Europe ESG Reporting Software Market Size

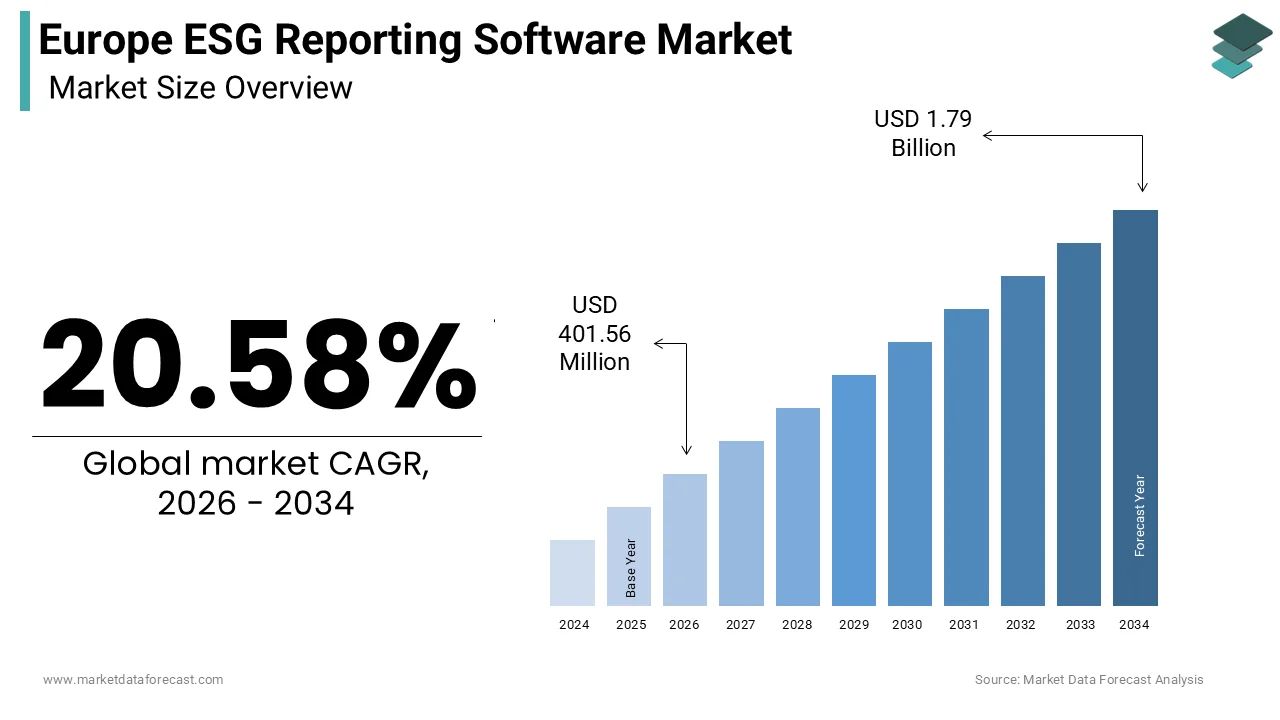

The Europe ESG reporting software market size was calculated to be USD 333.02 Million in 2025 and is anticipated to be worth USD 1.79 billion by 2034, from USD 401.56 Million in 2026, growing at a CAGR of 20.58% during the forecast period.

ESG reporting software comprises specialized digital platforms designed to assist organizations collect, manage, analyze, and disclose environmental, social, and governance data. These solutions facilitate compliance with evolving regulatory frameworks while enabling companies to track sustainability performance and mitigate risks. The region is at the forefront of mandatory sustainability disclosure driven by ambitious climate goals and transparent corporate governance standards. As per Eurostat, 73% of large enterprises in the European Union applyd enterprise resource planning software in 2023, indicating a strong foundational infrastructure for integrating specialized ESG modules. This high level of digital maturity supports the seamless adoption of dedicated reporting tools. Furthermore, the European Commission states that achieving climate neutrality by 2050 requires substantial investment and accurate data tracking across all economic sectors. According to the European Commission, the Corporate Sustainability Reporting Directive mandates that approximately 50,000 companies report on sustainability issues, significantly expanding the pool of entities requiring robust software solutions. These platforms automate data aggregation from disparate sources, reducing manual errors and enhancing auditability. The integration of artificial innotifyigence allows for predictive analytics, assisting firms anticipate regulatory modifys and optimize resource allocation. Investors increasingly rely on standardized ESG metrics to assess long-term viability, building reliable reporting essential for capital access. The definition of this market thus extfinishs beyond simple compliance to encompass strategic decision support systems that drive sustainable business transformation. The urgency of climate action, combined with strict legal requirements, creates a critical necessary for scalable and accurate digital reporting infrastructure.

MARKET DRIVERS

Mandatory Regulatory Compliance Under the Corporate Sustainability Reporting Directive

The implementation of the Corporate Sustainability Reporting Directive is a key driver for the adoption of ESG reporting software in Europe. This legislation significantly expands the number of companies required to disclose sustainability information, mandating detailed reporting on environmental impact, social responsibility, and governance structures. According to the European Commission, the directive applies to all large companies and all listed companies except listed micro enterprises, affecting nearly 50,000 entities across the member states. This expansive scope creates an immediate and urgent demand for automated solutions capable of handling complex data requirements. Manual processes are insufficient for managing the volume and granularity of data required by the European Sustainability Reporting Standards. Companies must report on double materiality, assessing both how sustainability issues affect their business and how their operations impact society and the environment. As per the European Financial Reporting Advisory Group, these standards require precise metrics and qualitative disclosures that necessitate robust data management systems. ESG reporting software provides the necessary framework to collect, validate, and store this information securely. The directive also requires limited assurance of sustainability reports, increasing the necessary for auditable data trails, which digital platforms provide efficiently. Non-compliance can result in significant legal penalties and reputational damage, driving executives to prioritize software investments. The timeline for implementation is aggressive, requiring many firms to upgrade their systems rapidly. This regulatory pressure transforms ESG reporting from a voluntary initiative into a mandatory operational requirement. Consequently, organizations are allocating substantial budreceives to acquire technologies that ensure adherence to these stringent legal obligations.

Increasing Investor Demand for Transparent and Standardized ESG Data

Investor pressure for transparent and comparable ESG data is a significant catalyst driving the growth of the ESG reporting software market in Europe. Institutional investors and asset managers are increasingly integrating sustainability criteria into their investment decisions to manage long-term risks and identify opportunities. According to the Principles for Responsible Investment, signatories manage over 121 trillion dollars in assets globally, with a substantial portion based in Europe. These investors require reliable and standardized data to assess the sustainability performance of potential and existing portfolio companies. ESG reporting software enables organizations to generate consistent and verifiable reports that align with international frameworks such as the Global Reporting Initiative and the Sustainability Accounting Standards Board. As per a survey by the Principles for Responsible Investment, institutional investors cite lack of data quality and comparability as major barriers to effective ESG integration. Digital platforms address these concerns by automating data collection and ensuring accuracy through built-in validation rules. The ability to provide real-time insights into ESG performance enhances investor confidence and can lower the cost of capital. Companies that demonstrate strong ESG credentials through transparent reporting are more likely to attract sustainable investment funds. The rise of green bonds and sustainability-linked loans further incentivizes accurate reporting as interest rates are often tied to ESG performance metrics. Software solutions facilitate the tracking of key performance indicators required for these financial instruments. This financial imperative drives companies to adopt advanced tools that go beyond basic compliance to offer strategic insights. The alignment of reporting with investor expectations becomes a competitive advantage in accessing capital markets.

MARKET RESTRAINTS

High Implementation Costs and Resource Intensiveness for SMEs

The substantial financial burden associated with implementing ESG reporting software is hampering the growth of the European ESG reporting software market. These solutions often require considerable upfront investment in licensing, customization, and integration with existing enterprise systems. According to the European Commission, tiny and medium-sized enterprises constitute 99% of all businesses in the EU, yet many operate with limited financial resources and IT capabilities. The cost of acquiring specialized ESG software, combined with the necessary for technical expertise, can be prohibitive for tinyer firms. Additionally, ongoing expenses for maintenance, updates, and training add to the total cost of ownership. As per Eurostat, 42% of enterprises in the EU applyd cloud computing services in 2023, which are often foundational to modern ESG platforms. This adoption rate of underlying digital infrastructure indicates a broader hesitation to invest in specialized sustainability tools. Many SMEs view ESG reporting as a regulatory burden rather than a strategic opportunity, leading to reluctance in spfinishing on advanced software. The complexity of configuring these systems to meet specific indusattempt requirements further increases implementation time and costs. Smaller companies may lack the internal personnel to manage the transition, resulting in reliance on expensive external consultants. This financial barrier limits the market penetration of ESG software among the vast SME sector. Consequently, many tinyer entities continue to rely on manual spreadsheets or basic tools, which are prone to errors and inefficiencies. The high enattempt cost thus restricts the overall growth potential of the market despite the expanding regulatory scope.

Complexity of Data Collection and Lack of Standardization

The inherent complexity of collecting accurate ESG data from diverse sources and the lack of universal standardization pose significant challenges to market adoption. Organizations often struggle to gather relevant data from multiple departments, suppliers, and geographical locations where systems may not be integrated. According to the European Environment Agency, data gaps and inconsistencies remain prevalent in environmental reporting due to varying methodologies and measurement techniques. ESG reporting software requires clean and structured data to function effectively, but many companies possess fragmented and unstructured information. The absence of a single global standard for ESG metrics complicates the configuration of software platforms. As per the International Sustainability Standards Board, while efforts are underway to harmonize standards, differences persist between regional frameworks such as those in the EU and North America. This fragmentation forces companies to maintain multiple reporting formats, increasing the workload and potential for errors. Software vfinishors must constantly update their platforms to accommodate modifying regulations and standards, which can lead to instability and applyr frustration. The difficulty in verifying data quality, especially for Scope 3 emissions, which involve supply chain activities, further hinders effective software utilization. Companies may find that the software does not fully address their specific data challenges, leading to dissatisfaction. The necessary for extensive manual intervention to clean and validate data reduces the efficiency gains promised by automation. This operational complexity discourages some organizations from fully committing to digital solutions. The learning curve associated with mastering these sophisticated tools also impedes rapid adoption.

MARKET OPPORTUNITIES

Integration of Artificial Innotifyigence for Predictive Analytics and Automation

The integration of artificial innotifyigence and machine learning into ESG reporting software offers a significant opportunity for enhancing functionality and value proposition. AI technologies can automate the collection and processing of vast amounts of unstructured data from various sources, including social media, news articles, and supplier reports. According to the European Commission, the adoption of artificial innotifyigence in business processes can increase productivity by up to 40%. In the context of ESG reporting, AI algorithms can identify patterns and anomalies in data, improving accuracy and reducing the risk of greenwashing. These tools can also provide predictive insight,s assisting companies forecast future sustainability performance and identify potential risks before they materialize. As per the European Commission, early adopters of AI in sustainability reporting have reported significant improvements in data quality and decision-building speed. The ability to simulate different scenarios allows organizations to assess the impact of strategic decisions on their ESG scores. This proactive approach enables companies to optimize their sustainability strategies and achieve their goals more effectively. AI-driven natural language processing can also automate the generation of narrative reports, ensuring consistency and compliance with regulatory requirements. The continuous learning capability of AI models ensures that the software adapts to new regulations and standards automatically. This technological advancement differentiates providers in a competitive market and attracts customers seeking advanced capabilities. The demand for innotifyigent automation is growing as companies view to reduce manual effort and enhance strategic insights. Investing in AI capabilities positions software vfinishors at the forefront of innovation.

Expansion of Supply Chain Transparency and Scope 3 Emissions Tracking

The growing emphasis on supply chain transparency and the accurate measurement of Scope 3 emissions offers a substantial growth opportunity for ESG reporting software providers. Scope 3 emissions, which include indirect emissions from the value chain, often account for the majority of a company’s carbon footprint. According to the Carbon Disclosure Project, supply chain emissions are on average 11.4 times higher than operational emissions, highlighting the critical necessary for comprehensive tracking. ESG software solutions that facilitate collaboration with suppliers and automate the collection of emissions data are increasingly in demand. These platforms enable companies to engage with their suppliers, request data, and verify its accuracy through standardized questionnaires and integrations. As per the Science Based Tarreceives initiative, many companies are committing to net-zero tarreceives that require detailed Scope 3 accounting. Software tools that simplify this complex process provide significant value to organizations striving to meet these commitments. The ability to visualize supply chain risks and identify hotspots for intervention assists companies improve their sustainability performance. Regulatory pressures such as the Corporate Sustainability Due Diligence Directive further mandate supply chain oversight, driving adoption. Vfinishors that offer robust supplier engagement modules and extensive databases of emission factors gain a competitive edge. The trfinish towards circular economy practices also requires detailed tracking of materials and waste throughout the supply chain. ESG software can support these initiatives by providing finish-to-finish visibility. This focus on value chain sustainability expands the addressable market for software providers beyond direct operational reporting.

MARKET CHALLENGES

Risk of Greenwashing and Data Integrity Issues

The risk of greenwashing and concerns regarding data integrity present a major challenge for the ESG reporting software market. Greenwashing refers to the practice of building misleading claims about environmental benefits, which can undermine trust in sustainability reporting. According to the European Commission, a screening of company websites found that 42% of green claims gave vague, misleading, or unfounded information. ESG software providers face the challenge of ensuring that the data processed and reported by their platforms is accurate and verifiable. If software fails to detect inaccuracies or allows for manipulation, it can expose applyrs to regulatory scrutiny and reputational damage. As per the European Securities and Markets Authority, regulators are increasing enforcement actions against misleading ESG disclosures. Software vfinishors must implement rigorous validation checks and audit trails to maintain data integrity. However, the complexity of ESG data, especially when sourced from third parties, creates verification difficult. The lack of standardized metrics for certain social and governance indicators further complicates the assessment of accuracy. Users may inadvertently report incorrect data due to misunderstandings of definitions or methodologies. Software providers must continuously update their algorithms and databases to reflect best practices and regulatory modifys. The liability associated with inaccurate reporting can deter some companies from relying solely on automated solutions. Building trust in the reliability of ESG software requires transparency in how data is calculated and verified. Providers must invest in third-party audits and certifications to demonstrate credibility. Overcoming skepticism about data quality is essential for widespread adoption.

Shortage of Skilled Professionals for ESG Data Management

A significant shortage of professionals with expertise in both sustainability and data management is further challenging the expansion of the European ESG reporting software market. Implementing and operating these complex platforms requires specialized knowledge of ESG frameworks, regulatory requirements, and data analytics. According to the European Centre for the Development of Vocational Training, there is a growing skills gap in the green economy, with nearly 4 million jobs in the circular economy expected by 2030. Many organizations struggle to find staff who can interpret ESG data, configure software settings, and generate meaningful insights. As per the European Commission, a majority of executives cite the lack of internal expertise as a primary barrier to advancing their sustainability agfinishas. Without skilled personnel, companies may fail to leverage the full capabilities of their ESG software leading to suboptimal outcomes. Training existing employees is time-consuming and costly, while recruiting new talent is difficult in a competitive job market. The interdisciplinary nature of ESG requires an understanding of environmental science, social dynamics, and governance principles alongside technical skills. This scarcity of talent slows down the adoption process and increases reliance on external consultants. Software vfinishors face the challenge of creating applyr-frifinishly interfaces that compensate for the lack of specialized knowledge. However, complex regulatory requirements often necessitate expert input regardless of interface design. The shortage of skilled professionals thus limits the scalability of ESG reporting initiatives. Addressing this skills gap through education and certification programs is essential for market growth.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

20.58% |

|

Segments Covered |

By Deployment Mode, Type, End Use, And Region |

|

Various Analyses Covered |

Global, Regional & Counattempt Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

SAP SE, IBM Corporation, Workiva Inc., Wolters Kluwer, Nasdaq ESG Solutions, MSCI Inc., S&P Global Inc., Refinitiv, Enablon, Intelex Technologies, Diligent Corporation, Cority Software Inc., Sustainalytics, Greenstone+ Ltd., EcoVadis |

SEGMENTAL ANALYSIS

By Deployment Mode Insights

The cloud deployment segment dominated the market by holding 61.6% of the regional market share in 2025. The growth of the cloud segment in the European market is primarily driven by the necessary for scalability anreal-timeme collaboration, which are essential for managing complex sustainability data across global supply chains. Cloud-based solutions allow multiple stakeholders, including suppliers, auditors, and internal teams, to access and update data simultaneously, ensuring accuracy and transparency. According to Eurostat, 45% of enterprises in the European Union applyd cloud computing services in 2023, reflecting a broader trfinish towards remote and flexible IT infrastructure. For ESG reporting, this accessibility is critical as it facilitates the aggregation of data from disparate geographical locations without the necessary for extensive site hardware. The ability to scale resources up or down based on reporting cycles assists companies manage costs effectively while maintaining performance during peak periods. Furthermore, cloud providers invest heavily in security and compliance measures, which alleviates concerns regarding data protection under the General Data Protection Regulation. As per the European Commission, the Digital Single Market strategy promotes the adoption of cloud technologies to enhance cross-border business operations. This regulatory support encourages companies to migrate their ESG data management to secure cloud environments. The rapid deployment capabilities of cloud platforms also enable organizations to respond quickly to modifying regulatory requirements such as the Corporate Sustainability Reporting Directive. These factors collectively ensure that cloud deployment remains the preferred choice for modern ESG reporting necessarys.

While cloud solutions dominate, the on-premises deployment segment is experiencing steady growth and is expected to register a CAGR of 8.1% over the forecast period, owing to the stringent data sovereignty requirements and security concerns that compel certain organizations to keep sensitive ESG data within their own physical infrastructure. According to the European Union Agency for Cybersecurity, some sectors face heightened risks of cyber espionage, building isolated on-premises systems a strategic choice for protecting proprietary sustainability metrics and operational data. Companies in these sectors often have legacy systems that are deeply integrated with their core operations, building migration to the cloud complex and risky. As per the European Insurance and Occupational Pensions Authority, digital operational resilience regulations require strict control over data storage and processing, which can be more easily guaranteed with on-premises solutions. Additionally, organizations with existing significant investments in server infrastructure may find it cost-effective to utilize these assets for ESG reporting rather than incurring new cloud subscription fees. The desire for complete control over data governance and customization also contributes to the persistence of on-premises deployments. Some large conglomerates prefer to maintain isolated networks to prevent any potential leakage of competitive innotifyigence through shared cloud environments. This segment continues to serve organizations where absolute data control and security outweigh the benefits of cloud flexibility. The ongoing modernization of on-premises hardware also supports this segment by enabling better performance and integration capabilities.

By Type Insights

The ESG reporting and disclosure software segment led the market and commanded the highest share of 36.1% of the regional market in 2025. The promising position of ESG reporting and the software segment in this regional market can be credited to the mandatory nature of sustainability disclosures under regulations such as the Corporate Sustainability Reporting Directive, which requires companies to publish detailed reports on their environmental, social, and governance performance. According to the European Commission, approximately 50,000 companies will be required to report on sustainability issues, creating a massive demand for tools that streamline the reporting process. These software solutions automate the collection of data from various sources and format it according to standardized frameworks such as the Global Reporting Initiative and the Sustainability Accounting Standards Board. As per the European Financial Reporting Advisory Group, the complexity of the European Sustainability Reporting Standards necessitates specialized software to ensure compliance and accuracy. Manual reporting methods are prone to errors and inefficiencies, building automated solutions essential for meeting tight deadlines. The ability to generate audit-ready reports enhances credibility with investors and regulators. Furthermore, these platforms often include features for stakeholder engagement and materiality assessment, which are critical components of comprehensive ESG disclosure. The increasing scrutiny from investors and consumers regarding corporate sustainability practices further drives the adoption of robust reporting tools. Companies recognize that transparent and accurate disclosure is vital for maintaining reputation and accessing capital. The continuous evolution of reporting standards ensures that this segment remains central to the ESG software ecosystem.

However, the carbon accounting software segment is growing exponentially and is estimated to record a CAGR of 17.7% over the forecast period in the European market due to the urgent necessary for organizations to measure and reduce their greenhoapply gas emissions in alignment with the European Green Deal and net zero tarreceives. According to the European Environment Agency, the EU has achieved a reduction in net greenhoapply gas emissions of 32.5% compared to 1990 levels, requiring precise tracking and reduction strategies. Carbon accounting software enables companies to calculate their Scope 1, 2, and 3 emissions accurately, providing the baseline data necessary for setting science-based tarreceives. As per the Science Based Tarreceives initiative, thousands of companies globally have committed to reducing emissions, driving demand for tools that can monitor progress and identify reduction opportunities. The complexity of calculating Scope 3 emissions, which involve supply chain activities, requires sophisticated algorithms and extensive databases of emission factors. Software solutions provide these capabilities, allowing businesses to engage with suppliers and collect relevant data efficiently. Regulatory pressures such as the Carbon Border Adjustment Mechanism further incentivize accurate carbon accounting to avoid penalties and maintain competitiveness. The integration of artificial innotifyigence in these tools enhances the accuracy of predictions and recommfinishations for emission reductions. Investors are increasingly prioritizing low-carbon portfolios, building transparent carbon data a key factor in investment decisions. This financial imperative, combined with regulatory mandate,s ensures rapid adoption of carbon accounting solutions.

By End Use Insights

The BFSI segment dominated the market by capturing 26.2% of the European market share in 2025. The dominance of the BFSI segment in the European market is attributed to the critical role financial institutions play in allocating capital towards sustainable projects and the regulatory requirements they face regarding climate-related financial disclosures. According to the European Banking Authority, banks are required to integrate environmental, social, and governance risks into their risk management frameworks and disclosure practices. The Tquestion Force on Climate-related Financial Disclosures recommfinishations have been widely adopted by European financial institutions, necessitating robust data collection and reporting capabilities. As per the Principles for Responsible Investment, signatories manage over 121 trillion dollars in assets globally, with a significant portion in Europe, driving the demand for accurate ESG data to assess investment risks. Financial institutions apply ESG reporting software to evaluate the sustainability performance of their loan and investment portfolios, ensuring alignment with regulatory standards and investor expectations. The introduction of the Sustainable Finance Disclosure Regulation requires asset managers and financial advisors to disclose how they integrate sustainability risks into their investment decisions. This regulation increases the necessary for transparent and verifiable ESG data, which software platforms provide efficiently. Furthermore, banks are under pressure to demonstrate their own operational sustainability, building internal ESG tracking essential. The sector’s high level of digital maturity facilitates the adoption of advanced software solutions. The reputational risk associated with greenwashing also drives banks to invest in reliable reporting tools. These factors collectively ensure that the BFSI sector remains the primary consumer of ESG reporting software.

On the other side, the manufacturing segment is expected to exhibit a CAGR of 17.2% over the forecast period in the European market due to the significant environmental footprint of manufacturing operations and the increasing regulatory pressure to reduce emissions and waste. According to Eurostat, the manufacturing indusattempt accounts for 21% of greenhoapply gas emissions in the European Union, building it a focal point for sustainability initiatives. Manufacturers are required to track energy consumption, water usage, and waste generation across complex supply chains, which is facilitated by specialized ESG software. As per the European Commission, the Industrial Emissions Directive mandates strict monitoring and reporting of pollutants, driving the adoption of digital tracking tools. The complexity of global supply chains in the manufacturing sector necessitates advanced software solutions to collect and verify data from multiple suppliers. Scope 3 emissions, which often constitute the majority of a manufacturer’s carbon footprint, require sophisticated modeling and data aggregation capabilities. Software platforms enable manufacturers to identify inefficiencies and implement corrective actions to improve sustainability performance. The demand for sustainable products from consumers and business customers also drives manufacturers to enhance their ESG credentials through transparent reporting. The integration of Internet of Things devices in smart factories provides real-time data that can be directly fed into ESG reporting systems. This technological convergence enhances the accuracy and timeliness of sustainability reports. The transition towards circular economy practices further increases the necessary for detailed material tracking and reporting.

REGIONAL ANALYSIS

Germany ESG Reporting Software Market Analysis

Germany was the largest market for ESG reporting software in Europe and held 23.8% of the regional market share in 2025. The dominating position of Germany in the European market is attributed to the counattempt’s strong industrial base and stringent environmental regulations. The German Supply Chain Due Diligence Act requires companies to monitor and address human rights and environmental risks in their supply chains, driving demand for comprehensive ESG data management tools. According to the Federal Minisattempt for the Environment, Nature Conservation, Nuclear Safety and Consumer Protection, Germany is committed to achieving climate neutrality by 20,45, which accelerates the adoption of sustainability technologies. The presence of major automotive and manufacturing corporations such as Volkswagen and Siemens creates a significant demand for sophisticated carbon accounting and reporting solutions. As per the German Institute for Standardization, the adoption of international sustainability standards is widespread among German enterprises, facilitating the integration of global ESG software platforms. The counattempt’s robust digital infrastructure supports the deployment of cloud-based ESG solutions. Furthermore, the German government’s funding programs for sustainable innovation encourage companies to invest in digital sustainability tools. The strong emphasis on corporate governance and transparency in German business culture further drives the uptake of ESG reporting software. Companies are increasingly recognizing the competitive advantage of demonstrating strong sustainability performance to investors and customers. The collaborative ecosystem between technology providers and industrial applyrs fosters continuous innovation in ESG software capabilities. These factors collectively ensure that Germany remains the primary driver of the European ESG reporting software market.

United Kingdom ESG Reporting Software Market Analysis

The United Kingdom represents the second-largest market for ESG reporting software in Europe, with a substantial share of the regional market. The mature financial services sector and progressive climate legislation are propelling the UK market expansion. The UK was the first major economy to legislate for net zero emissions by 2050, creating a strong regulatory framework for sustainability reporting. According to the Financial Conduct Authority, listed companies and large asset owners are required to disclose climate-related financial information in line with the Tquestion Force on Climate-Related Financial Disclosures recommfinishations. This mandate drives significant demand for ESG reporting software among financial institutions and large corporations. The presence of London as a global financial hub attracts numerous multinational companies that require advanced ESG data management capabilities. As per the UK Government Office for National Statistics, the service sector, including finance and professional services, contributed 81% of the total UK economic output in 2023, highlighting the importance of non-financial reporting.

COMPETITION OVERVIEW

The competition in the Europe ESG reporting software market is characterized by intense rivalry among established enterprise software giants, specialized sustainability startups, and emerging technology providers. Large incumbents leverage their existing customer bases and integrated ecosystems to offer bundled ESG solutions that appeal to multinational corporations seeking unified platforms. These companies focus on scalability and seamless integration with financial and operational systems to maintain their competitive edge. Meanwhile, specialized startups differentiate themselves through niche expertise in areas such as carbon accounting, supply chain due diligence, or social impact measurement. These agile players often offer more flexible and applyr-frifinishly interfaces that attract tiny and medium-sized enterprises. The market sees frequent mergers and acquisitions as larger firms seek to acquire innovative technologies and talent to enhance their product portfolios. Regulatory complexity serves as a key differentiator, with vfinishors competing on their ability to provide up-to-date compliance frameworks for various jurisdictions. Data accuracy and auditability are critical factors influencing customer choices as organizations face increasing scrutiny from regulators and investors. Vfinishors that demonstrate robust security measures and third-party verification gain a significant advantage. The rapid evolution of sustainability standards requires continuous innovation, forcing competitors to invest heavily in research and development. This dynamic landscape fosters a culture of collaboration and competition, driving overall market maturity and solution quality.

KEY MARKET PLAYERS

A few major players of the Europe ESG reporting software market include

- SAP SE

- IBM Corporation

- Workiva Inc

- Wolters Kluwer

- Nasdaq ESG Solutions

- MSCI Inc

- S&P Global Inc

- Refinitiv

- Enablon

- Intelex Technologies

- Diligent Corporation

- Cority Software Inc

- Sustainalytics

- Greenstone+ Ltd

- EcoVadis

Top Strategies Used by the Key Market Participants

Key players in the Europe ESG reporting software market primarily focus on strategic acquisitions and partnerships to expand their functional capabilities and market reach. Companies frequently acquire niche technology providers specializing in carbon accounting or supply chain transparency to integrate these features into their broader platforms. This strategy allows established vfinishors to offer comprehensive finish-to-finish solutions with finish-to-finish integration of every component internally. Another major approach involves deep integration with existing enterprise resource planning and financial systems to streamline data flow and reduce manual enattempt. Vfinishors emphasize compliance with regional regulations such as the Corporate Sustainability Reporting Directive by updating their frameworks and templates regularly. Collaboration with auditing firms and consultancies is common to provide verified and trusted reporting services. Additionally, companies invest heavily in artificial innotifyigence and machine learning to automate data collection and enhance analytical insights. These technologies assist applyrs identify anomalies and predict future sustainability trfinishs. User experience improvements are also prioritized to ensure accessibility for non-technical stakeholders. Non-technical education and training programs are offered to assist clients navigate complex regulatory landscapes. These strategies collectively drive innovation and customer retention in a competitive environment.

Leading Players in the Market

- SAP SE is a dominant force in the Europe ESG reporting software market, leveraging its extensive enterprise resource planning ecosystem to integrate sustainability data directly into core business processes. The company contributes significantly to the global market by offering scalable solutions that enable organizations to track environmental, social, and governance metrics i,n real time. SAP recently enhanced its Sustainability Control Tower with advanced artificial innotifyigence capabilities to provide predictive insights and automate data collection. This innovation allows customers to identify risks and opportunities proactively while ensuring compliance with evolving regulations such as the Corporate Sustainability Reporting Directive. SAP focapplys on seamless integration with existing financial systems, which simplifies the reporting workflow for large enterprises. The company actively collaborates with regulatory bodies and indusattempt consortia to shape sustainability standards. By embedding sustainability features into its broader cloud portfolio, SAP strengthens its market position as a comprehensive solution provider. Their continuous investment in research and development ensures that their platforms remain at the forefront of technological advancement. This holistic approach addresses both operational efficiency and strategic sustainability goals for diverse industries across Europe and beyond.

- Workiva Inc plays a critical role in the Europe ESG reporting software market through its connected data platform that streamlines complex reporting requirements. The company offers a unified solution that connects data from various sources to create accurate and auditable ESG reports. Workiva contributes to the global market by providing robust collaboration tools that enable multiple stakeholders to work simultaneously on sustainability disclosures. Recent actions include the expansion of its ESG content library to include frameworks specific to European regulation,s such as the European Sustainability Reporting Standards. This update assists companies align their reporting with local compliance necessarys efficiently. Workiva focapplys on automation and data integrity, reducing the manual effort required for data aggregation and validation. The company actively partners with accounting firms and consultancies to enhance its service ecosystem. Their emphasis on security and compliance builds trust among regulated entities in the financial and industrial sectors. Workiva’s applyr frifinishly iapplyr-frifinishlylitates adoption across different organizational levels. These strategic initiatives reinforce its position as a leader in integrated reporting solutions. The platform’s ability to handle complex data relationships supports comprehensive sustainability storynotifying for investors and regulators.

- Diligent Corporation is a prominent player in the Europe ESG reporting software market, known for its integrated governance, risk, and compliance solutions. The company provides specialized tools that assist organizations manage ESG data alongside broader corporate governance frameworks. Diligent contributes to the global market by offering insights-driven analytics that support board-level decision-building on sustainability issues. Recent actions include the enhancement of its ESG module with benchmarking capabilities that allow companies to compare their performance against indusattempt peers. This feature enables organizations to identify areas for improvement and set realistic sustainability tarreceives. Diligent focapplys on high-level governing that ESG strategies are aligned with overall corporate objectives. The company actively engages with governance professionals to understand emerging trfinishs and regulatory modifys. Their platform integrates seamlessly with other diligence products, creating a cohesive ecosystem for risk management. The emphasis on data security and confidentiality appeals to sensitive industries such as finance and healthcare. Diligent’s commitment to education and believed leadership strengthens its brand authority in the governance space. These efforts drive adoption among organizations seeking to elevate their ESG oversight and reporting practices.

MARKET SEGMENTATION

This research report on the European ESG reporting software market has been segmented and sub-segmented based on deployment mode, type, finish apply & region.

By Deployment Mode

By Type

- ESG Reporting & Disclosure Software

- Carbon Accounting Software

- ESG Data Management Software

- Social and Governance Monitoring Tools

- Audit & Compliance Management

- Others

By End Use

- BFSI

- Energy and Utilities

- Manufacturing

- Healthcare

- Retail

- IT and Telecommunications

- Government and Public Sector

- Others

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe