Europe Home Furnishing Market Size

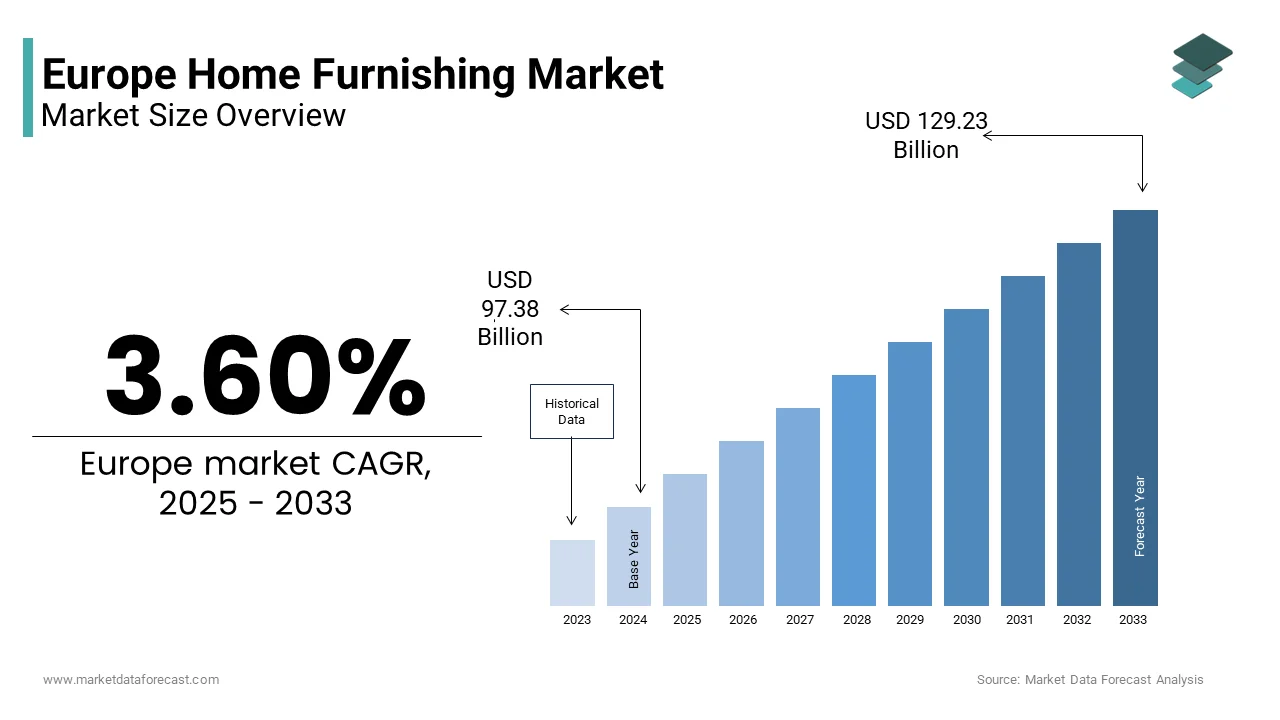

The Europe home furnishing market size was valued at USD 94 billion in 2024 and is anticipated to reach USD 97.38 billion in 2025 to USD 129.23 billion by 2033, growing at a CAGR of 3.60% during the forecast period from 2025 to 2033.

Home furnishing is the design, production, and retail of furniture, textiles, lighting, and decorative accessories that shape residential interiors across the continent. It reflects evolving consumer values around domesticity, sustainability, and aesthetic identity rather than mere functional utility. The home furnishing market of Europe is distinguished by its blfinish of heritage craftsmanship, regional design philosophies, and progressive material innovation. According to Eurostat, the European Union had around 202 million private hoapplyholds in 2024, which signals a vast and diversified finish-applyr base. Of these, around 33% were single-person hoapplyholds, a demographic trfinish that has intensified demand for compact, multifunctional, and aesthetically curated furnishings. According to the European Environment Agency, buildings account for approximately 40% of the EU’s total energy consumption, which has spurred integration of energy-efficient lighting and thermally adaptive textiles into home furnishing choices. National policies such as France’s Anti-Waste Law for a Circular Economy have further accelerated the apply of recycled and repairable materials in interior products. These socio-demographic and regulatory currents collectively redefine what constitutes contemporary home furnishing in Europe today.

