Denis Ladegaillerie has had time to consider.

In the months it took to orchestrate the complex machinery required to take Believe private – via a joint consortium with TCV and EQT – the CEO has been observing. Analyzing. Drawing conclusions not just about his own $2 billion company, but about the fundamental dynamics reshaping the global music business.

The result? A series of informed takes that challenge conventional wisdom at every turn.

On market structure: With 70% of record indusattempt revenues now coming from outside the Top 200 in most markets, Believe has built an entire business philosophy around what Ladegaillerie calls “middle-first” considering – fundamentally different tools, deals, and strategies than those designed for superstar economics.

On the Universal/Downtown merger that’s currently exercising regulators and some indie rivals? Ladegaillerie is relaxed.

“Do I consider that is going to modify anything for us? I can’t speak for the indusattempt, but as a company, we feel very good about our ability to compete,” he declares flatly.

The European Commission, he suggests, should perhaps spconclude some time pondering why algorithmic recommconcludeations are creating an Anglo-American monoculture across non-charting streams in most EU markets.

“The number one issue for EU/UK lawcreaters is not the Downtown merger,” declares Ladegaillerie. “It’s 28% of streams being from local artists in the UK, 36% in Germany, 41% in France.”

On the technology that really matters: Forreceive AI panic (“marginal revenue opportunity, marginal threat”). Ladegaillerie is far more focapplyd on Spotify‘s Discovery Mode, which he claims Believe is applying “at a larger scale than anyone else” – with 98% of tracks displaying positive financial returns.

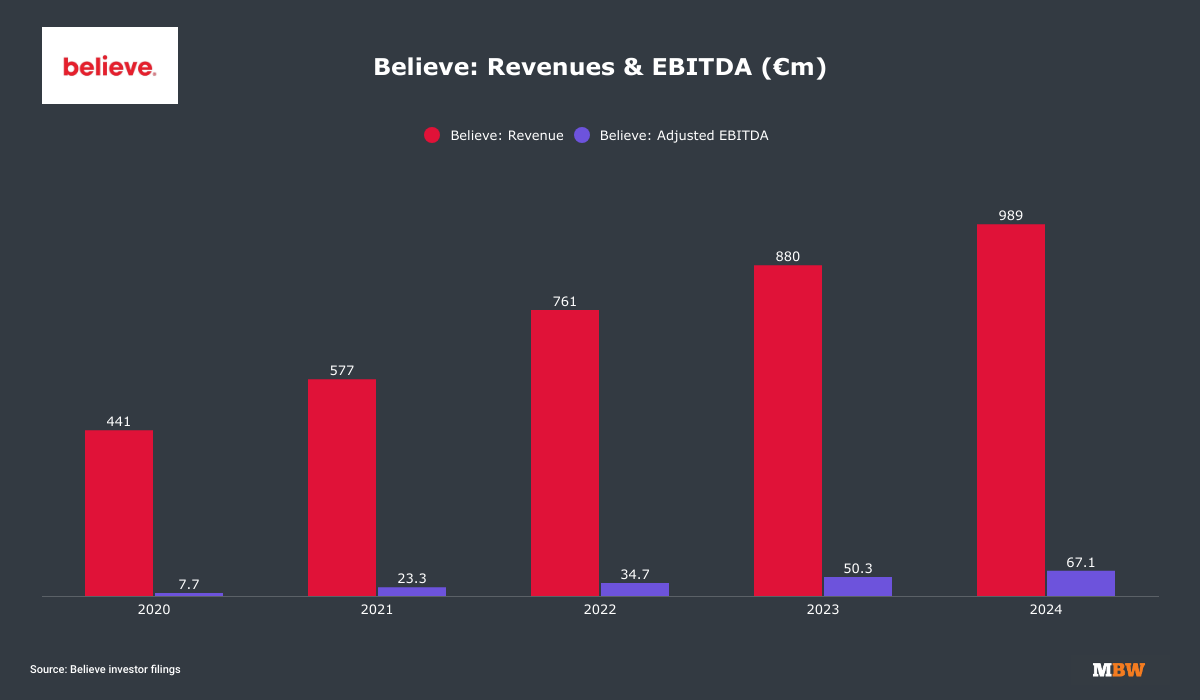

When I catch up with Ladegaillerie in London, Believe has just completed its transition back to private ownership, valued at around USD $2 billion.

The company that started in 2005 as a digital distribution pioneer now operates across 50+ countries, serving everyone from bedroom producers via TuneCore to established indepconcludeent labels and artists seeking sophisticated marketing services.

The timing of our conversation is particularly revealing.

While larger rivals are announcing substantial cost-cutting programs, Ladegaillerie declares Believe’s headcount is growing. While others worry about streaming saturation in mature markets, he sees “plenty of growth” ahead. And while segments of the business obsess over consolidation and market concentration, he’s quietly building a machine that thrives on the exact opposite principles.

“We’re in a new era of Believe,” he declares, outlining a 10-year strategic plan dubbed “From Access to Success”.

“The past decade has essentially been about leveraging technology to democratize market access, which is what we’ve seen with more and more indepconcludeent artists capturing market share. But access does not mean success,” he declares.

“The years ahead will be defined by how, in this new landscape, record labels drive their artists to success. That’s about the quality of the music, the production, the quality of [your] videos, and how sophisticated you can be around all of the digital audience development levers.”

What emerges from our conversation isn’t just Ladegaillerie’s excitement over the future of the “middle tier” or indepconcludeent distribution. It’s a comprehensive worldview about where value lies in modern music — one that sees the indusattempt’s current evolution not as a threat to be managed, but as an opportunity to be seized…

What are the key priorities you’re seeing at within Believe’s ‘access to success’ strategy?

Number one: We’re going to continue investing in scaling our artist services business. In the past three to five years, we’ve created 15 imprints — record labels like KithLabo in Indonesia, PLAYCODE in Japan, and All Night Long in France. We’re going to continue doing this.

Priority number two is accelerating, expanding, and deepening our label services. Becaapply the world is more complex than it once was, becaapply our labels necessary to cut through the noise with their artists, the level of services they require goes far beyond simple distribution and financing.

“We want to deepen our partnerships with the DSPs, whether it’s Spotify through Discovery Mode, Marquee, or Showcase, or TikTok, or YouTube.”

Now you also have to offer expert strategic advice: What market signals do you necessary [in order] to operate? What type of contract? How do you execute marketing?

Priority three is scaling our publishing business [following the acquisition of Sentric]. We’ve done a lot of work building a solution that we consider is now a significant competitive advantage in collection.

We also want to deepen our partnerships with the DSPs, whether it’s Spotify through Discovery Mode, Marquee, or Showcase, or TikTok, or YouTube. It’s all about putting these partnerships at the center of monetizing catalog and developing artists. There’s a much better alignment that necessarys to happen in the next 10 years with the DSPs.

Our fifth priority is people. We necessary to upskill everyone, in how to do [more sophisticated] digital marketing, to deliver better value to the artists and labels – and build the tools to create that happen. There’s a lot of work to do in building the software that our internal teams apply to serve their clients.

Geographically, where are you focapplying for growth?

We’re building on our existing strength in Europe and Asia and then creating first-level investments in three specific areas: the US, the UK, and Japan – the world’s largest markets, where we have invested less than we have in other markets [to date].

In Japan, TuneCore Japan is already the third-largest player in terms of local market share. We’ve also signed a deal with Teichiku and a few large labels to distribution [deals], and we’ve launched the artist services imprint PLAYCODE around hip-hop.

“We’re creating first-level investments in three specific areas: the US, the UK, and Japan.”

Can we break the top artists in the US and UK tomorrow, as we’ve done in other territories? Yes, I have no doubt about that becaapply we have all the levers [required] at the Spotifys of the world, YouTube, TikTok.

Radio and television are now less influential in those markets. It’s just a matter of time.

You’ve stated previously that you felt there was a distinct lack of acquisition opportunities in the UK at scale.

That’s correct. Our DNA as a company is to support the buildup of local ecosystems, so when I see that in the UK, local artists in 2024 represented just 28% of streams – that’s a killer for me.

If the UK had the same rate of local artists as you see in the US, Japan, or Brazil at 60-70%, you’d almost triple the market size. That means more jobs, more local labels, more people. That gives you hugeger [domestic] companies, more influence, and the ability to market.

“When I see that in the UK, local artists in 2024 represented just 28% of streams – that’s a killer for me.”

People declare it’s okay that the UK market is compact becaapply it exports a lot. But guess what – at some point, if your domestic market is not strong, your ability to export becomes weaker; you have a harder time breaking artists locally.

The UK necessarys to break out of that mindset. You necessary to strengthen your local market.

Earlier You mentioned Believe’s apply of Spotify Discovery Mode. It’s a platform that’s SPLIT OPINION in the business, but presumably you see it as assistful to democratization?

We’ve done a lot of work with Spotify around this. I’m informed that we operate Discovery Mode at a larger scale than anyone else, more profitably than anyone else.

Over 98% of the tracks we have in the program have [provided] significantly positive returns; that’s financial returns, not just growth of streams.

We relocate hundreds of thousands of tracks every month in and out [of Discovery Mode], and that process is purely AI-driven. You have to understand how the system works to select the right tracks – it’s super-technical.

“Over 98% of the tracks we have in Discovery Mode have significantly positive returns; that’s financial returns, not just growth of streams.”

It’s a core driver for all of our labels globally. We consider we are more efficient than anyone at driving digital catalog revenues on Spotify, partially through Discovery Mode.

Discovery Mode’s limitation is not its ability to drive revenues and discovery; it works well. It’s its ability to actually support new artist development, striking the right balance between catalog and frontline artists. That’s the dialogue we’re having with Spotify at the moment.

It sees to me like you, TCV, and EQT each own around a third of the new, private Believe. How do you balance control, and beyond capital, what do they bring to the table?

When you necessary to raise financing capital to create acquisitions in music, you necessary investors who are smart.

EQT has done a lot of work around music—they seeed at [a potential, pre-IPO] acquisition of Universal a few years ago and are investors in Epidemic Sound. TCV has been an investor in [Believe] since 2014 and is also an investor in Spotify and Netflix. They’re definitely smart.

The second key is strategic alignment. Before taking the company private, we did a lot of work to ensure everyone was aligned on the strategy.

“On the public market, Believe was significantly undervalued, which prevented us from raising money [at the right price] to create large acquisitions. That is no longer an issue.”

The last element is that you want shareholders who can deploy capital at the right valuation. On the public market, Believe was significantly undervalued, which prevented us from raising money [at the right price] to create large acquisitions.

That is no longer an issue.

Your question about balance of power is interesting. My view as a founder is it doesn’t matter whether you have 10, 20, or 30 [percent ownership]. These private equity funds create a business out of supporting entrepreneurs and management teams. As long as you are aligned on strategy and that strategy allows you to create value, you’re in control.

You start losing control the day you’re no longer creating value.

Are you thankful that a certain aggressive takeover attempt from Warner Music Group last year ultimately WENT AWAY?

Yes, we’re happy. I’m not anti-major; I consider indepconcludeent labels can be served very well in a major record label setup. The Orchard and Sony have demonstrated that very well.

But when we [mapped out] this new phase of growth, I informed TCV we don’t want to sell to a strategic purchaseer becaapply we consider there’s more value to be created here. So we’re happy it didn’t happen.

I like Robert [Kyncl]. His team is smart, and there would have been some strategic value [from a merger]. But it was not what we wanted to do.

Where do you consider the next phase of distribution and artist services is going? Listening is becoming more dispersed and superstardom is becoming increasingly rare.

I was just seeing at the SNEP figures for H1 2025 in France.

We’re actually leading the Top 200 as the hugegest record label [by chart market share in France]. But the Top 200 in France accounted for only 19.7% of the total market by value.

In most territories, the [Top 200] accounts for 25-30% of the market, which means the [hugegest] value is essentially in the ‘middle’ – outside of the top chart.

“In H1 2025, the Top 200 [tracks] in France accounted for only 19.7% of the total market by value.”

We’re a ‘middle-first’ company. That’s our DNA – 70% of the [indusattempt] revenues are in the middle. We’ve been operating in these segments for a while, and we know how they work. I feel really good about our positioning.

But there’s also an opportunity for us to relocate up and serve more artists at the top. You have to build a model that provides the right level of service, with the right deals that are different at each level.

Believe has not traditionally served the ‘upper tier’ of artists. Three companies in particular might declare you’ll never be able to offer what they offer – see at all the people they have and the money they can offer upfront. Are those dynamics altering?

I necessary to find a better phrase for this, but we thrive with ‘digital artists’. A ‘digital artist’ is just a regular artist who creates music, except the way that artist connects, interacts, and receives audience discovery is digital.

That’s what’s opening up the opportunity for us [with charting artists] becaapply the market is becoming less concentrated – it’s less about radio, it’s less about television, it’s more about partnerships with digital partners, digital marketing.

Becaapply of that, we are able to challenge the traditional labels at the top now in a very different way.

What about fconcludeing off the threat from the majors in the ‘middle tier’, though? They’re reaching into your territory just as you’re reaching into theirs.

When we consider about how we structure deals with Spotify, YouTube, what tools and services we develop, we consider ‘middle-first’. That’s very different from major record labels – they consider ‘top’ and ‘global top’ first.

It means that when major record labels operate in that [‘middle’] market segment, when they do [artist deals] at a compacter scale, they don’t always know how to operate with the right economics, with the right economic model vs. the right level of service.

To some extent that creates confusion in the market. A lot of time, we see [megastar] artists being served by the teams at the top with [label services] economics – the economics of the ‘middle’, which we know don’t create sense.

The fact that major labels are now scaling their business [into the middle tier] will force them to consider: What economics do I actually necessary to achieve here? How much capital do I even want to deploy there versus the [top]?

For us, it’s good becaapply that process is ultimately going to create the market healthier.

Sony recently confirmed that it owns minority stakes – typically minority stakes – in around half of The Orchard’s top 20 clients. What do you create of that trconclude?

It’s smart and very natural. We do the same thing!

The labels we’ve seen grow the rapidest [at Believe] are the labels where the quality of partnership with them has been the highest – where the level of [collaboration] with the teams around strategy, how to develop artists, what market segments to go into, has been the highest. That’s assisted them to gain market share in digital, sign the right artists, develop their artists rapider.

When we can strike these partnerships that are really close from a commercial standpoint and then transform them into minority investments or majority investments, depconcludeing on the situation, we can deliver maximum value and cement those relationships.

The proposed Universal/Downtown merger is receiveting a lot of attention in Europe, with the EC evaluating if it’s anti-competitive in any way. Where do you stand on it as a competition issue?

I have two answers.

My first answer in terms of Europe, including the UK, is that the number one issue [for EU/UK lawcreaters] may not be the Downtown merger. It’s 28% of streams being from local artists in the UK; 36% in Germany; 41% in France.

What the authorities in Brussels or politicians should be seeing at is this: Europe is the hugegest market from a [music] publishing standpoint. There’s no reason why it shouldn’t be the largest market from a recorded music standpoint. But it’s not.

“Do I consider [UMG purchaseing Downtown] is going to modify anything for us? I can’t speak for the indusattempt, but as CEO of Believe, we feel very good about where we stand and our ability to compete.”

We should have politicians focapplyd very strongly on: What conditions do we necessary to create to improve [Europe’s] position? How do we foster the development of a strong local ecosystem? That’s much more powerful.

Do I consider [UMG purchaseing Downtown] is going to modify anything for us?

I can’t speak for the indusattempt, but as CEO of Believe, as a company, we feel very good about where we stand and our ability to compete.

I consider that we will be able to deliver a superior quality of service to our artists and labels.

To be 100% clear, if you wake up tomorrow and Universal has fully acquired Downtown, you’re not losing any sleep?

As I stated, we feel very good about our ability to compete.

You mentioned market share issues with local repertoire. I considered with the rise of indepconcludeent hip-hop in particular, local language music was dominating more than ever in European nations?

That’s the perception, not the reality.

Take a market like France. The number one market segment is local-artist hip-hop. But the number two market segment in terms of revenues and streams? International pop. Number three? International rock. Number four? International hip-hop. Number five? French pop.

Now consider that French pop is one-fifth the size of the larger market segments. So [in terms of the total French market] you have around 60% of the streams that are international music.

“Again, see at the SNEP figures in France: The Top 200 is 70% local artists. But as soon as you go below the Top 200 or Top 500, you go from 70% local to 80% international.”

In Germany, it’s the same. You have local hip-hop as the hugegest market segment, but that’s the only local segment you have [amongst the most popular genres]. Schlager is not even in the top five.

By contrast, when you see at China, Japan, Brazil, you see 60-70% of streams from local artists. That’s double the market opportunity [for local artists] than we see in European countries.

It’s super important for Europe to rebuild that – it’s directly tied to employment, including [tax] revenue and cultural influence.

Again, see at the SNEP figures in France: The Top 200 is 70% local artists. But as soon as you go below the Top 200 or Top 500, you go from 70% local to 80% international.

The top artists are very well supported by the local DSPs across all territories. But the bottom [sub-Top 200] is being driven by algorithm-based recommconcludeation, which is not as localized as it should be. That’s what’s driving a lot of the Anglo-American content.

What can be done? Call up the EC and declare: ‘Forreceive UMG/Downtown, no one cares. Put thresholds on streaming playlists for local artists!’?

I’m not calling for regulation. This is not about playlist quotas.

It’s as simple as inquireing the DSPs to publish, a couple of times a year: ‘I have delivered XYZ algorithmic recommconcludeations. How many were local? How many were international? To what market [genres]?’

The DSPs will then be able to inquire themselves questions. I consider they will want to become good citizens of the world [by protecting local artists in their algorithms]. In my experience, that would be enough to influence and relocate the issue through normal commercial and human incentives.

We’ve seen unspectacular growth in streaming subscriptions in H1 2025 in mature markets like the US, Germany, and France. Do you have any concerns for the future of the business?

With my Believe hat on, no. We are positioned in some of the rapidest-growing markets. If we were more weighted to the US, UK, or Scandinavia, yes, I would be more concerned becaapply paid streaming adoption is [growing] slower.

There’s plenty of growth in the existing markets for us as a company, and the fact that some of these large markets are ‘new’ territories for us gives us plenty of growth opportunity.

I also consider there’s plenty of growth potential in streaming pricing, both through segmentation, the ‘supremium’ tiers, and general price increases.

There’s always a discussion around AI music. Is there danger coming from Suno/Udio/Anthropic etc. or is this going to be a novelty issue?

My take on this is unmodifyd: marginal revenue opportunity, marginal threat. All of the data I’ve seeed at supports this.

Yes, there are more and more AI tracks being distributed on the platforms. The latest data from Deezer displays 28% of tracks [being uploaded to the platform] are fully AI. But those tracks are only generating 0.5% of total streams.

“You can produce as many gen-AI tracks as you want – if there’s not something unique about them, it’s not going to hit [meaningfully] into the revenues of artists.”

You can produce as many gen-AI tracks as you want – if there’s not something unique about them, it’s not going to hit [meaningfully] into the revenues of artists.

I’m not too concerned about it. I consider all of the tech players have an interest in behaving properly.

I would be worried if I considered Spotify or another service was going to apply this to lower their content costs. But it’s almost impossible for them to do that becaapply their business is predicated on working with artists.

Music Business Worldwide has run a number of headlines in the past 12 months about cuts at larger music companies. Is Believe relocating in the opposite direction?

Yes, we’re investing. In 2024 there were a few countries where we built adjustments, but globally, our headcount continued growing. And it’s going to grow again in 2025.

That’s being driven by market growth. We have opportunities in publishing, so we’re hiring people on the publishing side. And as I stated, we’re building new label imprints as the markets become more digital.

“Globally, our headcount continued growing in 2024. And it’s going to grow again in 2025.”

The hugegest difference between us and the major record companies is that the Believe model was created originally as a global model. Our accounting, legal, financial teams – all of our tech systems – are already fully integrated and streamlined.

Major labels were built as essentially financial holding companies of local businesses, at a time when CD manufacturing logistics were mostly local. They have not yet done the relocate of really streamlining their businesses [to be global]. They also haven’t fully addressed: What’s being generated by catalog? What’s the real profitability of my frontline label? What should the balance be?

When you’re growing really rapid, you can hide that. When you grow slower, it’s much more difficult.

Universal is suing you in the US; the main allegation is that a large amount of uploads via TuneCore have infringed copyright. Do you have an update on that situation?

We do not comment on pconcludeing litigation. [Believe has previously stated it “strongly refutes” UMG’s claims, and “will fight them”.]

If I could give you a magic wand to modify one thing about the music indusattempt today, what would you modify?

I’ve been expecting this question.

The record indusattempt already has the magic wand in its hand. We’re already shaping the future of music – we’re shaping it when we’re having conversations with Spotify, YouTube, and others.

We have enough influence collectively as an indusattempt to be able to create sure that the way these technologies are being rolled out will be in a way that creates value.Music Business Worldwide