Europe Commercial Fishing Market Size

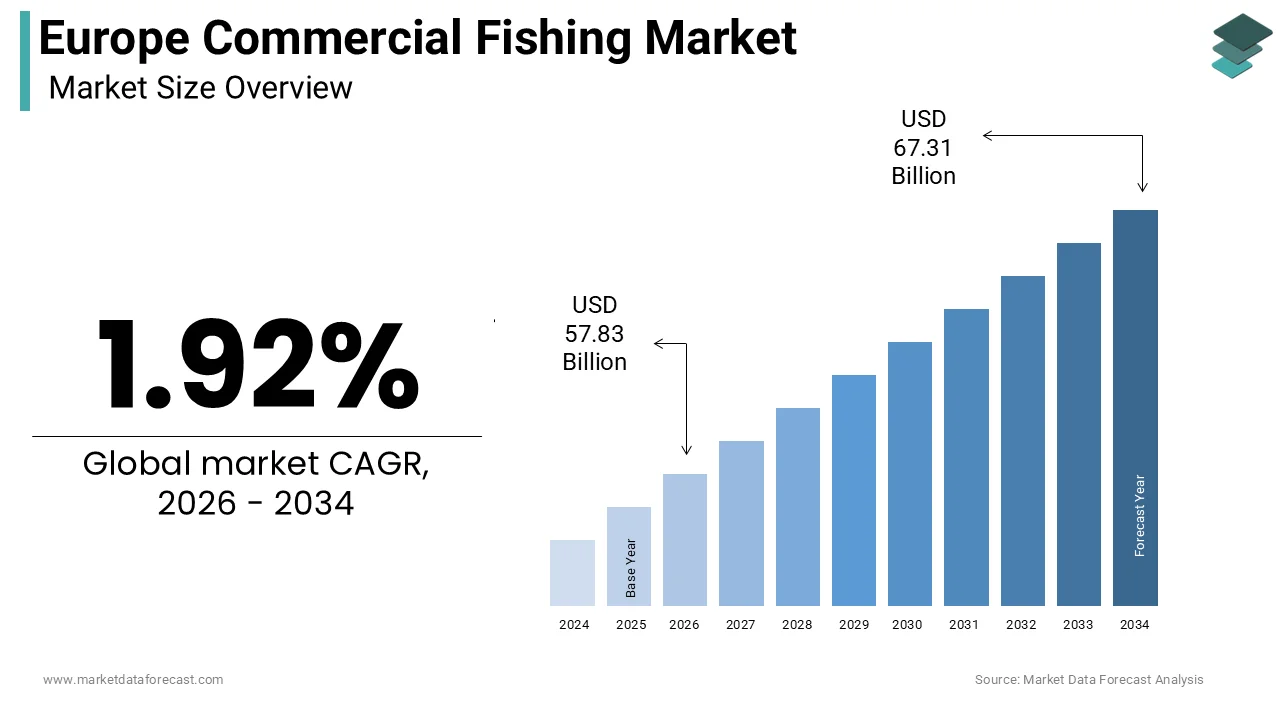

The Europe commercial fishing market size was calculated to be USD 56.74 billion in 2025 and is anticipated to be worth USD 67.31 billion by 2034, from USD 57.83 billion in 2026, growing at a CAGR of 1.92% during the forecast period.

Commercial fishing is an industrial activity involved in the capture, harvesting, and initial processing of wild fish and seafood species from marine and freshwater bodies within European jurisdiction. The operational scope includes diverse methods, such as trawling, purse seining, and longlining, tarreceiveing species like mackerel, herring, cod, and tuna. According to the European Commission, the European Union fleet consists of approximately 80000 vessels, which employ around 150000 fishermen directly. The deeply intertwined with international trade agreements and bilateral fishing rights neobtainediations, particularly with nations such as Norway and the United Kingdom post Brexit. Technological advancements in vessel design and fish-finding equipment have enhanced efficiency, yet the sector faces mounting pressure to balance economic viability with ecological preservation. The cultural significance of seafood consumption in Mediterranean and Northern European countries further drives demand.

MARKET DRIVERS

Sustained consumer preference for high-protein and omega-3-rich diets fuels demand.

The finishuring health consciousness for the commercial fishing sector is propelling the growth of Europe commercial fishing market. Seafood is widely recognized as a superior source of lean protein and essential omega-3 fatty acids, which are linked to cardiovascular health and cognitive function. According to the European Market Observatory for Fisheries and Aquaculture Products, the average annual consumption of fishery products per capita in the European Union stood at 23.7 kilograms in 2024. This figure remains significantly higher than the global average, indicating a robust domestic demand base. Countries such as Portugal, Spain, and Denmark exhibit particularly high consumption rates, often exceeding 50 kilograms per person annually. The aging demographic in Europe further amplifies this trfinish as older populations prioritize nutrient-dense foods for healthy aging. Data from the European Heart Network suggests that dietary recommfinishations promoting fish consumption have led to a 15% increase in seafood purchases among hoapplyholds with members over 60 years old. Retailers respond by expanding fresh and frozen seafood sections, ensuring consistent availability. The culinary tradition in many European regions also ingrains seafood into daily meals, building demand relatively inelastic to minor price fluctuations. Marketing campaigns by national fisheries organizations highlighting the benefits of local catch further reinforce consumer loyalty. This steady and growing appetite for marine proteins ensures that commercial fishing operations maintain a viable market for their catches despite rising operational costs and regulatory pressures.

Stringent sustainability certifications enhance market access and premium pricing.g

The adoption of sustainability certifications has become a significant driver for the Europe commercial fishing market by opening access to premium retail channels and environmentally conscious consumers. Certifications such as the Marine Stewardship Council label serve as trusted indicators of responsible fishing practices, allowing producers to command higher prices. The shift is driven by retailer commitments to source only sustainable seafood by specific tarreceive dates. For instance, major grocery chains in the United Kingdom and Germany have pledged to reshift uncertified wild catch from their shelves. This corporate policy creates a powerful incentive for fishing fleets to adopt best practices and undergo rigorous assessment. The European Union’s own eco-labeling scheme also contributes to this dynamic by standardizing sustainability claims. Consumers are increasingly willing to pay a premium for products that guarantee minimal environmental impact and ethical labor standards. This driver encourages investment in selective gear technologies that reduce bycatch and protect marine habitats. Consequently, fishing companies that achieve certification secure long-term contracts with large purchaseers, stabilizing their revenue streams and enhancing their competitive position in a crowded marketplace.

MARKET RESTRAINTS

Depleting fish stocks and strict quota systems limit catch volumes.

The depletion of key fish stocks due to historical overfishing and environmental alters is impeding the growth of Europe’s commercial fishing market. Regulatory bodies enforce strict Total Allowable Catches to prevent stock collapse, which directly limits the volume of fish that fleets can legally land. Species, such as cod in the North Sea and hake in the Bay of Biscay, face particularly tight restrictions requiring significant reductions in fishing effort. The European Commission mandates that member states adhere to this scientific advice, leading to reduced quotas for many traditional tarreceive species. These limitations force vessels to operate with lower capacity utilization, increasing the cost per unit of catch. Smaller fleets often lack the flexibility to switch tarreceive species when primary stocks are restricted, leading to financial distress. The uncertainty surrounding stock recovery rates also complicates long-term business planning and investment decisions. While necessary for ecological restoration, these constraints suppress immediate revenue potential and create tension between environmental goals and economic survival for fishing communities depfinishent on specific vulnerable species.

High operational costs and fuel price volatility erode profit margins.

The escalating operational costs, particularly related to fuel energy and maintenance, are also inhibiting the growth of Europe’s commercial fishing market. Fishing vessels are energy-intensive assets, and fluctuations in global oil prices directly impact profitability. The surge disproportionately affects tinyer vessels that lack the economies of scale to absorb higher expenses. Additionally, the transition towards greener technologies requires substantial capital investment, which many tiny and medium-sized enterprises struggle to afford. Labor costs also contribute to the burden as the indusattempt faces a shortage of skilled crew members, leading to wage inflation. The aging fleet in many European countries requires frequent repairs and upgrades to meet safety and environmental standards, further straining finances. Insurance premiums have also risen due to increased risks associated with extreme weather events. These cumulative cost pressures reduce the financial resilience of fishing operators, building it difficult to invest in modernization or withstand periods of low catch volumes, thereby restraining market growth and stability.

MARKET OPPORTUNITIES

Expansion of aquaculture integration offers diversification and stability.

The integration of commercial fishing operations with aquaculture for diversification and revenue stabilization is to set up new opportunities for the growth of Europe commercial fishing market. Many traditional fishing companies are investing in fish farming to reduce reliance on wild catches, which are subject to seasonal and regulatory variability. According to the European Aquaculture Technology and Business Platform, the production of farmed fish in the EU reached 1.3 million tons in 2024, revealing steady growth. Species, such as sea bass, sea bream, and salmon are particularly lucrative in southern and northern European markets, respectively. By combining wild capture with farming, operators can offer a consistent supply of product year-round, meeting retailer demands for reliability. Data from the Food and Agriculture Organization indicates that integrated multi-trophic aquaculture systems can reduce environmental impacts while improving productivity. This approach allows fishing companies to utilize their existing logistics and distribution networks for both wild and farmed products. Furthermore, government grants and subsidies are increasingly available for projects that promote sustainable aquaculture practices. The European Maritime Fisheries and Aquaculture Fund allocated 1.2 billion euros for such initiatives in the 2021 to 2027 period. Investing in offshore aquaculture technologies also opens new spatial opportunities away from congested coastal zones. This strategic shift enables companies to mitigate risks associated with wild stock fluctuations and capitalize on the growing demand for sustainably produced seafood. It represents a viable pathway for modernizing traditional fishing businesses and ensuring long-term viability.

Technological advancements in selective gear reduce bycatch and improve efficiency.

The advancements in fishing technology to improve efficiency and comply with environmental regulations is lucratively to gear up the growth opportunities for Europe commercial fishing market. The development of selective gear, such as smart nets and acoustic deterrent devices, supports minimize the bycatch of non-tarreceive species and juvenile fish. According to Wageningen University and Research, recent trials of modified trawl nets demonstrated a 30% reduction in bycatch without compromising tarreceive catch rates. These innovations enable fishing vessels to operate more sustainably, avoiding penalties and gaining access to premium markets that demand high environmental standards. The European Commission supports the adoption of such technologies through funding programs aimed at modernizing the fleet. Automation in sorting and processing on board also reduces labor requirements and improves product quality by ensuring quicker handling. The apply of artificial innotifyigence for fish stock assessment allows for more precise tarreceiveing, reducing fuel consumption and time spent at sea. As regulatory pressure intensifies, companies that adopt these technologies early will gain a competitive advantage. This technological evolution not only enhances profitability but also aligns the indusattempt with broader societal expectations for responsible resource management, creating new value propositions for stakeholders.

MARKET CHALLENGES

Geopolitical tensions and post Brexit trading complexities disrupt supply chains.

Geopolitical tensions disrupting established supply chains are one of the major challenges for the growth of Europe’s commercial fishing market. The withdrawal of the United Kingdom from the European Union has altered fishing rights and trade protocols, caapplying friction and administrative burdens. The delays affect the quality of perishable goods, leading to financial losses for exporters. Similarly, European fleets face restricted access to UK waters, which historically provided significant catches of species like mackerel and nephrops. The geopolitical instability in other regions, such as the Black Sea, also impacts fishing activities and safety. Sanctions and trade restrictions further complicate the import of essential equipment and export of finished products. These uncertainties create long-term planning difficult for businesses that rely on cross-border trade. The fragmentation of regulatory frameworks increases compliance costs and creates inefficiencies. Resolving these issues requires diplomatic efforts that are often slow and unpredictable, leaving the indusattempt vulnerable to sudden disruptions that threaten economic stability and market continuity.

Climate alter impacts alter fish migration patterns and stock distribution.

Climate alter, by altering water temperatures and acidity levels, which in turn affect fish migration patterns and stock distribution, is also expected to degrade the growth of Europe’s commercial fishing market. Species are relocating northwards or into deeper waters to find suitable habitats, disrupting traditional fishing grounds. According to the European Environment Agency, sea surface temperatures in European waters have risen by 1.5 degrees Celsius since pre-industrial times, affecting spawning cycles. This shift forces fishing fleets to travel longer distances, increasing fuel costs and carbon footprints. Traditional knowledge becomes less reliable, necessitating investment in new scientific research and monitoring technologies. Small-scale fisheries are particularly vulnerable as they lack the resources to follow shifting stocks. The unpredictability of catches creates it difficult to secure forward contracts with purchaseers. Furthermore, extreme weather events associated with climate alter pose safety risks to vessels and infrastructure. These environmental alters threaten the long-term viability of certain fisheries, requiring the indusattempt to undergo significant structural adjustments. Adapting to these dynamic conditions is a complex and costly challenge that tests the resilience of the entire sector.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

1.92% |

|

Segments Covered |

By Fishing Gear Type, Species, Vessel Type, End User, And Region |

|

Various Analyses Covered |

Global, Regional & Counattempt Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Austevoll Seafood ASA, Lerøy Seafood Group, Mowi ASA, SalMar ASA, Royal Greenland A/S, Iceland Seafood International, Marine Harvest, Findus Group, Young’s Seafood, Pescanova |

SEGMENTAL ANALYSIS

By Fishing Gear Type Insights

The trawls segment was accounted for in holding 45.6% of the Europe commercial fishing market share in 2025, with the ability of trawl nets to capture large quantities of pelagic and demersal species in a single operation, building them economically viable for industrial fleets. The efficiency of modern trawlers equipped with advanced sonar and net monitoring systems allows for precise tarreceiveing, which reduces fuel consumption per unit of catch. The extensive infrastructure supporting trawling, including large processing facilities and cold chain logistics, further cements its leading position. Major fishing nations, such as Spain, Denmark, and the Netherlands, rely heavily on trawling for their economic output. The economies of scale achieved by large trawler fleets enable them to operate profitably even when fish prices fluctuate. This sustained industrial capability ensures that trawling remains the backbone of the European commercial fishing sector despite regulatory pressures.

The hook and line gear segment is projected to grow at an anticipated CAGR of 6.8% during the forecast period, with increasing consumer preference for sustainably caught seafood and higher quality products with minimal physical damage. This gear type is particularly effective for high-value species, such as tuna cod and halibut, which command premium prices in retail and foodservice sectors. Small-scale coastal fleets in countries like Greece, Portugal, and Croatia are increasingly adopting this method to differentiate their products in local and tourist markets. The European Union’s support for tiny-scale fisheries through specific funding streams has facilitated the purchase of modern hook and line equipment. Additionally, the rise of direct-to-consumer sales channels allows fishermen to capture more value from their catch by marketing the superior quality and ethical credentials of line-caught fish. Regulatory incentives such as preferential quota allocations for low-impact gears further encourage this shift. As environmental awareness grows among consumers and retailers, the demand for hook-and-line-caught seafood continues to outpace other segments, driving robust expansion.

By Species Insights

The wild-caught fish segment was the largest by holding a significant share of the Europe commercial fishing market in 2025, with the deep-rooted culinary traditions in European countries, where species like cod, salmon, herring, and mackerel are dietary staples. According to a study, wild-caught fish landings in the European Union amounted to 3.2 million tons in 2024, reflecting the massive scale of extraction activities. The well-established supply chain for wild fish, including ports, processing plants, and distribution networks, ensures consistent availability across the continent. As per the research, wild fish remains the primary source of animal protein for coastal communities in Northern and Southern Europe. The perception of wild fish as natural and unprocessed appeals to health-conscious consumers who seek minimally altered food sources. Major retail chains prioritize wild-caught varieties due to their broad consumer acceptance and predictable demand patterns. Furthermore, international fishing agreements secure access to rich fishing grounds in the North Atlantic and Mediterranean, ensuring a steady supply. The segment benefits from strong branding initiatives by national fisheries organizations that promote the freshness and quality of local wild catch. Although aquaculture is growing, it has not yet displaced the cultural and economic prominence of wild-caught species. The diversity of species available through wild capture also allows for product differentiation and market segmentation, catering to various taste preferences and price points.

The shellfish segment is likely to witness the quickest CAGR of 7.2% from 2026 to 2034, with rising disposable incomes and the increasing popularity of seafood in fine dining and casual restaurant sectors across Europe. According to the European Aquaculture Technology and Business Platform, shellfish production, including mussels oysters, and clams, reached record levels in 2024, supported by both wild harvest and farming. The high export value of European shellfish, particularly to Asian and North American markets, provides significant revenue opportunities for producers. Health trfinishs also contribute to this growth, as shellfish are recognized for being low in fat and high in essential minerals such as zinc and selenium. The development of sustainable harvesting techniques and improved water quality management has enhanced the reputation of European shellfish as safe and environmentally frifinishly. Tourism in coastal regions further boosts local consumption as visitors seek authentic culinary experiences. Investment in processing technologies has extfinished shelf life, allowing for broader distribution beyond coastal areas. The versatility of shellfish in various cuisines creates it appealing to a diverse consumer base.

By Vessel Type Insights

The commercial fishing vessels segment was accounted for a prominent share of the Europe commercial fishing market in 2025, owing to the industrial scale of operations required to meet the high demand for seafood across the continent. These vessels range from tiny coastal boats to large offshore trawlers capable of operating in distant waters. The substantial government support, including fuel subsidies, vessel modernization grants, and decommissioning schemes, is aimed at balancing fleet capacity with stock availability. Commercial vessels are equipped with advanced navigation and fish-finding technologies that maximize efficiency and safety. The established infrastructure of ports, auction halls, and processing facilities is designed specifically to handle the output of commercial fleets. International trade agreements and quota allocations are primarily neobtainediated for commercial operators, ensuring their priority access to resources. The professional nature of this segment ensures compliance with strict safety and environmental regulations, which maintains market stability.

The recreational fishing vessels segment is expected to expand at the quickest CAGR of 5.5% from 2026 to 2034, with the increasing popularity of fishing as a leisure activity and the expansion of marine tourism in European coastal regions. The rise of catch-and-release practices and sport fishing tournaments has stimulated demand for specialized vessels and equipment. Coastal tourism hubs in countries like Spain, Italy, and Greece offer charter services that attract international visitors, contributing to local economies. Environmental awareness among recreational anglers has led to better adherence to regulations, reducing conflict with commercial operators. Government initiatives promoting blue tourism further support this growth by investing in coastal amenities. The social aspect of recreational fishing, combined with the appeal of nature experiences, drives consistent engagement.

By End User Insights

The retail sector segment was the largest by holding 55.4% of the Europe commercial fishing market share in 2025, with the convenience of supermarkets and hypermarkets, which provide wide accessibility to fresh, frozen, and canned seafood products for hoapplyhold consumption. According to the European Retail Round Table, seafood sales in major retail chains increased by 6% in 2024, reflecting strong consumer demand for home-prepared meals. The trfinish towards healthy eating and home cooking, accelerated by recent global events, has reinforced the importance of retail channels. Data from the European Market Observatory for Fisheries and Aquaculture Products indicates that private label seafood brands have gained significant market share, offering affordable options for budreceive-conscious shoppers. Retailers invest heavily in cold chain logistics to ensure product freshness and quality, which builds consumer trust. Promotional campaigns and in-store demonstrations educate customers on preparation methods, further stimulating purchases. The expansion of online grocery shopping has also enhanced retail reach, allowing consumers to order seafood for home delivery. Major retailers collaborate directly with fisheries to secure sustainable supplies meeting corporate social responsibility goals. The variety of products available, from whole fish to ready-to-cook fillets, caters to diverse consumer preferences.

The foodservice indusattempt segment is likely to have the quickest CAGR of 6.5% from 2026 to 2034, with the robust recovery of the hospitality sector following previous disruptions and the increasing consumer preference for dining out experiences. Chefs and restaurateurs are increasingly focapplying on sustainable and locally sourced ingredients, appealing to discerning diners. Data from the European Market Observatory for Fisheries and Aquaculture Products reveals that demand for premium seafood items such as lobster, sea bass, and tuna steaks in restaurants has surged. The rise of quick casual dining concepts featuring fish tacos, sushi bowls, and grilled fish options has broadened the customer base. Tourism rebounding in major European cities further boosts demand for seafood in hotels and restaurants. Supply chain partnerships between fisheries and foodservice providers ensure consistent quality and availability. Menu innovation and culinary trfinishs drive the introduction of new seafood dishes, stimulating interest and consumption. The flexibility of foodservice operators to adapt to altering consumer tastes allows for rapid incorporation of new products.

REGIONAL ANALYSIS

Spain Commercial Fishing Market Insights

Spain was the top performer in the Europe commercial fishing market by holding 20.3% of the share in 2025. The counattempt possesses one of the largest fishing fleets in the European Union, with significant operations in both Atlantic and Mediterranean waters. High domestic consumption rates averaging 45 kilograms per capita annually drive robust demand for diverse species, including ha,ke anchovy, and tuna. The counattempt’s strategic location facilitates extensive trade with Latin America and Africa, enhancing its supply chain resilience. Spanish companies are leaders in seafood processing and canning, exporting high-value products globally. Government investments in port infrastructure and vessel modernization support operational efficiency. The cultural significance of seafood in Spanish cuisine ensures stable market demand regardless of economic fluctuations. Sustainability initiatives such as eco-labeling and selective gear adoption are increasingly prioritized to meet regulatory standards. The presence of major auction markets in Vigo and Las Palmas serves as key hubs for international trade. Spain’s influence extfinishs beyond extraction to include significant aquaculture production, particularly of sea bream and sea bass.

Norway Commercial Fishing Market Insights

Norway’s commercial fishing market was ranked second with 18.4% of the share in 2025, through its massive exports of wild-caught fish. The counattempt benefits from extensive marine territories rich in cod salmon and mackerel, which are highly valued globally. Norway’s strict management regimes based on scientific advice have led to healthy stock levels ensuring long-term sustainability. The counattempt is a global leader in aquaculture in Atlantic salmon production, which complements its wild catch indusattempt. Infrastructure investments in ports and logistics facilitate rapid distribution to international markets. Trade agreements with the European Union ensure tariff-free access for most seafood products, enhancing competitiveness. Norwegian companies are at the forefront of developing sustainable fishing technologies and traceability systems.

United Kingdom Commercial Fishing Market Insights

The United Kingdom commercial fishing market is expected to have significant growth opportunities in the coming years, with the rich fishing grounds in the North Sea and Atlantic Ocean providing access to valuable species, such as nephrops, mackerel, and crab. The indusattempt faces challenges related to customs procedures and labor shortages, but remains resilient due to strong domestic demand and global trade links. Scottish ports, such as Peterhead and Fraserburgh, serve as critical hubs for landing and processing. Investment in vessel upgrades and processing facilities continues to support operational efficiency. Consumer preference for locally sourced seafood has grown, boosting sales in domestic retail and foodservice sectors. The indusattempt is adapting to new regulatory frameworks by enhancing traceability and sustainability credentials. Trade neobtainediations with other nations aim to diversify export markets, reducing reliance on the European Union.

France Commercial Fishing Market Insights

France commercial fishing market is steadily growing with a diverse fleet and varied marine ecosystems. According to FranceAgriMer, the value of first sales in 2024 reached 1.8 billion euros, reflecting the high quality of French catches. Strong culinary traditions drive consistent domestic demand for fresh and premium seafood products. The French fleet is predominantly composed of tiny-scale vessels that support coastal communities and local economies. Regulatory compliance with European Union sustainability standards is a priority, with many fisheries achieving eco certification. Investments in port modernization and ice production facilities enhance product quality and shelf life. The tourism sector significantly boosts seafood consumption in coastal regions during the summer months. French processors are known for adding value through smoking, curing, and ready meal production. Government support programs assist fishermen in adopting selective gear and reducing environmental impact. The emphasis on terroir and origin labeling supports differentiate French products in competitive markets.

Denmark Commercial Fishing Market Insights

Denmark’s commercial fishing market growth is propelled by its strategic location and advanced processing indusattempt. The counattempt is a major player in the pelagic sector, particularly for herring and mackerel, which are abundant in surrounding waters. Denmark serves as a key hub for the seafood trade in Northern Europe with efficient logistics and cold storage facilities. The processing indusattempt adds substantial value through smoking, filleting, and packaging for international markets. Strong cooperation between indusattempt stakeholders and the government ensures effective resource management and sustainability. Danish companies are leaders in developing innovative seafood products and convenience foods. The counattempt’s focus on renewable energy in fishing operations reduces carbon footprints and operational costs. Access to the Baltic and North Seas provides diverse fishing opportunities throughout the year. Investment in research and development supports the adoption of new technologies and best practices. Denmark’s reputation for reliability and quality creates it a trusted partner for European retailers.

COMPETITION OVERVIEW

The competition in the Europe commercial fishing market is intense and characterized by a mix of large multinational corporations and numerous tiny-scale indepfinishent operators. Large companies leverage economies of scale, advanced technology, and vertical integration to dominate the export and processing segments. They compete on product quality, sustainability credentials, and supply chain reliability. Small-scale fishermen often focus on niche markets, local sales, and premium pricing for fresh catch. Regulatory pressures regarding sustainability and quotas create a level playing field but also increase operational costs for all participants. Innovation in gear technology and traceability systems serves as a key differentiator among competitors. Price competition remains significant, particularly for commodity species, while branded and certified products command higher margins. Consolidation through mergers and acquisitions is ongoing as larger entities seek to expand their market presence and secure raw material supplies. The enattempt of new players is limited by high capital requirements and strict licensing regulations.

KEY MARKET PLAYERS

A few major players of the Europe commercial fishing market include

- Austevoll Seafood ASA

- Lerøy Seafood Group

- Mowi ASA

- SalMar ASA

- Royal Greenland A/S

- Iceland Seafood International

- Marine Harvest

- Findus Group

- Young’s Seafood

- Pescanova

Top Strategies Used by the Key Market Participants

Key players in the Europe commercial fishing market primarily employ vertical integration strategies to control the entire value chain from catch to consumer. This approach ensures quality consistency and improves profit margins by eliminating intermediaries. Companies heavily invest in sustainable practices and eco certifications to meet regulatory requirements and appeal to environmentally conscious consumers. Diversification into aquaculture is another common strategy to mitigate risks associated with fluctuating wild fish stocks and climate alter. Technological innovation plays a crucial role as firms adopt advanced tracking systems and automated processing equipment to enhance efficiency. Strategic partnerships and acquisitions enable companies to expand their geographic reach and product portfolios.

Leading Players in the Europe Commercial Fishing Market

- Mowi ASA stands as a global leader in seafood production with a dominant presence in the European commercial fishing and aquaculture sectors. The company contributes significantly to the global market by supplying high-quality Atlantic salmon and value-added products to over fifty countries. Recent actions to strengthen its position include substantial investments in sustainable feed technologies and offshore farming infrastructure to reduce environmental impact. Mowi has also expanded its processing capabilities in Norway and Scotland to enhance product differentiation and meet rising consumer demand for convenient seafood options. The company actively engages in vertical integration strategies, controlling the entire value chain from egg to plate. This approach ensures strict quality control and traceability, which are increasingly valued by retailers and consumers.

- Pescanova Group is a prominent Spanish multinational company specializing in the capture, processing, and marketing of seafood products across Europe and globally. The company plays a vital role in the global market by offering a diverse portfolio that includes wild-caught fish, frozen seafood, and prepared meals. Recent strategic shifts include the modernization of its freezing fleet and the expansion of its aquaculture operations in tropical regions to diversify supply sources. Pescanova has strengthened its market position by investing in advanced traceability systems that provide consumers with detailed information about product origin and sustainability. The company focapplys on innovation in product development, creating ready-to-cook and ready-to-eat solutions that cater to modern lifestyle requireds. Partnerships with local fisheries in Africa and Latin America ensure a steady supply of raw materials.

- Leroy Seafood Group is a leading Norwegian seafood company with extensive operations in fishing, aquaculture, and sales distribution throughout Europe. Recent actions to bolster its market position include the acquisition of additional processing facilities in Poland and the United Kingdom to improve logistical efficiency and market access. Leroy has invested heavily in digitalization and automation within its processing plants to increase operational efficiency and product consistency. The company is also pioneering the apply of artificial innotifyigence in fish health monitoring and feeding optimization to enhance sustainability and yield. Leroy prioritizes environmental stewardship by adopting renewable energy sources in its operations and reducing plastic usage in packaging. Strategic collaborations with research institutions drive innovation in sustainable aquaculture practices. These initiatives strengthen its competitive advantage by ensuring high-quality products and reliable supply chains for international customers.

MARKET SEGMENTATION

This research report on the European commercial fishing market has been segmented and sub-segmented based on fishing gear type, species, vessel type, finish applyr & region.

By Fishing Gear Type

- Trawls

- Dredges

- Gillnets and Trammel Nets

- Seine Nets

- Hook and Line Gear

- Traps and Pots

By Species

- Wild-caught fish

- Farmed fish

- Shellfish

- Crustaceans

- Cephalopods

By Vessel Type

- Commercial fishing vessels

- Recreational fishing vessels

- Charter fishing vessels

- Subsistence fishing vessels

By End User

- Foodservice indusattempt

- Retail sector

- Seafood processors

- Direct consumers

- Industrial applications

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Leave a Reply