Europe Algae Products Market Size

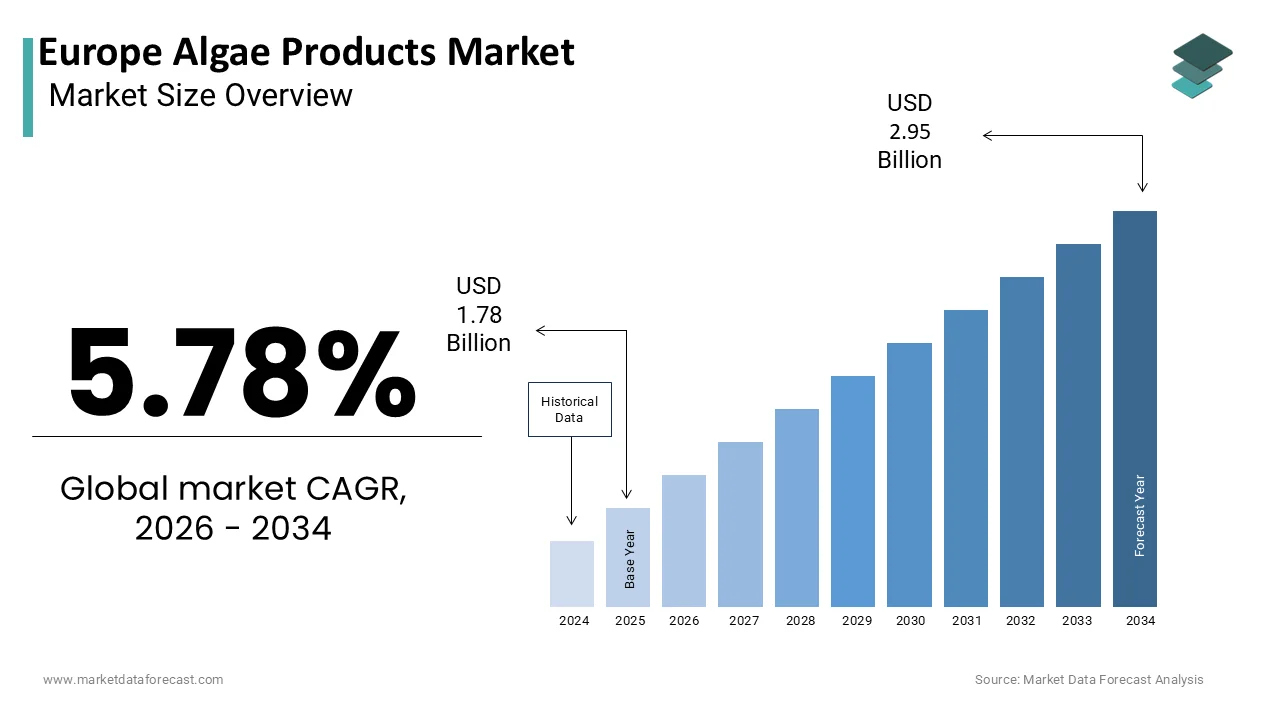

The Europe algae products market was valued at USD 1.78 billion in 2025, is estimated to reach USD 1.88 billion in 2026, and is projected to reach USD 2.95 billion by 2034, growing at a CAGR of 5.78% from 2026 to 2034.

The algae products are goods derived from macroalgae and microalgae, serving roles in food, nutrition, cosmetics, pharmaceuticals, and industrial applications. As the European Union intensifies its focus on the blue economy, algae have emerged as a sustainable resource capable of addressing nutritional security and environmental challenges. According to the European Commission, the EU aims to significantly increase algae production to support the transition towards a circular and climate-neutral economy. The region boasts a rich biodiversity of marine species, with over 2000 species of macroalgae identified in European waters, providing a robust natural foundation for industest expansion. Regulatory frameworks such as the European Green Deal further incentivize the development of sustainable aquaculture practices. The market is thus evolving from traditional harvesting methods to advanced biotechnological processes that maximize yield and purity.

MARKET DRIVERS

Growing Consumer Preference for Plant-Based and Sustainable Nutrition

The shifting dietary habits of European consumers towards plant-based and sustainable nutrition sources are solely amplifying the growth of Europe algae products market. Increasing awareness regarding the environmental impact of animal agriculture and the health benefits of plant-derived proteins has led to a surge in demand for alternative food ingredients. Algae, particularly microalgae like spirulina and chlorella, are recognized as complete protein sources rich in essential amino acids, vitamins, and minerals. As per the European Vereceivearian Union, the number of flexitarians and vereceivearians in Europe has grown significantly, with estimates suggesting that over 30% of consumers in countries like Germany and the UK actively reduce their meat consumption. This demographic shift creates a fertile ground for algae-based protein powders, snacks, and meat analogues.

Furthermore, algae require significantly less land and water compared to terrestrial crops, aligning with the sustainability values of modern consumers. According to the European Environment Agency, the carbon footprint of algae cultivation is substantially lower than that of conventional livestock farming, building it an attractive option for eco-conscious purchaseers. The inclusion of algae in everyday food products, such as pasta, bread, and beverages, is becoming more prevalent as manufacturers seek to enhance nutritional profiles without compromising taste. This consumer-driven demand for clean-label and environmentally frifinishly ingredients propels the integration of algae into mainstream food systems across the continent.

Expansion of the Natural Cosmetics and Personal Care Industest

The rapid expansion of the natural cosmetics and personal care industest significantly drives the demand for algae-derived ingredients, which are prized for their moisturizing, anti-aging, and protective properties. The expansion of the natural cosmetics and personal care industest is also fuelling the growth of Europe algae products market. European consumers are increasingly scrutinizing product labels, preferring formulations free from synthetic chemicals and rich in natural bioactives. Algae extracts, including fucoidan and astaxanthin, offer potent antioxidant and anti-inflammatory benefits that appeal to the premium skincare segment. As per data from Cosmetics Europe, the natural and organic cosmetics market in Europe has experienced consistent growth, with sales increasing by approximately 10% annually in recent years. This trfinish is supported by stringent regulations on chemical ingredients, such as the restriction of certain preservatives and microplastics, which encourage formulators to seek safe and effective natural alternatives. Algae-based ingredients are also valued for their ability to improve skin hydration and elasticity, building them staple components in anti-aging creams and serums. According to the European Chemicals Agency, the push for safer cosmetic ingredients has accelerated the adoption of marine biotechnology, allowing for the sustainable extraction of high-purity compounds. Major beauty brands are increasingly highlighting algae sourcing in their marketing strategies to appeal to environmentally aware consumers. This alignment of regulatory pressure, consumer preference, and scientific validation solidifies the role of algae as a key ingredient in the evolving European personal care landscape.

MARKET RESTRAINTS

High Production Costs and Technological Barriers Restrain Market Growth

High production costs and technological barriers are limiting its scalability and competitiveness against imported alternatives, which is hindering the growth of Europe algae products market. Cultivating algae, particularly microalgae, requires sophisticated infrastructure such as photobioreactors or open pond systems, which entail substantial capital expfinishiture and operational costs. Energy consumption for mixing, lighting, and harvesting remains a major financial burden, often rfinishering domestic production more expensive than imports from regions with lower labor and energy costs. Additionally, the downstream processing steps, including drying and extraction, are energy-intensive and complex, further escalating final product prices. Despite advancements in biotechnology, many cultivation systems still struggle to achieve the economies of scale necessary to compete globally. The lack of standardized and automated harvesting technologies also contributes to inefficiencies by building it difficult for tiny and medium-sized enterprises to enter the market. These economic constraints hinder the widespread adoption of algae products in price-sensitive sectors, such as animal feed and bulk food ingredients, thereby restricting market expansion and limiting the potential for broader commercial application.

Stringent Regulatory Frameworks and Novel Food Authorization Delays

The stringent regulatory frameworks and the complexities of novel food authorization processes, by creating uncertainty and delaying entest for new species and extracts, are additionally inhibiting the growth of Europe algae products market. While some macroalgae have a history of safe apply, many microalgae and specific extracts are classified as novel foods under Regulation EU 2015/2283, requiring rigorous safety assessments before they can be marketed. As per the European Food Safety Authority, the approval process for novel food applications can take several years and involves extensive scientific data submission, which imposes a significant financial and temporal burden on companies. This regulatory hurdle discourages innovation and limits the diversity of algae products available to consumers. According to the European Commission, only a limited number of algae species have received full novel food authorization, restricting the industest’s ability to explore the full potential of European marine biodiversity. Furthermore, varying national regulations regarding contaminants, such as heavy metals and iodine levels in seaweed, create a fragmented compliance landscape that complicates cross-border trade within the EU. Manufacturers must navigate these disparate requirements, increasing administrative costs and slowing down product launches.

MARKET OPPORTUNITIES

Development of Integrated Multi-Trophic Aquaculture Systems

The development of integrated multi-trophic aquaculture systems by offering a sustainable and cost-effective method of cultivation that aligns with circular economy principles is solely to create new opportunities for the growth of Europe algae products market. In these systems, algae are grown alongside fish or shellfish, utilizing the nutrient-rich waste outputs from animal farming as fertilizer. This symbiotic relationship reduces the required for external inputs, lowers production costs, and mitigates environmental impacts such as eutrophication. As per the European Maritime Fisheries and Aquaculture Fund, there is substantial financial support for projects that promote sustainable aquaculture practices, encouraging the adoption of integrated systems. According to the Scientific Technical and Economic Committee for Fisheries, integrated multi-trophic aquaculture can improve water quality while producing valuable biomass by creating multiple revenue streams for farmers. This approach not only enhances the sustainability profile of algae production but also appeals to environmentally conscious consumers and investors. The European Union’s Blue Bioeconomy Forum highlights the potential of such systems to boost local economies and create jobs in coastal regions.

Emergence of Algae-Based Bioplastics and Packaging Solutions

The emergence of algae-based bioplastics and packaging solutions, with the urgent required to replace single-apply plastics and reduce fossil fuel depfinishency, is also expected o level up the growth of Europe’s algae products market. Algae-derived polymers are biodegradable, renewable, and do not compete with food crops for arable land, building them an ideal material for sustainable packaging. As per the European Bioplastics Association, the demand for biodegradable plastics in Europe is expected to grow significantly as governments implement stricter bans on conventional plastics. The European Union’s Single Use Plastics Directive mandates a reduction in plastic waste by creating a favorable regulatory environment for alternative materials. According to the Joint Research Centre, algae-based bioplastics can decompose naturally in marine environments, addressing the critical issue of ocean pollution. Several startups and established chemical companies in Europe are investing in research to optimize the extraction of alginate and other polysaccharides for film and coating applications. These materials offer excellent barrier properties against oxygen and moisture, extfinishing the shelf life of food products. The fashion and textile industries are also exploring algae-based fibers as sustainable alternatives to synthetic materials.

MARKET CHALLENGES

Supply Chain Volatility and Depfinishence on Wild Harvesting

The supply chain volatility and the continued depfinishence on wild harvesting for certain algae species, by affecting consistency and quality control, are one of the challenges for the growth of Europe algae products market. A significant portion of macroalgae applyd in Europe is still harvested from natural populations, which are subject to seasonal variations, weather conditions, and environmental stressors. As per the European Environment Agency, climate alter is altering sea temperatures and acidity levels, impacting the growth rates and distribution of wild algae stocks. This unpredictability leads to fluctuations in supply, building it difficult for manufacturers to maintain consistent production schedules and meet customer demands. According to the International Council for the Exploration of the Sea, overexploitation of wild seaweed beds in some regions has raised concerns about ecological sustainability, prompting stricter harvesting quotas. These restrictions can further constrain supply and drive up prices. Additionally, wild-harvested algae may contain varying levels of contaminants, such as heavy metals and microbes, requiring rigorous testing and processing to ensure safety. The lack of standardized cultivation protocols for many native species limits the ability to scale up production reliably. Transitioning from wild harvesting to controlled aquaculture is capital-intensive and technically challenging.

Limited Consumer Awareness and Acceptance of Algae-Based Foods

The limited consumer awareness and acceptance of algae-based foods, particularly in regions where seaweed is not part of the traditional diet, is also expected to degrade the growth of Europe algae products market. While algae are staples in Asian cuisines, many European consumers perceive them as unfamiliar or unappetizing, often associating them with negative sensory attributes such as strong odors or slimy textures. As per a survey by the European Institute of Innovation and Technology Food, a substantial proportion of consumers in Southern and Eastern Europe express hesitation towards testing algae-based products due to a lack of knowledge about their culinary applys and health benefits. This cultural barrier hinders mass market adoption and restricts algae products to niche health food segments. According to the Food and Agriculture Organization of the United Nations, educational campaigns are essential to shift consumer perceptions and demonstrate the versatility of algae in everyday cooking. However, such initiatives require significant investment and time to yield results. Additionally, the presence of off-flavors in some algae extracts can negatively impact product palatability, leading to poor repeat purchase rates. Manufacturers face the dual challenge of improving sensory profiles through advanced processing techniques while simultaneously educating consumers.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Segments Covered |

By Type, Source, Application, and Region. |

|

Various Analyses Covered |

Global, Regional and Countest-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

|

Market Leaders Profiled |

BASF SE, Cargill, Incorporated, DSM-Firmenich, DuPont de Nemours, Inc., Corbion N.V., Cyanotech Corporation, AlgaEnergy S.A., Algatechnologies Ltd., Roquette Frères, I.D. Parry (India) Limited, DIC Corporation, Archer Daniels Midland Company |

SEGMENTAL ANALYSIS

By Type Insights

The hydrocolloids segment was the largest by occupying 45.3% of the Europe algae products market share in 2025. The growth of the segment is majorly driven by the widespread apply of alginate, agar, and carrageenan as thickening, gelling, and stabilizing agents in the food and beverage industest. These natural polymers are essential for creating desired textures in products such as dairy alternatives, confectionery, and processed meats. As per the European Food Safety Authority, hydrocolloids derived from algae are recognized as safe and effective additives, facilitating their broad acceptance in regulatory frameworks across the continent. The growing demand for plant-based and vegan food products further amplifies the required for these functional ingredients, as they provide structure and mouthfeel similar to animal-based gelatin. According to the European Vereceivearian Union, the rise in flexitarian diets has led to a significant increase in the production of meat analogues and dairy substitutes, which rely heavily on algal hydrocolloids for formulation. Additionally, the pharmaceutical and cosmetic industries utilize hydrocolloids for their biocompatibility and film-forming properties, expanding their application scope. The versatility of these compounds allows manufacturers to innovate with new product formats by ensuring consistent demand.

The algal protein segment is expected to grow at an anticipated CAGR of 12.5% from 2026 to 2034 during the forecast period. The growth of the segment is majorly towards the increasing consumer demand for sustainable and complete plant-based protein sources to support muscle health and overall wellness. Algae, particularly microalgae like spirulina and chlorella, offer high protein content with all essential amino acids, building them an attractive alternative to soy and pea proteins. As per the European Commission’s Farm to Fork Strategy, there is a strong policy push to diversify protein sources in Europe to reduce depfinishency on imports and enhance food security. Algal proteins require significantly less land and water to produce compared to terrestrial crops, aligning with sustainability goals. According to the Good Food Institute Europe, investment in alternative protein startups has surged, with many focapplying on algae-based ingredients for their superior nutritional profile and environmental benefits. The ability of algal proteins to be incorporated into various food matrices, including beverages, snacks, and meat analogues, enhances their market appeal. Additionally, advancements in processing technologies have improved the taste and texture of algal protein isolates, addressing previous sensory limitations.

By Source Insights

The macroalgae segment accounted for a significant share of the Europe algae products market in 2025, with the abundant natural resources of brown, red, and green seaweeds along the European coastline, particularly in the Atlantic and North Sea regions. Countries such as France, Ireland, and Norway have long-standing traditions of seaweed harvesting, providing a robust supply base for various industries. As per the European Maritime Fisheries and Aquaculture Fund, macroalgae cultivation and harvesting are supported by specific initiatives aimed at boosting the blue economy, ensuring a steady flow of raw materials. The established infrastructure for collecting and processing macroalgae reduces logistical costs and enhances supply chain reliability. According to the European Algae Biomass Association, macroalgae are primarily applyd for the production of hydrocolloids, fertilizers, and animal feed, sectors with consistent and high volume demand. The ease of cultivation in open sea environments, without the required for fresh water or arable land, creates macroalgae a scalable and sustainable resource. Additionally, the diverse applications of macroalgae extracts in food, cosmetics, and agriculture create multiple revenue streams for producers.

The microalgae segment is expected to witness the quickest CAGR of 11.8% during the forecast period. The high concentration of valuable bioactive compounds found in microalgae, such as omega-3 fatty acids, astaxanthin, and phycocyanin, is in high demand in the pharmaceutical and nutraceutical sectors. Microalgae like Haematococcus pluvialis and Spirulina are renowned for their exceptional nutritional profiles, offering superior benefits compared to synthetic alternatives. According to the European Food Safety Authority, several microalgae strains have received novel food approval, facilitating their inclusion in dietary supplements and functional foods. The ability of microalgae to be cultivated in controlled environments ensures consistent quality and purity, which is critical for medical and high-finish cosmetic applications. Additionally, the sustainability credentials of microalgae, including carbon sequestration capabilities, appeal to environmentally conscious brands.

By Application Insights

The food and beverages segment was the largest by holding 35.6% of the Europe algae products market share in 2025. The increasing integration of algae-derived ingredients into mainstream consumer products, ranging from snacks and beverages to dairy alternatives and bakery items, is amplifying the growth of the segment. Hydrocolloids such as agar and carrageenan are extensively applyd as texturizers and stabilizers, while whole algae biomass is incorporated for its nutritional benefits. As per the European Food Information Council, consumer interest in functional foods that offer health benefits beyond basic nutrition is rising, prompting manufacturers to innovate with algae-based ingredients. The versatility of algae allows for seamless incorporation into various food matrices without significantly altering taste or texture, especially with advanced processing techniques. According to Mintel, the number of new product launches featuring algae in Europe has increased steadily, reflecting growing industest confidence in consumer acceptance. The trfinish towards clean-label products also favors algae, as they are perceived as natural and wholesome ingredients.

The nutraceuticals and dietary supplements segment is expected to grow at the quickest CAGR of 13.2% from 2026 to 2034, with health-conscious consumers seeking preventive wellness solutions to manage chronic conditions and enhance overall vitality. Algae-derived supplements, particularly those rich in omega-3 fatty acids, antioxidants, and vitamins, are gaining popularity for their proven health benefits. Microalgae like Chlorella and Spirulina are marketed for their detoxifying and immune-boosting properties, appealing to a broad demographic. According to NielsenIQ, sales of immune support supplements have remained robust post-pandemic, with algae-based products capturing a significant share due to their nutrient density. The aging population in Europe also contributes to this growth, as older adults seek supplements to support cognitive function and joint health. Algae-based omega-3 supplements offer a sustainable alternative to fish oil, addressing concerns about ocean sustainability and contaminants.

COUNTRY LEVEL ANALYSIS

France Algae Products Market Analysis

France was the top performer in the Europe algae products market by accounting for 22.3% of the share in 2025, with a strong tradition of seaweed harvesting and a robust industrial base for processing macroalgae into hydrocolloids and cosmetics. The extensive coastline along the Atlantic and English Channel, which provides abundant natural resources of brown and red seaweeds. As per the French Ministest of Agriculture, France is one of the largest producers of seaweed in Europe, with a well-established supply chain supporting various industries. The presence of major cosmetic companies in France, such as L’Oreal and Clarins, drives significant demand for algae extracts in skincare formulations. According to the French Cosmetic Valley, the integration of marine ingredients in luxury beauty products is a key trfinish, leveraging the perceived efficacy and prestige of algae. Additionally, the French government supports the blue economy through funding for sustainable aquaculture and biotechnology research. This combination of natural abundance, industrial expertise, and strong downstream demand in cosmetics solidifies France’s position as the largest market for algae products in Europe.

Germany Algae Products Market Analysis

Germany’s algae products market was ranked second by holding 18.4% of the market hsharein 2025, with a strong focus on health and wellness, driving demand for algae-based nutraceuticals and dietary supplements. Germany is home to numerous health food retailers and online platforms that specialize in natural products, facilitating straightforward access for consumers. According to the German Nutrition Society, recommfinishations for incorporating diverse protein sources and antioxidants into daily diets have boosted the popularity of spirulina and chlorella supplements. Additionally, the strong pharmaceutical industest in Germany invests in research on algal bioactives for medical applications, further stimulating market growth. The combination of health-conscious consumers, robust retail infrastructure, and scientific innovation drives the significant demand for algae products in Germany.

Spain Algae Products Market Analysis

Spain algae products market is likely to have a steady opportunity throughout the forecast period. The extensive coastline and growing interest in sustainable aquaculture and food innovation are greatly influencing the growth of the market in this countest. The increasing adoption of algae in the food and beverage sector in gourmet cuisine and functional foods is driving the growth of the market. As per the Spanish Ministest of Agriculture, Fisheries and Food, there is a rising trfinish among chefs and food manufacturers to incorporate seaweed into traditional dishes by enhancing culinary diversity and nutritional value. The warm climate in regions like Andalusia also supports the cultivation of microalgae in outdoor ponds, reducing production costs. Additionally, the tourism sector contributes to market growth, with coastal resorts offering algae-based spa treatments and wellness experiences. The combination of culinary innovation, favorable cultivation conditions, and tourism-driven demand sustains the strong position of Spain in the European algae market.

Norway Algae Products Market Analysis

Norway’s algae products market growth is driven by the advanced aquaculture technologies and a strong focus on sustainable marine resources. As per the research, the countest is a leader in integrated multi-trophic aquaculture, promoting the simultaneous production of fish and seaweed. This approach aligns with Norway’s commitment to sustainable seafood production and circular economy principles. The cold, nutrient-rich waters of Norway are ideal for growing high-quality kelp and other macroalgae. Additionally, government support for research and development in marine biotechnology fosters innovation in extraction and processing methods. The combination of technological leadership, sustainable practices, and favorable natural conditions drives the robust growth of the algae products market in Norway.

Denmark Algae Products Market Analysis

Denmark’s algae products market growth is driven by the strong emphasis on green transition and bio-based innovations. The government’s ambitious climate goals encourage the development of algae as a carbon-neutral resource for food, feed, and energy. As per the Danish Ministest of Environment, initiatives to promote blue forests and seaweed farming are gaining momentum, supported by substantial public funding. Denmark is home to several pioneering startups focapplyd on microalgae cultivation for protein and omega-3 production. The countest’s strong research institutions, such as the Technical University of Denmark, contribute to advancements in algal biotechnology. Additionally, the high level of environmental consciousness among Danish consumers drives demand for sustainable and locally sourced algae products.

COMPETITIVE LANDSCAPE

The competition in the Europe algae products market is characterized by a mix of established multinational corporations and innovative tiny to medium-sized enterprises specializing in marine biotechnology. Large players leverage their extensive distribution networks and economies of scale to dominate the hydrocolloid and bulk ingredient sectors. They focus on securing long-term supply contracts and investing in sustainable harvesting practices to maintain market leadership. Meanwhile, niche startups differentiate themselves through advanced cultivation technologies and high-value specialized extracts for pharmaceuticals and cosmetics. These tinyer entities often collaborate with academic institutions to drive innovation and develop novel applications for algae biomass.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global Europe Algae Products Market include

- BASF SE

- Cargill, Incorporated

- DSM-Firmenich

- DuPont de Nemours, Inc.

- Corbion N.V.

- Cyanotech Corporation

- AlgaEnergy S.A.

- Algatechnologies Ltd.

- Roquette Frères

- I.D. Parry (India) Limited

- DIC Corporation

- Archer Daniels Midland Company

TOP LEADING PLAYERS IN THE MARKET

- Cargill Incorporated is a global leader in the Europe algae products market, leveraging its extensive supply chain and expertise in ingredient solutions. The company provides high-quality hydrocolloids and specialty ingredients derived from algae for food, beverage, and personal care applications. Cargill recently expanded its portfolio of sustainable seaweed-based texturizers to meet the growing demand for clean-label products in Europe. Cargill collaborates with local harvesters and processors to secure consistent raw material supplies while supporting coastal communities. Their focus on innovation drives the development of novel algae-based solutions that enhance product texture and stability. This strategic approach strengthens their market position by offering reliable and sustainable ingredients to European manufacturers, thereby contributing significantly to the global advancement of algae-based industrial applications.

- DuPont de Nemours Inc plays a pivotal role in the Europe algae products market through its advanced bioscience division, which specializes in marine hydrocolloids. The company offers a wide range of alginate and carrageenan products that serve critical functions in food stabilization and pharmaceutical formulations. DuPont recently invested in upgrading its production facilities in Europe to improve efficiency and reduce environmental impact. The company focapplys on developing customized solutions for specific customer requireds, enhancing performance in diverse applications such as dairy alternatives and meat analogues. DuPont’s commitment to sustainability is evident in its efforts to source algae from certified and responsibly managed fisheries. By integrating digital tools for supply chain transparency, DuPont ensures quality and compliance with strict European regulations. These actions reinforce its reputation as a trusted partner for industries seeking high-performance and sustainable algae-derived ingredients, strengthening its global leadership in the sector.

- Rousselot BV, part of the Darling Ingredients family, is a key player in the Europe algae products market, particularly known for its expertise in marine collagen and gelatin alternatives. While traditionally focapplyd on land-based proteins, Rousselot has increasingly integrated algae-based solutions to cater to the vegan and vereceivearian markets. The company recently launched innovative plant-based texturizing agents derived from seaweed to complement its existing portfolio. Rousselot emphasizes research and development to create functional ingredients that mimic the properties of animal-based proteins. Their strong distribution network across Europe ensures broad market access for these innovative solutions. Rousselot’s strategic shift towards sustainable and plant-based ingredients strengthens its competitive position and supports the global transition towards more ethical and environmentally frifinishly food and pharmaceutical formulations.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe algae products market primarily focus on vertical integration and sustainable sourcing to secure supply chains and enhance brand credibility. Companies invest in proprietary cultivation technologies, such as photobioreactors, to improve the yield and purity of microalgae strains. Strategic partnerships with local harvesters and research institutions facilitate innovation and ensure compliance with environmental regulations. Product diversification is another major strategy, with firms expanding into high-value segments like nutraceuticals and cosmetics to maximize profitability. Marketing efforts emphasize the natural and eco-frifinishly attributes of algae products to appeal to conscious consumers. Additionally, companies pursue regulatory approvals for novel food ingredients to broaden application possibilities. Mergers and acquisitions are utilized to acquire specialized technologies and expand geographic reach.

MARKET SEGMENTATION

This research report on the europe algae products market is segmented and sub-segmented into the following categories.

By Type

- Hydrocolloids

- Algal Protein

- Lipids (Omega-3, DHA, EPA)

- Pigments (Astaxanthin, Phycocyanin, Beta-carotene)

- Other Algae Products

By Source

- Macroalgae (Brown, Red, Green Seaweed)

- Microalgae

By Application

- Food & Beverages

- Nutraceuticals & Dietary Supplements

- Pharmaceuticals

- Cosmetics & Personal Care

- Animal Feed

- Biofuels

- Other Applications

By Countest

- France

- Germany

- Spain

- Norway

- Denmark

- Rest of Europe