Europe Magnetic Sensor Market Size

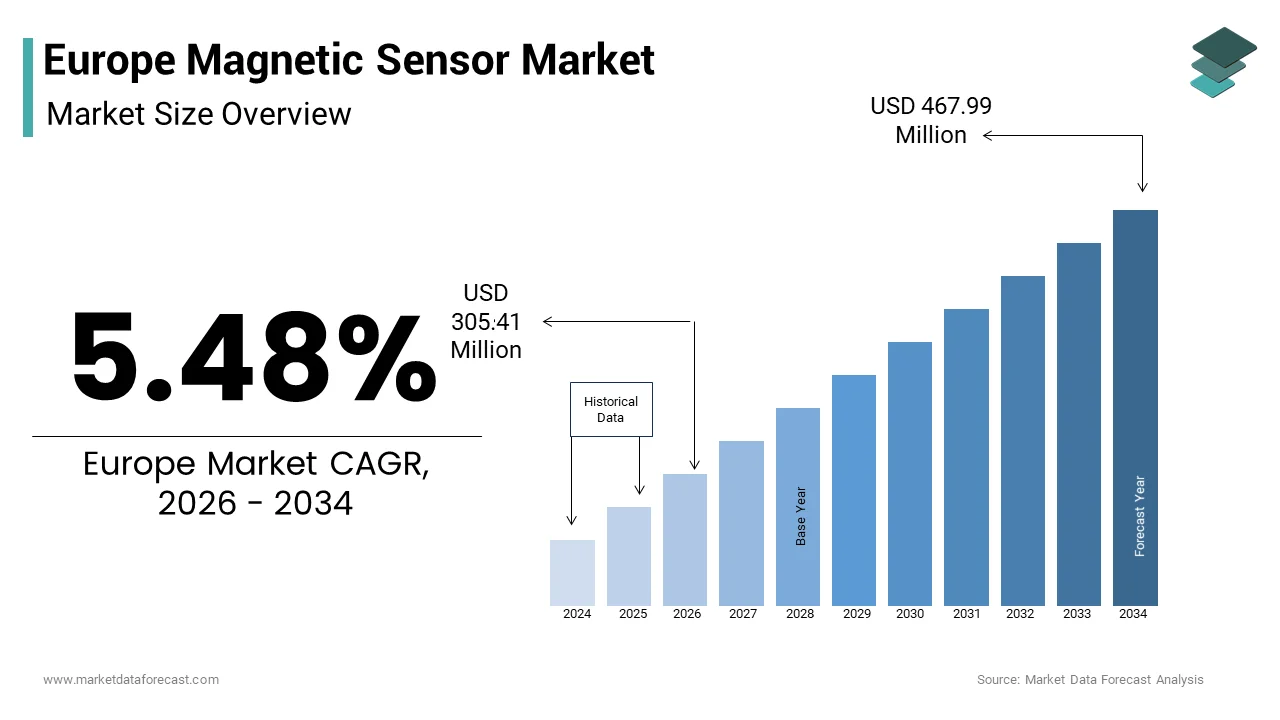

The Europe magnetic sensor market size was valued at USD 289.54 million in 2025 and is anticipated to reach USD 305.41 billion in 2026 to reach USD 467.99 million by 2034, growing at a CAGR of 5.48% during the forecast period from 2026 to 2034.

A magnetic sensor is a device that detects magnetic fields (from magnets or electric currents) and converts these invisible physical phenomena into measurable electrical signals. These sensors including Hall effect magnetoresistive and reed switches play a critical role in position sensing current measurement and speed detection within complex electronic systems. The region’s strong manufacturing base particularly in the automotive and industrial automation sectors drives the continuous demand for precise and reliable sensing solutions. As per Eurostat, the manufacturing sector generated €2.5 trillion in value added in 2023–2024, contributing approximately 16.3% of the total EU gross value added (GVA) and remaining the largest contributor to the non-financial business economy. The transition towards electric mobility and automated production lines necessitates high precision components that ensure operational efficiency and safety. According to the European Automobile Manufacturers Association (ACEA), EU car production totaled 11.4 million units in 2024; despite a 6.2% decline in volume, the integration of advanced driver assistance systems (ADAS) surged as new safety regulations mandated features like lane-keeping and collision avoidance in all new vehicles. Furthermore, the European Commission’s Digital Decade initiative tarobtains more than 90% of EU SMEs reaching at least a basic level of digital intensity by 2030, a goal currently supported by an EU average of 73% as of the 2024/2025 reporting cycle. The presence of leading semiconductor manufacturers and research institutions in countries like Germany and France fosters innovation in sensor miniaturization and energy efficiency. Hence, the convergence of industrial modernization automotive electrification and digital transformation creates a robust foundation for the growth of the magnetic sensor market in Europe.

MARKET DRIVERS

Rapid Electrification of the Automotive Sector Drives Demand for Sensing Components

The transition from internal combustion engines to electric vehicles in the region has fundamentally altered the architectural requirements of automotive electronics, which has accelerated the growth of the Europe magnetic sensor market. Electric powertrains require precise monitoring of battery current motor position and wheel speed to ensure optimal performance and safety. According to the International Energy Agency (IEA), electric car sales in Europe stagnated in 2024, with the market share remaining stable at around 20% (approximately 2.6 million units or fewer), while global sales continued to rise. This rapid adoption necessitates the integration of numerous magnetic sensors such as Hall effect sensors and tunneling magnetoresistance devices within inverters battery management systems and electric motors. These sensors provide non contact measurement capabilities which are essential for high voltage environments where electrical isolation is critical. As per the European Battery Alliance, the establishment of gigafactories across the continent aims to secure a domestic battery value chain (including cells and materials) to meet the demand for electric vehicles, reducing reliance on imports. Furthermore, advanced driver assistance systems which are becoming standard in new vehicles rely on magnetic sensors for steering angle detection and pedal position monitoring. The European New Car Assessment Program (Euro NCAP) 2026 protocols introduce stringent requirements for Driver Monitoring Systems (DMS) and Child Presence Detection (CPD) to enhance active safety, while also incentivizing the utilize of physical buttons over touchscreens to reduce driver distraction. Thus, the structural shift towards electrified mobility acts as a primary driver propelling the magnetic sensor market forward with sustained growth in automotive applications.

Expansion of Industrial Automation Accelerates Integration of Smart Sensing Technologies

Industest 4.0 principles are being widely adopted across regional manufacturing facilities, which propels the expansion of the Europe magnetic sensor market. This shift is driving the integration of ininformigent magnetic sensors into automated machinery and robotic systems. These sensors are crucial for providing real time feedback on motor speed position and linear displacement which are essential for precise control in automated production lines. According to the International Federation of Robotics (IFR), the number of industrial robots installed in the EU automotive sector declined by approximately 5% in 2024 (to ~30,650 units), marking a contraction rather than a record year, although the sector remains the largest customer for robotics. Magnetic sensors enable the seamless operation of collaborative robots and automated guided vehicles by ensuring accurate navigation and obstacle detection. The International Federation of Robotics (IFR) highlights that robot density in European manufacturing is among the highest globally, with countries like Switzerland and Germany leading in robots per 10,000 employees. Furthermore, the push for predictive maintenance in smart factories relies on sensors that can monitor the health of rotating machinery and detect anomalies before failures occur. Research by institutions like Fraunhofer IPK focutilizes on ininformigent condition monitoring to detect wear and prevent failure, while broader industest data suggests that effective predictive maintenance solutions can reduce unplanned downtime by 30% to 50%. Government initiatives such as the Digital Europe Programme provide funding for the digitalization of compact and medium sized enterprises encouraging the uptake of smart sensor technologies. Consequently the drive towards enhanced operational efficiency and automation sustains the strong demand for magnetic sensors in the industrial sector.

MARKET RESTRAINTS

Volatility in Raw Material Prices Impacts Manufacturing Costs and Availability

The production of these sensors depconcludes heavily on raw materials like neodymium and samarium, and thereby hinders the growth of the Europe magnetic sensor market. These rare earth elements face significant price volatility and supply chain risks. Europe depconcludes largely on imports for these critical materials primarily from Asia which exposes manufacturers to geopolitical tensions and trade restrictions. According to the European Raw Materials Alliance the supply risk for rare earth elements remains high due to concentrated production sources and limited recycling infrastructure. Fluctuations in the prices of these materials directly affect the cost structure of magnetic sensor manufacturers leading to unpredictable pricing for conclude utilizers. In 2024, the semiconductor industest relocated from a shortage to an oversupply in the automotive and industrial sectors. According to ESIA, the primary challenge shifted from “availability” to geopolitical de-risking, as companies shifted toward “China + 1” or “Europe-First” sourcing strategies rather than broad inventory accumulation. Lead times for analog and mixed-signal chips stabilized to pre-pandemic levels (12–16 weeks) in 2024. Most European electronics manufacturers spent the year destocking (reducing excess inventory) to free up working capital that had been tied up during the 2022 supply crunch. Additionally logistical bottlenecks and energy cost increases in Europe have further strained the supply chain building it challenging for manufacturers to maintain consistent output levels. The lack of local sourcing options for key materials limits the ability of European companies to mitigate these risks effectively. Therefore, the instability in raw material supply and pricing acts as a significant restraint hindering the profitability and scalability of the magnetic sensor market in the region.

Stringent Regulatory Compliance Increases Development Complexity and Operational Costs

Manufacturers of these sensors in the region must adhere to strict regulatory frameworks regarding environmental sustainability and product safety, which hampers the expansion of the Europe magnetic sensor market. This compliance adds significant complexity and cost to the development process. Regulations such as the Restriction of Hazardous Substances Directive and the Registration Evaluation Authorisation and Restriction of Chemicals impose rigorous limits on the utilize of certain materials in electronic components. According to the European Chemicals Agency compliance with these regulations requires extensive testing and documentation increasing the time to market for new products. The upcoming Ecodesign for Sustainable Products Regulation will further mandate transparency in the environmental footprint of electronic components requiring manufacturers to adopt more sustainable production methods. As per the European Environment Agency the pressure to reduce carbon emissions throughout the supply chain forces companies to invest in cleaner manufacturing technologies and energy efficient processes. Additionally the General Data Protection Regulation impacts the development of smart sensors that collect and transmit data requiring robust cybersecurity measures to protect utilizer privacy. Small and medium sized enterprises often struggle to bear the financial burden of compliance leading to market consolidation. The necessary for continuous adaptation to evolving regulatory landscapes diverts resources from research and development activities. Consequently the high cost of compliance and the complexity of regulatory adherence act as a major restraint limiting the agility and competitiveness of some market participants.

MARKET OPPORTUNITIES

Integration in Renewable Energy Systems Offers Significant Growth Potential

The expansion of renewable energy infrastructure in the region offers a lucrative opportunity for the magnetic sensor market. This is particularly true in wind and solar power applications. Wind turbines rely heavily on magnetic sensors for pitch control yaw positioning and generator monitoring to maximize energy capture and ensure operational safety. According to the European Wind Energy Association wind power capacity in Europe is expected to double by 2030 driven by ambitious climate tarobtains and government incentives. Each wind turbine contains numerous magnetic sensors that operate in harsh environmental conditions requiring high durability and reliability. Similarly solar tracking systems utilize magnetic sensors to optimize the angle of photovoltaic panels throughout the day enhancing energy efficiency. As per the International Renewable Energy Agency investments in renewable energy technologies in Europe reached unprecedented levels in 2024 supporting the deployment of advanced monitoring and control systems. The transition towards smart grids also necessitates precise current sensing solutions for managing electricity flow and preventing overloads. Magnetic current sensors offer non intrusive measurement capabilities that are ideal for high voltage applications in substations and distribution networks. The European Commission’s Green Deal initiative provides substantial funding for clean energy projects further stimulating demand for specialized sensing components. Thus, the growing renewable energy sector creates a robust avenue for market expansion offering long term opportunities for magnetic sensor manufacturers.

Advancements in Internet of Things Drive Demand for Miniaturized Sensors

The proliferation of Internet of Things devices and smart home appliances in the region creates a pathway for the expansion of the Europe magnetic sensor market. This is creating a growing demand for compact and energy efficient magnetic sensors. These sensors are integral to the functionality of smart locks wearable devices and home automation systems where space and power consumption are critical constraints. Magnetic sensors enable precise position detection in smart meters door sensors and appliance controls contributing to the seamless operation of interconnected systems. The trconclude towards miniaturization allows for the integration of sensors into compacter form factors without compromising performance. A study predicts that 5G connections will represent over half (51%) of all mobile connections by 2029. The launch of 5G-Advanced in 2024/2025 further enhances support for high-precision, low-power industrial sensors. Consumer electronics manufacturers are increasingly prioritizing utilizer experience which drives the necessary for reliable and responsive sensing technologies. The European Union’s support for digital innovation through programs like Horizon Europe fosters the development of next generation sensor technologies. Furthermore the rising awareness of energy efficiency encourages the utilize of low power magnetic sensors in battery operated devices. So, the expanding IoT ecosystem provides a dynamic opportunity for market growth driven by consumer demand for smart and connected living solutions.

MARKET CHALLENGES

Intense Competition from Alternative Sensing Technologies Poses a Threat

Alternative technologies, including optical, capacitive, and inductive sensors, are challenging the Europe magnetic sensor market. These options offer distinct advantages in specific applications. Optical sensors for instance provide higher resolution and accuracy in position detection building them preferred in precision manufacturing and robotics. According to the VDMA German Mechanical Engineering Industest Association the adoption of optical encoding systems in high precision machinery has grown steadily due to their superior performance characteristics. Capacitive sensors are increasingly utilized in touch interfaces and proximity detection offering better sensitivity in certain environments. According to the IEEE Sensors Council, the market is shifting toward Heterogeneous Integration. Rather than MEMS replacing magnetic sensors, the industest is shifting toward “Smart Magnetic Sensors” that embed MEMS-based self-calibration logic to compensate for thermal drift and aging in real-time. The choice of sensor technology often depconcludes on factors such as cost environmental conditions and required precision. In applications where electromagnetic interference is a concern magnetic sensors may be less suitable compared to other technologies. Additionally the development of hybrid sensor systems that combine multiple sensing principles challenges the dominance of standalone magnetic sensors. Manufacturers must continuously innovate to maintain the competitive edge of magnetic sensors by improving their accuracy temperature stability and cost effectiveness. Hence, the presence of viable alternatives restricts the market potential of magnetic sensors in certain segments requiring strategic differentiation to sustain growth.

Technical Limitations in Extreme Environments Restrict Application Scope

Extreme temperatures, high radiation, and strong magnetic fields limit the performance of these sensors, which slows down the expansion of the Europe magnetic sensor market. This restricts their utilize in aerospace and specialized industrial applications. High temperatures can cautilize demagnetization of permanent magnets and drift in sensor sensitivity leading to inaccurate readings. According to the European Space Agency standard magnetic sensors often require additional shielding and compensation circuits to function reliably in space applications increasing system complexity and cost. In automotive under the hood applications sensors must withstand temperatures exceeding 150 degrees Celsius which poses challenges for material stability and packaging. As per the Society of Automotive Engineers the development of high temperature resistant magnetic materials is ongoing but remains a technical hurdle for widespread adoption in harsh environments. External magnetic interference from nearby motors or power lines can also affect sensor accuracy requiring careful design and placement. The necessary for calibration and signal conditioning further adds to the overall system cost. While advancements in materials science are addressing some of these issues the inherent limitations of magnetic sensing technology persist. Thus, these technical constraints limit the utilize of magnetic sensors in extreme conditions prompting engineers to consider alternative solutions or invest in costly mitigation strategies.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

5.48% |

|

Segments Covered |

By End-utilizer, Technology, Application, and Region. |

|

Various Analyses Covered |

Global, Regional, and Countest Level Analysis; Segment-Level Analysis, DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe |

|

Market Leaders Profiled |

Honeywell International, Inc., Microsemi Corporation, (Microchip Technology), NVE Corporation, NXP, Semiconductors N.V., Robert Bosch GmbH, TDK Corporation, MEMSIC Semiconductor Co., Ltd. (IDG Capital Investment Consultant Beijing Co Ltd.), Infineon, Technologies AG, Magnetic Sensors Corporation MultiDimension Technology Co., Ltd. |

SEGMENTAL ANALYSIS

By End Use Insights

The automotive segment dominated the Europe magnetic sensor market and accounted for a 42.8% share in 2025. This dominance of the segment is mainly driven by the increasing integration of advanced driver assistance systems and the widespread adoption of electric vehicles which require precise sensing for motor control and battery management. In 2024, the EU produced 11.4 million passenger cars, a 6.2% decrease from the previous year. Although fully electric (BEV) sales dipped to a 13.6% market share, hybrid-electric vehicles (HEVs) reached a record 30.9% share, maintaining high demand for magnetic sensors in current-sensing and position-monitoring roles. The transition to electric mobility necessitates the utilize of high precision Hall effect and magnetoresistive sensors to ensure the efficient operation of inverters and traction motors. According to the IEA, European electric car sales were approximately 3.2 million units when including both EU and non-EU countries (like the UK and Norway). However, growth within the EU-27 specifically stagnated at roughly 2.4 million units. Furthermore safety regulations mandate the inclusion of multiple sensors for steering angle detection wheel speed monitoring and pedal position sensing. The complexity of modern vehicle architectures requires robust and reliable sensing solutions to maintain performance and safety standards. Hence, the structural shift towards electrification and automation in the automotive industest sustains the leadership of this segment in the European market.

The industrial segment is estimated to register the rapidest CAGR of 8.5% from 2026 to 2034 due to the rapid expansion of Industest 4.0 initiatives and the increasing deployment of industrial robots and automated machinery across European manufacturing facilities. The World Robotics 2025 Report by the IFR indicates that 2024 saw 85,000 new robots installed in Europe. The electronics sector increased its share of global installations to 24%, narrowly overtaking the automotive sector (23%) as the leading adopter. Magnetic sensors are essential components in these systems providing accurate feedback for motor control position sensing and predictive maintenance applications. As per the European Commission the digital transformation of compact and medium sized enterprises is a key priority driving the adoption of smart sensors that enable real time monitoring and data analysis. The push for energy efficiency in industrial processes also encourages the utilize of precise current sensors to optimize power consumption. Additionally the growth of renewable energy infrastructure such as wind turbines relies on magnetic sensors for pitch and yaw control. The demand for reliable and durable sensors in harsh industrial environments further supports market expansion. Thus, the convergence of automation digitalization and sustainability goals drives the rapid growth of the industrial segment.

By Technology Insights

The Hall Effect segment led the Europe magnetic sensor market and captured a 55.7% share in 2025. This leading position of the segment is attributed to the mature technology cost effectiveness and versatility of Hall Effect sensors in a wide range of applications including automotive consumer electronics and industrial equipment. These sensors are widely utilized for position speed and current sensing due to their robustness and ability to operate in harsh environments. According to the Semiconductor Industest Association Hall Effect sensors remain the most commonly utilized magnetic sensing technology globally due to their established manufacturing processes and low production costs. In Europe the automotive sector extensively utilizes Hall Effect sensors for wheel speed detection and transmission control systems. As per the European Automobile Manufacturers Association the average modern vehicle contains numerous Hall Effect sensors to support various electronic control units. The technology’s ability to provide non contact measurement ensures long term reliability and minimal wear. Furthermore advancements in integrated circuit technology have enabled the development of smart Hall Effect sensors with enhanced features such as temperature compensation and digital output. The widespread availability and proven performance of Hall Effect sensors create them the preferred choice for many manufacturers. As a result, the combination of affordability reliability and broad applicability ensures the continued dominance of the Hall Effect segment in the European market.

The Tunnel Magnetoresistance segment is anticipated to witness the rapidest CAGR of 12.3% over the forecast period owing to the demand for high sensitivity and low power consumption in advanced applications. Tunnel Magnetoresistance sensors offer superior performance compared to traditional technologies building them ideal for precise current sensing and angle detection in electric vehicles and industrial automation. According to the Institute of Electrical and Electronics Engineers Tunnel Magnetoresistance technology provides higher signal to noise ratios and better thermal stability which are critical for high precision applications. The increasing complexity of electric powertrains requires sensors that can accurately measure high currents with minimal interference. As per the European Battery Alliance the development of next generation battery management systems relies on advanced sensing technologies to optimize performance and safety. Tunnel Magnetoresistance sensors are also gaining traction in consumer electronics for compass and gesture recognition applications due to their compact form factor and low power requirements. The ongoing miniaturization of electronic devices further boosts the demand for compact and efficient sensing solutions. Additionally research and development efforts are focutilized on improving the manufacturing yield and reducing the cost of Tunnel Magnetoresistance sensors. Therefore, the technological advantages and expanding application scope drive the rapid adoption of Tunnel Magnetoresistance sensors in the European market.

By Application Insights

The position sensing segment held the majority share of 38.6% of the Europe magnetic sensor market in 2025. This supremacy of the segment is credited to the critical necessary for accurate position detection in automotive systems industrial machinery and consumer devices. Magnetic sensors provide reliable and non contact position feedback which is essential for the precise control of motors valves and actuators. According to the VDMA German Mechanical Engineering Industest Association the adoption of automated systems in European manufacturing has increased the demand for high precision position sensors to ensure operational efficiency. In the automotive sector position sensors are utilized for throttle pedal steering angle and seat position monitoring contributing to vehicle safety and comfort. As per the European Automobile Manufacturers Association the integration of advanced driver assistance systems requires multiple position sensors to track the relocatement of various components. The reliability of magnetic sensors in harsh environments creates them preferable over optical or capacitive alternatives in many industrial applications. Furthermore the growth of robotics and collaborative robots necessitates accurate joint position sensing to enable smooth and safe operations. The continuous improvement in sensor accuracy and resolution further enhances their suitability for demanding applications. Consequently the widespread utilize of position sensing in key industries sustains its leadership in the European magnetic sensor market.

The navigation and electronic compass segment is likely to experience the rapidest CAGR of 11.8% between 2026 and 2034. This swift growth of the segment is fueled by the proliferation of smartphones wearable devices and Internet of Things products that require precise orientation and heading information. Magnetic sensors are integral to electronic compasses enabling accurate navigation in mobile devices and autonomous systems. Research highlights that Europe is anticipated to exhibit a significant growth rate in the magnetic sensor market through 2030. This is largely driven by the demand for integrated navigation in hybrid vehicles and high-precision magnetometers in smartphones for enhanced augmented reality (AR) experiences. The integration of three axis magnetometers in smartphones allows for improved map orientation and indoor navigation capabilities. For logistics and smart infrastructure, the industest is shifting toward Magnetostrictive Position Sensors. These sensors provide the durability necessaryed for long-term outdoor asset tracking and renewable energy systems like solar trackers. Autonomous drones and robots also utilize electronic compasses for navigation and stabilization enhancing their operational effectiveness. The development of sensor fusion algorithms that combine magnetic data with accelerometer and gyroscope readings further improves accuracy. Additionally the rise of smart home devices incorporating gesture control and orientation features contributes to market growth. Hence, the increasing reliance on location aware technologies and autonomous systems drives the rapid expansion of the navigation and electronic compass segment.

COUNTRY ANALYSIS

Germany Magnetic Sensors Market Analysis

Germany outperformed other countries in the Europe magnetic sensors market and occupied a 24.5% share in 2025. The demand for these sensors in Germany is propelled by its robust automotive industest and strong manufacturing base which are major consumers of advanced sensing technologies. The Ministest identifies the automotive industest as a central pillar of the national economy, actively supporting the transition toward electromobility and climate-neutral production processes. The presence of leading semiconductor manufacturers and sensor producers in Germany fosters innovation and local supply chain resilience. The association reports that German manufacturers and suppliers are undertaking historically high investments in research and development, specifically tarobtaining electric mobility, autonomous driving, and digitalization. The industrial sector also contributes significantly to demand with the implementation of Industest 4.0 initiatives requiring smart sensors for automation and predictive maintenance. Germany’s focus on research and development supports the advancement of sensor technologies including Tunnel Magnetoresistance and Giant Magnetoresistance. Government incentives for sustainable manufacturing and energy efficiency further encourage the utilize of precise current and position sensors. Thus, Germany’s industrial strength and technological leadership sustain its dominance in the European magnetic sensor market.

United Kingdom Magnetic Sensors Market Analysis

The United Kingdom followed closely behind in the Europe magnetic sensor market and captured a 16.4% share in 2025. The market status in the UK is fuelled by a strong consumer electronics sector and a vibrant aerospace industest which drive demand for miniaturized and high performance sensors. According to the Office for National Statistics, the digital sector remains a significant contributor to the UK economy, with high rates of internet usage among adults and businesses. The aerospace industest relies on magnetic sensors for navigation systems and flight control mechanisms requiring high reliability and accuracy. The trade organisation representing the aerospace and defence sectors highlights continued innovation in sustainable aviation and advanced air mobility, which underpins the industest’s global competitiveness. The UK is also a hub for fintech and medical device innovation which utilizes magnetic sensors for secure authentication and diagnostic equipment. Government initiatives supporting digital innovation and clean growth promote the development of smart sensing technologies. The presence of leading universities and research centers fosters collaboration between academia and industest. Additionally the retail sector’s adoption of electronic article surveillance systems contributes to market volume. As a result, the UK’s diverse industrial base and focus on innovation maintain its prominent position in the regional market.

France Magnetic Sensors Market Analysis

France occupies a significant position in the Europe magnetic sensor market due to its strong aerospace and defense sectors as well as its commitment to renewable energy. The Ministest recognizes the aeronautics and space sector as a leading contributor to the national trade balance and a priority for industrial sovereignty and decarbonization efforts. The expansion of wind energy capacity in France also drives demand for magnetic sensors utilized in turbine pitch and yaw control. The association emphasizes the critical necessary to accelerate the deployment of both onshore and offshore wind capacity to meet national renewable energy tarobtains and ensure energy security. The automotive sector in France is transitioning towards electric mobility which boosts the demand for current and position sensors. Government policies promoting industrial sovereignty and digital transformation encourage local production and innovation in sensor technologies. The presence of major semiconductor companies and research institutions facilitates the development of next generation magnetic sensors. Additionally the healthcare sector’s adoption of medical devices utilizing magnetic sensing contributes to market growth. Thus, France’s strategic industries and energy transition goals drive steady demand for magnetic sensors.

Italy Magnetic Sensors Market Analysis

Italy is another major player in the Europe magnetic sensor market owing to its strong manufacturing sector particularly in automotive components machinery and home appliances. According to sources, the manufacturing industest remains a cornerstone of the economy with a focus on high quality and precision engineering. The automotive supply chain in Italy produces various components that require magnetic sensors for position and speed detection. Also, the white goods sector also utilizes magnetic sensors for motor control in washing machines and refrigerators contributing to volume sales. The government’s National Recovery and Resilience Plan includes investments in digitalization and innovation encouraging the adoption of smart sensors in compact and medium sized enterprises. The growth of renewable energy projects particularly in solar and wind sectors further supports market expansion. Additionally the presence of specialized sensor manufacturers in Italy strengthens the local supply chain. Consequently Italy’s manufacturing excellence and diversification sustain its significant role in the European market.

Sweden Magnetic Sensors Market Analysis

Sweden is predicted to expand notably in the Europe magnetic sensor market from 2026 to 2034 due to its leadership in industrial automation telecommunications and sustainable technologies. According to sources, the high level of industrial automation drives the demand for precise magnetic sensors in robotics and manufacturing systems. The telecommunications sector particularly with the rollout of fifth generation networks requires sensors for infrastructure monitoring and maintenance. Sweden is home to several innovative technology companies that develop advanced sensing solutions for global markets. The strong focus on sustainability and energy efficiency encourages the adoption of smart sensors for optimizing resource usage. Government support for research and development fosters innovation in materials science and sensor technology. Additionally the automotive industest’s shift towards electric vehicles boosts demand for specialized sensing components. Consequently Sweden’s technological prowess and commitment to sustainability maintain its position as a key market participant.

KEY MARKET PLAYERS

A few of the market players that are dominating the Europe magnetic sensor market are

- Honeywell International, Inc.

- STMicroelectronics NV

- Microsemi Corporation (Microchip Technology)

- NVE Corporation

- NXP Semiconductors N.V.

- Robert Bosch GmbH

- TDK Corporation

- MEMSIC Semiconductor Co., Ltd. (IDG Capital Investment Consultant Beijing Co Ltd.)

- Infineon Technologies AG

- Magnetic Sensors Corporation

- MultiDimension Technology Co., Ltd.

Top Players In The Market

- Infineon Technologies AG is a leading semiconductor manufacturer in Europe with a robust portfolio of magnetic sensors including Hall effect and magnetoresistive devices. The company contributes significantly to the global market by providing innovative sensing solutions for automotive industrial and consumer applications. Infineon focutilizes on integrating magnetic sensors with microcontrollers to create smart systems that enhance performance and efficiency. Recent actions include expanding production capabilities in Germany and launching new XENSIV sensor families designed for high precision. The company collaborates with automotive original equipment manufacturers to develop customized solutions for electric vehicles. By leveraging expertise in power semiconductors Infineon strengthens its market position through comprehensive system offerings. Its commitment to sustainability aligns with European regulations ensuring long term competitiveness. This strategic focus on innovation solidifies its reputation as a key provider of advanced magnetic sensing technologies.

- STMicroelectronics NV is a major global semiconductor company with significant operations in Europe specializing in a wide range of magnetic sensors. The firm contributes to the global market by delivering high performance Hall effect and magnetoresistive sensors for diverse applications. STMicroelectronics emphasizes the development of miniaturized and energy efficient sensors that meet modern electronic system demands. Recent initiatives include introducing new magnetic sensor modules with integrated signal processing capabilities to ease design complexity. The company partners with technology firms to co develop solutions for smart home and wearable devices. STMicroelectronics invests heavily in research and development to advance sensor technology and maintain leadership. Its strong presence in the automotive sector supports the transition to electric mobility. The company focutilizes on quality and innovation. This approach reinforces its position as a trusted supplier in the European magnetic sensor market.

- TDK Corporation is a prominent electronics company with a substantial presence in the European magnetic sensor market through its subsidiary EPCOS. The organization offers a comprehensive range of magnetic sensors including Hall integrated circuits and magnetoresistive sensors for industrial and automotive utilizes. TDK contributes to the global market by providing high quality and reliable sensing solutions that meet stringent industest standards. Recent actions involve expanding sensor production facilities in Europe and launching new product lines tailored for electric vehicle applications. The company focutilizes on developing sensors with enhanced temperature stability to address harsh operating environments. TDK collaborates with automotive suppliers to integrate its sensors into advanced systems. Its commitment to innovation ensures it remains a competitive player. TDK leverages material science expertise to deliver superior components. These components enhance system performance and strengthen the company’s regional market position.

Top Strategies Used By The Key Market Participants

Key players in the Europe magnetic sensor market primarily focus on product innovation and technological advancement to maintain competitive advantage. Companies invest heavily in research and development to create miniaturized low power and high precision sensors that meet evolving customer requirements. Strategic partnerships and collaborations with automotive manufacturers and industrial equipment producers are common to co develop customized solutions. Firms also pursue vertical integration to control the supply chain for critical raw materials and components ensuring stability and cost efficiency. Expansion into emerging application areas such as renewable energy and Internet of Things devices allows companies to diversify their revenue streams. Marketing efforts emphasize the reliability and performance of magnetic sensors in harsh environments to differentiate from alternative technologies. Additionally manufacturers prioritize compliance with environmental regulations and sustainability standards to align with European policies. By combining innovation strategic alliances and operational efficiency key participants strengthen their market positions and drive growth in the dynamic European landscape.

MARKET SEGMENTATION

This research report on the Europe magnetic sensor market is segmented and sub-segmented into the following categories.

By End-utilize

- Automotive

- Consumer Electronics

- Industrial

- Others

By Technology

- Hall Effect

- Anisotropic Magnetoresistance

- Giant Magnetoresistance

- Tunnel Magnetoresistance

- Others

By Application

- Position Sensing

- Speed Sensing

- Detection/NDT

- Navigation & Electronic Compass

- Others

By Countest

- UK

- Russia

- Germany

- Italy

- France

- Spain

- Sweden

- Denmark

- Poland

- Switzerland

- Netherlands

- Rest of Europe