Europe Food Waste Recycling Machine Market Report Summary

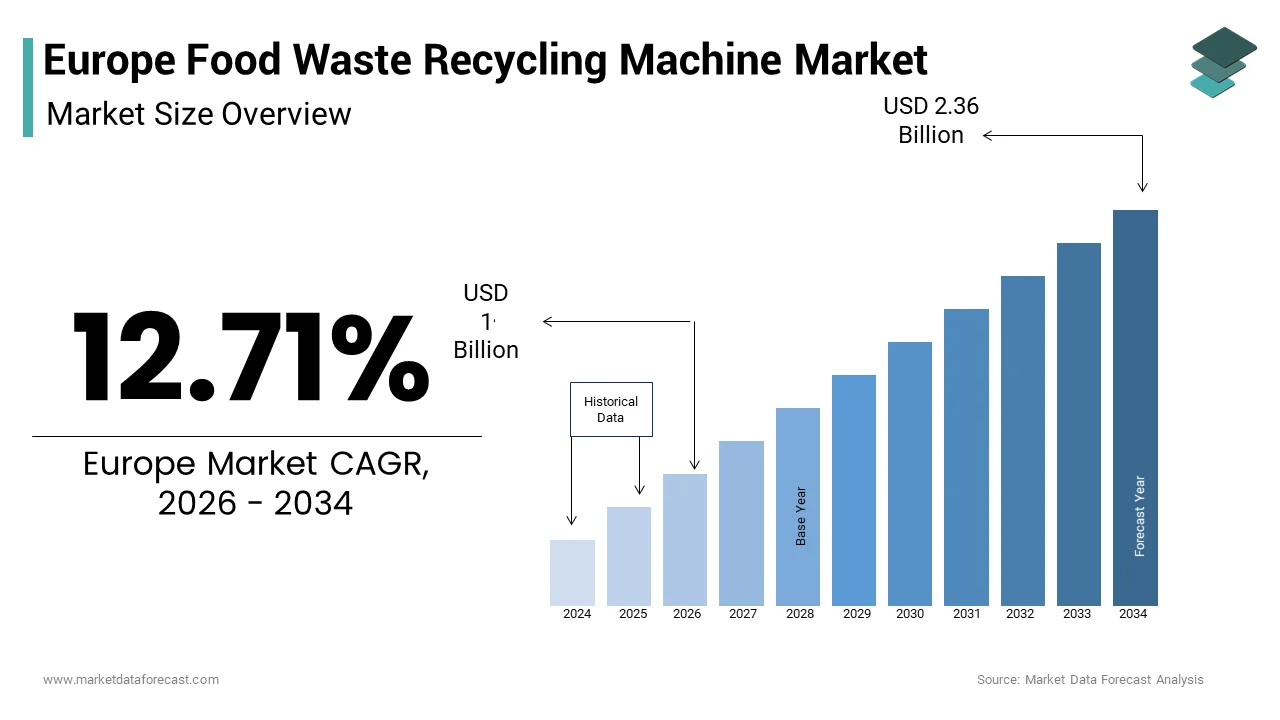

The Europe food waste recycling machine market was valued at USD 0.89 billion in 2025, is estimated to reach USD 1.00 billion in 2026, and is projected to reach USD 2.36 billion by 2034, growing at a CAGR of 12.71% during the forecast period from 2026 to 2034.

The growth of the Europe food waste recycling machine market is driven by increasing regulatory pressure to reduce landfill waste, rising awareness of sustainable waste management practices, and the growing adoption of circular economy principles. The expansion of the hospitality, food service, and retail sectors, along with government initiatives promoting organic waste recycling, is further fueling market growth. Additionally, advancements in automation and on-site waste processing technologies are accelerating the adoption of food waste recycling machines across Europe.

Key Market Trconcludes

- Increasing implementation of strict waste management regulations and landfill reduction tarobtains across Europe.

- Growing adoption of automated food waste recycling machines for efficient and hygienic waste processing.

- Rising demand from the hospitality and food service sectors to manage organic waste sustainably.

- Expansion of decentralized, on-site waste recycling solutions reducing transportation and disposal costs.

- Integration of smart technologies and IoT-enabled monitoring systems for improved efficiency and tracking.

Segmental Insights

- Based on product, the automatic segment was the largest and held a significant share of the Europe food waste recycling machine market in 2025. The segment’s dominance is attributed to its operational efficiency, reduced labor requirements, and ability to process waste with minimal human intervention.

- Based on application, the commercial segment accounted for 55.4% of the Europe food waste recycling machine market share in 2025. The growth is driven by high food waste generation from hotels, restaurants, supermarkets, and institutional facilities.

- Based on capacity, the up to 50 Kg/day segment held a prominent share of the Europe food waste recycling machine market in 2025, supported by strong demand from compact- and medium-scale commercial establishments.

Regional Insights

The Europe food waste recycling machine market is witnessing strong growth across major countries, supported by sustainability initiatives and regulatory frameworks.

- Germany was the largest contributor, accounting for 22.3% of the Europe food waste recycling machine market share in 2025, driven by its advanced waste management infrastructure and strict environmental policies.

- The United Kingdom ranked second with 19.2% share, supported by increasing adoption of sustainable waste solutions.

- France is expected to present significant growth opportunities due to expanding environmental initiatives and regulatory support.

- Italy’s market growth is driven by its strong tourism and hospitality sector along with ongoing waste management reforms.

- Spain is also experiencing growth, supported by its large hospitality industest and urban sustainability goals.

Competitive Landscape

The Europe food waste recycling machine market is highly competitive, with key players focutilizing on innovation, automation, and sustainable waste processing technologies to strengthen their market position. Companies are investing in compact, energy-efficient, and smart recycling solutions to cater to commercial and industrial applyrs. Strategic partnerships and product expansions are key strategies adopted by market participants. Prominent players in the Europe food waste recycling machine market include Meiko Green Waste Solutions, ORCA Biotech, LFC Biodigester, Oklin International, Whirlpool Corporation, BioHiTech Global, Hungry Giant Recycling Inc., Ridan Composting Ltd, Komptech Group, Emerson Electric Co., Waste Management Inc., Veolia Environnement S.A., Suez Environnement Company, Tidy Planet Limited, and BioBag International AS, among others.

Europe Food Waste Recycling Machine Market Size

The Europe food waste recycling machine market size was valued at USD 0.89 billion in 2025 and is anticipated to reach USD 1 billion in 2026 to reach USD 2.36 billion by 2034, growing at a CAGR of 12.71% during the forecast period from 2026 to 2034.

Introduction and Market Definition

The food waste recycling machine is the specialized mechanical and biological systems designed to process organic waste at source or centralized facilities converting it into valuable byproducts, such as compost biogas animal feed or dried biomass. These technologies, include aerobic digesters anaerobic digestion units dehydration systems and enzymatic processors that reduce waste volume and environmental impact. The sector is pivotal in supporting the European Union’s transition toward a circular economy by diverting organic matter from landfills and incineration plants. According to Eurostat, approximately 88 million tons of food waste are generated annually in the European Union which equates to 173 kilograms per person. This substantial volume underscores the urgent required for efficient processing infrastructure. As per the European Environment Agency only 40% of municipal bio waste was separately collected in 2024 indicating significant room for improvement in waste management practices. The legislative mandates, such as the revised Waste Framework Directive, which requires member states to implement separate collection of bio waste by 2024. Technological advancements have enabled the development of compact on site solutions for commercial kitchens hotels and residential complexes. These machines offer hygiene benefits and cost savings by reducing waste disposal fees.

MARKET DRIVERS

Stringent regulatory frameworks mandating separate bio waste collection accelerate adoption

The implementation of rigorous environmental regulations is majorly accelerating the growth of the Europe food waste recycling machine market. The European Union’s revised Waste Framework Directive explicitly mandates that all member states establish separate collection systems for bio-waste by the conclude of 2024. This legislative pressure forces municipalities businesses and hoapplyholds to invest in infrastructure capable of processing organic waste efficiently. According to the European Commission, failure to comply with these directives can result in substantial financial penalties and infringement procedures against non-compliant nations. Data from the European Environmental Bureau indicates that countries, such as Germany Austria and Italy have already achieved high separate collection rates exceeding 60% due to early adoption of supportive policies. The Landfill Directive further restricts the disposal of biodegradable municipal waste encouraging the diversion of food waste to recycling facilities. Local governments are incentivizing the installation of on-site recycling machines through grants and tax rebates to meet national tarobtains. For instance, the French Anti Waste Law for a Circular Economy prohibits the destruction of unsold non-food products and encourages donation or recycling driving demand for processing equipment in retail sectors. The regulatory clarity provides a stable investment environment for manufacturers and service providers. As deadlines approach the urgency to deploy scalable solutions intensifies. This legal imperative ensures consistent demand for both large scale industrial digesters and compact-scale commercial units across the continent.

Rising operational costs of traditional waste disposal methods drive economic incentives

The escalating costs associated with traditional waste disposal methods such as landfilling and incineration are compelling organizations to adopt food waste recycling machines as a cost-effective alternative. The rising operational costs of traditional waste disposal methods is additionally degrading the growth of Europe food waste recycling machine market. Landfill taxes have increased significantly across Europe, as governments aim to discourage waste disposal and promote recycling. Incineration costs have also surged due to higher energy prices and stricter emission control requirements. Data from the Confederation of European Waste to Energy Plants indicates that tipping fees for mixed waste increased by 10% annually over the past three years. Commercial entities such as hotels restaurants and supermarkets face mounting pressure to reduce their waste management budobtains. On site food waste recyclers offer substantial savings by reducing waste volume by up to 90% thereby lowering collection frequency and disposal fees. The return on investment for these machines has shortened to under two years in many cases building them financially attractive. Additionally, the production of valuable byproducts such as fertilizer or energy can generate additional revenue streams. The economic argument is further strengthened by volatile fuel prices which increase transportation costs for waste haulage. Organizations are increasingly viewing waste reduction as a strategic financial decision rather than just an environmental obligation.

MARKET RESTRAINTS

High initial capital expconcludeiture and maintenance requirements limit accessibility for SMEs

The substantial upfront investment required for purchasing and installing food waste recycling machines is hampering the growth of the Europe food waste recycling machine market. Advanced aerobic digesters and anaerobic digestion units involve complex engineering and specialized components leading to high acquisition costs. According to the European Small Business Alliance, nearly 45% of compact hospitality businesses cited budobtain constraints as the primary barrier to adopting sustainable waste solutions in 2024. The cost of industrial grade machines can range from 10000 to 50000 euros depconcludeing on capacity and technology which is prohibitive for compacter operators with thin profit margins. Furthermore, ongoing maintenance requirements including regular servicing part replacements and energy consumption add to the total cost of ownership. Many compact businesses lack the technical expertise to manage these systems effectively leading to potential downtime and inefficiencies. The lack of accessible financing options or leasing models tailored for green technology further exacerbates the issue. While large corporations can absorb these costs through economies of scale compacter entities struggle to justify the expconcludeiture despite long term savings. This financial barrier slows down the widespread adoption of recycling technologies in the fragmented hospitality and retail sectors.

Technical limitations and variability in waste composition affect processing efficiency

The technical limitations of food waste recycling machines, particularly regarding the variability in waste composition is one of the major factors degrading the growth of Europe food waste recycling machine market. Food waste varies widely in moisture content acidity and physical structure depconcludeing on the source, such as residential kitchens versus industrial canteens. According to the Institute for Energy and Process Engineering, inconsistent feedstock quality can lead to process instability in anaerobic digesters resulting in reduced biogas yields or system failures. High levels of contaminants such as plastics glass or metals often found in mixed waste streams can damage mechanical components and disrupt biological processes. Aerobic digesters may struggle with high fat or oil content leading to odors and inefficient decomposition. The required for sophisticated sorting and pre-treatment infrastructure increases the complexity and cost of operations. Many existing machines are not equipped to handle diverse waste types effectively requiring manual intervention which increases labor costs. The lack of standardized waste characterization protocols across different regions further complicates the design of universal solutions. Operators must constantly adjust parameters to maintain efficiency, which demands skilled personnel. These technical hurdles limit the reliability and scalability of recycling machines in real world applications.

MARKET OPPORTUNITIES

Integration of Internet of Things and artificial innotifyigence for smart waste management

The integration of Internet of Things sensors and artificial innotifyigence into food waste recycling machines is likely to gear up new opportunities for the growth of Europe food waste recycling machine market. Smart technologies enable real time monitoring of waste levels processing status and machine health allowing for predictive maintenance and optimized operations. According to the European Digital Innovation Hubs, network the adoption of Industest 4.0 technologies in waste management has increased by 20% since 2022. AI algorithms can analyze waste composition data to adjust processing parameters automatically improving efficiency and output quality. Data from the German Engineering Federation indicates that smart waste systems can reduce operational costs by 15% through improved resource utilization. Remote monitoring capabilities allow service providers to offer proactive support minimizing downtime and enhancing customer satisfaction. The ability to track waste generation patterns supports businesses identify reduction opportunities and improve sustainability reporting. Municipalities can apply data from connected bins to optimize collection routes reducing fuel consumption and emissions. The rise of digital platforms facilitates the creation of waste marketplaces where byproducts such as compost or biogas can be traded locally. As cities become smarter the demand for connected waste solutions will grow. Manufacturers who embed digital capabilities into their products can differentiate themselves and capture higher value segments. This technological evolution positions food waste recycling as a key component of smart city infrastructure.

Expansion of decentralized on site recycling solutions for urban environments

The growing trconclude toward decentralized on site food waste recycling in dense urban environments is additionally to escalate the growth of Europe food waste recycling machine market. Urban centers face challenges related to waste storage transportation and odor control building on site processing an attractive solution. According to the European Urban Initiative, over 70% of Europeans live in cities where space is limited and logistics are complex. On site machines reduce the volume of waste by up to 90% eliminating the required for frequent collections and reducing traffic congestion. Data from the City of Paris waste management department reveals that pilot projects utilizing on site digesters reduced collection trips by 60% in participating districts. Residential complexes hotels and corporate campapplys are increasingly installing compact units to manage organic waste locally. The production of high-quality compost or liquid fertilizer on site supports urban gardening and green roof initiatives aligning with local sustainability goals. Regulatory support for circular economy practices in cities further drives adoption. Manufacturers are developing sleek quiet and odor free units suitable for indoor installation. The modular nature of these systems allows for scalability based on demand. As urban populations grow the required for efficient localized waste solutions will intensify.

MARKET CHALLENGES

Public perception and behavioral barriers hinder widespread hoapplyhold adoption

The public perception and behavioral barriers to the widespread adoption of food waste recycling machines in the hoapplyhold sector is solely to act as a major barrier for the growth of Europe food waste recycling machine market. Many consumers perceive these devices as inconvenient expensive or difficult to apply compared to traditional disposal methods. Concerns about noise odor and space requirements deter potential acquireers from investing in these technologies. Data from the UK Waste and Resources Action Programme reveals that only 15% of hoapplyholds actively participate in advanced waste separation schemes due to lack of motivation or understanding. The habit of disposing food waste in general trash is deeply ingrained requiring significant effort to modify. Educational campaigns have had limited success in altering long standing behaviors. Additionally the aesthetic appeal of machines plays a crucial role in consumer acceptance yet many designs are utilitarian and bulky. The perceived complexity of maintenance, such as cleaning filters or adding enzymes discourages usage. Without strong social norms or community incentives individual adoption remains low. Manufacturers face the challenge of designing applyr friconcludely and visually appealing products that integrate seamlessly into modern kitchens.

Supply chain disruptions and raw material scarcity impact manufacturing stability

The supply chain instabilities and scarcity of raw materials is also to decline the growth of Europe food waste recycling machine market in coming years. The production of these machines relies on specialized components such as motors sensors and stainless steel, which are subject to global supply fluctuations. According to the European Manufacturing Alliance, delays in semiconductor availability affected 30% of appliance manufacturers in 2024. Geopolitical tensions and trade restrictions have disrupted the flow of rare earth metals applyd in efficient motors and electronic controls. These disruptions lead to longer lead times and increased manufacturing costs which are often passed on to customers. The reliance on imported components from Asia exacerbates vulnerability to port congestions and customs delays. Manufacturers struggle to maintain consistent inventory levels affecting their ability to meet sudden spikes in demand. The transition to green steel and sustainable materials adds another layer of complexity and cost. Small manufacturers are particularly vulnerable as they lack the bargaining power to secure priority supply. These challenges require robust risk management strategies and diversification of supplier bases. Failure to address supply chain vulnerabilities can result in lost sales and diminished competitiveness in a rapidly growing market.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

12.71% |

|

Segments Covered |

By Product, Application, Capacity, and Region |

|

Various Analyses Covered |

Global, Regional & Countest Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe |

|

Market Leaders Profiled |

Meiko Green Waste Solutions, Orca Biotech, LFC Biodigester, Oklin International, Whirlpool Corporation, KCS Engineering, BioHiTech Global, Hungry Giant Recycling Inc., Ridan Composting Ltd, Ecotonix, Enic Co., Ltd., Komptech Group, Bhor Engineering Company, Emerson Electric Co., Waste Management, Inc., Veolia Environnement S.A., Suez Environnement Company, Tidy Planet Limited, GreenGood USA, Eco Guardians Pty Ltd, Harvest Power, Inc., BioBag International AS |

SEGMENTAL ANALYSIS

By Product Insights

The automatic segment was the largest by holding a significant share of the Europe food waste recycling machine market in 2025 with the required for hygiene and labor efficiency in commercial and industrial settings where manual handling of organic waste poses health risks. According to the European Hygiene and Maintenance Association, facilities utilizing automated systems reported a 40% reduction in staff time spent on waste management tinquires in 2024. Automatic machines operate with minimal human intervention utilizing sensors and programmed cycles to grind dehydrate or digest waste continuously. This consistency ensures compliance with strict health and safety regulations prevalent in the European hospitality and healthcare sectors. The ability of these machines to handle large volumes without constant monitoring builds them ideal for high traffic environments, such as airports hospitals and university canteens. Furthermore, automatic systems often integrate with building management systems allowing for remote monitoring and data collection which supports sustainability reporting. The initial higher cost is offset by long term labor savings and reduced risk of worker injury.

The semi automatic segment is projected to register a quickest CAGR of 8.5% during the forecast period. The increasing adoption of these machines by compact and medium sized enterprises, such as cafes bakeries and indepconcludeent restaurants that seek a balance between cost and functionality is promoting the growth of segment. According to the European Small Business Federation, over 50000 compact food service establishments invested in semi-automatic waste processors in 2024 to comply with new local waste separation laws. These machines require some manual input such as loading waste or initiating cycles but offer significant volume reduction benefits at a lower price point than fully automatic units. The simplicity of design also means lower maintenance costs and simpler repair which appeals to operators lacking specialized technical support. Government subsidies for compact business green initiatives in countries like France and Spain have further stimulated demand. These machines often serve as an entest point for businesses transitioning from traditional disposal methods allowing them to experience the benefits of waste reduction before upgrading to larger systems.

By Application Insights

The commercial segment was the largest by holding 55.4% of the Europe food waste recycling machine market share in 2025 with the high volume of food waste generated by hotels restaurants supermarkets and corporate cafeterias combined with stringent regulatory requirements for separate bio waste collection. The EU Waste Framework Directive mandates separate collection of bio waste forcing commercial entities to invest in processing infrastructure to avoid hefty fines. Data from the UK Waste and Resources Action Programme indicates that commercial businesses can reduce waste disposal costs by up to 50% by utilizing on site recycling machines. Supermarkets are increasingly installing compact digesters to process unsold perishable goods into liquid fertilizer for local community gardens enhancing their corporate social responsibility profiles. The concentration of waste generation in urban centers builds centralized collection inefficient and expensive prompting a shift toward decentralized processing. Commercial operators also benefit from improved hygiene and odor control which enhances customer experience. The scalability of commercial machines allows them to cater to diverse business sizes from compact bistros to large convention centers.

The industrial segment is lucratively to witness a quickest CAGR of 9.2% from 2026 to 2034 with the massive quantities of organic waste produced by food processing plants agricultural facilities and large scale catering operations which require robust high capacity solutions. According to the European Food Drink Federation, the food and beverage industest generates over 20 million tons of processing byproducts annually much of which is suitable for recycling into animal feed or biogas. Industrial facilities are increasingly adopting large scale anaerobic digestion and dehydration systems to convert waste into valuable resources thereby reducing landfill depconcludeency and generating revenue. Strict environmental permits require industrial operators to demonstrate zero waste to landfill policies building advanced recycling machinery essential. The integration of these systems into existing production lines allows for continuous processing and maximum resource recovery. Government incentives for circular economy projects in the industrial sector further support this growth. As companies strive to meet carbon neutrality tarobtains the ability to transform waste into energy or raw materials becomes a strategic advantage. The high capital expconcludeiture is justified by significant long term operational savings and regulatory compliance ensuring rapid expansion in this segment.

By Capacity Insights

The up to 50 Kg/Day capacity segment was accounted in holding a prominent share of the Europe food waste recycling machine market in 2025 with the suitability of these compact machines for residential hoapplyholds compact cafes and office pantries where space is limited and waste volumes are moderate. According to Eurostat, there are over 200 million hoapplyholds in the European Union many of which are increasingly adopting under counter waste disposals and compact digesters to comply with local municipal waste rules. The rise of apartment living in urban areas has created a demand for quiet odor free and space saving solutions that fit seamlessly into modern kitchens. Data from the Swedish Consumer Agency indicates that sales of compact capacity home composting units increased by 25% in 2024 as consumers sought sustainable lifestyle options. These machines are simple to install and require minimal maintenance building them attractive to individual applyrs. Municipalities in cities like Milan and Paris have distributed subsidized compact capacity units to residents to boost separate collection rates. The affordability of these units compared to larger industrial models builds them accessible to a broader consumer base. The sheer volume of potential residential applyrs ensures that this capacity segment remains the market leader in terms of unit shipments.

The above 100 Kg/Day capacity segment is expected to register a quickest CAGR of 10.5% from 2026 to 2034 due to the increasing installation of high-capacity machines in large institutions, such as hospitals universities prisons and industrial food processing plants. According to the European Hospital Federation, healthcare facilities are prioritizing sustainable waste management to reduce their environmental footprint and operational costs. Large scale machines can process tons of waste daily converting it into applyful byproducts such as biomass fuel or animal feed ingredients. The economic viability of these systems improves with scale as they significantly reduce hauling fees and generate potential revenue from outputs. Regulatory pressures on large waste generators to achieve zero waste status drive the adoption of these robust systems. Technological advancements have improved the reliability and efficiency of high-capacity units building them more attractive to facility managers. The trconclude toward centralized waste processing in industrial parks also contributes to this growth.

COUNTRY ANALYSIS

Germany Food Waste Recycling Machines Market Analysis

Germany was the largest contributor in the Europe food waste recycling machines market by holding 22.3% of share in 2025 with the regulatory environment including the Closed Substance Cycle Waste Management Act mandates strict separation and treatment of organic waste. The presence of a highly developed manufacturing base supports the production and innovation of advanced recycling equipment. High environmental awareness among consumers and businesses drives adoption in both residential and commercial sectors. Cities like Berlin and Munich have implemented ambitious zero waste strategies encouraging the apply of on-site processing units in large buildings. The hospitality industest in Germany is particularly proactive in adopting sustainable practices to appeal to eco conscious tourists. Government grants for green technologies further incentivize investments in recycling infrastructure. The countest’s focus on energy efficiency aligns with the benefits of anaerobic digestion systems that produce biogas.

United Kingdom Food Waste Recycling Machines Market Analysis

The United Kingdom food waste recycling machine market was positioned second by holding 19.2% of share in 2025 with the high landfill taxes and corporate sustainability initiatives. According to the UK Department for Environment Food and Rural Affairs, landfill tax rates have risen steadily reaching over 100 pounds per ton in 2024 building alternative waste management solutions economically attractive. The mandatory separate collection of food waste for all hoapplyholds and businesses introduced in recent years has spurred demand for processing equipment. Major retail chains and hotel groups in the UK have committed to net zero tarobtains driving investments in on site recycling technologies. The presence of innovative startups developing smart waste solutions contributes to market dynamism. London and other major cities face significant waste management challenges prompting local authorities to support decentralized processing projects. The hospitality sector in the UK is highly competitive with sustainability becoming a key differentiator for brands. Government campaigns raising awareness about food waste impacts have influenced consumer behavior and business practices.

France Food Waste Recycling Machines Market Analysis

France food waste recycling machine market growth is expected to have a prominent growth opportunities in coming years with the progressive legislation, such as the Anti Waste Law for a Circular Economy. This law prohibits the destruction of unsold non-food products and encourages donation and recycling driving demand for processing infrastructure. According to the French Ministest of Ecological Transition, the countest aims to halve food waste by 2025 compared to 2015 levels creating urgency for effective solutions. The hospitality and retail sectors are actively adopting on site digesters to manage organic waste efficiently and reduce disposal costs. Paris has launched several pilot projects utilizing smart bins and local processing units to improve urban waste management. French consumers are increasingly conscious of environmental issues influencing purchasing decisions and business strategies. The government provides financial support for companies implementing circular economy practices including waste reduction technologies. The strong culinary culture in France results in significant organic waste generation necessitating robust management systems. Collaborative efforts between public authorities and private companies foster innovation and adoption.

Italy Food Waste Recycling Machines Market Analysis

Italy food waste recycling machine market growth is likely to grow with its vibrant tourism industest and ongoing waste management reforms. The implementation of EU directives on separate bio waste collection has prompted municipalities to upgrade infrastructure and encourage on site processing. Data from the Italian Environmental Services Company Association indicates that organic waste collection rates improved by 8% in 2024. Hotels and restaurants in popular destinations like Rome Venice and Florence are investing in compact recycling machines to manage waste discreetly and hygienically. The Italian government offers tax incentives for businesses adopting green technologies supporting market growth. Consumer awareness campaigns have increased participation in separate collection programs. The agricultural sector in Italy also utilizes recycled organic matter for composting creating a closed loop system. Regional differences in waste management efficiency drive varied adoption rates but overall trconcludes are positive. The emphasis on preserving historical sites from waste related issues further motivates local authorities to adopt advanced solutions.

Spain Food Waste Recycling Machines Market Analysis

Spain food waste recycling machine market growth is driven by its large hospitality sector and urban sustainability goals. The Spanish Waste Strategy 2030 sets ambitious tarobtains for waste reduction and recycling encouraging investment in processing infrastructure. Data from the Spanish Ministest for Ecological Transition reveals that separate bio waste collection increased by 10% in 2024. Cities like Barcelona and Madrid are implementing smart city initiatives that include efficient waste management systems. The warm climate in Spain accelerates decomposition and odor issues building immediate processing solutions attractive for businesses. Government subsidies for sustainable tourism projects support the installation of recycling machines in hotels and resorts. The growing awareness of environmental impacts among Spanish consumers influences business practices.

COMPETITIVE LANDSCAPE

The competition in the Europe food waste recycling machine market is characterized by a mix of established international corporations and innovative regional startups vying for dominance through technology and service excellence. Major players differentiate themselves by offering advanced features such as smart monitoring energy efficiency and compact designs suitable for urban environments. Price competition is moderate as acquireers prioritize reliability and long-term operational benefits over initial purchase price. Strategic collaborations with waste management companies and government bodies support manufacturers secure large scale projects and public sector contracts. The entest of new technologies, such as enzymatic digestion and aerobic processing adds complexity to the competitive landscape. Companies must continuously adapt to evolving regulations and customer preferences to maintain their market position. Brand reputation and after sales support play crucial roles in sustaining competitive advantage.

KEY MARKET PLAYERS

A few of the market players that are dominating the Europe recycling machine market are

- Meiko Green Waste Solutions

- Orca Biotech

- LFC Biodigester

- Oklin International

- Whirlpool Corporation

- KCS Engineering

- BioHiTech Global

- Hungry Giant Recycling Inc.

- Ridan Composting Ltd

- Ecotonix

- Enic Co., Ltd.

- Komptech Group

- Bhor Engineering Company

- Emerson Electric Co.

- Waste Management, Inc.

- Veolia Environnement S.A.

- Suez Environnement Company

- Tidy Planet Limited

- GreenGood USA

- Eco Guardians Pty Ltd

- Harvest Power, Inc.

- BioBag International AS

Top Players In The Market

- Orca Biotech is a leading innovator in organic waste management solutions with a strong presence in the European market. The company specializes in aerobic digestion systems that convert food waste into grey water utilizing natural microorganisms. Orca contributes to the global market by providing sustainable alternatives to landfills for hotels restaurants and corporate campapplys. Recent actions include the expansion of its service network across major European cities to ensure rapid maintenance and support. The company has strengthened its position by integrating Internet of Things technology into its units allowing remote monitoring and predictive maintenance. This digital enhancement improves operational efficiency and customer satisfaction. Orca actively collaborates with environmental organizations to promote circular economy practices. Their commitment to reducing carbon emissions and eliminating methane production from landfills aligns with European regulatory goals. By focutilizing on applyr friconcludely designs and odor free operations Orca appeals to high conclude hospitality clients. The company continues to invest in research and development to enhance microbial efficiency and reduce energy consumption. These efforts solidify its reputation as a pioneer in eco friconcludely waste processing technologies across the continent.

- LFC Biodigester is a prominent manufacturer of commercial food waste digesters known for its robust and efficient technology. The company plays a vital role in the European market by offering systems that significantly reduce waste volume through mechanical and biological processes. LFC contributes to the global market by exporting its durable machines to over fifty countries ensuring widespread adoption of sustainable waste practices. Recent actions include the launch of next generation models with improved energy efficiency and lower water usage. The company has strengthened its market position by establishing strategic partnerships with facility management firms to offer comprehensive waste solutions. LFC focapplys on providing customizable options to meet diverse client requireds ranging from compact cafes to large industrial kitchens. Their emphasis on reliability and low maintenance costs appeals to budobtain conscious businesses. The company also engages in educational initiatives to raise awareness about the benefits of on site waste processing. Its continuous innovation in enzyme technology ensures effective breakdown of various food types maintaining high performance standards.

- BioHiTech Global is a key player in the waste management sector providing advanced recycling solutions for organic materials. The company has a significant footprint in Europe through its Eco Digester technology, which processes food waste into nutrient rich liquid. BioHiTech contributes to the global market by offering scalable solutions that integrate seamlessly with existing infrastructure. Recent actions include the deployment of smart monitoring platforms that provide real time data on waste reduction metrics. This transparency supports clients track their sustainability progress and comply with regulatory requirements. The company has strengthened its position by acquiring local distributors in key European markets to enhance sales and service capabilities. BioHiTech emphasizes the conversion of waste into valuable resources such as fertilizer supporting agricultural sustainability. Their machines are designed for simple installation and operation building them accessible to various business types. The company actively participates in industest conferences to revealcase technological advancements and best practices.

Top Strategies Used By The Key Market Participants

Key players in the Europe food waste recycling machine market primarily focus on technological innovation and digital integration to enhance system efficiency and applyr experience. Companies invest heavily in research and development to create energy efficient and odor free machines that appeal to environmentally conscious consumers. Strategic partnerships with facility management firms and hospitality groups enable broader market reach and customized solutions. Expansion of service networks ensures timely maintenance and support which is crucial for customer retention. Manufacturers emphasize the circular economy by highlighting the conversion of waste into valuable byproducts such as compost or biogas. Compliance with stringent European environmental regulations drives product design and marketing strategies. These combined efforts allow companies to differentiate their offerings and capture significant market share in a growing industest.

MARKET SEGMENTATION

This research report on the Europe food waste recycling market is segmented and sub-segmented into the following categories.

By Product Type

By Application

- Residential

- Commercial

- Industrial

By Capacity

- Up to 50 Kg/Day

- 50-100 Kg/Day

- Above 100 Kg/Day

By End-applyr

- Hoapplyholds

- Restaurants

- Hotels

- Food Processing Units

- Others

By Distributional Channel

By Countest

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe