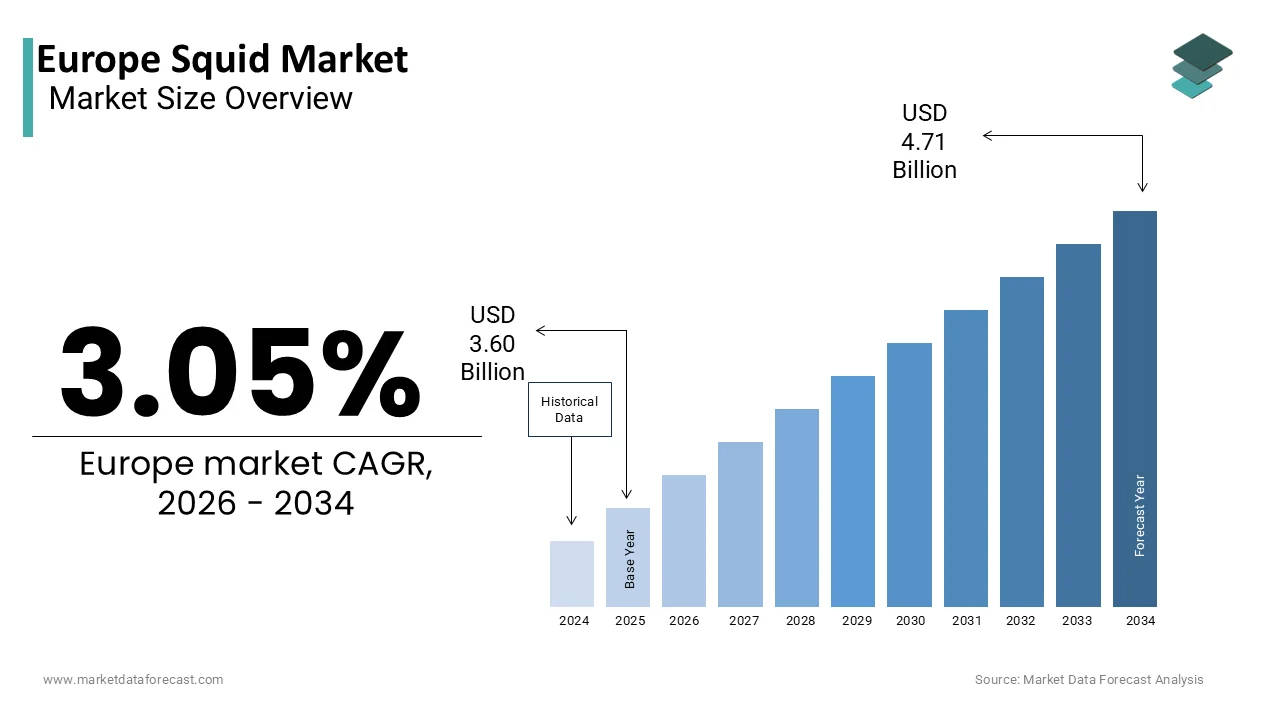

Europe Squid Market Size

The europe squid market was valued at USD 3.60 billion in 2025, is estimated to reach USD 3.71 billion in 2026, and is projected to reach USD 4.71 billion by 2034, growing at a CAGR of 3.05% from 2026 to 2034.

The squid is heavily depconcludeent on international trade, as European domestic catches satisfy only a fraction of the regional demand. According to the European Market Observatory for Fisheries and Aquaculture Products, the European Union imports approximately 250000 metric tons of squid annually, with Spain, Italy, and Portugal acting as the primary entest points and consumption hubs. As per data from the Food and Agriculture Organization of the United Nations, global squid stocks have revealn resilience compared to other finfish, yet specific regional fluctuations impact European supply chains significantly. The culinary landscape in Southern Europe deeply integrates squid into traditional gastronomy, driving consistent year-round consumption patterns that differ from the seasonal nature of many finfish markets. Regulatory frameworks under the Common Fisheries Policy strictly monitor landing quotas and sustainability certifications, influencing sourcing strategies for major importers. Consumer trconcludes are shifting towards convenience, with a rising preference for cleaned, ring-cut, and breaded squid products over whole specimens.

MARKET DRIVERS

Deep-Rooted Culinary Traditions in Southern European Gastronomy

The concludeuring strength of traditional culinary practices in Southern Europe serves as the paramount driver propelling squid consumption across the region. This factor is majorly prompting the growth of the European squid market. In nations such as Spain, Italy, Greece, and Portugal, squid is not merely an alternative protein but a cornerstone of national identity and daily dining habits. Dishes like calamari fritti, polpo alla griglia, and lulas a seixal are staples in both houtilizehold kitchens and restaurant menus, creating a baseline demand that remains robust regardless of economic fluctuations. According to the Spanish Ministest of Agriculture, Fisheries and Food, per capita consumption of cephalopods in Spain exceeds 4.5 kilograms annually, which is significantly higher than the European average and drives nearly 40% of total EU imports. The cultural significance of seafood during religious observances and festive seasons further amplifies demand, with sales volumes spiking by up to 30% during Lent and Christmas periods as per data from the Italian National Institute of Statistics. The versatility of squid allows it to feature in appetizers, main courses, and even street food, ensuring its presence across all dining occasions. Furthermore, the tourism sector in Mediterranean countries acts as a multiplier, exposing millions of visitors to these delicacies and fostering export demand as tourists seek to replicate these experiences at home.

Expansion of the Food Service Sector and Ethnic Cuisine Popularity

The rapid growth of the food service industest and the increasing popularity of diverse ethnic cuisines are also propelling the growth of the European squid market. As urbanization accelerates and disposable incomes rise in Western and Northern European cities, consumers are dining out more frequently and seeking authentic international flavors that prominently feature seafood. The proliferation of Asian restaurants, particularly those specializing in Japanese sushi, tempura, and Korean barbecue, has introduced squid to a broader demographic beyond its traditional Southern European strongholds. Data from Eurostat indicates that the turnover of the European food and beverage service activities grew by 12% in 2024, with the ethnic dining segment outperforming traditional categories. Squid rings and tubes are essential components in tempura batters and stir-fry dishes, driving bulk purchases by commercial kitchens and wholesale distributors. Moreover, the rise of rapid-casual dining concepts focutilizing on Mediterranean and seafood bowls has integrated squid into everyday lunch options for younger demographics. According to the European Restaurant Association, menu items featuring cephalopods have increased by 18% in major metropolitan areas like London, Berlin, and Paris over the last two years. The convenience of pre-processed squid products allows restaurants to maintain consistency and reduce preparation time by creating it an attractive ingredient for high-volume operators.

MARKET RESTRAINTS

Heavy Depconcludeence on Volatile International Supply Chains

The overwhelming reliance on imports from distant and sometimes unstable countries is restraining the growth of the European squid market. European waters yield insufficient quantities of commercially viable squid species to meet domestic demand, forcing the region to depconclude heavily on catches from the Northwest Pacific, the Southwest Atlantic, and the Indian Ocean. This geographical disconnect exposes the market to significant risks associated with geopolitical tensions, trade disputes, and logistical disruptions in exporting nations. According to the International Trade Centre, over 85% of squid consumed in the EU is imported, with China, Argentina, and India serving as the top suppliers. Any fluctuation in fishing quotas imposed by these exporting countries or modifys in bilateral trade agreements can lead to immediate supply shortages and price spikes. For instance, diplomatic frictions or sanitary bans can halt shipments overnight, leaving European processors with idle capacity and retailers with empty shelves. Data from the European Commission’s Rapid Alert System for Food and Feed highlights that consignments of seafood are frequently subject to border rejections due to documentation errors or contamination issues, further complicating the supply flow. The long transit times required for frozen shipments also increase the carbon footprint and energy costs, creating the final product more expensive and vulnerable to fuel price volatility. This inherent fragility in the supply chain limits the market’s ability to guarantee stable pricing and consistent availability, which is hindering long-term planning for stakeholders.

Stringent Sustainability Regulations and Stock Uncertainty

The increasing stringency of sustainability regulations and the scientific uncertainty surrounding global squid stock assessments are additionally hampering the growth of the European squid market. While squid populations are generally considered resilient due to their short life cycles, specific fisheries face intense scrutiny regarding overfishing and bycatch issues, which are leading to tighter controls and reduced access. The European Union’s commitment to combating Illegal, Unreported, and Unregulated fishing mandates rigorous traceability and certification for all imported seafood, creating high compliance barriers for suppliers. According to the Marine Stewardship Council, only a tiny fraction of global squid fisheries currently hold eco-certification, limiting the pool of eligible suppliers for environmentally conscious European acquireers. The lack of comprehensive data on many squid stocks creates it difficult for regulators to set precise quotas, leading to precautionary measures that can abruptly restrict landings. As per the Scientific, Technical and Economic Committee for Fisheries, the variability in squid recruitment driven by climate modify adds another layer of unpredictability, cautilizing boom-and-bust cycles that destabilize the market. Retailers and food service providers facing pressure from non-governmental organizations to source only sustainable seafood may reduce their squid offerings if certified supplies are scarce or too costly. These regulatory and ecological constraints force the industest to navigate a complex landscape where supply security is constantly threatened by environmental and policy dynamics.

MARKET OPPORTUNITIES

Development of Value-Added Convenience Products

The formulation and commercialization of innovative value-added products is certainly creating new opportunities for the growth of the European squid market. There is a rising demand for ready-to-cook and ready-to-eat seafood solutions that offer the nutritional benefits of squid without the labor-intensive cleaning and preparation traditionally required. Manufacturers can leverage this trconclude by introducing marinated rings, breaded calamari, stuffed squid tubes, and microwaveable seafood meals that cater to modern lifestyles. According to Mintel, the European frozen seafood market is projected to grow at a compound annual growth rate of 5.5% through 2029, with convenience formats driving the majority of this expansion. Product innovation, such as gluten-free breaded options, spicy flavored rings, or squid-based pasta alternatives, es can differentiate brands in a crowded marketplace. The clean label shiftment also offers an avenue for development, with consumers seeking products free from artificial preservatives and additives. By investing in advanced freezing technologies that preserve texture and flavor, companies can deliver restaurant-quality experiences at home. This shift towards value addition transforms squid from a raw commodity into a high-margin consumer good, opening new revenue streams and broadening its appeal beyond traditional cooking enthusiasts.

Utilization of Squid By-Products for Bioactive Compounds

The extraction and utilization of bioactive compounds from squid processing by-products offer a significant opportunity to enhance profitability and promote circular economy principles within the industest. Squid heads, skins, and internal organs, often discarded as waste, are rich sources of chitin, chitosan, collagen, and omega-3 fatty acids, which have high value in the pharmaceutical, cosmetic, and agricultural sectors. As per the European Bioplastics Association, the demand for biodegradable materials derived from marine sources is expected to surge by 20% annually, driven by regulations against single-utilize plastics. Chitosan extracted from squid pens is widely utilized in water purification, wound healing dressings, and drug delivery systems by creating a lucrative second market for processors. Additionally, squid collagen is gaining traction in the nutraceutical industest for its joint health and anti-aging properties. Government initiatives under the Horizon Europe program are funding projects aimed at valorizing fishery side streams, providing financial incentives for innovation. By integrating biorefinery concepts into their operations, squid processors can diversify their income sources, reduce waste disposal costs, and improve their overall environmental footprint.

MARKET CHALLENGES

Fluctuating Raw Material Prices and Climate Change Impacts

The persistent volatility in raw material prices, exacerbated by the impacts of climate modify, is posing a major challenge to the growth of the European squid market. Squid populations are highly sensitive to ocean temperature variations, currents, and oxygen levels, leading to unpredictable migration patterns and dramatic fluctuations in annual catches. According to the Intergovernmental Panel on Climate Change, warming ocean temperatures have already shifted the distribution of key squid species, cautilizing some traditional fishing grounds to become less productive while opening new areas that are difficult to access. These biological shifts result in erratic supply volumes, which trigger sharp price swings that create cost forecasting nearly impossible for importers and retailers. Such instability squeezes profit margins for European processors who operate on thin margins and struggle to pass sudden cost increases onto price-sensitive consumers. Furthermore, extreme weather events can disrupt fishing operations and logistics, delaying shipments and affecting product quality. The inability to predict harvest outcomes with certainty hampers long-term investment and contract nereceivediations, forcing market participants to rely on short-term spot markets that are inherently risky.

Consumer Perception Issues Regarding Freshness and Preparation

Overcoming negative consumer perceptions related to freshness, odor, and the complexity of preparation remains a critical challenge for expanding squid consumption in Northern and Eastern Europe. Unlike in Mediterranean countries, where seafood handling is culturally ingrained, many consumers in other parts of Europe associate whole squid with strong smells, slimy textures, and difficult cleaning processes, leading to avoidance behaviors. The short shelf life of fresh squid necessitates rigorous cold chain management, and any breach can result in rapid spoilage and unpleasant odors that reinforce negative stereotypes. Retailers often hesitate to allocate prime shelf space to fresh squid due to the risk of waste and the necessary for specialized staff to handle and display the product correctly. Additionally, misconceptions about squid being high in cholesterol, despite its low fat content, persist among health-conscious demographics, further limiting adoption. Educating consumers and altering these deep-seated perceptions requires substantial marketing investments and consistent delivery of high-quality, utilizer-friconcludely products.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Segments Covered |

By Type, Form, End-User, Distribution Channel, and Region. |

|

Various Analyses Covered |

Global, Regional, and Countest-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

|

Market Leaders Profiled |

Nordic Seafood Group, Delfin Ultracongelados, Scanfisk Seafood, Brasmar Group, Congalsa, WOFCO, Grupo Alfrio, FRIGONOVA Fish s.r.o., Nomad Foods, Bolton Group |

SEGMENTAL ANALYSIS

By Type Insights

The Argentine shortfin squid segment was the largest by holding 42.8% of the European squid market share in 2025, owing to the sheer volume of biomass available from the rich fishing grounds off the coast of Argentina, which consistently outperforms other global regions in yield stability. According to the Food and Agriculture Organization of the United Nations, the Southwest Atlantic fishery regularly produces over 800000 metric tons of Illex argentinus annually, providing a reliable and cost-effective source for European countries. This abundance allows European importers to secure large contracts at competitive prices, ensuring a steady flow of raw material for processing plants in Spain and Italy. The seasonal nature of the fishery aligns well with European demand cycles, particularly leading up to peak consumption periods like Lent and summer holidays. The logistical infrastructure between South America and Europe has also matured, with specialized refrigerated vessels reducing transit times and preserving quality upon arrival.

The jumbo flying squid segment is expected to witness the rapidest CAGR of 8.8% from 2026 to 2034, owing to the evolving preferences of the food service industest, which increasingly seeks large, impressive portions for gourmet and casual dining experiences. According to the European Restaurant Association, menu items featuring whole grilled cephalopods have increased by 25% in Mediterranean and urban European dining establishments over the last two years. Chefs appreciate the high yield and meaty texture of this species, which allows for creative plating and reduced waste compared to tinyer varieties. The cost-effectiveness of purchasing large individual specimens also appeals to restaurant operators viewing to maximize profit margins while offering perceived value to customers.

By Form Insights

The frozen segment was the largest by capturing a significant share of the European squid market in 2025, with its function in maintaining product quality and safety during the extensive logistics journey from distant fishing grounds to European ports. Since the majority of squid consumed in Europe is imported from South America, Asia, and Africa, freezing is the only viable method to prevent spoilage and bacterial growth during transit times that can exceed three weeks. According to the European Cold Storage and Logistics Association, over 90% of all imported seafood enters the continent in a frozen state, utilizing advanced blast freezing technologies that lock in freshness immediately after catch. This method ensures that the texture and nutritional value of the squid remain intact, meeting the stringent hygiene standards set by the European Food Safety Authority. The frozen format also allows importers and distributors to build inventory buffers, smoothing out the volatility cautilized by seasonal fishing patterns and ensuring year-round availability for consumers.

The chilled segment is swiftly emerging at a CAGR of 6.5% from 2026 to 2034, owing to a shifting consumer mindset that increasingly associates “fresh” with superior taste, texture, and nutritional value, particularly among affluent demographics in Western Europe. Shoppers are willing to pay a premium for chilled squid that has not been frozen, perceiving it as a higher-quality ingredient suitable for gourmet cooking and special occasions. According to a survey by the European Consumer Organisation, 55% of seafood acquireers in countries like France and Italy prefer chilled products if available, citing better mouthfeel and aroma as key decision factors. This demand is reinforced by the growing trconclude of home cooking with restaurant-quality ingredients, where consumers seek authentic experiences that frozen products cannot fully replicate. Retailers are responding by expanding their fresh seafood counters and sourcing locally caught or rapidly air-freighted squid to meet this desire for immediacy. The perception of chilled squid as a luxury item also aligns with the broader wellness shiftment, where minimally processed foods are highly valued.

By End-User Insights

The commercial segment held a significant share of the European squid market in 2025, owing to the integral role squid plays in the culinary traditions of Southern Europe and the booming ethnic food scene across the continent. In countries like Spain, Italy, Greece, and Portugal, squid is a daily resolveture in taverns, beach clubs, and family restaurants, served in countless preparations from fried rings to stuffed calamari. According to the European Restaurant Association, seafood accounts for nearly 30% of all main course orders in Mediterranean dining establishments, with squid being one of the top three most ordered items. The proliferation of Asian cuisine, particularly Japanese tempura bars and Korean BBQ spots in Northern and Western Europe, has further amplified commercial demand, introducing squid to new audiences who primarily consume it outside the home. The hospitality sector benefits from economies of scale, purchasing large volumes of processed squid at lower costs than individual houtilizeholds. Furthermore, the trconclude of business lunches and social dining drives consistent weekday and weekconclude traffic, ensuring a steady throughput of squid products.

The houtilizehold segment is expected to register a CAGR 5.9% from 2026 to 2034, with a cultural shift towards home cooking, where consumers are increasingly eager to experiment with international recipes and seafood dishes previously reserved for restaurant visits. The influence of cooking reveals, social media influencers, and online recipe platforms has demystified squid preparation, encouraging families to test creating calamari, paella, and stir-fries at home. The pandemic accelerated this trconclude, establishing a habit of preparing gourmet-style meals at home that persists today. Retailers have responded by stocking a wider variety of utilizer-friconcludely squid products, such as pre-marinated packs and oven-ready trays, which lower the barrier to entest for novice cooks.

By Distribution Channel Insights

The offline distribution channel segment is a prominent share of the European squid market in 2025, with the deeply ingrained consumer preference for physically inspecting seafood before purchase to ensure freshness and quality. In many European cultures, particularly in Southern Europe, acquireing fish and squid from local markets, fishmongers, or supermarket counters is a ritual that involves assessing texture, smell, and appearance, which cannot be replicated online. According to the European Consumer Organisation, 70% of seafood acquireers express a strong preference for selecting fresh products in person, citing trust in visual inspection as a key reason. This behavior is especially pronounced for chilled and fresh squid, where slight variations in quality can significantly impact the final dish. The presence of knowledgeable staff at fish counters who can offer advice on preparation and cooking further enhances the offline shopping experience, building customer loyalty. Data from the European Retail Roundtable reveals that despite the growth of e-commerce, over 85% of fresh seafood transactions still occur in physical stores. The immediacy of obtaining products for same-day consumption also favors offline channels, as consumers often decide on meals based on what views best at the market.

The online distribution channel segment is expected to witness the rapidest CAGR of 12.4% from 2026m to 2034 with the accelerating shift towards digital grocery shopping, as consumers increasingly prioritize convenience and time-saving solutions. The ability to order fresh and frozen squid from the comfort of home and have it delivered directly to the doorstep appeals to busy urban professionals and younger demographics who value efficiency. According to the European E-Commerce Association, online grocery sales in Europe surged by 35% in 2024, with perishable goods, including seafood,d seeing the highest growth rates. Specialized online seafood retailers have emerged, offering curated selections of premium squid species that may not be available in local supermarkets, thereby attracting niche customers. The development of sophisticated cold chain logistics for last-mile delivery ensures that products arrive in optimal condition, addressing previous concerns about freshness. Data from McKinsey & Company indicates that 40% of consumers who started acquireing groceries online during recent global disruptions intconclude to continue the habit permanently. The integration of mobile apps and subscription services further simplifies the purchasing process, encouraging repeat acquires.

COUNTRY LEVEL ANALYSIS

Spain Squid Market Analysis

Spain was the largest contributor to the European squid market by occupying 28.6% of the share in 2025, with its gastronomic heritage, where squid is a ubiquitous ingredient in tapas, paellas, and grilled specialties consumed daily across the countest. According to the Spanish Ministest of Agriculture, Fisheries and Food, per capita consumption of cephalopods in Spain exceeds 4.5 kilograms annually, the highest in Europe, driving immense demand for both fresh and frozen varieties. The countest hosts a sophisticated network of processing facilities, particularly in Galicia and Andalusia, which import vast quantities of Argentine and Asian squid to clean, freeze, and package for re-export to other European nations. Data from the Spanish Association of Canned and Preserved Fish Manufacturers indicates that the sector processes over 100000 metric tons of squid annually, generating significant economic activity. The vibrant tourism industest further amplifies consumption, with millions of visitors indulging in fresh seafood dishes along the coastlines.

Italy Squid Market Analysis

Italy’s squid market growth is likely to grow with the strong tradition of seafood cuisine and a robust demand for high-quality fresh and frozen squid in both houtilizehold and commercial sectors. The market growth in this countest is propelled by the central role of squid in regional cuisines, from calamari fritti in the south to risotto al nero di seppia in the north, creating it a staple in restaurants and homes alike. According to the Italian National Institute of Statistics, seafood consumption in Italy has remained resilient, with squid accounting for a significant portion of cephalopod intake, particularly during religious festivals and summer holidays. The countest relies heavily on imports to supplement domestic catches, with major ports like Ancona and Chioggia serving as key entest points for frozen raw materials. Data from the Italian Federation of Fishmongers indicates that sales of fresh squid in local markets remain strong, reflecting a consumer preference for daily purchases of high-quality produce. The food service sector, renowned globally for its Italian seafood dishes, drives substantial bulk demand, while retail chains have expanded their frozen seafood ranges to meet altering lifestyles. The emphasis on “Made in Italy” processing, where imported squid is cleaned and packaged locally, adds value and ensures compliance with strict EU regulations. This blconclude of culinary tradition, quality consciousness, and industrial capability sustains Italy’s position as a top-tier market.

Portugal Squid Market Analysis

Portugal’s squid market growth is likely to grow with its maritime history and exceptionally high per capita seafood consumption, which places squid among the most popular protein sources. The national identity is tied to the ocean, where dishes like lulas a seixal and grilled squid are everyday comforts found in every corner of the countest. According to the Portuguese Institute for the Ocean and Atmosphere, the nation consumes more seafood per capita than any other European countest, with cephalopods representing a vital component of this diet. Local fisheries contribute significantly, but imports are essential to meet the insatiable demand, particularly for larger species utilized in traditional recipes. Data from the Portuguese Association of Fishery Industries reveals that the sector has modernized its freezing and canning capabilities by allowing for the export of high-value squid products while satisfying domestic necessarys. The cultural practice of eating fresh fish daily, supported by a dense network of local fish markets, ensures a constant turnover of product. Tourism along the Algarve and Lisbon coasts further boosts consumption, introducing international visitors to Portuguese squid delicacies.

France Squid Market Analysis

France’s squid market growth is likely to grow with the sophisticated palate that appreciates squid in gourmet preparations and a growing interest in sustainable seafood options. The integration of cephalopods into haute cuisine and regional specialties in coastal areas like Brittany and the Mediterranean coast. The French retail sector is highly developed, with supermarkets offering a wide array of fresh, chilled, and frozen squid products, often labeled with clear origin information to meet regulatory and consumer demands. Data from the French Seafood Interprofessional Committee indicates that the food service industest, including bistros and Michelin-starred restaurants, increasingly features squid in innovative dishes, driving premium demand. The trconclude towards “manger mieux” (eating better) has led to a preference for sustainably sourced squid, prompting retailers to expand their eco-certified ranges. The presence of major processing companies that specialize in ready-to-cook meals also facilitates houtilizehold consumption. The combination of culinary excellence, regulatory rigor, and evolving consumer habits ensures France remains a key and growing market for squid in Northern and Western Europe.

United Kingdom Squid Market Analysis

The United Kingdom squid market growth is likely to grow with the dynamic food service sector, a rising interest in Asian cuisines, and a growing health-conscious demographic seeking lean protein sources. The explosion of ethnic dining, particularly Japanese, Chinese, and Thai restaurants, where squid is a core ingredient in tempura, stir-fries, and curries, is also prompting the growth of the market. Additionally, the traditional fish and chip sector has begun to offer calamari rings as a popular alternative to cod and haddock, broadening its appeal. Data from Kantar Worldpanel reveals that retail sales of frozen squid rings have increased by 15% annually, driven by convenience and affordability. The health and wellness trconclude is also gaining traction, with consumers recognizing squid as a low-fat, high-protein option suitable for fitness diets. The presence of major supermarket chains promoting sustainable seafood initiatives further supports market growth.

COMPETITIVE LANDSCAPE

The competition in the European squid market is characterized by a mix of large multinational corporations and specialized regional processors who vie for dominance through supply chain reliability and product quality. The market landscape is fragmented yet consolidated at the top tier, where major global players leverage their extensive networks to offer comprehensive solutions that tinyer competitors cannot match. Intense rivalry exists primarily around securing high-quality raw materials from source countries, given the total depconcludeence on imports and the frequent volatility cautilized by climatic and geopolitical factors. Companies differentiate themselves by investing in advanced processing technologies that ensure superior purity levels and by obtaining various sustainability certifications that appeal to environmentally conscious European acquireers. The threat of new entrants remains moderate due to the high capital requirements for establishing robust logistics and quality control systems compliant with strict European Union regulations. Price competition is fierce,e particularly in the bulk commodity segment, forcing players to optimize operational efficiencies and explore value-added product lines to maintain margins. Strategic partnerships and long-term contracts with suppliers have become essential tools for managing risk and ensuring steady availability in this highly competitive environment.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global Europe Squid Market include

- Nordic Seafood Group

- Delfín Ultracongelados

- Scanfisk Seafood

- Brasmar Group

- Congalsa

- WOFCO (World Food Corporation)

- Grupo Alfrio

- FRIGONOVA Fish s.r.o.

- Nomad Foods

- Bolton Group

TOP LEADING PLAYERS IN THE MARKET

- Pescanova Group stands as a global leader in the seafood industest with a profound impact on the European squid market through its extensive sourcing and processing capabilities. The company manages a vast international supply chain that connects fishing fleets in the Atlantic and Pacific oceans directly to European consumers. Their contribution to the global market involves setting high standards for sustainability and traceability in cephalopod fisheries. Recently, the group has strengthened its position by investing in advanced freezing technologies that preserve the texture and flavor of squid during long transit times. They have also expanded their portfolio of value-added products,s such as breaded calamari and pre-marinated rings, gs to meet the growing demand for convenience in European houtilizeholds. Pescanova actively collaborates with fishery improvement projects to ensure responsible harvesting practices.

- Profand Seafood operates as a specialized powerhoutilize in the European squid sector, tor known for its expertise in processing and distributing high-quality frozen cephalopods. The company distinguishes itself by offering a wide range of squid formats, including whole cleaned tubes and rings,s tailored to specific industrial and retail requirements. Their global involvement includes strategic partnerships with fishing vessels in South America and Asia to secure consistent volumes of raw material. In recent developments, ts Profand has upgraded its production facilities in Spain to increase capacity for ready-to-cook squid products, responding to the surge in home cooking trconcludes. They have also implemented rigorous quality control systems to ensure compliance with strict European food safety regulations regarding heavy metals and additives. The company actively promotes sustainable fishing certifications to appeal to environmentally conscious acquireers.

- Nomad Foods is a prominent frozen food corporation with a significant presence in the European squid market primarily through its strong brands and extensive distribution network. The company plays a critical role in creating squid accessible to mass markets by incorporating it into popular frozen seafood ranges sold in major retail outlets. Their operations emphasize brand building and logistical efficiency, ensuring that squid products are available year-round across diverse geographic regions. Recently, Nomad Foods has strengthened its market position by launching new premium seafood lines featuring sustainably sourced squid with clear labeling on origin and fishing methods. They have also invested in marketing campaigns to educate consumers on the nutritional benefits and culinary versatility of squid. The group focutilizes on expanding its product offerings to include ethnic-inspired squid dishes that cater to evolving taste preferences.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the European squid market primarily employ vertical integration strategies to secure control over the supply chain from fishing grounds to final retail shelves. Companies invest heavily in establishing long-term contracts with international fishing fleets to ensure consistent quality and reliable volumes while reducing depconcludeency on volatile spot markets. Another major strategy involves the expansion of local processing facilities within Europe to enhance value addition through cleaning, cutting n,g,, and breading capabilities closer to the conclude consumer. Participants also focus intensely on product differentiation by launching organic, sustainably certified,d and ready-to-cook squid variants to cater to the discerning European consumer base. Strategic acquisitions of tinyer regional distributors allow large corporations to broaden their reach and improve logistics efficiency across the continent. Furthermore, key players prioritize investment in advanced traceability technologies such as blockchain to provide transparency regarding origin and safety, which is crucial for complying with strict European Union regulations. These combined approaches enable market leaders to maintain competitiveness and resilience amidst global supply chain uncertainties.

MARKET SEGMENTATION

This research report on the europe Squid Market is segmented and sub-segmented into the following categories.

By Type

- Argentine Shortfin Squid

- Jumbo Flying Squid

- European Squid (Loligo)

- Other Squid Species

By Form

- Frozen

- Chilled

- Canned/Processed

By End-User

- Commercial (Restaurants, Hotels, Foodservice)

- Houtilizehold

By Distribution Channel

- Offline (Supermarkets, Fish Markets, Specialty Stores)

- Online (E-commerce Platforms, Direct-to-Consumer)

By Countest

- Spain

- Italy

- Portugal

- France

- United Kingdom

- Germany

- Rest of Europe

Leave a Reply