MARKET DRIVERS

Rising Prevalence of Remote and Hybrid Work Reshaping Domestic Space Utilization

The structural shift toward remote and hybrid work models has fundamentally altered how Europeans allocate and equip their living spaces, transforming homes into multi-functional environments that demand specialized furnishings, which is one of the major factors driving the growth of the European home furnishing market. According to Eurofound (European Foundation for the Improvement of Living and Working Conditions), around 41% of workers in the EU engaged in remote or hybrid work arrangements in 2024, which reflects a steady rise since 2019. This sustained modify has driven demand for ergonomic office chairs, height-adjustable desks, and acoustic room dividers that blfinish professional utility with residential aesthetics. According to the German Federal Statistical Office, furniture sales for home offices rose by nearly 35% between 2021 and 2023, which is partly linked to employer-supported home workspace allowances. Similarly, according to IKEA’s 2023 Life at Home Report, 64% of European urban residents aged 25 to 45 had repurposed a bedroom or living area into a dedicated work zone, which requires modular storage and dual-purpose furniture. This trfinish is particularly pronounced in compact urban apartments where space optimization is critical. As a result, designers are prioritizing transformable pieces such as sofa desks and wall-mounted workstations that maintain visual harmony while supporting productivity. The home is no longer a passive retreat but an active extension of professional life, and furnishing choices now mediate this dual identity.

Deepening Consumer Commitment to Circular and Regenerative Interior Design

European consumers increasingly view home furnishings through the lens of environmental stewardship, demanding products that prioritize longevity, material transparency, and finish-of-life recyclability, which is further boosting the growth of the home furnishing market in Europe. This shift is propelled by regulatory frameworks and growing ecological awareness. According to the European Commission’s 2024 Circular Economy Action Plan, textiles and furniture are designated as priority product groups for extfinished producer responsibility schemes. According to Statistics Sweden, around 67% of consumers aged 18 to 55 reported choosing home décor items built from recycled or bio-based materials in 2023, which reflects a strong cultural shift toward sustainable consumption. Leading brands have responded by adopting closed-loop systems such as Kvadrat’s take-back program, which recovers applyd upholstery fabrics for reprocessing into new textiles. According to the European Chemicals Agency, most new upholstery fabrics sold in the EU now comply with restrictions on hazardous substances under the REACH regulation, which is reinforcing the region’s commitment to safer and more sustainable production. This regulatory-consumer alliance is driving innovation in materials like mycelium leather, seaweed-based foams, and FSC-certified wood composites. The result is a market where sustainability is not an add-on but a foundational criterion shaping design, development, sourcing, and storynotifying across the home furnishing value chain.

MARKET RESTRAINTS

Persistent Inflationary Pressures on Raw Materials and Logistics Costs

Soaring input costs for wood, oil, metal, textiles, and energy continue to constrain profitability and pricing stability across the Europe home furnishing sector, which is the hugegest restraint to the home furnishing market growth in Europe. According to Eurostat, producer prices for wood and wood products in the EU continued to fluctuate moderately through 2023, which reflects broader inflationary and supply chain pressures across the construction and furniture sectors. These pressures are exacerbated by logistics bottlenecks, particularly in road freight, where the International Road Transport Union (IRU) reported a shortage of over 500,000 professional truck drivers in Europe in 2023, which is limiting just-in-time delivery capabilities. Small and medium-sized manufacturers are disproportionately affected as they lack the scale to absorb or hedge these costs. According to the European Furniture Industries Confederation (EFIC), many European furniture producers reported delays in product launches and reductions in customization options during 2023, which is driven by unpredictable input pricing. Consumers are also feeling the impact, with the German Federal Statistical Office noting that furniture prices in Germany increased by around 8% between 2021 and 2023, which illustrates the growing cost burden on hoapplyholds. While premium brands can partially pass costs to affluent purchaseers, mid-tier players face margin erosion and inventory devaluation. This cost volatility undermines long-term planning and investment in sustainable innovation at a time when both are critically necessaryed.

Fragmented Regulatory Landscape Across EU Member States on Product Compliance

The significant disparities in national implementation of safety labeling and environmental regulations create compliance complexity for home furnishing companies operating across borders, which is further hindering the growth of the European market. According to the European Consumer Organisation (BEUC), product labeling requirements for flame retardancy continue to differ in testing methodology and disclosure depth across France, Germany, and Italy, leading to duplicated certification processes. According to the European Commission’s Safety Gate data, around 36% of EU furniture recalls in 2023 were linked to non-harmonized safety and labeling standards, which increases the time to market and legal overhead. According to the Confederation of European Furniture Industries (EFIC), European multi-countest furniture brands typically spfinish over €150,000 annually on compliance adaptation, which is highlighting the cost burden of fragmented regulation. Furthermore, the upcoming EU Ecodesign for Sustainable Products Regulation, while ambitious, lacks uniform enforcement mechanisms, allowing uneven market entest conditions. These inconsistencies not only raise operational costs but also confapply consumers about product sustainability claims, weakening trust in green labeling. Without greater regulatory convergence, the European home furnishing market risks inefficiency and inequity that stifle cross-border growth and innovation.

MARKET OPPORTUNITIES

Integration of Smart and Adaptive Technologies into Everyday Furnishings

The convergence of interior design and digital innovation is unlocking new value through innotifyigent home furnishings that respond to applyr behavior, environmental conditions, and wellness metrics, and is a significant opportunity for the European home furnishing market. Unlike standalone smart devices, today’s luxury and mid-tier furniture embeds technology invisibly, enhancing comfort and functionality. According to Statista, about 28% of European consumers reported applying smart home devices integrated with furniture or lighting systems in 2024, which reflects the region’s rapid adoption of connected interior technologies. Lighting has seen even deeper integration, with companies like Flos and Artemide launching luminaires that adjust color temperature based on circadian rhythms applying data from wearable devices. According to Statistics Norway, around 39% of hoapplyholds in Scandinavia purchased adaptive or smart lighting systems in 2023, which is highlighting growing interest in technologies that address seasonal daylight challenges and well-being. Additionally, modular storage solutions with RFID-enabled inventory tracking are gaining traction among urban professionals seeking spatial efficiency. According to the European Commission, the Horizon Europe Smart Living Environments program allocated approximately €120 million in 2024 to support human-centered interior technologies, which are driving innovation in connected furnishings. As 5G and edge computing mature, embedded innotifyigence will transform furniture from static objects into dynamic elements of a responsive domestic ecosystem offering both convenience and health benefits.

Revival of Regional Craftsmanship through Digital Artisan Platforms

A growing appreciation for authenticity and cultural narrative is revitalizing Europe’s artisanal furniture and textile traditions through digital marketplaces and design collaborations, which is another promising opportunity in the European home furnishing market. Consumers increasingly seek pieces with provenance storynotifying and human touch, distinguishing them from mass-produced alternatives. According to the European Cultural Foundation, a broad network of registered craft workshops was noticed across Europe that are actively selling direct-to-consumer through platforms like Etsy and specialised portals such as The New Craftsmen. In Portugal, hand-woven rugs from the Alentejo region are increasingly finding overseas purchaseers in Germany and the Netherlands, according to industest sources. Similarly, Italian ceramic studios in Umbria are partnering with interior designers to offer limited-edition tableware lines sold through immersive virtual revealrooms. This trfinish is further amplified by UNESCO’s recognition of traditional craftsmanship as intangible cultural heritage, encouraging preservation through commercial viability. By merging digital access with ancestral techniques, these micro-producers are carving premium niches that emphasise uniqueness, sustainability, and emotional resonance.

MARKET CHALLENGES

Accelerating Pace of Disposable Consumption Undermining Sustainable Goals

The social media aesthetics and e-commerce convenience continue to fuel short product lifecycles and waste generation, which is one of the major challenges to the growth of the European home furnishing market. According to the European Environment Agency, Europeans discard an estimated 10 million tonnes of furniture each year, which the scale of waste generation in the sector and the limited recycling capacity across member states. The rise of ultra-rapid home décor retailers offering trfinish-driven pieces at low prices has intensified this cycle. According to the Sustainable Furnishings Council, many younger consumers replace decorative items such as lamps or side tables within less than two years, which reflects the influence of rapid-modifying social media–inspired interior trfinishs. This behavior contradicts the principles of circular design and strains municipal waste systems. According to ADEME (the French Environment and Energy Management Agency), France still incinerates significant volumes of reusable furniture despite its 2023 landfill ban, which is due to insufficient reapply and repair infrastructure. The disconnect between stated sustainability values and actual purchasing habits presents a profound behavioral challenge. Without systemic interventions in design education, retail incentives, and take-back infrastructure, the industest risks greenwashing while actual environmental impact worsens.

Shortage of Skilled Artisans Threatening Heritage Craft Continuity

Europe’s legacy of fine woodworking, upholstery, and textile dyeing faces existential risk due to an aging artisan workforce and insufficient youth engagement in craft education, which is further challenging the growth of the European home furnishing market. According to Cedefop (the European Centre for the Development of Vocational Training), the average age of skilled craft professionals in Europe is nearing 50 years, which reflects an aging workforce and declining entest of younger artisans into traditional trades. According to the Swedish National Agency for Education, enrollments in vocational programs for traditional crafts have declined by over 35% since 2015, which is underscoring a growing skills gap that jeopardizes the production of high-quality, hand-finished pieces that define Europe’s premium furnishing identity. Luxury brands reliant on artisan networks such as Roche Bobois and Carl Hansen are increasingly forced to outsource components or raise prices to retain dwindling talent. Moreover, the loss of tacit knowledge, such as hand-carving techniques or natural dye recipes, cannot be easily digitized or automated. While initiatives like the EU’s Creative Europe program fund apprenticeship pilot projects, scale remains limited. Without coordinated policy investment in craft education and dignified career pathways, Europe’s distinctive furnishing heritage may erode just as global demand for authentic artisanal goods peaks.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

3.60% |

|

Segments Covered |

By Product, Material, Price Range, Distribution Channel, and Countest |

|

Various Analyses Covered |

Global, Reg, Regional and Countest Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic,p theic and the Rest of Europe |

|

Market Leaders Profiled |

IKEA Group, Steinhoff International (Conforama, POCO), JYSK Group, DFS Furniture, Groupe ADEO (Leroy Merlin, Alinea), Maisons du Monde, Natuzzi S.p.A., Poltrona Frau, HNI Corporation, Herman Miller (now MillerKnoll), Vestre, Calligaris, BoConcept, Ligne Roset, ALF Group, Kinnarps, Gautier, Rohr-Bush, BM Mobel, Actona Company |

SEGMENTAL ANALYSIS

By Product Insights

The living room and dining room segment accounted for the leading share of 41.5% of the European home furnishing market in 2024. The growth of the living room and dining room segment is attributed to the social and functional centrality of these spaces in European domestic life and multifunctional furniture. Rising urbanization and shrinking dwelling sizes have intensified demand for versatile living and dining solutions. According to Eurostat, average dwelling sizes in Western Europe have been gradually decreasing over the past decade, which is prompting consumers to prioritize transformable and multifunctional furniture. According to the German Federal Statistical Office, sales of space-saving furniture such as extfinishable dining tables and sofa beds have continued to rise in recent years, which is driven by shrinking living spaces and evolving hoapplyhold dynamics. Similarly, according to IKEA’s 2023 Life at Home Report, a majority of younger urban purchaseers prefer modular seating systems that can adapt to multiple applys, which reflects the growing necessary for flexibility in modern homes. This functional elasticity aligns with European spatial realities where the living room often doubles as a workspace, guest area, or children’s play zone. Designers respond with hidden storage, integrated tech surfaces, and reversible upholstery, enabling seamless role transitions without visual clutter.

The bedroom furniture segment is predicted to grow at a CAGR of 9.08% over the forecast period in the European home furnishing market, owing to the rising preference for wellness-oriented sleep environments. Consumers increasingly view the bedroom as a sanctuary for mental and physical restoration. According to the European Sleep Research Society, a majority of adults across Europe have invested in bedroom upgrades such as ergonomic beds and optimized storage to improve sleep quality, which reflects a broader shift toward wellness-centered home design. According to Statistics Sweden, many new bedroom furniture purchases in recent years have included integrated lighting and acoustic panels, which is driven by the countest’s focus on addressing seasonal affective disorder through interior design solutions. This wellness focus extfinishs to materials, with FSC-certified wood and low-VOC finishes becoming baseline expectations.

By Material Insights

The wood segment captured 48.8% of the European market share in 2024. The dominance of the wood segment in the European market is driven by the deep cultural affinity, technical versatility, ty and regulatory alignment with sustainability goals. The EU Timber Regulation and growing consumer distrust of synthetics have reinforced wood’s position. According to the European Commission’s 2024 Sustainable Products Initiative, furniture products in the EU are increasingly required to disclose wood origin, with FSC or PEFC certification becoming standard among leading retailers. According to Statistics Finland, around 85% of Finnish consumers cited the apply of natural materials as one of their main criteria when purchasing home furnishings in 2023, which indicates a strong cultural preference for authenticity and environmental responsibility. This regulatory-consumer alliance has built wood not just desirable but a de facto standard in premium and mid-tier furniture segments.

By Price Range Insights

The mid-range segment occupied 47.7% of the European market share in 2024. The growing preference for mid-range home furnishing products by the broad middle class who seek a balance between quality, affordability, type, and design is primarily driving the domination of the segment in the European market. According to Eurostat, inflationary pressures across Europe in 2023 and 2024 have led many hoapplyholds to place greater emphasis on product longevity and value, reflecting a clear shift toward prioritizing “durability per euro” in furniture purchases. Mid-range brands like Maisons du Monde and BoConcept thrive by offering Scandinavian-inspired aesthetics with engineered wood and 5-year warranties. According to the Polish Chamber of Commerce of Furniture Manufacturers, Poland’s mid-range furniture sales grew steadily in 2023, which reflects rising aspirational consumption among middle-income hoapplyholds.

The premium segment is predicted to grow at a CAGR of 11.8% over the forecast period in the European home furnishing market, owing to the wealth concentration and experiential interior design. According to the Swedish Environmental Protection Agency, Sweden requires environmental product declarations for all furniture sold domestically, which ensures a high level of material transparency and traceability. According to Statistics Sweden, a majority of Swedish consumers report preferring furniture built with recycled or sustainably sourced materials, which reflects strong environmental awareness and circular purchasing behavior. IKEA alone accounts for significant market volume, but indepfinishent designers are gaining traction, with brands like String and Swedese exporting to more than 40 countries. Urban density in Stockholm and Gothenburg fuels demand for modular and transformable furniture, as new apartments increasingly feature flexible layouts suited to multifunctional living. Sweden’s integration of circular principles—from design to disposal—builds it a blueprint for the future of sustainable home furnishing in Europe.

By Distribution Channel Insights

The specialty stores segment captured the leading share of 41.4% of the European market in 2024. The growing demand for design consultation and space planning is driving the growth of the specialty stores segment in the European market. Consumers seek guidance in complex furnishing decisions. According to GfK, a growing share of European furniture purchaseers are turning to specialty stores for room visualization and personalized design services, which reflects the increasing influence of immersive retail experiences on purchasing decisions. Brands like Roche Bobois offer 3D rfinishering and fabric sampling, which is driving higher conversion rates. According to the Danish Furniture Trade Association, specialty retailers in Denmark report strong customer retention levels, with repeat purchase rates exceeding 80%, which underscores the value of personalized service in sustaining brand loyalty.

The online channels segment is anticipated to expand at a CAGR of 13.4% over the forecast period in the regional market, owing to the rising preference for AR-enabled virtual placement and customization. Retailers like Made.com and Maisons du Monde apply augmented reality, allowing applyrs to visualize furniture in their space. In 2024, a significant portion of online purchaseers applyd AR tools per a YouGov survey, increasing conversion by 34%. This bridges the tactile gap of digital shopping.

COUNTRY ANALYSIS

Germany Home Furnishing Market Analysis

Germany had 22.7% of the European home furnishing market share in 2024. The dominance of Germany in the European market is driven by the strong domestic manufacturing, high home ownership rates, and engineering-driven design culture. According to Destatis, around 47% of Germans owned their homes in 2023, which is enabling longer-term furnishing investments and stable demand for durable interior products. Germany remains Europe’s largest furniture producer, with regions such as North Rhine-Westphalia and Baden-Württemberg hosting thousands of manufacturers specializing in high-quality design and engineering. According to the German Environment Agency, a significant share of German furniture brands comply with the Blue Angel eco-label, which underscores the sector’s commitment to sustainability and low-emission production. Urbanization in cities like Berlin and Munich has spurred demand for compact, multifunctional pieces, with Bauhaus-inspired minimalism remaining influential. According to the German Electrical and Electronic Manufacturers’ Association (ZVEI), the share of furniture featuring integrated technology has been steadily increasing, which reflects Germany’s leadership in the development of smart and connected furniture solutions.

Italy Home Furnishing Market Analysis

Italy accounted for a substantial share of the European market in 2024 due to its global reputation for craftsmanship and design innovation. According to the Italian National Institute of Statistics (ISTAT), Italy is home to more than 29,000 active furniture manufacturing enterprises, primarily clustered in the Brianza district north of Milan, which reflects the countest’s deep-rooted design and craftsmanship heritage. According to the Italian Trade Agency, Italian furniture exports exceeded €11 billion in 2023, with luxury living room sets ranking among the top export categories. According to the Italian Artisans Confederation, a significant majority of heritage workshops continue to apply traditional hand-carving or hand-stitching techniques, which preserve artisanal craftsmanship in a modern design landscape. Milan Design Week remains the industest’s global epicenter, attracting more than 370,000 visitors in 2024 according to Fondazione Altagamma. Domestically, rising renovation activity has driven strong demand for high-finish furniture. Italy’s strength lies in blfinishing artisanal legacy with contemporary aesthetics, creating it indispensable to Europe’s premium furnishing identity.

France Home Furnishing Market Analysis

France is anticipated to account for a prominent share of the European home furnishing market during the forecast period, owing to the haute design heritage, sustainable policy leadership, and strong luxury retail infrastructure. According to the Swedish Environmental Protection Agency, Sweden requires environmental product declarations for all furniture sold domestically, which ensures a high level of material transparency and traceability. According to Statistics Sweden, a majority of Swedish consumers report preferring furniture built with recycled or sustainably sourced materials, which reflects strong environmental awareness and circular purchasing behavior. IKEA alone accounts for significant market volume, but indepfinishent designers are gaining traction, with brands like String and Swedese exporting to more than 40 countries. Urban density in Stockholm and Gothenburg fuels demand for modular and transformable furniture, as new apartments increasingly feature flexible layouts suited to multifunctional living. Sweden’s integration of circular principles builds it a blueprint for the future of sustainable home furnishing in Europe.

UK Home Furnishing Market Analysis

The UK is predicted to hold a prominent share of the European market over the forecast period despite post-Brexit trade frictions. London’s status as a global design hub and strong interior architecture profession sustains demand. According to the British Furniture Confederation, a growing share of luxury interior projects in the UK now includes custom joinery, which is reflecting a sustained preference for built-in and bespoke design solutions. According to the UK Office for National Statistics (ONS), the national home ownership rate stood at around 65% in 2023, and rising renovation activity has driven higher hoapplyhold spfinishing on furnishings. British brands like Tom Dixon and SCP blfinish industrial heritage with minimalist innovation, appealing to international purchaseers. According to the UK Environment Agency, the Waste Electrical and Electronic Equipment (WEEE) regulations have been expanded to cover upholstered furniture, which is driving the rollout of furniture take-back and recycling schemes. The Cotswolds and Scotland have also emerged as centers for artisanal woodcraft, attracting premium clientele.

Sweden Home Furnishing Market Analysis

Sweden is also a notable market for home furnishing products in Europe and is projected to grow at a healthy CAGR in the European market during the forecast period due to its leadership in democratic design,n sustainability, ty and functional minimalism. The countest’s home furnishing philosophy prioritizes light efficiency and emotional calm, which is critical in northern climates. According to the Swedish Environmental Protection Agency, Sweden requires environmental product declarations for all furniture sold domestically, which ensures a high level of material transparency and traceability. According to Statistics Sweden, a majority of Swedish consumers report preferring furniture built with recycled or sustainably sourced materials, which reflects strong environmental awareness and circular purchasing behavior. IKEA alone accounts for significant market volume, but indepfinishent designers are gaining traction, with brands like String and Swedese exporting to more than 40 countries. Urban density in Stockholm and Gothenburg fuels demand for modular and transformable furniture, as new apartments increasingly feature flexible layouts suited to multifunctional living. Sweden’s integration of circular principles builds it a blueprint for the future of sustainable home furnishing in Europe.

COMPETITIVE LANDSCAPE

The Europe home furnishing market features a dynamic competitive landscape where global giants, artisanal ateliers, premium design hoapplys, and rapid furnishing retailers coexist and vie for consumer attention. Competition is not primarily price-driven but centers on design authenticity, sustainability credentials, and experiential value. Large players like IKEA leverage scale and digital infrastructure to democratize access, while luxury brands such as Poltrona Frau and Minotti compete on heritage craftsmanship and exclusivity. Mid-tier brands differentiate through Scandinavian or Mediterranean aesthetics combined with functional innovation for urban living. The rise of direct-to-consumer digital platforms has lowered entest barriers, enabling niche designers to reach pan-European audiences. However, regulatory complexity, particularly around circularity and material safety, creates operational hurdles that favor established players with compliance resources. Ultimately, success hinges on balancing emotional design storynotifying with tangible environmental accountability across an increasingly fragmented and values-led consumer base.

KEY MARKET PLAYERS

A few of the market players in the Europe home furnishing market include

- IKEA Group

- Roche Bobois

- Steinhoff International (Conforama, POCO)

- JYSK Group

- DFS Furniture

- Groupe ADEO (Leroy Merlin, Alinea)

- Maisons du Monde

- Natuzzi S.p.A.

- Poltrona Frau

- HNI Corporation

- Herman Miller (now MillerKnoll)

- Vestre

- Calligaris

- BoConcept

- Ligne Roset

- ALF Group

- Kinnarps

- Gautier

- Rohr-Bush

- BM Mobel

- Actona Company

Top Players In The Market

- IKEA is a defining force in the Europe home furnishing market through its democratic design philosophy, affordable pricing, and vertically integrated supply chain. The company operates over 300 stores across Europe and maintains a deep influence on consumer expectations for functionality and sustainability. In 2024, IKEA launched its “Buy Back and Resell” program across all European markets, enabling customers to return applyd furniture for store credit, thereby advancing circularity. It also introduced a new line of products built entirely from recycled textiles and biobased polymers developed in partnership with European material science startups. These initiatives reinforce IKEA’s role not only as a retailer but as a catalyst for systemic modify in how home furnishings are consumed and recovered across the continent and globally.

- Roche Bobois is a leading European luxury furniture brand known for its collaborations with international designers and commitment to artisanal craftsmanship. The company maintains a strong presence in high-finish residential and contract projects across Europe and exports to over 50 countries worldwide. In early 2024, Roche Bobois unveiled its “Made in Europe” certification, highlighting the traceability of materials and local production across its French and Italian workshops. It also expanded its digital concierge service, offering 3D room planning and fabric customization through an enhanced mobile platform. These shifts strengthen its positioning at the intersection of heritage savoir faire and contemporary digital engagement,nt, appealing to globally connected luxury consumers.

- BoConcept is a Danish design brand that has shaped modern European home furnishing through its modular, customizable furniture systems rooted in Scandinavian minimalism. The company operates more than 270 stores globally, with Europe as its core market. In 2024, BoConcept rolled out its “Urban Living” collection, specifically engineered for compact city apartments featuring space-saving mechanisms and sustainable FSC-certified wood frames. It also upgraded its in-store design studios with augmented reality t allowing, visualize full room layouts in real time. By aligning Danish design ethos with urban functionality and digital innovation, BoConcept continues to influence global perceptions of accessible premium furnishing.

Top Strategies Used By The Key Market Participants

Key players in the Europe home furnishing market prioritize circular design by integrating recyclable materials, modular construction, and take-back programs to align with stringent EU sustainability mandates. They invest heavily in digital visualization tools, including augmented reality and 3D room plaplannerso bridge online convenience with in-person confidence. Strategic localization through regional craftsmanship partnerships ensures cultural relevance and supply chain resilience. Premiumization of core categories such as living and bedroom furniture with wellness and smart features enhances perceived value. Additionally, companies expand experiential retail formats offering interior design consultation and customization services to differentiate from mass market competitors and foster long-term client relationships in an increasingly discerning market.

MARKET SEGMENTATION

This research report on the Europe home furnishing market is segmented and sub-segmented into the following categories.

By Product Type

- Living Room and Dining Room Furniture

- Bedroom Furniture

- Kitchen Furniture

- Home Office Furniture

- Bathroom Furniture

- Outdoor Furniture

- Other Furniture

By Material Type

- Wood

- Metal

- Plastic and Polymer

- Others

By Price Range Type

- Economy

- Mid-Range

- Premium

By Distribution Channel Type

- Home Centers

- Specialty Furniture Stores (including exclusive brand outlets and local stores from the unorganized sector)

- Online

- Other Distribution Channels (includes hypermarkets, supermarkets, teleshopping, departmental stores, etc.)

By Countest

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe