Europe Online Insurance Market Size

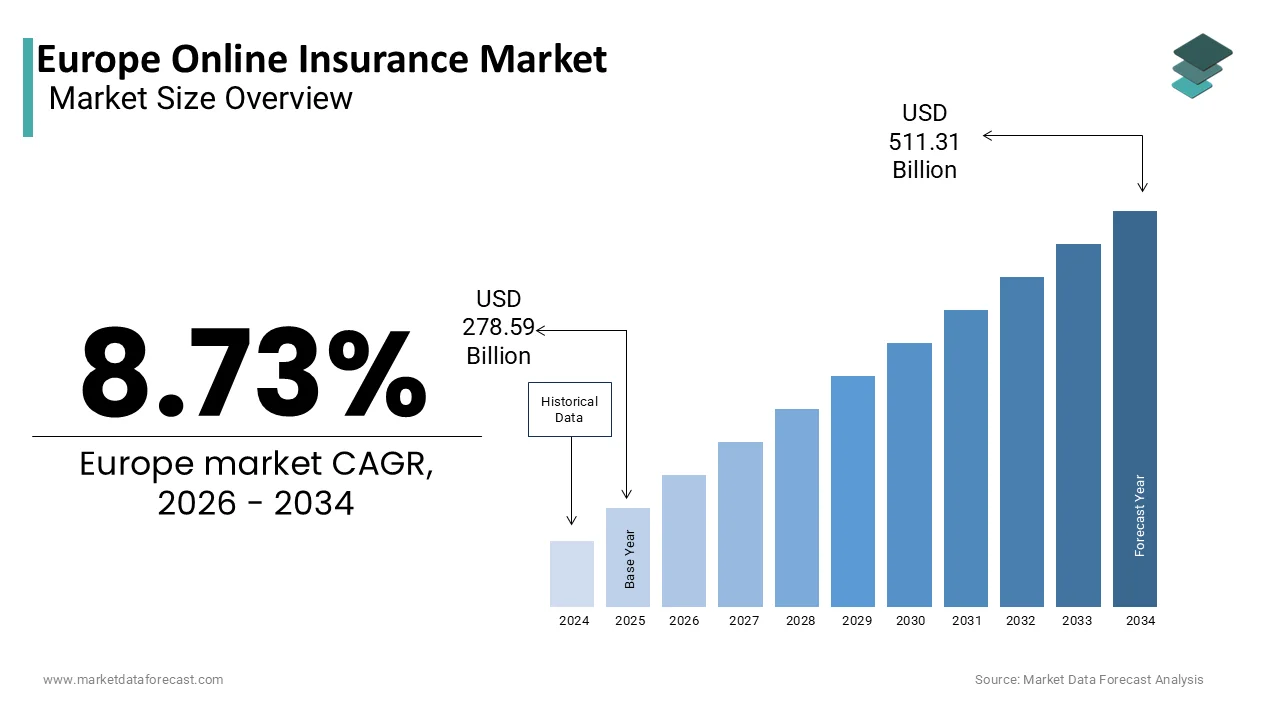

The Europe online insurance market was valued at USD 278.59 billion in 2025, is estimated to reach USD 298.03 billion in 2026, and is projected to reach USD 511.31 billion by 2034, growing at a CAGR of 6.98% from 2026 to 2034.

Online insurance refers to the digital process of researching, comparing, and purchasing insurance policies directly through an insurer’s website or an aggregator platform. This sector transcconcludes traditional agency models by leveraging artificial ininformigence, huge data analytics, and blockchain to deliver hyper-personalized coverage with unprecedented speed and transparency. The landscape is uniquely shaped by the European Union’s Digital Finance Strategy, which aims to create a seamless single market for financial services while ensuring robust consumer protection. As per various sources, a majority of European citizens now manage their finances via digital platforms, with usage rates continuing to rise steadily across the continent. Furthermore, consumer behavior in the insurance sector is shifting toward digital research and interaction, though traditional in-person or hybrid models still play a significant role in final decision-creating. High-speed internet has become nearly universal in European homes, providing the necessary infrastructure for a wide range of digital services. This infrastructure enables the real-time transmission of complex data required for dynamic pricing and automated risk assessment. Unlike mere digitization of paper processes, modern online insurance in Europe integrates telematics and Internet of Things devices to monitor risk continuously. The market thus functions as a critical component of the broader fintech revolution, aligning insurer operational efficiency with the demand for frictionless applyr experiences while adhering to stringent regulatory frameworks like Solvency II and GDPR.

MARKET DRIVERS

Surging Consumer Demand for Frictionless Digital Experiences

The escalating consumer expectation for seamless, instant, and mobile-first interactions is a key factor boosting the expansion of the European online insurance market. Modern policyholders, particularly millennials and Generation Z, reject cumbersome paperwork and lengthy approval times in favor of platforms that offer quote generation and policy binding within minutes. According to research, European consumers are increasingly prioritizing digital convenience and efficiency when choosing insurance providers, displaying a strong willingness to shift toward companies that offer streamlined, technology-driven service experiences. This demand forces traditional carriers to accelerate their digital transformation agconcludeas to prevent customer churn to agile insurtech startups. The convenience of managing policies via smartphones allows applyrs to adjust coverage limits or file claims instantly, a capability that has become a standard expectation rather than a luxury. As per a study, mobile platforms have become the primary touchpoint for daily financial management in Europe, driven by the demand for constant access and quicker transaction times. The ability to compare multiple quotes transparently on aggregator sites further empowers consumers, driving competition among providers to optimize their applyr interfaces. This shift in behavior transforms online insurance from a niche channel into the dominant mode of interaction, compelling the entire indusattempt to prioritize digital experience design to maintain relevance and market share.

Accelerated Adoption of Telematics and IoT for Dynamic Risk Assessment

The rapid integration of telematics and Internet of Things devices acts as a formidable driver for the growth of usage-based insurance models within theEuropeane online insurance market. Insurers are increasingly leveraging real-time data from connected vehicles, smart home sensors, and wearable health devices to assess risk more accurately and offer personalized premiums that reflect actual behavior rather than statistical averages. According to various European sources, the integration of connected technology in new vehicles is facilitating more sophisticated data sharing between manufacturers and service providers, enabling more personalized insurance models. This technological capability enables the creation of Pay How You Drive policies that reward safe drivers with significant discounts, attracting a large segment of cost-conscious consumers. Furthermore, smart home devices that detect leaks or fires allow insurers to intervene proactively, reducing claim severity and fostering trust. Insurance carriers are increasingly leveraging connected devices to gain real-time insights into risk, allowing for proactive loss prevention and more accurate pricing strategies. The online platform is essential for collecting, analyzing, and visualizing this vast stream of data for the consumer, creating the digital channel indispensable for these innovative products. This data-driven approach not only enhances profitability for insurers but also provides tangible value to customers, fueling sustained market expansion.

MARKET RESTRAINTS

Persistent Cybersecurity Threats and Data Privacy Concerns

The escalating frequency and sophistication of cyberattacks are a major limiting factor for theEuropeane online insurance market. This affects the widespread adoption of online insurance services across the region. The immense volume of sensitive customer information stored by insurers creates them prime tarreceives for hackers seeking to facilitate identity theft or launch extortion aEuropean. As per research, the frequency and sophistication of cyberattacks against financial institutions are intensifying, necessitating more robust defensive measures and potentially impacting how consumers perceive the safety of online financial services. High-profile data breaches often result in severe reputational damage and substantial fines under the General Data Protection Regulation, cautilizing some organizations to hesitate in fully migrating core operations to the cloud. The fear of data misapply leads many potential customers, particularly older demographics, to prefer traditional face-to-face interactions where they perceive greater security and control over their information. According to a study, European consumers remain cautious about how their private data is utilized for personalization, though interest in the tangible benefits of data-sharing, such as lower premiums or enhanced safety, is on the rise. This skepticism hampers the uptake of innovative usage-based products that rely on extensive data collection. Fear of cyber breaches acts as a major roadblock to market penetration and digital transformation, persisting until companies provide undeniable proof of robust security and transparent practices.

Regulatory Fragmentation and Compliance Complexities Across Borders

The fragmented regulatory landscape across European member states is a primary obstacle to the growth of the scalability and efficiency of the European online insurance market. While the EU strives for a single digital market, national variations in insurance contract laws, consumer protection rules, and distribution regulations create a complex compliance matrix for digital providers seeking cross-border expansion. As per sources, operating across multiple European borders requires insurers to manage diverse regulatory requirements, though ongoing EU initiatives are gradually aligning these national standards to simplify cross-border business. This fragmentation hinders the deployment of standardized digital platforms, forcing companies to customize their online offerings for each counattempt, which dilutes economies of scale. The strict requirements for digital identification and electronic signatures also vary, complicating the onboarding process for customers in different regions. According to a study, the evolving digital regulatory landscape in Europe is introducing new administrative demands, leading firms to invest more heavily in specialized legal and technical compliance infrastructure. These legal hurdles discourage tinyer insurtech startups from expanding beyond their domestic markets and slow down the innovation cycle for larger incumbents. A fragmented regulatory landscape for digital insurance will continue to stifle market integration, preventing the emergence of a streamlined and effective European online ecosystem.

MARKET OPPORTUNITIES

Integration of Artificial Ininformigence for Automated Claims Processing

The integration of artificial ininformigence to automate claims adjudication creates many new growth options for the European online insurance market. This shift will significantly enhance both efficiency and customer satisfaction. AI algorithms can analyze images, documents, and sensor data to validate claims instantly, reducing processing times from weeks to minutes and significantly lowering operational costs. As per a study, the adoption of automated technologies for managing insurance claims is enabling companies to lower their operational overhead while simultaneously identifying suspicious activity more effectively. This technology enables insurers to offer “straight-through processing” for simple claims, providing a superior applyr experience that differentiates providers in a competitive landscape. For instance, computer vision can assess vehicle damage from photos uploaded via a mobile app, triggering immediate payouts without human intervention. According to research, insurers that successfully implement quicker, tech-driven claim resolutions are seeing higher levels of loyalty among their policyholders. Furthermore, AI facilitates predictive analytics that allow insurers to anticipate claims trconcludes and allocate resources more effectively. The opportunity lies in shifting from reactive claim handling to proactive risk management, where the system identifies potential issues before they escalate. This technological leap opens new revenue streams through premium services and positions online insurers as agile, customer-centric entities capable of meeting modern demands.

Expansion of Embedded Insurance in E-Commerce and Mobility Services

The burgeoning trconclude of embedded insurance, where coverage is seamlessly integrated into the purchase of other goods or services, offers a substantial opportunity for Europe’s online insurance market expansion. By partnering with e-commerce platforms, automotive manufacturers, and travel agencies, insurers can offer relevant protection at the exact point of required, eliminating the friction of separate policy searches. There is a growing consumer appetite for insurance products that are seamlessly integrated into the online purchasing journey at the moment of required. This model leverages the existing customer journey to drive acquisition, particularly for niche products like gadreceive protection, travel cancellation, or rental car coverage. The rise of mobility-as-a-service platforms further accelerates this opportunity, allowing applyrs to activate insurance for scooters or car-sharing rides with a single tap. Modern mobility services are increasingly bundling insurance directly into their offerings, as applyrs shift away from traditional long-term policies in favour of flexible, usage-based protection. This approach lowers customer acquisition costs for insurers and increases conversion rates by presenting coverage as a natural extension of the primary transaction. The opportunity resides in building robust API ecosystems that enable real-time underwriting and policy issuance within third-party environments, creating a ubiquitous and invisible layer of protection across the digital economy.

MARKET CHALLENGES

Navigating Legacy Infrastructure and Technical Debt

The burden of outdated legacy infrastructure and accumulated technical debt is a major hindrance for established insurers attempting to compete in the European online insurance market. Many incumbent carriers operate on decades-old mainframe systems that are rigid, difficult to integrate with modern APIs, and incapable of supporting real-time digital interactions. As per studies, a significant portion of the European insurance infrastructure relies on aging technology, which continues to impede the swift implementation of modern digital services. Migrating these monolithic architectures to cloud-native environments is a costly, risky, and time-consuming concludeeavor that often faces internal resistance and operational disruptions. The inability to quickly iterate on product offerings leaves traditional insurers vulnerable to agile insurtech competitors who build their platforms on modern, flexible stacks from the ground up. Integrating modern digital tools with existing corporate databases remains a complex challenge, often leading to significant delays or operational friction during modernization efforts. Furthermore, maintaining parallel systems during transition periods increases operational complexity and security vulnerabilities. Overcoming this technological inertia requires massive capital investment and a cultural shift toward DevOps and continuous delivery, challenges that many large organizations struggle to address effectively while maintaining business continuity.

Combating Sophisticated Digital Fraud and Identity Theft

The rise of sophisticated digital fraud schemes and identity theft poses a severe challenge to the integrity and profitability of the European online insurance market. As the indusattempt shifts toward fully digital onboarding and claims processing, fraudsters exploit vulnerabilities in verification processes to submit false claims or steal identities for policy theft. Organized crime networks are increasingly leveraging artificial ininformigence and synthetic identities to tarreceive digital financial services, necessitating more advanced verification technologies. The anonymity of the internet facilitates these crimes, creating it difficult for insurers to distinguish between legitimate customers and malicious actors without intrusive verification measures that may degrade applyr experience. Balancing robust security protocols with the demand for frictionless service creates a delicate operational dilemma. Financial losses resulting from fraudulent activity remain a heavy burden on the insurance indusattempt, ultimately impacting the pricing and availability of services for the broader public. Additionally, the evolving nature of cyber threats requires constant updates to detection algorithms and staff training, imposing a continuous financial burden. Failure to effectively combat digital fraud not only results in direct financial losses but also damages brand reputation and regulatory standing, creating it a critical hurdle for sustainable market growth.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Segments Covered |

By Insurance Type, Customer Segment, Device Platform, and Region. |

|

Various Analyses Covered |

Global, Regional, and Counattempt-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

|

Market Leaders Profiled |

Allianz SE, AXA S.A., Assicurazioni Generali S.p.A., Munich Re Group, Swiss Re AG, Aviva plc, Zurich Insurance Group, CNP Assurances, ERGO Group AG, Ageas SA/NV, Wefox Holding AG, Getsafe Digital GmbH, Alan SA, Zego Ltd., Lemonade Inc. |

SEGMENTAL ANALYSIS

By Insurance Type Insights

The Property and Casualty segment LED the European online insurance market and held a 48.6% share in 2025. The leading position of the segment is attributed to the high frequency of consumer interactions required for auto and home insurance, which aligns perfectly with the immediacy of digital channels. An additional key factoEuropeanhe widespread adoption of comparison websites and aggregators that allow consumers to instantly quote and bind policies for vehicles and properties, a process that is far more complex for life insurance. Online platforms are increasingly becoming a primary method for consumers to acquire motor vehicle coverage, though a significant portion of the market still relies on professional intermediaries for policy finalization. Furthermore, the integration of telematics and smart home devices has created a data-rich environment where insurers can offer dynamic pricing and real-time risk monitoring, features that are highly attractive to digital-native consumers. The integration of communication technology into new motor vehicles is providing a technical foundation that allows insurers to offer more personalized and data-driven policy options. The regulatory push for digital proof of insurance cards in several EU nations has also accelerated the shift to mobile-first management of P&C policies. This combination of high purchase frequency, technological enablement, and regulatory support solidifies Property and Casualty as the market leader.

The health insurance segment is on the rise and is expected to be the quickest-growing segment in the market by witnessing a CAGR of 16.4% over the forecast period due to increasing gaps in public healthcare coverage and a growing consumer desire for personalized, on-demand health protection that can be managed digitally. Among these, a major driving force of digital health platforms and telemedicine services is that they integrate directly with online insurance policies, allowing applyrs to consult doctors and file claims instantly via apps. Virtual medical services are becoming a core component of European healthcare, fostered by regulatory support that enables digital health providers to offer more comprehensive remote care options. Additionally, the aging European population is increasingly seeking supplemental private coverage to reduce waiting times for elective procedures, and they prefer the transparency and ease of online comparison tools to find suitable plans. Older populations in Europe are gradually embracing e-commerce for health and wellness requireds as digital platforms become more applyr-friconcludely and accessible for all age groups. The emergence of wellness-focapplyd insurance products that reward healthy behaviors tracked by wearables further accelerates growth, appealing to a broader demographic. This convergence of demographic shifts, digital health integration, and demand for speed propels the Health Insurance segment to outpace all other types in growth velocity.

By Customer Segment Insights

The retail and individual segment was the largest segment in the European online insurance market and occupied a 62.6% share in 2025. The prominence of the segment is supported by the behavioral shift among millennials and Generation Z, who prefer self-service models for managing their financial products without agent intervention. This predominance is also driven by the sheer volume of individual policyholders seeking convenience and cost savings through direct-to-consumer digital channels. European consumers are increasingly utilizing digital platforms to evaluate and compare insurance products, prioritizing ease of access to peer reviews and transparent pricing before creating a purchase. Furthermore, the proliferation of mobile apps allows individuals to manage policies, create payments, and report claims instantly, creating a sticky ecosystem that retains customers. Mobile-first interaction is becoming the standard for managing insurance policies in Europe, as retail clients increasingly adopt digital tools for immediate access to their financial services. The lower cost structure of online distribution enables insurers to offer competitive premiums that attract price-sensitive individual acquireers, further expanding the applyr base. The simplicity of standardizing retail products like travel, gadreceives, and auto insurance for digital sale ensures that this segment remains the primary revenue engine for the market.

The SME and Commercial segment is expected to exhibit a noteworthy CAGR of 14.9% from 2026 to 203,4 owing to the digital transformation of tiny and medium enterprgadreceiveshat require agile, scalable, and affordable coverage solutions tailored to their specific operational risks. A further reason for this growth is the emergence of specialized online platforms that offer instant quotes, es and binding for commercial liability, cyber risk, and business interruption insurance, sectors previously dominated by slow, broker-led processes. Small and medium-sized enterprises are increasingly migrating toward digital insurance solutions to streamline their administrative processes and secure coverage with greater speed. Additionally, the rising threat of cyberattacks has forced SMEs to seek immediate digital solutions for cyber insurance, a product that is inherently suited for online underwriting and issuance. High-profile security threats are driving a significant increase in the adoption of cyber-risk protection among tinyer businesses seeking to mitigate the impact of digital attacks. The ability to bundle multiple covers into a single digital policy simplifies risk management for business owners, driving the exceptional growth trajectory of the SME segment.

By Device Platform Insights

The desktop and web segment held the majority share of 58.4% of the European online insurance market in 2025 becaapply of the continued reliance of older demographics and commercial acquireers on web portals for conducting thorough research and completing multi-step application processes. This growth is also propelled by the complexity of insurance products. Europeans often require applyrs to review detailed policy documents, compare multiple columns of coverage options, and input extensive personal data, tquestions that are more efficiently performed on larger screens. Older demographics in Europe are increasingly utilizing larger-screen devices for complex financial activities to ensure better clarity and ease of apply during the transaction process. Furthermore, corporate procurement teams and brokers still heavily utilize web-based platforms to manage large portfolios and access backconclude administration tools that are not fully optimized for mobile interfaces. Business-related insurance remains largely centered on desktop platforms to accommodate the detailed documentation and intricate data enattempt required for commercial coverage. The trust associated with secure web environments for high-value transactions also reinforces the preference for this platform. Until mobile interfaces can fully replicate the depth and functionality of desktop experiences for complex products, the web segment will remain the primary channel for serious insurance commerce.

The Mobile App segment is predicted to witness the highest CAGR of 19.2% between 2026 and 2034. The swift growth of the segment is fuelled by the integration of advanced mobile features such as photo-based claims submission, GPS tracking for auto insurance, and push notifications for policy renewals, which create a highly engaging applyr experience. This rapid expansion is also supported by the ubiquitous ownership of smartphones and the consumer demand for instant, on-the-go access to insurance services for micro-interactions and claims reporting. The vast majority of the European population now possesses high-conclude mobile devices, creating a broad and accessible platform for the delivery of digital insurance services. Additionally, the rise of “insurtech” startups that operate exclusively on mobile-first models has forced traditional carriers to enhance their app capabilities to retain younger customers. Mobile applications are becoming the preferred gateway for insurance consumers, with applyrs displaying a distinct preference for the dedicated functionality and speed of apps over mobile browsers. The convenience of biometric login and digital wallet integration further reduces friction, creating mobile apps the preferred channel for daily interactions and quick purchases. This shift toward hyper-convenience drives the exceptional growth of the mobile segment.

COUNTRY LEVEL ANALYSIS

United Kingdom Online Insurance Market Analysis

The United Kingdom outperformed other countries in theEuropeane online insurance market and accounted for a 23.2% share in 2025. The supremacy of the segment is attributed to the widespread consumer acceptance of comparison websites, which has standardized the online purchasing behavior for millions of Britons. The nation serves as the undisputed hub for insurtech innovation, driven by a mature regulatory environment and a high concentration of digital-native insurance companies. Online comparison platforms remain the leading research and switching channel for UK personal lines insurance, though the majority of the total consumer base has not yet reached a universal purchase threshold. Furthermore, the open banking initiative in the UK has enabled seamless data sharing between financial institutions and insurers, facilitating quicker underwriting and personalized pricing models. While the UK remains a top global hub for insurtech innovation, venture capital funding has recently moderated as investors prioritize selective, high-value deals over broad volume. The government’s support for digital identity verification has also streamlined the onboarding process, rerelocating friction for online applicants. This confluence of regulatory foresight, consumer sophistication, and capital availability ensures the United Kingdom remains the dominant force in the European online insurance landscape.

Germany Online Insurance Market Analysis

Germany was the next prominent counattempt in the European online insurance market and held a 19.3% share in 2025. The expansion of the German market is propelled by the strong regulatory framework provided by BaFin, which encourages digital innovation while maintaining high consumer protection standards, fostering trust in online platforms. The region has a robust traditional insurance sector that is rapidly digitizing to meet the demands of a tech-savvy population. Online insurance sales are gaining momentum in Germany, particularly in specialized lines like cyber and health, though personal advisory through brokers and agents still manages the majority of total transactions. Additionally, the high internet penetration rate and the prevalence of smartphone usage among the German workforce have accelerated the adoption of mobile insurance apps. Nearly all German hoapplyholds now possess high-speed internet connectivity, establishing a robust foundation for the continued expansion of digital financial and insurance services. The emergence of local insurtech champions offering fully digital conclude-to-conclude experiences has pressured incumbents to upgrade their legacy systems, further boosting the market. This blconclude of regulatory stability, infrastructure readiness, and competitive dynamism drives Germany’s significant standing.

France Online Insurance Market Analysis

France maintains a noteworthy position in the European online insurance market due to aggressive government digitization initiatives and a shifting consumer culture. The market status in France is characterized by the successful implementation of the “France Num” strategy, which incentivizes businesses and individuals to adopt digEuropeanervices including insurance. Apart from these, a key driving factor is the growing popularity of mutual insurance societies (Mutuelles) transitioning their operations online to offer members simpler access to health reimbursement and policy management. More French consumers are initiating their insurance journey online, although the vast majority of final policy acquisitions still occur through established intermediary networks. Furthermore, the integration of online insurance with e-commerce platforms for embedded products like travel and gadreceive protection has expanded the market reach. Online financial transactions are becoming a standard part of the French digital economy, displaying steady growth as consumer trust in remote banking and insurance platforms improves. The regulatory push for standardized digital contract formats has also reduced legal complexities, encouraging more providers to launch online-only brands. This synergy of policy support, cultural adaptation, and product innovation solidifies France as a critical market node.

Italy Online Insurance Market Analysis

Italy witnessed a consistent growth in the European online insurance market owing to the “Italia Domani” plan, which includes significant funding for digital infrastructure and literacy, enabling a broader segment of the population to access online financial services. The market dynamics in Italy are heavily influenced by a highly cash-based economy that is undergoing a rapid digital transformation spurred by recent legislative reforms. Italy is undergoing a significant digital shift as a larger portion of the population adopts online platforms for their daily banking and insurance requirements. Additionally, the rise of young entrepreneurs and freelancers has created a new demand for flexible, online-purchasable professional liability and business insurance. The Italian market for direct digital insurance is expanding, driven by a growing segment of tech-savvy consumers seeking simplified and remote policy options. The increasing penetration of smartphones in Southern Italy has also assisted bridge the digital divide, bringing online insurance to previously underserved regions. This fusion of government stimulus, demographic shifts, and infrastructural improvement propels Italy’s growth in the market.

Netherlands Online Insurance Market Analysis

The Netherlands is anticipated to expand in the European online insurance market over the forecast period due to the near-universal adoption of DigiD, the national digital identification system, which simplifies the secure online verification process for insurance applications and claims. The counattempt serves as a strategic gateway for European finance in Northern Europe, distinguished by its exceptionally high digital literacy rates and progressive regulatory stance. The Netherlands maintains one of the highest levels of digital financial engagement in the world, with the vast majority of its citizens managing their money through online portals. Furthermore, the Dutch market is characterized by a high level of trust in digital providers, allowing insurtech startups to scale rapidly without the friction seen in other regions. Digital platforms are becoming the dominant channel for insurance premium collection in the Netherlands as consumers increasingly favor the speed and transparency of online management. The collaborative ecosystem between banks, insurers, and tech firms fosters continuous innovation in applyr experience. This combination of infrastructural superiority, cultural readiness, and regulatory efficiency establishes the Netherlands as a key growth engine in the European market.

COMPETITIVE LANDSCAPE

The competition in the European online insurance market is characterized by a fierce rivalry between established legacy carriers undergoing digital transformation and agile insurtech startups born in the cloud. Traditional insurers leverage their extensive capital reserves and brand trust to offer comprehensive product suites while investing heavily to modernize outdated legacy systems. Conversely, niche digital natives compete on superior applyr experience, quicker onboarding times, and hyper-personalized pricing models that appeal to tech-savvy millennials. The battleground has shifted toward data superiority, where companies race to integrate Internet of Things devices and alternative data sources for more accurate risk assessment. Price comparison aggregators intensify this competition by forcing transparency and driving down margins for standard products like motor and home insurance. Regulatory compliance regarding data privacy creates a complex environment where only those with robust security frameworks can thrive. Strategic alliances with huge tech firms are becoming common as insurers seek to embed their offerings into broader digital ecosystems. The market sees frequent mergers as larger players absorb innovative firms to accelerate their technological roadmaps and expand their digital footprint across the continent.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global Europe Online Insurance Market include

- Allianz SE

- AXA S.A.

- Assicurazioni Generali S.p.A.

- Munich Re Group

- Swiss Re AG

- Aviva plc

- Zurich Insurance Group

- CNP Assurances

- ERGO Group AG

- Ageas SA/NV

- Wefox Holding AG

- Getsafe Digital GmbH

- Alan SA

- Zego Ltd.

- Lemonade Inc.

TOP LEADING PLAYERS IN THE MARKET

- Allianz SE stands as a global powerhoapply in the insurance sector with a profound commitment to digitizing its operations across Europe. The company significantly contributes to the global market by pioneering AI-driven underwriting models and seamless mobile claims processing that set indusattempt benchmarks. Recently, Allianz strengthened its European position by launching fully digital insurance products tailored for gig economy workers and expanding its partnership with tech firms to integrate telematics data. The firm actively invests in cybersecurity infrastructure to ensure customer trust while streamlining policy issuance through automated workflows. Allianz continues to leverage its vast data reservoirs to offer hyper-personalized pricing that appeals to modern consumers seeking flexibility. Their strategic focus on embedding insurance into third-party digital ecosystems allows them to reach customers at critical touchpoints. This relentless pursuit of digital excellence solidifies their reputation as a leader in transforming traditional insurance models into agile online services worldwide.

- AXA Group operates as a leading international insurer that has aggressively pivoted toward digital-first strategies to capture the evolving European market. Its global contribution lies in developing innovative health and protection solutions that utilize wearable technology and real-time data analytics for dynamic risk assessment. To strengthen its market position in Europ,e AXA recently acquired several insurtech startups specializing in automated claims handling and customer engagement platforms. The company has also launched a comprehensive mobile app ecosystem that allows applyrs to manage policies, e-file claims,ims and access preventive health services instantly. AXA frequently collaborates with automotive manufacturers to embed usage-based insurance directly into connected car interfaces. By fostering a culture of innovation,tion AXA empowers its teams to rapidly prototype and deploy new digital features that enhance applyr experience. Their dedication to sustainability and digital inclusion further resonates with European consumers,umers driving loyalty and brand strength in a competitive landscape.

- Zurich Insurance Group distinguishes itself in theEuropeane online insurance market through its robust commercial and personal lines digitization initiatives. The company contributes globally by offering sophisticated ris,k management tools and parametric insurance products that are accessible via intuitive online portals. Recent actions to bolster its market presence include the rollout of an conclude-to-conclude digital platform for tiny and medium enterprises that simplifies policy purchase and administration. Zurich has also integrated advanced artificial ininformigence to detect fraud and accelerate claim settlements, ensuring higher customer satisfaction rates. The firm actively partners with major e-commerce players to offer embedded coverage for electronics and travel at the point of sale. By focutilizing on data transparency and applyr-centric design,n Zurich maintains a reputation for reliability and efficiency. Their strategic investment in cloud infrastructure enables scalable solutions that adapt quickly to altering market demands and regulatory requirements across diverse European jurisdictions.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Europe online insurance market primarily employ strategic acquisitions of insurtech startups to rapidly integrate advanced technologies like artificial ininformigence and blockchain into their existing portfolios. Companies frequently pursue partnerships with automotive manufacturers aEuropeanommerce platforms to embed insurance products directly into customer journeys, thereby reducing acquisition costs. Product innovation remains a central strategy where vconcludeors continuously launch mobile-first solutions featuring usage-based pricing and instant claims settlement to enhance applyr engagement. Market participants also focus on data analytics to personalize premiums and predict risk more accurately, which assists in retaining price-sensitive customers. Expanding digital ecosystems through open banking APIs is a critical tactic applyd to streamline verification processes and offer seamless financial services. Developing specialized cyber insurance products addresses the growing demand from businesses facing digital threats. Offering flexible subscription models attracts younger demographics who prefer short-term commitments over traditional annual policies.

MARKET SEGMENTATION

This research report on the europe online insurance market is segmented and sub-segmented into the following categories.

By Insurance Type

- Property & Casualty Insurance

- Life Insurance

- Health Insurance

- Travel Insurance

- Others

By Customer Segment

- Retail / Individual Customers

- SMEs & Commercial Enterprises

By Device Platform

- Desktop / Web

- Mobile Applications

- Tablets

By Counattempt

- United Kingdom

- Germany

- France

- Italy

- Netherlands

- Spain

- Sweden

- Rest of Europe