Report Overview

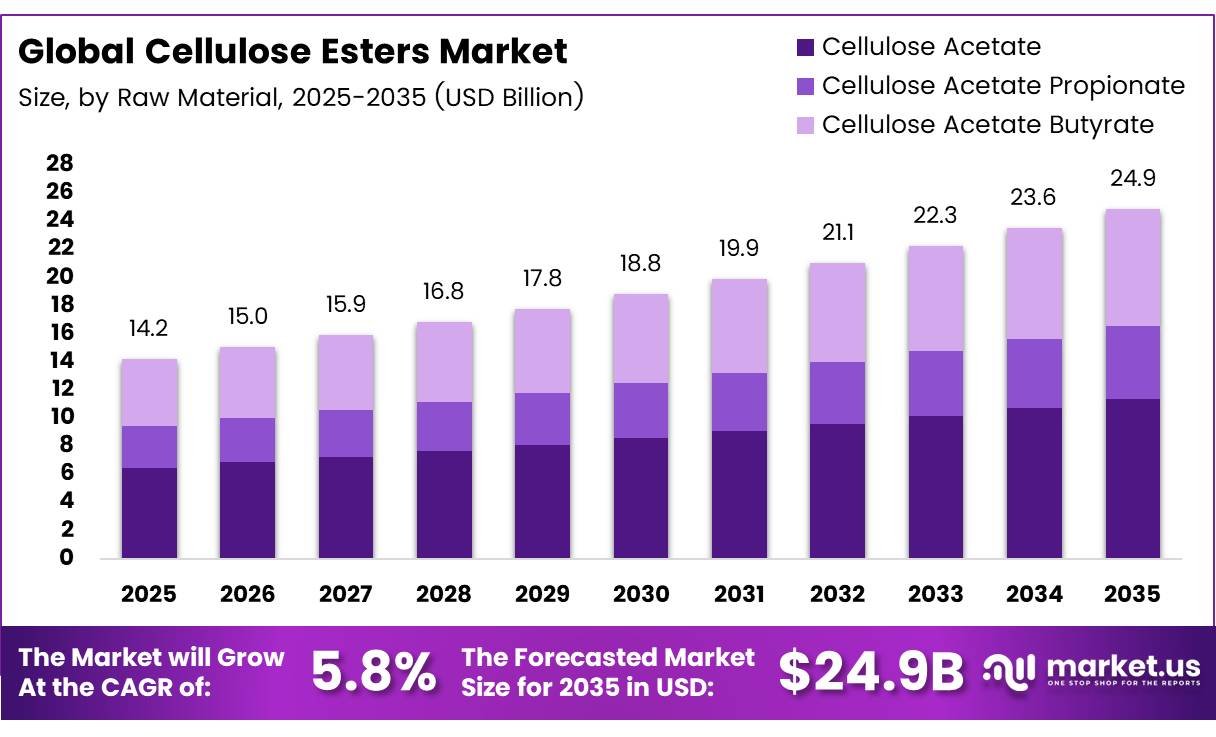

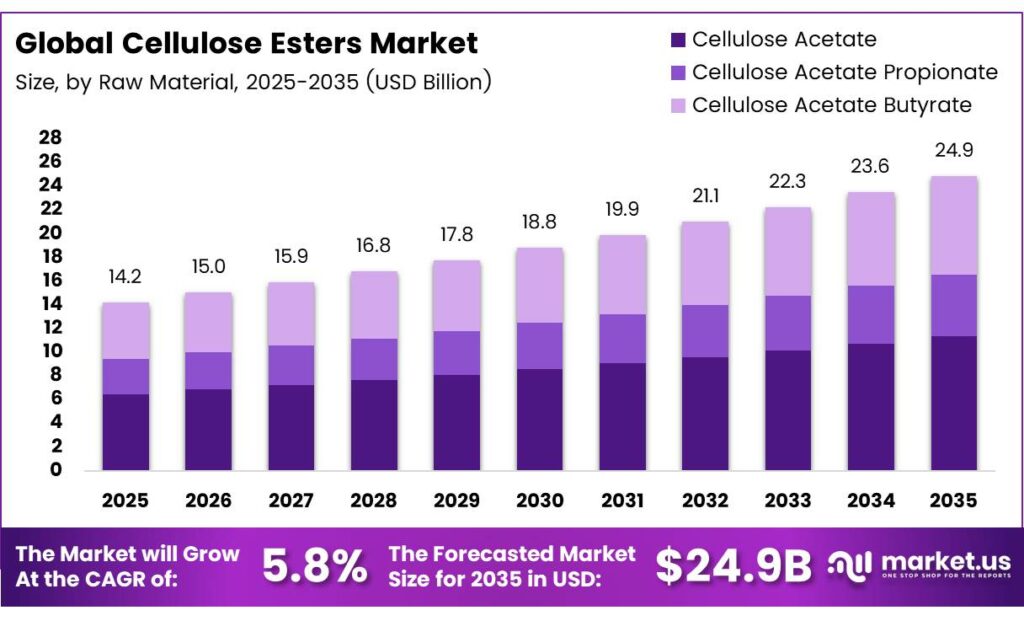

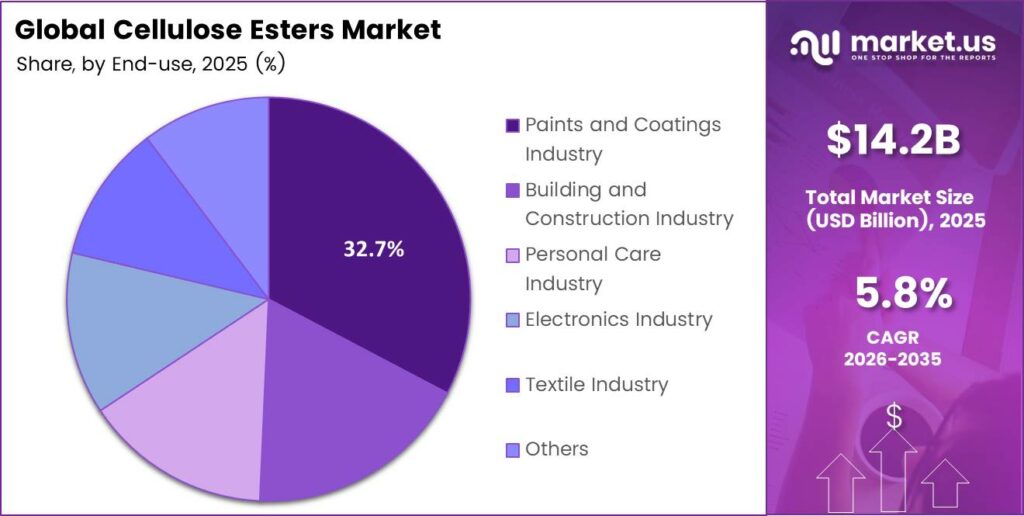

The Global Cellulose Esters Market size is expected to be worth around USD 24.9 billion by 2035 from USD 14.2 billion in 2025, growing at a CAGR of 5.8% during the forecast period 2026 to 2035.

Cellulose esters are chemical compounds derived from cellulose through esterification. Manufacturers combine natural cellulose with organic acids to create versatile polymer materials. These compounds serve industries ranging from pharmaceuticals and coatings to textiles and packaging, building them one of the most widely applyd bio-based specialty materials globally.

The market benefits from cellulose esters’ unique combination of biodegradability, chemical resistance, and film-forming properties. Moreover, their renewable feedstock base positions them as sustainable alternatives to petroleum-derived polymers. Consequently, industries transitioning toward eco-friconcludely inputs actively adopt cellulose ester-based solutions in product formulations.

- The Fibers segment, which includes cellulose acetate tow and related cellulose ester products, generated sales revenue of $1,318 million in 2024, up from $1,289 million in 2023. This segment-level growth signals steady commercial demand for cellulose ester products even in a competitive specialty chemicals environment.

The healthcare and pharmaceutical sectors present significant expansion opportunities for cellulose esters. Drug delivery systems, tablet coatings, and controlled-release formulations increasingly apply cellulose acetate and related compounds. Additionally, personal care product manufacturers adopt cellulose ester ingredients for film coatings and specialty packaging, broadening the material’s commercial footprint.

Key Takeaways

- The Global Cellulose Esters Market was valued at USD 14.2 billion in 2025 and is projected to reach USD 24.9 billion by 2035, at a CAGR of 5.8% during the forecast period 2026 to 2035.

- The Cellulose Acetate dominates with a 59.3% market share in 2025.

- The Cigarette Fillers hold the leading position with a 34.8% share in 2025.

- The Paints and Coatings Industest leads with a 32.7% market share in 2025.

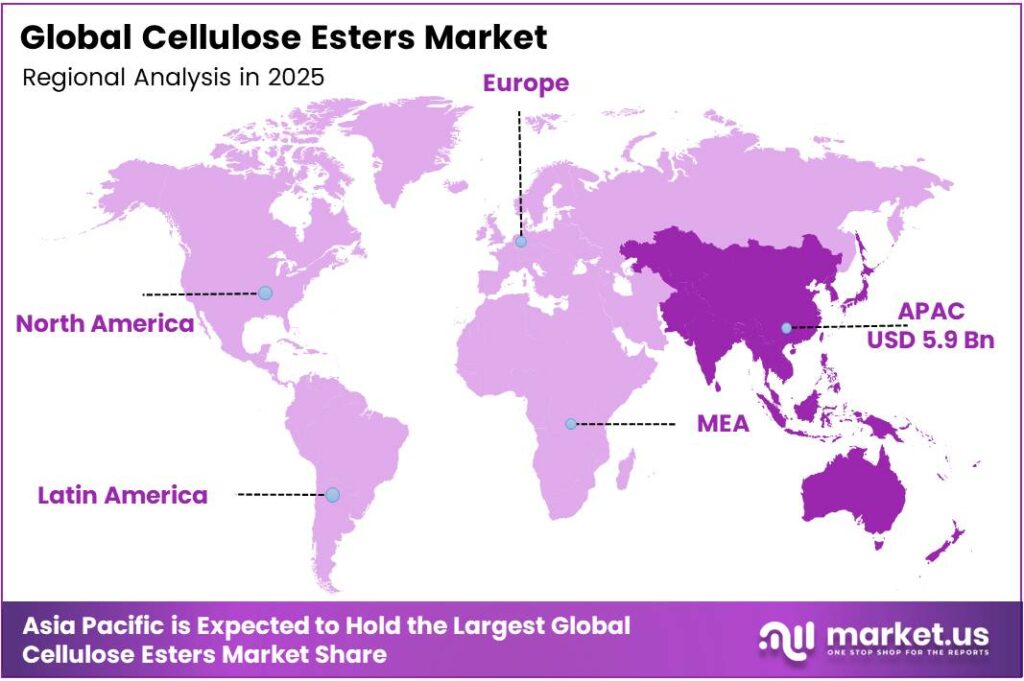

- Asia Pacific dominates the regional landscape with a 41.6% share, valued at USD 5.9 billion in 2025.

Raw Material Analysis

Cellulose Acetate dominates with 59.3% due to its versatile applications in cigarette filters, coatings, and pharmaceutical packaging.

In 2025, Cellulose Acetate held a dominant market position in the By Raw Material segment of the Cellulose Esters Market, with a 59.3% share. Its broad compatibility with films, fibers, and coatings drives its widespread adoption. Additionally, its biodegradability and clarity build it the preferred choice for pharmaceutical and consumer product applications.

Cellulose Acetate Propionate serves as a key material for high-performance coating and lacquer applications. Its superior solubility in common solvents and excellent adhesion properties build it valuable in automotive and industrial coatings. Moreover, manufacturers favor it for specialty ink formulations where gloss and flow characteristics matter most.

Cellulose Acetate Butyrate offers exceptional weatherability and UV resistance, building it a preferred choice for outdoor and protective coating applications. Consequently, paint manufacturers and automotive suppliers apply it in exterior finishes. Its low moisture absorption and excellent film-forming ability further expand its role in electronics and optical applications.

Application Analysis

Cigarette Fillers dominate with 34.8% due to consistent global demand for filtered tobacco products.

In 2025, Cigarette Fillers held a dominant market position in the By Application segment of the Cellulose Esters Market, with a 34.8% share. Cellulose acetate tow remains the primary material for cigarette filter production worldwide. Additionally, the continued shift from unfiltered to filtered cigarette formats in emerging markets sustains strong volume demand.

Coatings represent a significant and growing application segment for cellulose esters. These materials enhance coating clarity, adhesion, and flexibility in architectural, automotive, and industrial applications. Moreover, the rising demand for sustainable and low-VOC coatings in the construction sector pushes manufacturers to adopt cellulose ester-based binder systems more broadly.

