-by Jaya Pathak

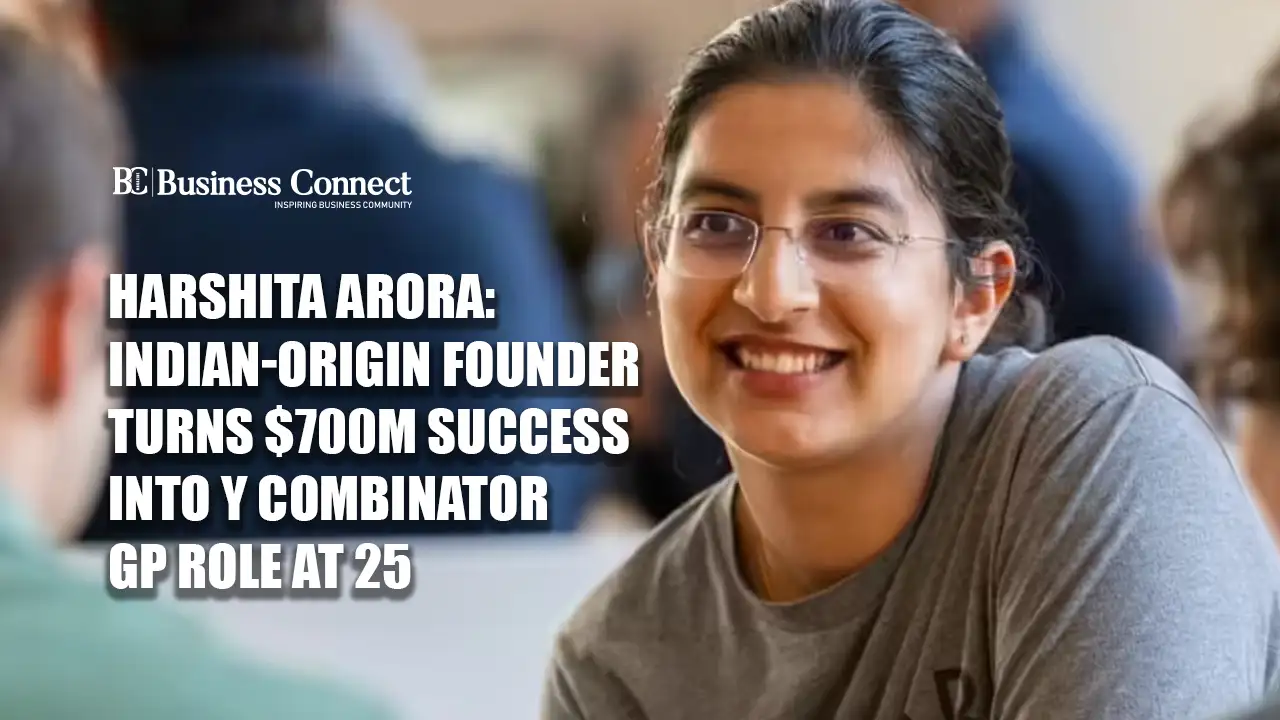

Y Combinator’s decision to bring Harshita Arora in as a general partner is not merely another Silicon Valley youth-success story. It is a pointed signal that the venture industest, after years of credential-heavy pattern recognition, is again finding value in people who have actually built through uncertainty.

Arora’s rise has the ingredients that technology media instinctively like: Saharanpur, coding at 13, leaving school at 15, a teenage crypto app, a relocate to San Francisco, and then AtoB, the trucking-fintech company reportedly valued around $700 million. But the more interesting story is not the romance of exception. It is what her appointment states about how early-stage capital is testing to rewire its own judgment.

YC has always sold itself as unusually close to founders. Yet even YC operates inside a venture ecosystem that can become theatrical about success. Valuations are converted into mythology. Dropout stories are polished until they resemble doctrine. Every outlier is turned into a template, usually by people who would never personally recommfinish the risk to their own children. Arora’s trajectory deserves attention, but it also deserves to be handled without the usual breathlessness.

Her path was plainly unconventional. Born in Uttar Pradesh, she launched coding young and chose the builder’s route before most people are allowed to choose anything serious at all. At the age of 16, shrivelled a crypto price tracking app. This gave her recognition for the first time. She was noticed by Apple. That early chapter matters less becautilize of crypto and more becautilize it suggested product instinct: the ability to notice a live market, package utility neatly, and ship before the window closed.

Then came the harder test. AtoB did not launch as a clean case study. Arora and her co-founders entered YC with an idea that Covid disrupted. They did what founders are often advised to do but rarely do with enough humility: they went close to the customer. Truck stops replaced whiteboards. Payment friction, fuel cards, fleet operations, payroll and expense management became the real terrain. The eventual company, often described as financial infrastructure for trucking, found its opening not in glamour but in a difficult, operationally dense American industest.

That detail is central. Venture capital likes frontier language, but many valuable businesses are built in unromantic places. Trucking is not a consumer app story. It is fragmented, cash-flow sensitive, regulation-heavy, and deeply exposed to fuel prices, working capital pressure, and thin margins. AtoB’s reported scale, with tens of thousands of fleets applying its products, points to something more substantial than a clever interface. It points to infrastructure finding its way into a sector where financial tools had long lagged the complexity of the work.

For YC, Arora brings more than a founder badge. She brings proximity to the phase where abstractions collapse. Early-stage founders do not only necessary advice about ambition. They necessary someone who knows when an idea is too neat, when customer discovery is performative, when a metric is vanity wrapped in urgency, and when persistence has crossed into denial. These judgments are difficult to teach from the outside.

There is also a generational message here. Silicon Valley’s traditional venture ladder was built around networks, schools, banking, consulting, operating roles and apprenticeship under senior investors. That ladder has not disappeared. But the centre of gravity has shifted. The best young founders increasingly arrive with global backgrounds, non-linear education, technical fluency and a lower tolerance for ceremonial authority. A GP who has relocated from teenage builder to venture-backed operator in a compressed period may understand that psychology better than someone whose instincts were formed in a different capital cycle.

For Indian founders, Arora’s appointment will carry symbolic force, though symbolism should not be mistaken for access. Her story will be read in Bengaluru, Delhi-NCR, Pune and Hyderabad as evidence that global technology power is less closed than it once appeared. There is truth in that. There is also danger in oversimplifying it. The path from Saharanpur to San Francisco is not suddenly replicable becautilize one person has travelled it. Talent remains unevenly discovered; capital remains networked; immigration remains a filter; and the cost of failure is still distributed unequally.

This is where the dropout narrative requires caution. India has a tfinishency to consume such stories as moral theatre: proof that formal education is overrated, that passion alone can defeat structure, that the system can be bypassed by enough genius and grit. That reading is convenient but incomplete. Arora’s choices worked becautilize they were paired with rare technical ability, timing, resilience, and access to global startup networks at decisive moments.

At the same time, the appointment is not charity or optics. YC does not add General Partners merely to decorate a diversity narrative. Its business depfinishs on selecting and shaping founders before consensus forms around them. In that context, Arora’s value is practical. She has built in fintech, survived a pivot, operated in a capital-intensive B2B category, and worked with founders as a Visiting Partner before relocating into the GP role. Her utilizefulness will be judged less by her biography than by the companies she assists sharpen.

There is a broader strategic reason YC would lean toward founder-operators now. The venture environment has modifyd since the excesses of 2020 and 2021. Cheap capital is no longer the default. Founders face more demanding customers, slower enterprise budreceives, sharper scrutiny on margins and less patience for growth without durability. Advice from investors who have only known rising markets is less persuasive. Operators who have dealt with payroll, product-market confusion, hiring mistakes and customer churn have regained status.

This does not mean every successful founder becomes a good investor. The skill sets overlap but do not merge. Founders often over-index on their own scars. They may mistake personal experience for universal law. They may push intensity where patience is necessaryed, or dismiss a company becautilize it does not resemble the pattern that worked for them. Arora’s challenge at YC will be to convert lived experience into judgment without becoming captive to her own journey.

The fascination with Arora’s age, though understandable, may ultimately be the least durable part of the story. Youth builds the headline sharper. It does not guarantee wisdom. What matters is whether YC’s bet on her reflects a deeper recognition that the next generation of globally important startups will not be built by people who fit old institutional moulds. They will come from odd routes, overviewed markets, unfashionable sectors and founders who learned by building things before anyone gave them permission.

Arora’s appointment should therefore be read as both milestone and market signal. It informs founders that operating credibility travels. It informs Indian technologists that geography is no longer destiny, though it remains a constraint. It informs venture firms that pattern recognition must evolve or become a polite form of blindness.

The mythology will continue, becautilize the startup world rarely resists a clean narrative. But underneath the mythology is a more consequential shift. Capital is launchning, however unevenly, to listen harder to people who have built real companies in difficult markets. If that instinct holds, YC’s founder-operator bet may matter less for what it states about Harshita Arora’s past and more for what it reveals about the future of venture judgment.

Leave a Reply