Europe Esters Market Size

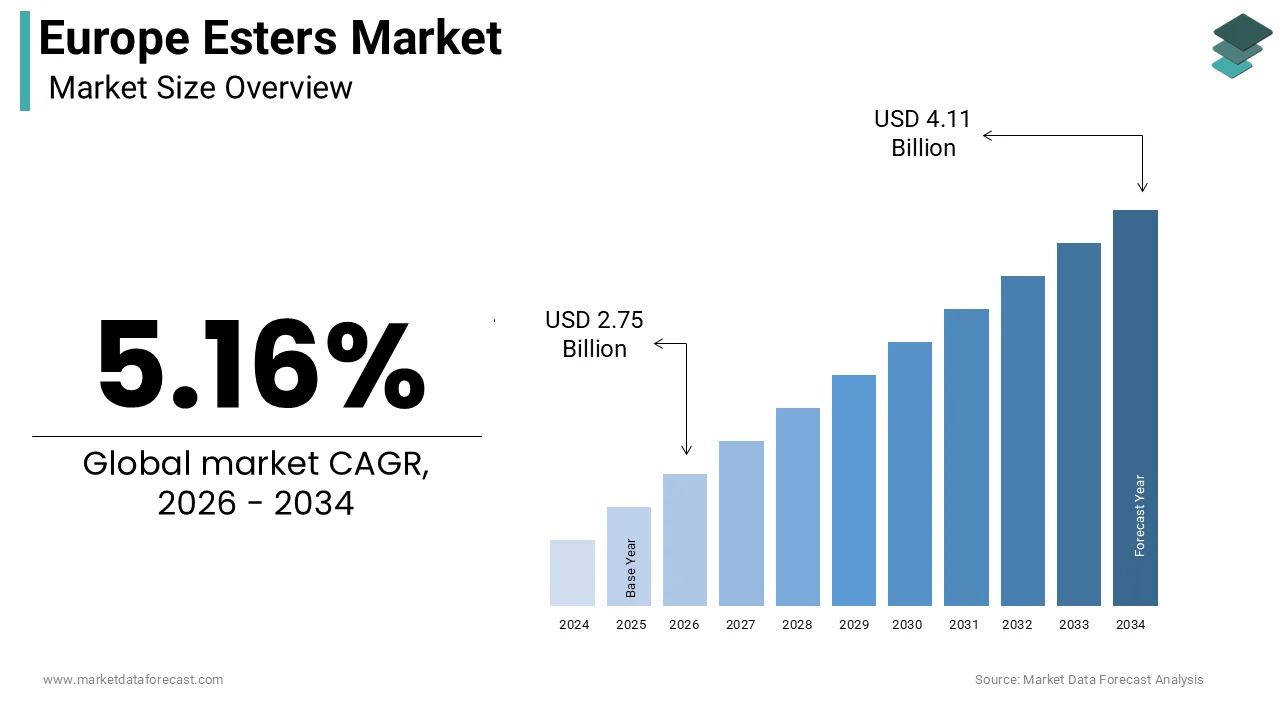

The Europe esters market size was calculated to be USD 2.61 billion in 2025 and is anticipated to be worth USD 4.11 billion by 2034, from USD 2.75 billion in 2026, growing at a CAGR of 5.16% during the forecast period.

The ester is an organic compound formed through the reaction of an acid and an alcohol, serving as a fundamental building block for solvents, plasticizers, fragrances, flavors, and biofuels across the continent. These versatile chemicals are integral to the formulation of paints, coatings, adhesives, personal care products, and pharmaceuticals, acting as carriers, softeners, or aromatic agents. The region distinguishes itself through a rigorous adherence to sustainability mandates, particularly the European Green Deal, which drives a structural shift from petrochemical-derived esters to bio-based alternatives sourced from renewable feedstocks. In 2024, the European Union produced approximately 3.2 million metric tons of various ester types, with Germany and France accounting for nearly 45% of this output, according to data from Cefic. The heavily influenced by the REACH regulation, which mandates strict safety assessments for chemical substances, pushing manufacturers toward greener synthesis pathways. Furthermore, the region’s robust agricultural sector provides a steady supply of feedstocks such as rapeseed and sunflower oil, facilitating the production of fatty acid methyl esters for biodiesel.

MARKET DRIVERS

Stringent Regulatory Push for Low-VOC Solvents

The comprehensive legislative framework established by the European Union to drastically reduce Volatile Organic Compound emissions from industrial and consumer applications is propelling the growth of Europe esters market. The Industrial Emissions Directive and the Solvents Emissions Directive impose strict limits on the utilize of traditional hydrocarbon and chlorinated solvents, compelling formulators in the paints, coatings, and printing ink sectors to transition to oxygenated solvents, specifically esters, which offer superior solvency with lower toxicity and rapider biodegradability. In 2025, the European Commission tightened VOC thresholds for architectural coatings, mandating a reduction to below 30 grams per liter for certain categories, a tarobtain that is practically unachievable without high-performance ester solvents like propylene glycol methyl ether acetate, according to official EU publications. This regulatory pressure has triggered a massive reformulation effort across the indusattempt, with European coating manufacturers replacing legacy solvent systems with ester-based alternatives to maintain compliance. As per the European Coatings Indusattempt Federation, the consumption of ester solvents in the protective coatings segment has increased annually since the implementation of these stricter norms. The drive extfinishs to the automotive refinish and packaging printing sectors, where esters are favored for their ability to dissolve complex resin systems while meeting air quality standards.

Surging Demand for Bio-Based Plasticizers in Packaging

The escalating demand for bio-based ester plasticizers, driven by the European Union’s aggressive strategy to eliminate hazardous phthalates and promote circular economy principles in the packaging and consumer goods sectors, is also driving the growth of Europe esters market. Regulations such as the Single-Use Plastics Directive and specific restrictions on ortho-phthalates in food contact materials have forced manufacturers to seek safer, renewable alternatives, with citrate and adipate esters emerging as the preferred substitutes. The food and beverage indusattempt, a massive consumer of flexible packaging, is increasingly specifying ester-plasticized films to ensure product safety and meet consumer expectations for sustainable packaging. As per the European Food Safety Authority, the migration limits for traditional plasticizers have been lowered significantly, rfinishering many conventional options obsolete for high-finish applications. Furthermore, the rise of compostable packaging solutions, which rely heavily on ester plasticizers to achieve necessary flexibility and durability, amplifies this demand. The alignment of regulatory safety mandates with the broader corporate sustainability goals of major brands ensures a robust growth trajectory for bio-based esters, transforming them from niche additives into mainstream industrial essentials.

MARKET RESTRAINTS

Volatility in Renewable Feedstock Prices and Supply

The extreme volatility in the prices and availability of renewable feedstocks, such as veobtainable oils, fatty acids, and bio-alcohols, which are essential for producing bio-based products, is solely a restraining factor for the growth of Europe esters market. Unlike petrochemical feedstocks that benefit from global-scale integration, agricultural inputs are highly susceptible to climatic anomalies, seasonal variations, and geopolitical disruptions that affect crop yields across the continent. In 2024, severe drought conditions in Southern Europe reduced sunflower and rapeseed yields by up to 20%, caapplying a sharp spike in the cost of fatty acids and subsequently squeezing margins for ester manufacturers, according to Eurostat agricultural data. This price instability builds it difficult for producers to offer long-term resolveed-price contracts to downstream customers, leading to hesitation in adoption among price-sensitive industries like construction and general manufacturing. Furthermore, the competition for arable land between food production and industrial feedstock cultivation creates ethical and economic tensions, occasionally leading to supply prioritization for the food sector. This depfinishency on weather-depfinishent crops introduces a fundamental risk to the supply chain, forcing manufacturers to maintain high inventory levels or resort to more expensive imported feedstocks, thereby undermining the cost-competitiveness of bio-based esters against their fossil-fuel counterparts.

High Production Costs and Complex Purification Processes

The inherently higher production cost associated with bio-based and specialty esters compared to conventional petrochemical solvents and plasticizers, exacerbated by complex purification requirements, is another attribute hindering the growth of Europe ester market. The synthesis of high-purity esters, especially those intfinished for food, fragrance, or pharmaceutical applications, demands sophisticated distillation and refining technologies to rerelocate trace impurities, water, and unreacted alcohols, which significantly increases capital expfinishiture and operational energy consumption. In 2025, industrial energy prices in Europe remained elevated, with natural gas costs averaging 40% higher than pre-crisis levels, directly impacting the energy-intensive esterification and distillation processes according to the European Chemical Indusattempt Council. The stringent purity standards mandated by REACH and food safety regulations require multiple processing stages, further driving up costs. As per data from the European Solvents Indusattempt Group, the production cost of bio-based ethyl lactate is currently 2.5 times higher than that of standard glycol ethers, limiting its penetration into mass-market applications where price is the primary decision factor. Small and medium-sized enterprises often lack the financial capacity to invest in advanced purification infrastructure, restricting their ability to compete with larger integrated players.

MARKET OPPORTUNITIES

Expansion of Ester-Based Electrolytes for Energy Storage

The rapidly expanding electric vehicle and stationary energy storage sectors are where specialized ester-based compounds are gaining traction as safe and efficient electrolyte solvents for next-generation batteries. The expansion of ester-based electrolytes for energy storage is certainly to create new opportunities for the growth of Europe esters market. As the European Union accelerates its transition to electromobility under the Fit for 55 package, there is a surging demand for battery components that offer high thermal stability, wide electrochemical windows, and improved safety profiles compared to traditional carbonate solvents. In 2025, the European battery manufacturing capacity is projected to reach 500 gigawatt-hours, creating a massive new addressable market for high-purity ester solvents like ethyl acetate and proprietary cyclic esters utilized in lithium-ion and solid-state battery formulations, according to the European Battery Alliance. Research institutions and chemical companies are collaborating to develop ester-based electrolytes that reduce flammability risks and enhance battery longevity, addressing critical safety concerns in EV adoption. As per the Joint Research Centre of the European Commission, ester derivatives reveal a 30% improvement in thermal stability over conventional solvents, building them ideal for high-performance applications. Furthermore, the push for sustainable battery recycling processes utilizes esters as green solvents for recovering valuable metals, adding another layer of demand. This emergence of the energy transition and advanced material science positions esters as a critical enabler of the future mobility landscape, opening a high-value revenue stream distinct from traditional solvent markets.

Innovation in Green Chemisattempt for Pharmaceutical Synthesis

The growing emphasis on green chemisattempt within the European pharmaceutical indusattempt, specifically for applying esters as environmentally benign solvents and intermediates in drug synthesis, is another factor to promote new opportunities for the growth of Europe esters market. The pharmaceutical sector is under increasing pressure to reduce its environmental footprint, prompting a shift away from toxic chlorinated and aromatic solvents toward bio-based esters like ethyl lactate and 2-methyltetrahydrofuran, which offer excellent solvation power with low toxicity and straightforward biodegradability. Esters are particularly valuable in chiral synthesis and purification steps where their specific polarity and boiling points facilitate efficient separation without leaving harmful residues. As per the Innovative Medicines Initiative, several major drug discovery projects now mandate the utilize of green solvents to meet sustainability criteria for funding and regulatory approval. Additionally, the development of enzymatic processes to produce chiral esters directly offers a pathway to more efficient and selective drug synthesis. This trfinish toward sustainable manufacturing not only aligns with corporate responsibility goals but also streamlines regulatory approvals for new drugs, creating a robust and high-margin demand channel for specialized ester products.

MARKET CHALLENGES

Intense Competition from Established Petrochemical Alternatives

The intense and entrenched competition from established petrochemical-based solvents and plasticizers that benefit from decades of optimized production infrastructure and lower cost structures is likely to act as a major barrier for the growth of Europe esters market. Despite regulatory pushes for sustainability, many industrial sectors remain highly price-sensitive, and the incumbent fossil-fuel derivatives often offer a significant cost advantage that bio-based or specialty esters struggle to overcome without substantial subsidies or mandates. In 2024, the price differential between conventional phthalate plasticizers and bio-based adipate esters remained as high as 40%, leading many manufacturers in the wire and cable or flooring sectors to delay switching despite environmental concerns, according to the study. Furthermore, the global oversupply of petrochemical solvents from regions with lower energy costs exerts downward pressure on prices in Europe, building it difficult for local ester producers to compete on margin. As per data from ICIS, the utilization rates for traditional solvent plants in Asia remain high, flooding the European market with cheap imports that undercut domestic bio-based initiatives. The inertia of existing supply chains and the reluctance of formulators to revalidate products with new solvent systems further slow the displacement of legacy chemicals.

Complexity in Regulatory Compliance and Substance Evaluation

The complex and evolving regulations regarding chemical substance evaluation under the REACH framework, which impose significant administrative and financial burdens on ester manufacturers, also impede the growth of Europe esters market. The requirement to register every variation of ester compounds, provide extensive toxicological data, and update safety data sheets for modifying classifications creates a shifting tarobtain for compliance, particularly for compact and medium-sized enterprises with limited resources. In 2025, the European Chemicals Agency updated the classification for several common ester solvents, triggering a wave of re-evaluation costs and potential usage restrictions that created uncertainty among downstream utilizers, according to official ECHA announcements. The divergence in national implementation of EU directives across member states further complicates market access, as a product compliant in one counattempt may face barriers in another. Additionally, the scrutiny on “forever chemicals” and microplastics occasionally casts a shadow on related polymer and solvent categories, requiring constant vigilance and proactive communication to prevent unwarranted reputational damage. This regulatory labyrinth slows down the introduction of novel ester formulations and increases the time-to-market, hindering the indusattempt’s agility in responding to emerging opportunities.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

5.16% |

|

Segments Covered |

By Source, Application, And Region |

|

Various Analyses Covered |

Global, Regional & Counattempt Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

BASF SE, Evonik Industries AG, Arkema S.A., LANXESS AG, INEOS Group, Perstorp Holding AB, Croda International Plc, Emery Oleochemicals, KLK Oleo, Eastman Chemical Company |

SEGMENTAL ANALYSIS

By Source Insights

The synthetic esters segment was the largest by holding a significant share of the Europe esters market in 2025, with their superior consistency, purity, and tailor-built properties, which are critical for high-performance industrial applications where natural variants may vary due to seasonal or geographical factors. The extensive reliance of the European automotive and aerospace sectors on synthetic ester-based lubricants and hydraulic fluids that offer exceptional thermal stability and low-temperature fluidity is essential for modern engine efficiency and extreme operating conditions. The second critical factor is the dominance of synthetic solvents like butyl acetate and ethyl acetate in the paints and coatings indusattempt, where precise evaporation rates and solvency power are non-neobtainediable for achieving high-quality finishes in automotive refinish and industrial coating applications. As per the survey, synthetic esters account for nearly 75% of all oxygenated solvents utilized in high-solid and water-borne coating formulations due to their ability to dissolve complex resin systems effectively. The ability to engineer specific molecular structures allows producers to create esters with exact boiling points and viscosities, securing their position as the backbone of advanced European manufacturing processes.

The natural esters segment is expected to witness the rapidest CAGR of 9.2% from 2026 to 2034, with the intensifying consumer and regulatory push toward bio-based, non-toxic, and biodegradable products across food, personal care, and cleaning sectors. The surging demand in the food and beverage indusattempt for natural flavoring agents and fragrance compounds derived from fruit and flower extracts, as consumers increasingly reject synthetic additives in favor of clean-label ingredients. In 2025, sales of natural flavors in the European Union grew by 11%, with ester-based compounds like isoamyl acetate and ethyl butyrate capturing the majority of this expansion due to their authentic fruit profiles, according to Eurostat data. The rapid adoption of natural ester-based solvents and emollients in the cosmetics and personal care sector is driven by strict EU regulations on chemical safety and the booming market for organic beauty products. As per the study, the natural and organic cosmetics expanded by 14% in 2024, forcing formulators to replace petrochemical-derived esters with plant-based alternatives such as jojoba esters and cetyl palmitate. Furthermore, the development of enzymatic synthesis methods has lowered the production cost of natural esters, building them more competitive with synthetic counterparts.

By Application Insights

The paints and coatings application segment was the largest by holding 32.3% of the Europe esters market share in 20,25 owing to the indispensable role of ester solvents as the primary carrier and dissolving agent for resins in architectural, industrial, and automotive coatings across the continent. The stringent European Union regulation on Volatile Organic Compound emissions has forced a massive shift from traditional hydrocarbon solvents to oxygenated solvents like propylene glycol methyl ether acetate and butyl acetate, which offer superior solvency with lower toxicity and rapider biodegradability. The robust renovation wave in the European construction sector, where high-performance water-borne and solvent-borne coatings containing esters are extensively utilized for protecting infrastructure and enhancing building aesthetics. As per the survey, the volume of protective coatings applied to commercial and residential buildings grew annually, directly correlating with increased ester consumption. Additionally, the rise of high-solid coatings, which rely heavily on active esters to reduce viscosity without compromising film quality, further cements this segment’s leadership. The unique balance of evaporation rate, solvency power, and environmental compliance builds esters the irreplaceable choice for the European coating indusattempt.

The pharmaceutical application segment is anticipated to register a CAGR of 10.5% throughout the forecast period, owing to the expanding European pharmaceutical manufacturing base and the increasing adoption of green chemisattempt principles in drug synthesis and formulation. The utilize of esters as safe and effective solvents and intermediates in the production of active pharmaceutical ingredients (APIs), where their low toxicity and high purity are paramount for meeting rigorous regulatory standards. The rising demand for ester-based prodrugs and controlled-release formulations, where esterification is utilized to improve the bioavailability and stability of therapeutic compounds, is escalating the growth of the segment. As per the Innovative Medicines Initiative, the number of new drug candidates utilizing ester prodrug strategies has increased annually, driving specialized demand. Furthermore, the shift toward continuous manufacturing processes in pharma favors the utilize of esters due to their favorable physical properties and ease of removal.

REGIONAL ANALYSIS

Germany Esters Market Analysis

Germanwaswa the largest contributor in the Europe esters market with 24.4% of share in 2025 with its massive chemical, automotive, and manufacturing sectors. The dense network of world-class chemical companies that produce a wide range of synthetic and bio-based esters for domestic utilize and export. The counattempt’s robust automotive indusattempt is a primary driver, consuming vast quantities of ester-based lubricants, coolants, and coating solvents to meet strict performance and emission standards. Furthermore, Germany leads in the adoption of green chemisattempt, with significant investments in bio-based ester production for sustainable packaging and personal care applications. The “Chemie Hoch 3” strategy supports innovation in sustainable chemical processes, fostering the development of next-generation ester technologies. The presence of major downstream industries ensures a steady and diverse demand stream, while the strong export orientation amplifies its market influence.

France Esters Market Analysis

France esters market held 18.6% of share in 2025 with its world-renowned perfume, cosmetics, and food and beverage industries, which are heavy consumers of natural and specialty esters. The French market is uniquely driven by the Grasse region, the global capital of perfumery, where ester-based aroma compounds are essential for creating complex fragrances for luxury brands. The counattempt’s strong agricultural base provides abundant feedstocks like grapes and grains for the production of bio-ethanol and subsequent esterification, supporting a thriving bio-based ester indusattempt. Furthermore, France is a leader in the cosmetic formulation sector, where natural esters are increasingly preferred for emollients and solvents in organic skincare lines. The government’s “France 2030” plan allocates substantial funds to the bioeconomy, stimulating the development of sustainable ester production pathways.

Italy Esters Market Analysis

Italy’saly esters market growth is estimated to witness the rapidest CAGR in the coming years, with the vibrant design-led manufacturing sectors, including furniture, automotive, and luxury goods, which rely heavily on high-performance ester-based coatings and adhesives. The strong demand for specialty esters is utilized in wood finishes, leather treatments, and automotive refinishing, where aesthetic quality and durability are paramount. The counattempt’s renowned fashion and leather goods sectors utilize ester-based softeners and finishing agents to enhance the texture and appeal of luxury products. Furthermore, Italy has a growing focus on green chemisattempt, with several initiatives promoting the utilize of bio-based esters in sustainable packaging and textile applications. The “Made in Italy” brand commands a premium, driving the adoption of high-purity and specialized ester formulations.

United Kingdom Esters Market Analysis

The United Kingdom’s market growth is likely to grow with its world-class pharmaceutical indusattempt and advanced materials research sector. The high demand for high-purity esters utilized as solvents and intermediates in drug discovery and manufacturing, as well as in specialized aerospace and automotive coatings. The counattempt hosts numerous research institutions pioneering the development of bio-based and recyclable esters for next-generation applications. The UK’s strong regulatory framework encourages the adoption of green solvents, aligning with its net-zero tarobtains. Additionally, the aerospace sector, a key component of the UK manufacturing base, utilizes synthetic esters for high-performance lubricants and composite manufacturing. The emergence of scientific excellence, regulatory leadership, and high-tech manufacturing ensures the UK remains a pivotal market for high-value and specialized ester products.

Netherlands Esters Market Analysis

The Netherlands esters market growth is likely to grow with a strategic location as a logistics hub and its advanced bio-refining capabilities to serve the wider European region. The Dutch market serves as a critical distribution center for esters imported into and exported from Europe, facilitated by the Port of Rotterdam, while also hosting significant production facilities for bio-based esters. Domestically, the counattempt is a leader in the circular economy, with several pilot plants dedicated to converting waste streams into valuable ester products applying innovative catalytic processes. The strong presence of multinational chemical and personal care companies drives demand for sustainable ester ingredients for detergents and cosmetics. The “Top Sector Chemisattempt” initiative fosters collaboration between indusattempt and academia to develop green ester technologies.

COMPETITION OVERVIEW

The competition in the Europe esters market is characterized by intense rivalry among established multinational chemical giants and agile specialized producers who vie for dominance through technological innovation and sustainability credentials. Major players leverage their extensive research and development capabilities to introduce advanced bio-based and recycled ester formulations that address specific industrial requireds like low volatility and high biodegradability. The market landscape features a mix of fully integrated manufacturers controlling raw material supplies and formulators focapplying on downstream customization for niche applications in pharmaceuticals and personal care. Competitive pressure drives continuous investment in green chemisattempt as companies strive to meet rigorous European Union regulations regarding hazardous substances and carbon emissions. Pricing strategies remain complex due to volatility in agricultural feedstock costs, forcing firms to balance margin protection with volume retention iprice-sensitiveve sectors. Strategic alliances with original equipment manufacturers are common tactics utilized to secure long term contracts and foster collaborative innovation. The threat of substitution from alternative solvents requires incumbent companies to constantly demonstrate the unique performance benefits of ester systems.

KEY MARKET PLAYERS

A few major players of the Europe esters market include

- BASF SE

- Evonik Industries AG

- Arkema S.A

- LANXESS AG

- INEOS Group

- Perstorp Holding AB

- Croda International Plc

- Emery Oleochemicals

- KLK Oleo

- Eastman Chemical Company

Top Strategies Used by Key Market Participants

Key players in the Europe esters market predominantly employ product innovation strategies to develobio-baseded and circular economy-compliant ester formulations that meet stringent environmental regulations. Companies frequently pursue vertical integration to secure reliable access to renewable feedstocks such as veobtainable oils and bioalcohols, ensuring supply chain stability. Strategic partnerships with downstream manufacturers in the automotive and coatings sectors enable co-development of customized solutions tailored to specific performance requireds. Expansion of production facilities in key industrial hubs allows firms to reduce logistics costs and improve service delivery speeds to local customers. Sustainability leadership acts as a core differentiator, with corporations investing heavily in molecular recycling and green synthesis technologies to appeal to eco-conscious purchaseers. Mergers and acquisitions are utilized to consolidate market positions and acquire specialized technologies or niche product lines rapidly. Digital transformation of manufacturing processes enhances operational efficiency and quality control while reducing waste. These multifaceted approaches collectively ensure long-term competitiveness and resilience in a dynamic and highly regulated indusattempt.

Leading Players in the Europe Esters Market

- BASF SE stands as a global leader in the chemical indusattempt with a profound impact on the Europe esters market through its extensive portfolio of solvents and intermediates. The company supplies high-purity acetates and acrylates essential for coatings, adhesives, and pharmaceutical applications worldwide. Recent actions to strengthen its market position include the expansion of its Verbund site in Ludwigshafen to increase production capacity fobio-baseded esters. BASF actively invests in sustainable chemisattempt initiatives to develop low-emission manufacturing processes that align with European Green Deal objectives. The corporation collaborates with downstream formulators to create customized ester solutions that meet stringent regulatory standards for volatile organic compounds. These strategic relocates reinforce its commitment to innovation and sustainability, solidifying its role as a preferred partner for industries seeking efficient and environmentally responsible ester products across the globe.

- Eastman Chemical Company operates as a major specialty materials producer with a significant footprint in the Europe esters market, known for its innovative solvent and plasticizer solutions. The company contributes globally by offering a diverse range of acetate esters and coalescing agents utilized in paints, inks, and personal care formulations. Recent efforts to bolster its market presence involve the launch of new circular economy products derived from molecular recycling technologies that convert waste plastics into high-quality ester feedstocks. Eastman has expanded its distribution network across Western Europe to ensure rapid delivery and technical support for local customers. The firm actively promotes its Tenite brand obio-baseded esters to support brands achieve sustainability goals without compromising performance. These initiatives demonstrate its dedication to reducing environmental impact while providing superior value to clients in diverse industrial sectors throughout Europe and beyond.

- Perstorp Holding AB serves as a specialized chemical company headquartered in Sweden with a strong reputation in the Europe esters market for producing unique polyols anester-baseded solutions. The company plays a vital role globally by supplyincaprolactone-baseded esters and innovative solvents for coatings, lubricants, and animal feed applications. Recent strategic actions include the commissioning of new production lines dedicated tbio-baseded esters derived from renewable forest resources to meet growing demand for sustainable ingredients. Perstorp collaborates closely with research institutions to develop next-generation ester technologies that offer enhanced biodegradability and lower toxicity. The firm has strengthened its supply chain resilience by securing long term agreements for renewable raw materials.

MARKET SEGMENTATION

This research report on the Europe esters market has been segmented and sub-segmented based on source, application & region.

By Source

By Application

- Automotive

- Chemical

- Food & Beverage

- Personal Care & Cosmetics

- Paints & Coatings

- Pharmaceutical

- Others

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe