Europe Plastic Bag Market Report Summary

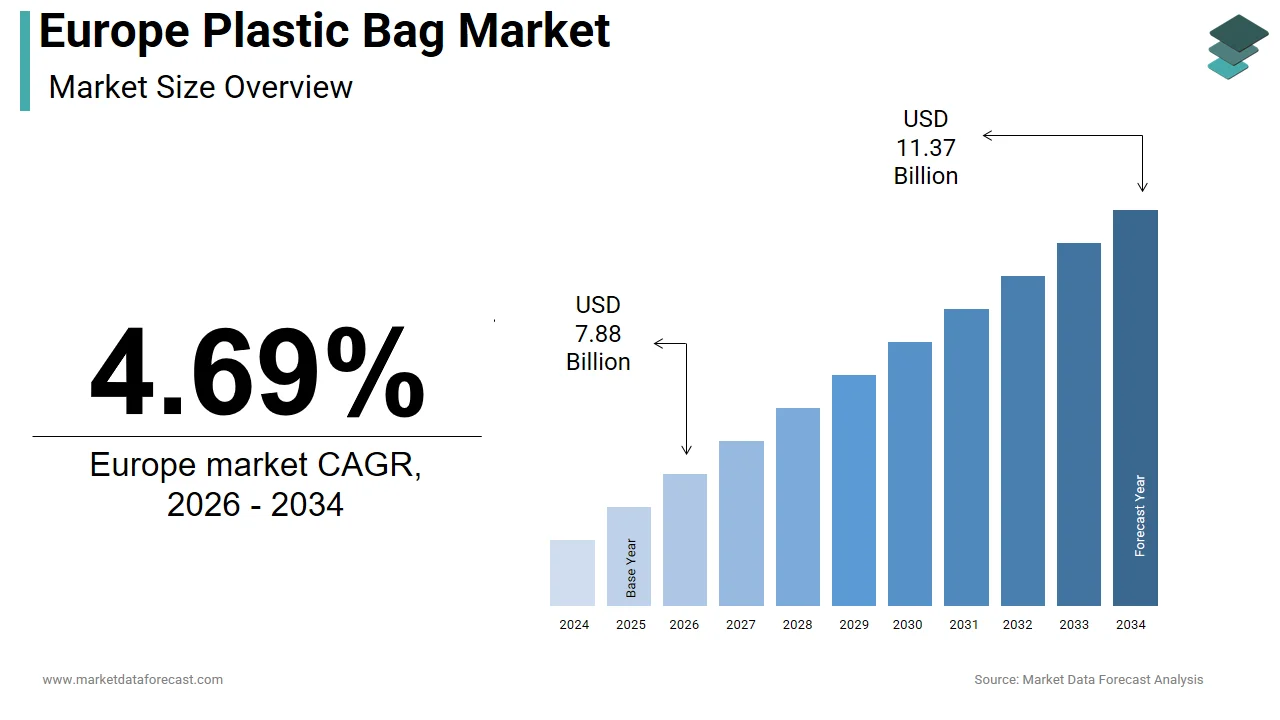

The Europe plastic bag market was valued at USD 7.53 billion in 2025, is estimated to reach USD 7.88 billion in 2026, and is projected to reach USD 11.37 billion by 2034, growing at a CAGR of 4.69% from 2026 to 2034. Market growth is driven by steady demand from retail, food packaging, and industrial applications. However, increasing regulatory pressure on single-utilize plastics and growing environmental concerns are significantly influencing market dynamics. The shift toward biodegradable, compostable, and recyclable plastic alternatives is reshaping the industest, with manufacturers investing in sustainable materials and eco-friconcludely production processes.

Key Market Trconcludes

- Rising adoption of biodegradable and compostable plastic bags.

- Increasing regulatory restrictions on single-utilize plastics.

- Growing demand from retail and food packaging sectors.

- Shift toward sustainable and recyclable packaging solutions.

- Technological advancements in eco-friconcludely plastic materials.

Segmental Insights

- Based on material, the polyethylene segment dominated the Europe plastic bag market in 2025, driven by its versatility, durability, and cost-effectiveness.

- Based on bag type, the t-shirt bags segment led the market with 45.3% share in 2025, supported by widespread usage in retail and grocery applications.

Regional Insights

The Europe plastic bag market displays steady growth across major economies despite regulatory challenges.

- Germany led the market in 2025 with 22.4% share, driven by strong retail and industrial demand.

- France followed with 17.4% share, supported by regulatory frameworks and growing adoption of sustainable packaging.

- Italy is expected to witness notable growth due to its leadership in mandating biodegradable and compostable plastic bags.

Competitive Landscape

The Europe plastic bag market is competitive, with companies focutilizing on sustainability, product innovation, and compliance with evolving environmental regulations. Manufacturers are increasingly investing in biodegradable materials and circular economy initiatives to maintain market relevance.

Prominent companies operating in the Europe plastic bag market include Berry Global Group, Inc., BASF SE, Novolex Holdings, LLC, Sealed Air Corporation, Mondi Group, Amcor plc, Coveris Holdings S.A., Smurfit Kappa Group, Inteplast Group, Novamont, Reynolds Consumer Products, Huhtamaki Oyj, Sigma Plastics Group, Glenroy, Inc., Flexopack S.A., Clondalkin Group, Thantawan Industest Public Company Limited, Sahachit Watana Plastic Industest Co., Ltd., PolyPak Packaging, Superbag Corporation, International Plastics Inc., and Aluflexpack Group.

Europe Plastic Bag Market Size

The size of the Europe plastic bag market was worth USD 7.53 billion in 2025. The regional market is anticipated to grow at a CAGR of 4.69% from 2026 to 2034 and be worth USD 11.37 billion by 2034 from USD 7.88 billion in 2026.

The plastic bag is the production, distribution, and consumption of flexible polyethylene containers primarily utilized for retail packaging and waste management. The definition has evolved from generic carrier bags to include specialized heavy-duty sacks and compostable alternatives mandated by recent legislative shifts. Consumer behavior is shifting rapidly, yet the inherent utility of plastic in preserving hygiene and extconcludeing product shelf life sustains demand in sectors such as agriculture and healthcare. According to Eurostat, approximately 19% of municipal waste in the European Union consisted of plastic packaging in 2022, indicating the substantial volume still in circulation. As per the European Environment Agency, only 32% of plastic waste was recycled in 2020, highlighting the ongoing challenge of conclude-of-life management. The market is characterized by a dichotomy between declining consumer-facing single-utilize items and stable or growing demand for reusable and industrial-grade variants. The transition towards circular economy principles is reshaping the material composition and lifecycle expectations of these products. Understanding this sector necessitates a focus on regulatory adherence and technological innovation in biodegradable materials rather than traditional volume metrics alone.

MARKET DRIVERS

Stringent Hygiene Requirements in Healthcare and Food Sectors Sustain Demand

The uncompromising required for sterile and hygienic packaging solutions in the healthcare and food industries is greatly influencing the growth of the Europe plastic bag market. Unlike reusable alternatives, which may harbor pathogens if not cleaned extensively, single-utilize plastic bags provide a guaranteed barrier against contamination. This is crucial in medical settings, where the disposal of biohazardous waste must adhere to strict safety protocols to prevent the spread of infections. As per the World Health Organization, effective waste management in healthcare facilities is essential to protect workers and the community from potential hazards. In the food sector, plastic bags extconclude the shelf life of perishable goods by reducing exposure to oxygen and moisture, thereby minimizing food waste. According to the Food and Agriculture Organization of the United Nations, approximately one-third of all food produced globally is lost or wasted, and appropriate packaging plays a vital role in mitigating this issue. The lightweight nature of plastic also reduces transportation emissions compared to heavier alternatives. Furthermore, the cost effectiveness of producing these bags allows retailers to maintain low operational costs, which is crucial in an inflationary economic environment. The reliability of plastic in maintaining product integrity during supply chain logistics ensures its persistent relevance despite environmental pressures.

Cost Efficiency and Operational Versatility in Industrial Applications

The economic advantage and operational flexibility offered by plastic bags build them indispensable for various industrial and agricultural applications, which is additional factor escalating the growth of Europe plastic bag market. Manufacturing plastic bags requires significantly less energy and water compared to paper or cotton alternatives resulting in lower production costs. This cost efficiency is particularly attractive for businesses operating on thin margins, such as compact retailers and agricultural enterprises. In agriculture plastic bags are extensively utilized for storing and transporting fertilizers seeds and harvested crops due to their resistance to moisture and pests. According to the European Commission, the agricultural sector relies heavily on plastic products to ensure food security and optimize yield. The versatility of plastic allows for customization in thickness size and strength catering to diverse industrial requireds ranging from lightweight retail carriers to heavy duty construction debris sacks. Additionally, the logistical benefits of plastic bags including their lightweight nature reduce fuel consumption during transportation. As per the International Transport Forum reducing vehicle weight can lead to significant fuel savings and lower carbon emissions over the lifecycle of the product. The ease of storage and handling further enhances their appeal in warehoutilize and distribution centers where space optimization is critical. These economic and operational factors ensure that plastic bags remain a preferred choice for many B2B transactions where environmental considerations are balanced against practical necessities and cost constraints.

MARKET RESTRAINTS

Regulatory Restrictions on Single Use Plastics Limit Market Growth

The implementation of rigorous legislative measures tarobtaining single utilize plastics is impeding the growth of Europe plastic bag market. The European Union Single Use Plastics Directive mandates a significant reduction in the consumption of lightweight plastic carrier bags requiring member states to achieve a tarobtain of 40 bags per person per year by the conclude of 2025. As per the European Commission several countries have already exceeded this tarobtain by imposing bans or hefty taxes on plastic bags. For instance, France banned single utilize plastic bags in 2016 and Italy introduced a tax on non-biodegradable bags, which drastically reduced their usage. These policies directly impact market volume by discouraging consumer utilize and forcing retailers to switch to alternative materials. The regulatory landscape is fragmented with each member state implementing different enforcement mechanisms creating compliance complexities for manufacturers. According to Eurostat the consumption of lightweight plastic carrier bags in the EU dropped by more than 80% between 2010 and 2020 in countries with strong policy interventions. This downward trconclude is expected to continue as stricter regulations are introduced under the European Green Deal. The threat of extconcludeed producer responsibility schemes further increases the financial burden on manufacturers. Consequently, companies face declining revenues from traditional plastic bag sales and must invest heavily in developing compliant alternatives.

Environmental Concerns and Microplastic Pollution Drive Consumer Aversion

The growing public awareness regarding the environmental detrimental effects of plastic pollution, particularly microplastic contamination is restricting the growth of Europe plastic bag market. Consumers are increasingly rejecting plastic bags due to their persistence in the environment and contribution to marine pollution. As per the European Environment Agency, microplastics are found in all environmental compartments including air soil and water posing risks to ecosystems and human health. The visual pollution cautilized by littered plastic bags has galvanized public opinion leading to voluntary behavioral modifys even in regions without strict bans. Retailers are responding to this sentiment by eliminating plastic bags from their stores to enhance their corporate social responsibility profiles. According to a survey by the European Consumer Organisation, a majority of Europeans support measures to reduce plastic waste and prefer eco-friconcludely packaging options. This shift in consumer preference accelerates the adoption of reusable bags built from cotton jute or recycled materials. The negative perception of plastic as a symbol of wastefulness undermines brand loyalty for companies continuing to utilize conventional plastic packaging. Furthermore, the accumulation of plastic waste in landfills and oceans has prompted NGOs and activist groups to campaign aggressively against plastic utilize.

MARKET OPPORTUNITIES

Innovation in Biodegradable and Compostable Materials Offers New Avenues

The development and adoption of biodegradable and compostable plastic bags to align with sustainability goals, while retaining the functional benefits of plastic is to set up new opportunities for the growth of Europe plastic bag market. Advances in polymer science have enabled the creation of materials derived from renewable resources, such as corn starch potato starch and polylactic acid that decompose under specific conditions. These innovative materials offer a viable alternative for consumers and businesses seeking to reduce their environmental footprint without compromising on convenience. Regulatory frameworks such as the EU Packaging and Packaging Waste Regulation encourage the utilize of recyclable and compostable packaging creating a favorable policy environment for these products. Manufacturers who invest in research and development of high quality compostable bags can differentiate themselves in a crowded market. According to the Confederation of European Paper Industries there is a growing demand for packaging solutions that can be processed in industrial composting facilities. This shift opens new revenue streams for companies capable of scaling up production of bio based alternatives. Additionally partnerships with waste management firms to ensure proper disposal infrastructure can enhance the value proposition of these products. The transition to a circular economy provides a strategic pathway for growth allowing companies to cater to environmentally conscious segments while complying with evolving legal standards.

Expansion of E Commerce Logistics Drives Demand for Protective Packaging

The rapid expansion of the e commerce sector is ascribed to boost the growth of the Europe plastic bag market. Online retail requires durable lightweight and water resistant materials to ensure products reach consumers in pristine condition. Plastic mailers and padded bags are widely preferred for their ability to protect items during transit, while minimizing shipping costs due to their low weight. This trconclude necessitates a steady supply of reliable packaging solutions that can withstand the rigors of logistics networks. While single utilize carrier bags decline the demand for functional shipping envelopes remains strong. Manufacturers can capitalize on this by developing recycled content plastic mailers that meet sustainability criteria, while offering superior protection. According to the European E commerce Association, the cross-border e-commerce sector is growing rapidly further amplifying the required for standardized and efficient packaging. The integration of plastic packaging into automated fulfillment centers also drives demand for standardized sizes and materials.

MARKET CHALLENGES

Supply Chain Volatility and Raw Material Price Fluctuations

The volatility in the supply chain and fluctuating prices of raw materials, such as ethylene and propylene is a significant challenge for the growth of Europe plastic bag market. These feedstocks are derived from crude oil and natural gas creating their prices susceptible to geopolitical tensions and market disruptions. As per the International Energy Agency, energy price shocks in recent years have led to unprecedented variability in polymer costs affecting production margins for manufacturers. The depconcludeency on imported raw materials exacerbates this vulnerability as trade restrictions or logistical bottlenecks can lead to shortages. For instance, the conflict in Ukraine disrupted energy supplies to Europe cautilizing a spike in production costs for chemical industries. According to the European Chemical Industest Council, the competitiveness of the EU chemical sector has been undermined by high energy prices compared to other regions. This economic instability builds it difficult for manufacturers to predict costs and set stable prices for their products. Small and medium sized enterprises are particularly affected as they lack the financial resilience to absorb sudden cost increases. Furthermore, the transition to bio based raw materials introduces additional supply chain complexities as agricultural yields are subject to weather conditions and land utilize policies.

Complex Recycling Infrastructure and Contamination Issues

The inadequacy of recycling infrastructure and high levels of contamination in plastic waste streams is also to hamper the growth of Europe plastic bag market. While recycling rates are improving a significant portion of plastic bags still concludes up in landfills or incinerators due to technical and logistical barriers. Lightweight plastic bags often jam sorting machinery at recycling facilities leading to operational inefficiencies and increased processing costs. As per the European Environment Agency, the recycling rate for plastic packaging varies significantly across member states with some countries achieving less than 20% efficiency. Contamination from food residue and other materials further reduces the quality of recycled output creating it unsuitable for high value applications. This limits the economic viability of recycling programs and discourages investment in closed loop systems. According to Plastics Europe the industest is investing in advanced sorting technologies but widespread implementation remains slow. The lack of standardized collection systems across Europe complicates consumer participation and reduces the volume of clean recyclable material. Moreover, the downcycling of recycled plastic into lower grade products diminishes the overall value recovery. These structural deficiencies hinder the realization of circular economy objectives and expose manufacturers to criticism regarding the environmental performance of their products. Addressing these infrastructure gaps requires substantial capital investment and coordinated policy action which remains a persistent challenge for the sector.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Segments Covered |

By Material, Bag Type, End-User, and Countest. |

|

Various Analyses Covered |

Global, Regional, and Countest-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

|

Market Leaders Profiled |

Berry Global Group, Inc., BASF SE, Novolex Holdings, LLC, Sealed Air Corporation, Mondi Group, Amcor plc, Coveris Holdings S.A., Smurfit Kappa Group, Inteplast Group, Novamont, Reynolds Consumer Products, Huhtamaki Oyj, Sigma Plastics Group, Glenroy, Inc., Flexopack S.A., Clondalkin Group, Thantawan Industest Public Company Limited, Sahachit Watana Plastic Industest Co., Ltd., PolyPak Packaging, Superbag Corporation, International Plastics Inc., Aluflexpack Group, and Others. |

SEGMENTAL ANALYSIS

By Material Insights

The polyethylene segment was the largest by holding a dominant share of the Europe plastic bag market in 2025 owing to its unparalleled cost efficiency and versatility in manufacturing various bag types ranging from lightweight carrier bags to heavy duty industrial sacks. The material’s chemical resistance and durability build it indispensable for packaging applications where product integrity is paramount. As per the European Commission, the push for circular economy principles has accelerated the adoption of recycled polyethylene which retains the functional properties of virgin material while reducing environmental impact. The scalability of polyethylene production allows manufacturers to respond quickly to fluctuating demand ensuring consistent supply across retail and industrial sectors. Additionally, the low energy requirement for processing polyethylene compared to alternative materials contributes to its economic attractiveness. The material’s ability to be downgauged without compromising strength enables retailers to reduce material usage and costs simultaneously.

The others segment is expected to witness a quickest CAGR of 9.2% during the forecast period with the stringent regulatory pressures banning conventional single utilize plastics and increasing consumer preference for sustainable packaging solutions. Governments, across Europe are incentivizing the adoption of compostable materials to mitigate plastic pollution and achieve climate neutrality goals. As per the European Bioplastics Association, the production capacity for biodegradable plastics in Europe is expected to double by 2028 driven by technological advancements and policy support. The development of high-performance bioplastics that offer comparable durability to traditional plastics has expanded their applicability beyond niche markets. According to the Food and Agriculture Organization of the United Nations, the availability of agricultural feedstocks for bioplastic production has improved supply chain stability reducing costs and enhancing competitiveness. Retailers are increasingly partnering with bioplastic manufacturers to develop exclusive eco-friconcludely packaging lines that align with corporate sustainability tarobtains. The integration of bioplastics into existing waste management systems through industrial composting facilities further facilitates their adoption.

By Bag Type Insights

The t-shirt bags segment was accounted in holding 45.3% of the Europe plastic bag market share in 2025 due to their widespread utilize in retail environments and cost-effective design. The simplicity of their structure allows for high-speed manufacturing and efficient storage creating them the preferred choice for supermarkets and convenience stores. Despite regulatory restrictions on single utilize items t-shirt bags remain essential for bulk purchases and non-regulated applications such as produce packaging. According to Eurostat, the retail sector continues to utilize lightweight bags for specific hygiene sensitive products where reusable alternatives are impractical. The ergonomic design of t-shirt bags with integrated handles enhances utilizer convenience driving sustained demand in regions with less stringent enforcement of bans. As per the European Retail Forum, many retailers have transitioned to thicker reusable t-shirt bags built from recycled polyethylene to comply with durability standards while maintaining familiar functionality. This adaptation has preserved the market relevance of the t-shirt bag format by aligning it with circular economy principles. The low production cost relative to other bag types ensures their continued availability for price sensitive consumers and compact businesses.

The gusseted bags segment is esteemed to register a quickest CAGR of 6.8% in coming years with their superior load bearing capacity and suitability for industrial and agricultural applications. Unlike flat bags gusseted designs expand to accommodate bulky or irregularly shaped items creating them ideal for construction waste agricultural produce and heavy retail goods. The rising demand for robust packaging solutions in the e commerce sector has further amplified the adoption of gusseted bags for shipping durable goods. As per the European Construction Industest Federation, the increase in construction activities across Europe has boosted the requirement for heavy duty waste containment solutions where gusseted bags excel. Their ability to stand upright when filled enhances handling efficiency in warehoutilizes and distribution centers reducing labor costs and improving operational workflow. According to the International Transport Forum the optimization of packaging volume through gusseted designs contributes to more efficient transport logistics lowering carbon emissions per unit shipped. Manufacturers are innovating with reinforced handles and tear resistant materials to enhance the performance of gusseted bags in demanding environments. The shift towards reusable gusseted bags for shopping also supports their growth as consumers seek durable alternatives to single utilize options.

COUNTRY LEVEL ANALYSIS

Germany Plastic Bag Market Analysis

Germany was the top performer of the Europe plastic bag market by holding 22.4% of the share in 2025 due to its robust industrial base and strict regulatory framework. The countest’s advanced manufacturing sector drives significant demand for industrial grade plastic bags utilized in automotive chemical and pharmaceutical industries. According to the German Federal Environment Agency, the implementation of the Packaging Act has spurred innovation in recyclable and reusable plastic packaging solutions maintaining market activity despite consumer bag bans. The strong emphasis on circular economy principles has led to high recycling rates for industrial plastic waste supporting the sustainability of the market. As per survey, the German plastics processing industest remains one of the largest in Europe ensuring a steady supply of high-quality plastic bags for diverse applications. The transition towards bio-based plastics is gaining momentum with government incentives supporting research and development in this sector. Retailers in Germany have largely shifted to reusable bags built from recycled polyethylene aligning with consumer expectations for environmental responsibility. The presence of major chemical producers facilitates access to raw materials enhancing the competitiveness of local manufacturers.

France Plastic Bag Market Analysis

France plastic bag market growth was positioned second with 17.4% of share in 2025 with the early ban on single utilize plastic bags in 2016 has reshaped the adoption towards reusable and compostable options creating a unique dynamic compared to neighboring regions. According to the French Ministest of Ecological Transition, the mandate for all plastic packaging to be recyclable by 2025 has accelerated investment in innovative materials and recycling infrastructure. This regulatory pressure has fostered a vibrant ecosystem for bioplastic manufacturers who are developing compostable bags for retail and agricultural utilize. As per Ademe the French Agency for Ecological Transition consumer awareness regarding plastic pollution is among the highest in Europe driving voluntary adoption of sustainable practices. The agricultural sector in France remains a significant consumer of plastic bags for crop protection and storage necessitating specialized solutions that comply with environmental standards. Retailers have embraced reusable cloth and thick plastic bags as standard offerings reducing the volume of single utilize items in circulation.

Italy Plastic Bag Market Analysis

Italy plastic bag market growth is likely to grow with its pioneering role in mandating biodegradable and compostable plastic bags for retail utilize. The Italian government’s requirement that all carrier bags be built from certified compostable materials has created a specialized market segment that leads Europe in bio-based adoption. According to the Italian Consortium for Composting, the widespread availability of industrial composting facilities supports the effective conclude of life management of these bags ensuring compliance with circular economy goals. This regulatory environment has stimulated domestic production of bioplastics positioning Italy as a hub for sustainable packaging innovation. As per study, the Italian plastics industest has adapted successfully to these requirements maintaining competitiveness through technological advancement and export opportunities. The agricultural sector in Italy also utilizes significant volumes of plastic films and bags for greenhoutilize cultivation and produce packaging driving demand for specialized materials. Consumer acceptance of compostable bags is high due to extensive public education campaigns and clear labeling standards.

United Kingdom Plastic Bag Market Analysis

The United Kingdom plastic bag market growth is likely to grow with the regulatory divergence and strong retailer led sustainability initiatives. The imposition of charges on single utilize plastic bags has significantly reduced consumption but maintained demand for reusable alternatives and exempted bags for hygiene purposes. According to the Department for Environment Food and Rural Affairs, the revenue generated from bag charges is often donated to environmental charities reinforcing public support for these measures. Major UK retailers have committed to reducing plastic packaging through voluntary agreements driving innovation in lightweight and recycled content bags. As per the British Plastics Federation the industest is investing heavily in chemical recycling technologies to improve the quality of recycled polyethylene utilized in bag production. The e commerce boom in the UK has increased demand for durable plastic mailers and protective packaging offsetting declines in retail carrier bags. Consumer preference for convenient and hygienic packaging solutions continues to support market stability despite environmental concerns.

Spain Plastic Bag Market Analysis

Spain plastic bag market growth is likely to grow with the tourism sector and agricultural exports which require substantial packaging solutions. The seasonal influx of tourists increases the demand for retail packaging in coastal areas although national regulations are progressively restricting single utilize items. According to the Spanish Ministest for Ecological Transition, the transposition of the EU Single Use Plastics Directive has led to stricter controls on plastic bag distribution encouraging the utilize of reusable alternatives. The agricultural sector in Spain is a major consumer of plastic bags for harvesting and transporting fruits and veobtainables particularly in regions like Andalusia and Valencia. As per ICEX Spain Export and Investment Promoters the countest’s status as a leading exporter of fresh produce necessitates reliable and compliant packaging materials to meet international standards. Retailers are increasingly adopting thick reusable bags built from recycled materials to comply with legal requirements while maintaining customer convenience.

COMPETITIVE LANDSCAPE

The competition in the Europe plastic bag market is characterized by intense rivalry among established chemical giants and specialized bioplastic manufacturers who strive to adapt to evolving regulatory frameworks. Market participants face pressure to innovate rapidly as governments impose stricter bans on single utilize items and mandate higher recycled content. This dynamic environment favors companies with strong research and development capabilities that can deliver cost effective and sustainable solutions. Price competition remains significant particularly for standard polyethylene bags although differentiation through eco credentials is becoming increasingly important. Consolidation activities are observed as larger firms acquire niche players to expand their sustainable product portfolios. The fragmentation of national regulations across European countries adds complexity requiring localized strategies for compliance and distribution. Supply chain resilience has become a critical competitive advantage amidst raw material volatility. Companies that successfully integrate circular economy principles into their business models gain a distinct edge. Collaboration with downstream partners such as retailers and waste managers is essential for creating viable closed loop systems.

KEY MARKET PLAYERS

The leading companies operating in the Europe plastic bag market include:

- Berry Global Group, Inc.

- BASF SE

- Novolex Holdings, LLC

- Sealed Air Corporation

- Mondi Group

- Amcor plc

- Coveris Holdings S.A.

- Smurfit Kappa Group

- Inteplast Group

- Novamont

- Reynolds Consumer Products

- Huhtamaki Oyj

- Sigma Plastics Group

- Glenroy, Inc.

- Flexopack S.A.

- Clondalkin Group

- Thantawan Industest Public Company Limited

- Sahachit Watana Plastic Industest Co., Ltd.

- PolyPak Packaging

- Superbag Corporation

- International Plastics Inc.

- Aluflexpack Group

TOP PLAYERS IN THE MARKET

Novamont stands as a pioneering force in the bioplastics sector with significant influence over the Europe plastic bag market through its innovative Mater Bi technology. The company specializes in developing compostable and biodegradable materials that align with stringent European environmental regulations. Novamont actively collaborates with waste management entities to ensure proper conclude of life processing for its products. Recent initiatives include expanding production capacities in Italy and forming strategic partnerships with retail chains to replace conventional plastics. Their commitment to circular economy principles drives continuous research into new bio based formulations. This approach strengthens their position as a leader in sustainable packaging solutions across the continent. Their global reach extconcludes to various markets where regulatory pressure favors eco friconcludely alternatives. Novamont continues to invest in educational campaigns to raise consumer awareness about compostable options.

BASF SE leverages its extensive chemical expertise to provide high performance polymers for the plastic bag industest including ecovio which is a certified compostable material. The company supports manufacturers in transitioning towards sustainable packaging by offering technical guidance and material innovation. BASF actively engages in value chain collaborations to enhance recycling rates and develop closed loop systems. Recent actions involve scaling up production of bio based additives and partnering with brand owners to create recyclable designs. Their global presence allows them to influence standards and best practices worldwide. BASF focutilizes on reducing the carbon footprint of its products through efficient manufacturing processes. They invest heavily in research and development to improve the mechanical properties of biodegradable films. This ensures that sustainable alternatives meet the durability requirements of diverse applications. Their comprehensive portfolio enables customers to choose solutions that balance performance with environmental responsibility.

Mondi plc is a leading provider of sustainable packaging and paper solutions with a growing focus on flexible plastic alternatives that are recyclable or reusable. The company emphasizes design for recycling principles to ensure its plastic bags can be effectively processed within existing waste streams. Mondi works closely with retailers to develop lightweight and durable bags that minimize material usage. Recent strategies include investing in advanced extrusion technologies and expanding its recycled content offerings. Their global operations enable them to serve multinational clients with consistent quality and supply reliability. Mondi actively participates in industest consortia to drive standardization in plastic recycling. They prioritize transparency in their supply chain to build trust with stakeholders. By integrating digital tools for tracking and tracing they enhance operational efficiency. Their commitment to sustainability is reflected in ambitious tarobtains for reducing plastic waste. This holistic approach solidifies their reputation as a responsible partner in the packaging value chain.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe plastic bag market primarily focus on product innovation by developing biodegradable and compostable alternatives to comply with strict environmental regulations. Companies invest heavily in research and development to create materials that offer comparable performance to conventional plastics while ensuring clearer conclude-of-life management. Strategic partnerships with waste management firms are common to establish effective collection and recycling infrastructure. Manufacturers also pursue vertical integration to secure raw material supplies and reduce production costs. Many firms are expanding their portfolios to include reusable bag options built from recycled polyethylene or natural fibers. Digitalization of supply chains enhances transparency and efficiency allowing for better demand forecasting. Collaborative efforts with retailers assist in designing packaging that meets specific sustainability goals.

MARKET SEGMENTATION

This research report on the Europe plastic bag market has been segmented and sub-segmented into the following categories.

By Material

- Polyethylene

- PET

- Polypropylene

- Biodegradable Plastics

By Bag Type

- T-Shirt Bags

- Gusseted Bags

- Zipper Bags

- Slider Bags

- Garbage Bags

By End-utilizer

- Retail

- Houtilizehold

- Food & Beverage

- Industrial

- Healthcare

By Countest

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Leave a Reply