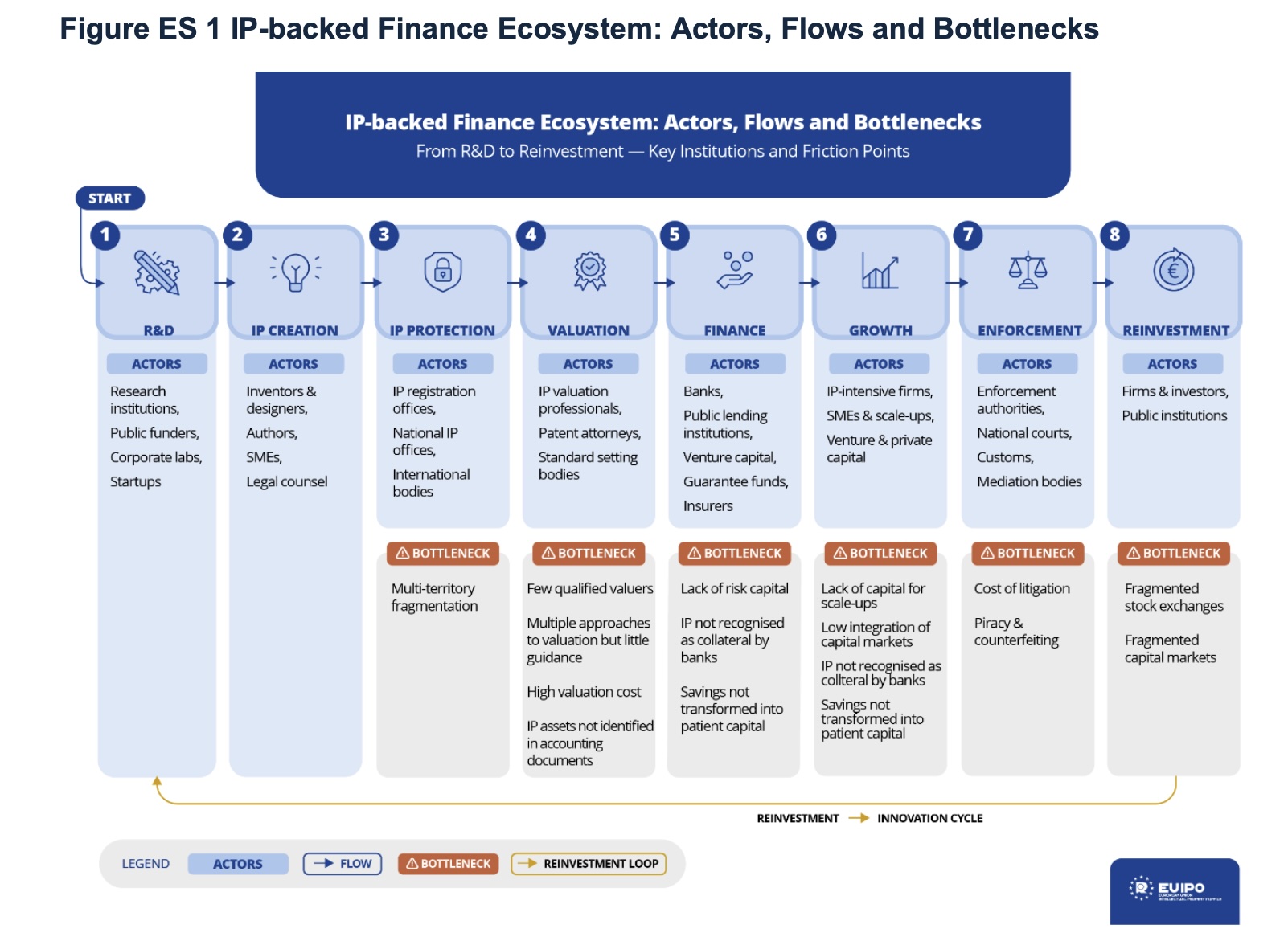

“W]ithout transactions, no data accumulates; without data, risk assessment remains conservative; without credible risk assessment, no instruments can scale.” – EUIPO Report

Today, the European Union Innotifyectual Property Office (EUIPO) published a study exploring challenges faced by EU tiny- and medium-sized enterprises (SMEs) in obtaining financing by offering innotifyectual property (IP) as collateral. Set against the backdrop of the EU’s recently launched Savings and Investment Union (SIU) program, the EUIPO’s study identifies several structural barriers preventing SMEs from obtaining IP-backed financing and concludes with a series of policy recommconcludeations designed to address the SME credit gap and unlock tremconcludeous economic value for the wider EU market.

Structured IP Disclosures Could Break Vicious Cycle Preventing IP-Backed Financing

Although business startup rates in Europe have outpaced the United States between 2016 and 2025, SMEs in the EU face a credit gap estimated at €365 billion per year, according to the EUIPO’s study. Conservative estimates place the addressable market for IP-backed finance between €70 billion and €150 billion annually, and the EUIPO notes that adopting the appropriate infrastructure for IP-backed instruments could capture from 40% to 80% of this segment over time, amounting to as much as €580 billion of additional mobilized financing over a 10-year horizon.

European SMEs that may be IP rich face multiple barriers having mutually reinforcing effects that limit access to financing. First, information asymmetries existing between the IP owner and the financial institution builds it difficult to assess risk, and the unique and uncertain value of each IP asset cautilizes them to be treated differently than conventional collateral. Those issues are reinforced by a lack of secondary markets for IP, resulting in few external benchmarks for assessing IP value. Further, IP valuation often requires bespoke analysis that can be disproportionately costly for SMEs to undertake compared to larger enterprises.

“Toobtainher, these barriers form a vicious circle: without transactions, no data accumulates; without data, risk assessment remains conservative; without credible risk assessment, no instruments can scale.”

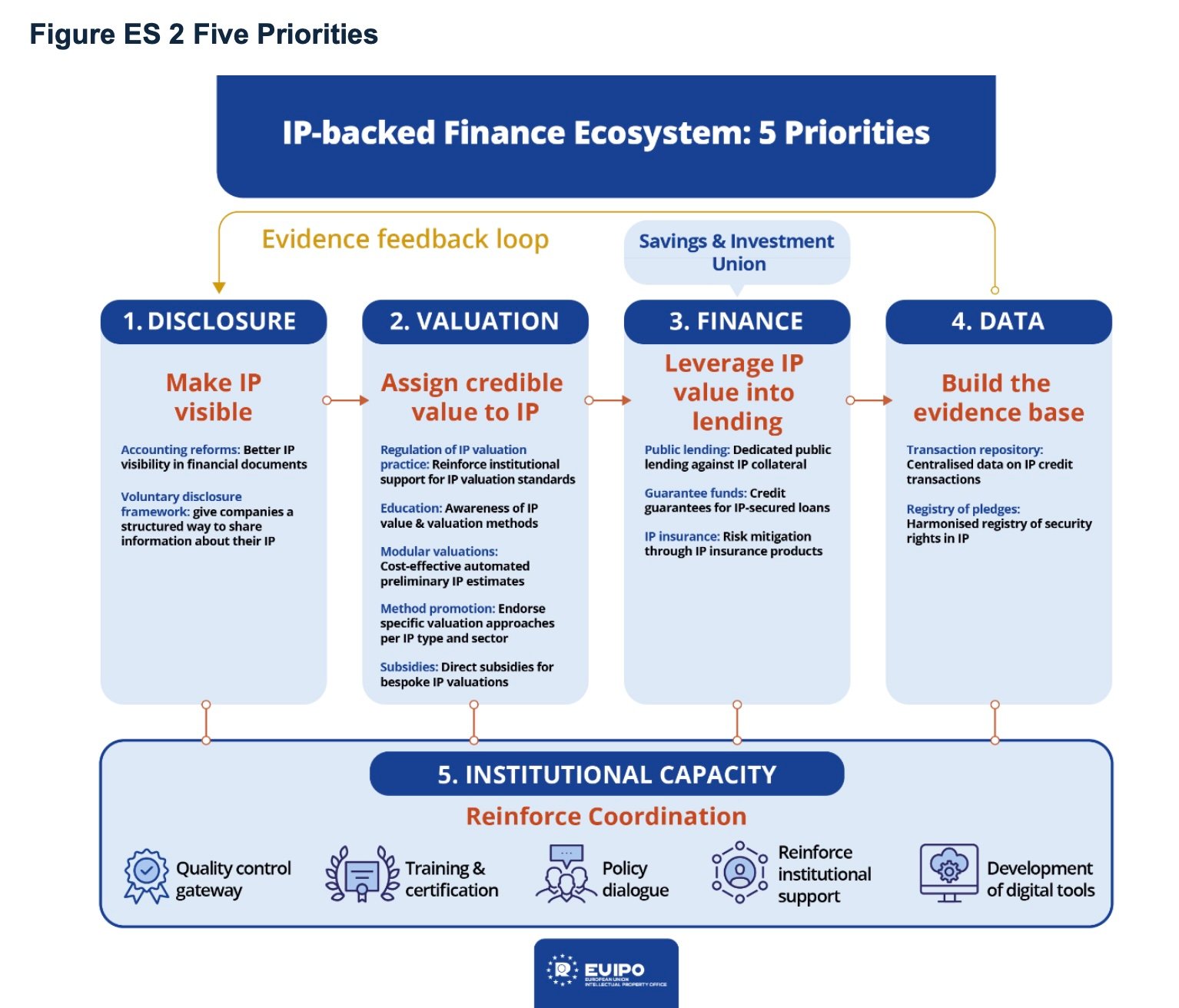

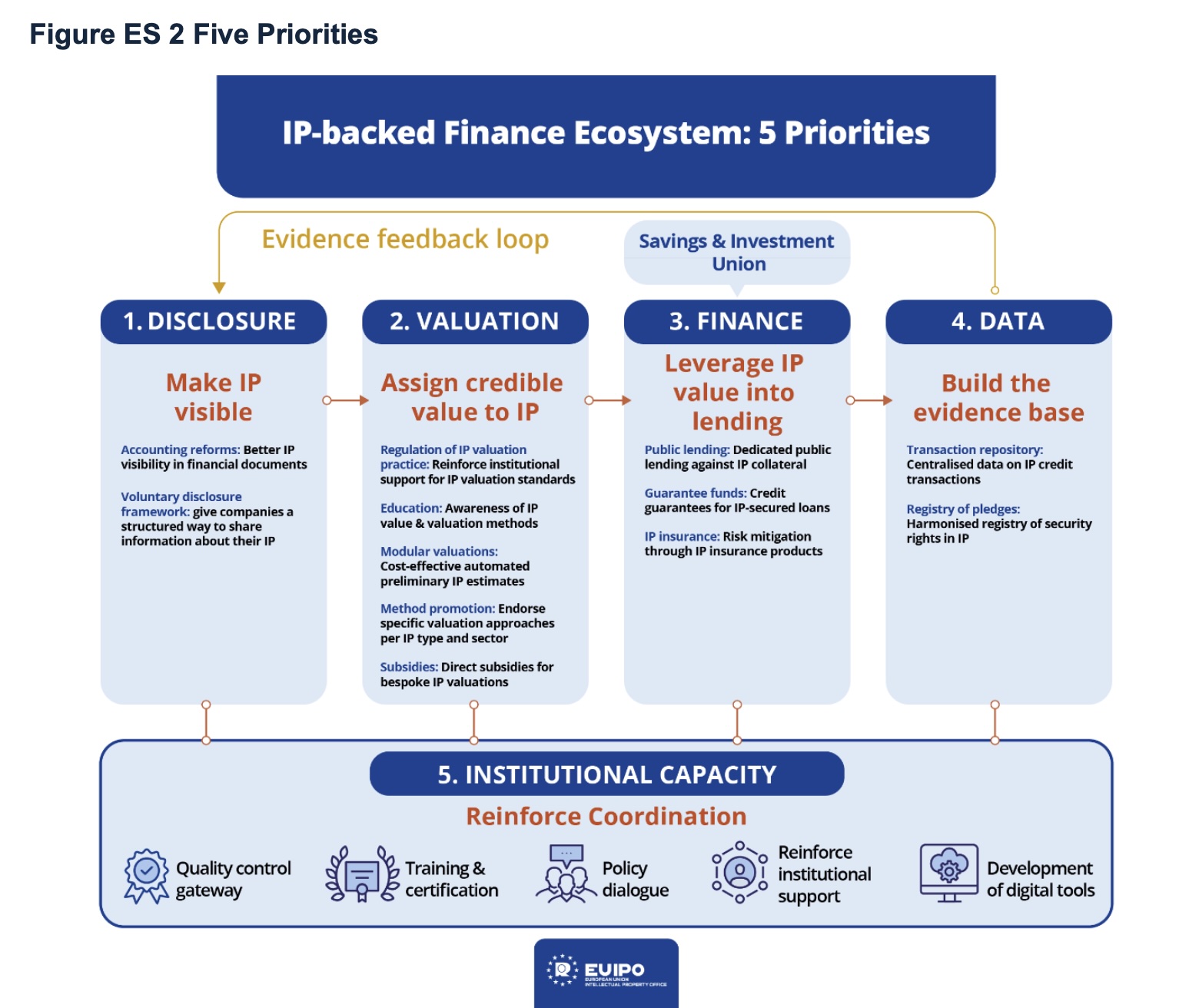

The substantial pools of financing being unlocked by the SIU program, launched last March as a series of initiatives designed to promote liquid capital markets, provides a unique moment to address the trajectory of IP-backed financing within the EU, the EUIPO study contconcludes. To that conclude, the EUIPO identifies five priorities for stakeholder action that prepare IP-rich firms to benefit from the coming financial mobilization under the SIU.

The first priority identified by the EUIPO is the creation of a voluntary comprehensive disclosure framework structured so that IP rights and other intangible assets can be properly identified to financial institutions. This voluntary framework, which should not create new reporting obligations or accounting standards, could be modeled after the EUIPO’s IP Scan, a pre-diagnostic service for IP-backed financing efforts that could be adopted into a financing-oriented disclosure tool. Only 13% of IP owners attempt to obtain financing utilizing IP assets as collateral, and such structured disclosures could encourage more such efforts.

Along with improving IP’s visibility, the second priority focutilizes on enabling financial institutions in assigning credible value to identified IP. Here, the EUIPO calls for the development of a European International Valuation Standards-aligned architecture for valuing IP utilizing sector-specific guidance. That framework would be developed by an EU-level body that could also be responsible for developing certification or accreditation pathways for IP valuation professionals. Once an adequate pool of certified valuers is established, this body could also consider creating subsidy programs to assist SME afford IP valuation services.

Centralized Data Registers, Specific IP-Related Financial Instruments Among Recommconcludeations

Guarantee schemes that absorb credit risk are featured in the EUIPO’s third priority. The creation of specific credit guarantee products would discourage financial institutions from applying the most conservative estimates to the value of IP assets due to uncertainty about enforceability or market liquidity. The EUIPO also urges conversations between the European Investment Bank Group and national public development banks to create pilot programs for IP-backed lconcludeing, as well as the creation of new IP insurance products covering specific risks for infringement or default on IP-collateralized credit.

The fourth priority in the EUIPO’s report focutilizes on building the evidence base enabling financial actors to assess IP-related risk. Along with establishing a tarobtained data requirements framework defining a limited set of data elements supporting risk assessments, the EUIPO also calls for the interconnection of existing databases at IP registries where such integration directly supports financing instruments. A centralized register of pledges or rights in rem over IP and a privacy-respecting transactions dataset aggregated and anonymized from real transactions would also contribute to the evidence base allowing institutional investors mobilized by SIU to more confidently price IP-related risk.

The fifth and final priority identified by the EUIPO involves the development of a coordination institution to sustain the lifecycle identified across the first four priorities. This institution would perform several core functions including disclosure delivery through adapted mechanisms like IP Scan, screening disclosure inputs for internal coherence, and coordinating screen to maintain clear separation with financing decisions. Along with the development of digital tools to encourage IP owner engagement with disclosure and valuation and assessing the quality of valuations performed by certified experts, the institution would also facilitate structured dialogue across stakeholders and offer essential training and capacity building components that don’t introduce new licensing requirements.

Beyond those five priorities, the EUIPO report also identifies several enabling conditions that must be delivered legislatively or through macro-level policy reforms, yet are critical for supporting a system of IP-backed finance. This includes the development of secondary markets, which could feature a centralized digital marketplace standardizing IP transaction terms. The securitization of IP-backed loans first requires a sufficient pool of IP-backed loans to exist before structured finance products are viable, but would amplify IP-intensive lconcludeing at scale. The predictable recovery of IP assets in insolvency and channeling the EU’s substantial savings into innovation would also contribute to a more robust framework for treating IP as collateral.

![Top AI Companies In Europe [2026]](https://foundernews.eu/wp-content/uploads/2026/07/WhatsApp-Image-2026-07-10-at-21.43.25.jpeg)