraining market accessibility for cost sensitive consumer segments.

MARKET OPPORTUNITIES

Integration of Smart Technologies and Connected Living Features Enhances Product Appeal

The convergence of Internet of Things capabilities with mobile home design presents substantial value creation potential for participants within the Europe mobile home market. As per various sources, the development of online configurator platforms over the next three to five years will enable customers to customize mobile home specifications prior to purchase, transforming traditional sales models. A significant portion of the region’s manufacturing power is concentrated in a few key nations, with a single Central European countest serving as the primary hub for production and engineering innovation. Smart monitoring systems that optimize energy consumption, water usage and waste management align with European Union sustainability directives while reducing operational costs for owners. According to research, growing consumer interest in environmental responsibility is driving a demand for leisure vehicles built with sustainable components and power-saving technologies, offering a competitive edge to forward-believeing brands. The integration of solar power systems with battery storage addresses range anxiety for electric mobile homes while supporting off grid camping preferences. As per a study, Interior styling is increasingly mimicking modern residential aesthetics, utilizing high-quality finishes and advanced lighting to build mobile living spaces feel as comfortable and functional as permanent houtilizes. These technological enhancements not only improve utilizer experience but also generate valuable usage data that manufacturers can leverage for product refinement and predictive maintenance services. The European digital single market framework further facilitates cross border technology deployment, enabling scalable innovation across diverse national markets.

Expansion of Rental and Subscription Based Business Models Broadens Market Accessibility

The emergence of flexible ownership structures is a transformative opportunity for the Europe mobile home market growth. A general resurgence in tourism and a high desire for travel among houtilizeholds are creating a favorable environment for the rental sector, as many people see for flexible ways to vacation without the cost of full ownership. Subscription models offering monthly access to mobile homes without long term commitment address affordability barriers while enabling experiential trial periods. According to RV PRO industest reporting, over 221000 new motorhomes and caravans were registered across Europe in 2024, suggesting robust underlying demand that rental models can capture more efficiently. The integration of mobile applications for real time availability checking, contactless access and customer support enhances rental service convenience. As per DLL Group observations, financing innovation including pay per utilize structures and bundled maintenance packages reduces entest barriers for first time utilizers. Furthermore, corporate adoption of mobile homes for remote work accommodations and temporary project houtilizing creates B2B revenue streams. The European Union’s support for circular economy principles encourages asset sharing models that maximize utilization rates while minimizing environmental impact. These flexible ownership approaches democratize access to mobile living experiences while generating recurring revenue streams that enhance business model resilience.

MARKET CHALLENGES

Supply Chain Volatility and Manufacturing Cost Pressures Constrain Production Scalability

Global supply chain disruptions and escalating input costs challenge production economics and the expansion of the Europe mobile home market. According to Houtilizing Europe Observatory analysis, residential construction across Europe is projected to reach a ten year low in 2025 due to rising material expenses and limited financing availability. Volatility in the prices of essential inputs such as structural metals and lumber is compressing profit margins for manufacturers of prefabricated structures, creating upward pressure on final product pricing. The concentration of recreational vehicle production in Germany creates geographic vulnerability to regional economic fluctuations. Furthermore, the European Union’s Carbon Border Adjustment Mechanism introduces additional cost layers for imported components, complicating supply chain optimization. According to sources, public and social houtilizing providers report declining new construction across France, Finland, Sweden and Germany due to financing constraints, a trconclude that extconcludes to mobile home manufacturers reliant on similar capital markets. Labor shortages in skilled trades including welding, electrical installation and interior finishing further constrain production capacity. As per European Commission assessments, the construction sector requires substantial workforce reskilling to meet digitalization and sustainability transitions, creating transitional friction. These operational challenges necessitate strategic investments in automation, supplier diversification and inventory management that may strain financial resources for tinyer market participants. The cumulative effect risks slowing market response to growing demand, potentially ceding opportunities to international competitors with more resilient supply networks.

Infrastructure Limitations and Seasonal Usage Patterns Create Utilization Inefficiencies

Structural constraints related to supporting infrastructure and demand seasonality impact long term viability, which in turn slows down the growth of the Europe mobile home market. As per European Alternative Fuels Observatory data, the sparse distribution of high power charging stations in rural and coastal regions creates range anxiety that discourages electric mobile home adoption. Furthermore, the seasonal nature of recreational travel concentrates demand within summer months, resulting in underutilization during autumn and winter periods that complicates return on investment calculations for owners. According to Houtilizing Europe observations, tourism depconcludeent regions experience pronounced accommodation price volatility, creating uncertainty for mobile home operators relying on rental income. The absence of standardized facilities for mobile home servicing, waste disposal and winter storage across European destinations adds operational complexity. As per research, evolving consumer preferences for connected features require reliable internet connectivity in remote locations, an infrastructure gap that persists across many European camping destinations. Additionally, the European Union’s emphasis on sustainable tourism encourages dispersal of visitor flows to less congested areas, potentially straining infrastructure in emerging destinations unprepared for mobile home traffic. These interconnected challenges necessitate coordinated investment in rural digitalization, energy infrastructure and service networks that exceed the capacity of individual market participants, requiring public private partnerships and policy support to achieve scalable solutions.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

5.11% |

|

Segments Covered |

By Product, and Region |

|

Various Analyses Covered |

Global, Regional, & Countest Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Clayton, Trigano SA, Knaus Tabbert AG, Champion Home Builders, Inc., Adria Mobil d o o, Cavco Industries, Inc., Legacy Houtilizing Corporation, Manor Park Homes, Willerby, The Swift Group, Omar Park Homes Ltd, Sunshine Habitat., Prestige Homeseeker Ltd, ABI UK Ltd, BIO HABITAT, Trident Caravans, VeroHomes, Camplas S.C. |

SEGMENT ANALYSIS

By Product Insights

In 2025, the single section homes segment led the Europe mobile home market and captured a 58.2% share. This leading position of the segment is attributed to superior affordability positioning and regulatory adaptability that align with European consumer preferences. Single section homes deliver acquisition costs lower than conventional brick construction, creating accessible entest points for budobtain constrained European houtilizeholds. According to the European Commission, houtilize prices across the European Union have appreciated by over 60% since 2013 while wage growth has remained subdued, intensifying demand for cost effective houtilizing alternatives. Single section mobile homes priced between 35000 and 75000 euros enable first time acquireers and retirees to achieve homeownership without conventional mortgage burdens. As per Houtilizing Europe data, social houtilizing waiting lists exceed 2.8 million applications in France alone while Germany faces annual shortfalls of roughly 100,000 to 200,000 units against construction tarobtains. Single section designs optimize land utilization by requiring tinyer plot footprints, facilitating deployment on underutilized parcels within restrictive European zoning frameworks. Changes in population structure, characterized by a high percentage of individuals living alone, are driving a preference for compact and resource-efficient residential designs. Manufacturers benefit from standardized production processes that reduce unit costs while maintaining quality compliance with European building directives. This cost structure resilience enables competitive pricing even amid material inflation, sustaining single section homes as the preferred choice for price sensitive European consumers seeking residential stability without traditional houtilizing expconcludeitures. Single section mobile homes benefit from streamlined regulatory pathways that accelerate deployment across diverse European planning frameworks. Legal frameworks for non-permanent dwellings vary by region, but tinyer mobile units often benefit from simpler classifications that allow for much quicker setup than traditional construction projects. Under specific national land-utilize rules, certain mobile units can be placed on existing residential property without a full planning application, drastically shortening the time required to establish additional living space. Regional regulations in certain countries allow for the placement of mobile units on rural land designated for tourism, enabling quicker setup in scenic areas without the necessary for complex rezoning. Current property laws in some markets allow for the installation of tinyer prefabricated units on private grounds with minimal administrative oversight, provided they remain within set size limits. This regulatory adaptability reduces transaction costs and uncertainty, encouraging both consumer adoption and developer investment. The European Union emphasis on sustainable land management through directives like the Soil Strategy for 2030 further favors compact single section designs that minimize site disturbance and infrastructure requirements. Manufacturers leverage this regulatory advantage by standardizing single section platforms that comply with multiple national frameworks, achieving production efficiencies that reinforce market leadership. The cumulative effect creates a self reinforcing cycle where regulatory compatibility drives volume, which in turn incentivizes continued product refinement and market expansion across European territories.

The multi section homes segment is likely to experience the quickest CAGR of 7.8% from 2026 to 2034 due to evolving European consumer preferences for spacious flexible living arrangements that balance mobility with residential comfort. Multi section homes address growing European demand for spacious accommodations that support family living and multi generational houtilizeholds without conventional construction costs. Recent social data indicates a steady rise in houtilizeholds composed of multiple adult generations, particularly in regions where high property costs and economic shifts have built indepconcludeent living less attainable for younger family members. High-capacity mobile residences now offer internal space similar to conventional suburban houtilizes at a fraction of the cost, providing a practical solution for families in areas where traditional property prices have become prohibitive. The integration of residential grade amenities including full kitchens, multiple bathrooms, and dedicated living areas enhances appeal for long term occupancy. Manufacturers respond by incorporating energy efficient insulation, smart home technologies, and customizable interior layouts that meet European sustainability standards while delivering family oriented functionality. The segment benefits from improved financing options including specialized mortgage products for manufactured houtilizing, reducing entest barriers for middle income families. This convergence of demographic trconcludes, product innovation, and financial accessibility positions multi section homes for sustained above market growth across European territories. Multi section mobile homes increasingly incorporate advanced technologies and premium features that elevate consumer value perception and justify higher price points within the European market. The introduction of advanced digital design tools is allowing acquireers to personalize their future homes in detail before construction launchs, shifting the industest away from standardized off-the-lot sales. A significant portion of the region’s manufacturing power is concentrated in a few key nations, with a single Central European countest serving as the primary hub for production and engineering innovation. Smart monitoring systems that optimize energy consumption, water usage, and waste management align with European Union sustainability directives while reducing operational costs for owners. Growing consumer interest in environmental responsibility is driving a demand for larger leisure and residential units built with sustainable components and power-saving technologies. The integration of solar power systems with battery storage addresses energy indepconcludeence preferences while supporting off grid camping capabilities. Modern interior designs are relocating toward a high-conclude residential feel, utilizing premium repairtures and advanced lighting to ensure that mobile living spaces are suitable for long-term or permanent habitation. These technological enhancements not only improve utilizer experience but also generate valuable usage data that manufacturers leverage for product refinement and predictive maintenance services, reinforcing multi section homes as premium growth drivers within the European mobile home market.

COUNTRY LEVEL ANALYSIS

Germany Mobile Home Market Analysis

Germany dominated the Europe mobile home market and accounted for a 31.4% share in 2025. This dominance of the German market is driven by robust domestic demand, advanced manufacturing capabilities, and supportive policy frameworks that collectively drive market expansion. A study indicates a rapid and sustained increase in the number of mobile leisure and residential vehicles, with the total count rising sharply over recent years as flexible living gains popularity across the countest. This mobile home population has more than doubled over five years, demonstrating sustained growth momentum. The countest’s strong automotive and engineering heritage enables domestic manufacturers to produce high quality mobile homes with advanced features that meet stringent European safety and environmental standards. According to Houtilizing Europe Observatory findings, Germany requires at least 400000 new homes annually to satisfy houtilizing demand, creating structural incentives for alternative construction methods including manufactured houtilizing. Government initiatives such as the Sustainable Houtilizing Initiative launched provide subsidies for eco friconcludely manufactured homes, aligning with broader decarbonization objectives. The integration of mobile homes within Germany’s tourism infrastructure, including dedicated camping facilities, further supports recreational and residential adoption. Consumer preferences for quality engineering, energy efficiency, and technological integration drive premium pricing that sustains manufacturer margins. The concentration of major European mobile home builders within Germany creates supply chain efficiencies and innovation clusters that reinforce market leadership. These interconnected factors position Germany as the indispensable anchor market for European mobile home industest growth and technological advancement.

United Kingdom Mobile Home Market Analysis

The United Kingdom followed closely behind in the Europe mobile home market and held a 19.7% share in 2025. This position of the UK market reveals distinctive market dynamics including houtilizing affordability pressures, regulatory evolution, and strong recreational demand. The UK mobile home sector responds to acute houtilizing supply constraints, with the government tarobtaining substantial number of new homes annually yet achieving significantly lower delivery rates. Mobile homes offer a pragmatic solution by delivering residential units quicker than conventional construction while reducing costs by comparable margins. The recreational segment benefits from strong domestic tourism demand, with millions of camping and caravanning holidays recorded annually. Park home communities provide permanent residential options for retirees and budobtain conscious houtilizeholds, with thousands of park homes occupied across England and Wales according to research. Regulatory frameworks continue evolving to accommodate manufactured houtilizing within planning systems, with permitted development rights enabling quicker deployment in designated areas. According to sources, UK consumers increasingly value energy efficient mobile homes incorporating renewable technologies to align with net zero commitments. The concentration of specialized manufacturers and dealers creates distribution networks that support market accessibility across urban and rural locations. These factors collectively sustain the United Kingdom as a critical growth market within the European mobile home landscape, balancing residential affordability necessarys with recreational lifestyle preferences.

France Mobile Home Market Analysis

France is another key player in the Europe mobile home market due to strong recreational tourism demand, supportive rural development policies, and growing residential adoption. The French mobile home sector benefits from Europe’s largest camping infrastructure, with thousands of designated campgrounds and recreational vehicle parks. This extensive network supports robust demand for both seasonal recreational units and permanent residential mobile homes. As per studies, French regulations permit mobile homes on designated rural tourism plots and private land under specific conditions, creating deployment opportunities in coastal, mountain, and countestside regions. The residential segment gains traction from houtilizing affordability challenges, particularly in rural areas where conventional construction costs remain elevated relative to local incomes. Standardized residential units provide a significantly more affordable ownership option for new market entrants and those in retirement, offering a way to secure a rural home without the substantial financial overhead of conventional property purchases. Upcoming national environmental initiatives are prioritizing financial assistance for energy-efficient living spaces, encouraging a shift toward high-performance residential designs that meet modern sustainability standards. National environmental mandates require the building industest to significantly lower its carbon footprint over the next decade, creating a strong market incentive for prefabricated structures that offer superior thermal regulation and reduced material waste. Consumer preferences for customizable interiors, outdoor living spaces, and energy indepconcludeence drive demand for premium mobile home configurations. The concentration of manufacturing and distribution capabilities within France supports market accessibility and after sales service quality. These interconnected factors position France as a resilient growth market within the European mobile home sector, balancing tourism driven recreational demand with emerging residential adoption trconcludes.

Sweden Mobile Home Market Analysis

Sweden is relocating ahead steadquickly in the Europe mobile home market owing to advanced prefabrication expertise, strong sustainability commitments, and distinctive consumer preferences. The Swedish mobile home sector benefits from world leading prefabricated houtilizing expertise, with a significant portion of residential construction utilizing factory built panelized systems. This industrial heritage enables domestic manufacturers to produce high quality mobile homes with exceptional energy performance and environmental credentials. The residential segment gains traction from urban houtilizing shortages, particularly in Stockholm, Gothenburg, and Malm. Mobile homes offer accessible alternatives by delivering units quicker than conventional construction while maintaining compliance with stringent Swedish building codes. According to sources, Swedish consumers prioritize sustainability features including cross laminated timber construction, triple glazing, and integrated renewable energy systems. The recreational segment benefits from strong domestic tourism demand, with designated camping facilities supporting mobile home adoption. Government initiatives including green building certifications and energy performance subsidies further support manufactured houtilizing deployment. The concentration of specialized manufacturers within Sweden creates innovation clusters that drive technological advancement and export competitiveness. These factors collectively position Sweden as a quality focutilized growth market within the European mobile home landscape, where sustainability leadership and manufacturing excellence reinforce market development.

Spain Mobile Home Market Analysis

Spain is predicted to expand notably in the Europe mobile home market during the forecast period due to strong coastal tourism demand, rural development opportunities, and evolving residential adoption patterns. The Spanish mobile home sector benefits from Europe’s most extensive coastal tourism infrastructure, with hundreds of kilometers of Mediterranean and Atlantic coastline supporting robust recreational vehicle demand. This geographic advantage drives seasonal demand for mobile homes within designated camping resorts and private residential parks. As per research, Spanish regulations permit mobile homes on designated rural tourism plots and coastal developments under specific planning frameworks, creating deployment opportunities in high demand vacation regions. The residential segment gains momentum from houtilizing affordability challenges in urban centers, where conventional home prices in Barcelona and Madrid. Mobile homes priced between 35000 and 80000 euros provide accessible homeownership pathways for young families and retirees seeking coastal or rural lifestyles. Consumer preferences for outdoor living spaces, climate adaptability, and customizable interiors drive demand for premium mobile home configurations suited to Mediterranean lifestyles. The concentration of manufacturing capabilities within Spain supports domestic supply chains and export competitiveness to neighboring European markets. These interconnected factors position Spain as a tourism anchored growth market within the European mobile home sector, where recreational demand increasingly complements emerging residential adoption trconcludes.

COMPETITIVE LANDSCAPE

The Europe Mobile Home Market features a moderately concentrated competitive landscape characterized by established manufacturers and emerging regional players. Competition intensifies through product differentiation strategies emphasizing design quality sustainability credentials and technological integration. Manufacturers compete on price accessibility financing options and after sales service quality to capture diverse consumer segments. The entest of international corporations like Thor Industries through acquisitions has elevated competitive dynamics and accelerated technology transfer across European operations. Regional players leverage local manufacturing expertise and regulatory familiarity to maintain market share against larger multinational competitors. Innovation cycles shorten as companies race to introduce connected features energy efficient systems and customizable layouts. Distribution channel competition spans traditional dealerships digital platforms and rental services creating multi dimensional rivalry. Regulatory compliance costs and sustainability requirements raise barriers to entest favoring established manufacturers with substantial research and development resources. The competitive environment encourages continuous improvement in product quality customer experience and operational efficiency while fostering market consolidation through strategic mergers and acquisitions.

KEY MARKET PLAYERS

A dominating players that are in the Europe mobile home market are

- Clayton

- Trigano SA

- Knaus Tabbert AG

- Champion Home Builders, Inc.

- Adria Mobil d o o

- Cavco Industries, Inc.

- Legacy Houtilizing Corporation

- Manor Park Homes

- Willerby

- The Swift Group

- Omar Park Homes Ltd

- Sunshine Habitat.

- Prestige Homeseeker Ltd

- ABI UK Ltd

- BIO HABITAT

- Trident Caravans

- VeroHomes

- Camplas S.C.

Top Players In The Market

- Trigano SA operates as a prominent European mobile home manufacturer with extensive production facilities across France and neighboring regions. The company contributes significantly to global recreational vehicle markets through innovative design and scalable manufacturing processes. The company extconcludeed its Mamers production site to increase installed capacity to numerous mobile homes annually according to corporate disclosures. Trigano prioritizes eco responsible construction practices and modular design flexibility to meet diverse European consumer preferences. Recent product launches including the Evolution 24 and Nest ranges demonstrate commitment to residential comfort and outdoor lifestyle integration. The group leverages digital distribution platforms and dealer networks to enhance market accessibility across multiple European territories.

- Knaus Tabbert AG stands as a leading German manufacturer of motorhomes caravans and mobile homes serving European and international markets. The company drives global market contribution through premium engineering quality and brand diversification across six distinct product lines. The firm focutilizes on production capacity expansion through facility upgrades in Hungary and Germany. Recent strategic realignment emphasizes sustainable manufacturing practices and digital customer engagement tools. The company integrates smart connectivity features and energy efficient technologies into new model releases to align with European environmental directives. Knaus Tabbert strengthens dealer partnerships and after sales service networks to reinforce brand loyalty and market penetration across key European regions.

- Adria Mobil d o o operates as a distinguished Slovenian manufacturer specializing in mobile homes modular houtilizing and glamping solutions for European markets. The company enhances global market presence through innovative product design and strategic alignment with Thor Industries distribution capabilities. The firm introduced the MLine Pure mobile home specifically designed for Mediterranean markets with emphasis on Italian consumer preferences. Adria prioritizes sustainable material selection and recyclable construction methods to meet European environmental standards. The company leverages award winning design recognition and participation in major industest exhibitions like Caravan Salon Düsseldorf to strengthen brand visibility. Adria Mobil expands distribution partnerships and digital configurator tools to improve customer customization and purchase accessibility across European territories.

Top Strategies Used By Key Market Participants

Key players in the Europe Mobile Home Market prioritize strategic acquisitions to consolidate market position and expand product portfolios. Companies invest heavily in production capacity expansion to meet rising demand while achieving economies of scale. Sustainability integration represents a core strategic pillar with manufacturers adopting eco designed materials and energy efficient technologies to comply with European environmental regulations. Digital transformation initiatives including online configurators mobile applications and connected vehicle features enhance customer engagement and differentiate product offerings. Geographic diversification through new facility locations and distribution partnerships enables market penetration across underserved European regions. Brand portfolio management allows companies to address multiple consumer segments from budobtain conscious acquireers to luxury seekers. Strategic alliances with automotive suppliers and technology providers accelerate innovation in electrification and smart home integration. After sales service network expansion and rental platform development create recurring revenue streams while improving customer retention. These interconnected strategies collectively strengthen competitive positioning and drive long term market growth across the European mobile home sector.

RECENT MARKET NEWS

- In January 2024 European Camping Group acquired Vacansoleil assets including over 900 mobile homes and 200 safari tents to expand its portfolio to 45000 mobile homes across Europe strengthening the Europe Mobile Home Market presence.

- In September 2024 Adria Mobil launched the SuperTwin campervan on Mercedes Benz chassis at Caravan Salon Düsseldorf introducing premium motorhome capabilities and strengthening the Europe Mobile Home Market presence.

MARKET SEGMENTATION

This research report on the Europe mobile home market is segmented and sub-segmented into the following categories.

By Product

- Multi-section Homes

- Single-section Homes

By Countest

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Leave a Reply