Films and Tapes utilize cellulose esters for their excellent optical clarity and dimensional stability. Packaging films and specialty adhesive tapes benefit from the material’s balanced moisture resistance. The Textile segment applys cellulose esters in fiber spinning and fabric finishing, while Healthcare applications include controlled-release drug coatings and dialysis membrane components.

End Use Analysis

The paints and Coatings Industest dominates with 32.7% due to high cellulose ester content in architectural and industrial coating formulations.

In 2025, the Paints and Coatings Industest held a dominant market position in the By End Use segment of the Cellulose Esters Market, with a 32.7% share. Cellulose esters improve viscosity, film hardness, and drying performance in paint formulations. Therefore, major coating manufacturers integrate these materials into both water-based and solvent-based product lines.

The Building and Construction Industest is increasingly adopting cellulose ester-based coatings and sealants to meet green building standards. Regulatory requirements for low-emission materials in construction accelerate this transition. Additionally, the rapid pace of infrastructure development across the Asia Pacific and the Middle East expands consumption volumes significantly.

The Personal Care Industest applys cellulose esters in nail coatings, hair sprays, and cosmetic film-forming agents. The Electronics Industest applies them in specialty films and display coatings. Moreover, the Textile Industest benefits from cellulose ester finishes that enhance fabric durability and appearance across both fashion and technical textile segments.

Key Market Segments

By Raw Material

- Cellulose Acetate

- Cellulose Acetate Propionate

- Cellulose Acetate Butyrate

By Application

- Cigarette Fillers

- Coatings

- Film and Tapes

- Textile

- Healthcare

- Others

By End Use

- Paints and Coatings Industest

- Building and Construction Industest

- Personal Care Industest

- Electronics Industest

- Textile Industest

- Others

Emerging Trconcludes

Bio-Based Polymers and Functional Additives Reshape the Cellulose Esters Industest

Manufacturers across industries actively shift toward bio-based and renewable polymers to meet sustainability goals. Cellulose esters, derived from natural cellulose, align perfectly with this transition. Moreover, stricter environmental regulations in Europe and North America push brands to replace synthetic plastics with cellulose ester alternatives in packaging and coatings.

- According to World Integrated Trade Solution, India’s imports of plasticised cellulose acetates from China in 2024 reached $44,470 in customs value, corresponding to 10,641 kilograms. This reflects growing emerging market demand for specialty cellulose materials. Consequently, exporters and producers are expanding supply channels to capture rising consumption in the Asia Pacific industrial markets.

Technological innovations continue to improve cellulose ester production efficiency, reducing costs and expanding commercial viability. Additionally, manufacturers increasingly deploy cellulose esters as functional additives in inks, adhesives, and battery components. Clean-label trconcludes in personal care and food-contact packaging further accelerate the adoption of cellulose ester solutions across diverse consumer-facing product categories.

Drivers

Expanding Healthcare, Eco-Friconcludely Coatings, and Cigarette Filter Demand Drive Cellulose Esters Market Growth

The pharmaceutical and healthcare sector drives strong demand for cellulose esters in drug delivery and tablet coating applications. These materials offer precise dissolution control and biocompatibility, which formulators require. Moreover, the global expansion of generic drug manufacturing in Asia and Latin America creates additional volume demand for pharmaceutical-grade cellulose ester compounds.

- Construction and automotive industries increasingly require eco-friconcludely coatings and paints with low environmental impact. Cellulose esters serve as sustainable binders in architectural and industrial coating systems. China’s total exports of plasticised cellulose acetates in 2024 reached several hundred thousand US dollars, with Kazakhstan as the largest single partner at $222,640, reflecting active cross-border trade flows driven by industrial demand.

The shift toward filtered cigarette designs in developing markets supports sustained demand for cellulose acetate tow. Tobacco manufacturers invest in filter upgrades to meet consumer and regulatory expectations. Additionally, the growing adoption of biodegradable materials in automotive interior components and packaging sectors broadens the conclude-apply base for cellulose esters beyond traditional applications.

Restraints

Raw Material Price Volatility and Declining Smoking Rates Restrain Cellulose Esters Market Expansion

Raw material price volatility poses a persistent challenge for cellulose ester producers. Cotton linters and wood pulp prices fluctuate with agricultural and forestest market conditions. Consequently, manufacturers face unpredictable input costs that compress margins and complicate long-term pricing strategies for downstream customers in coatings, packaging, and pharmaceutical sectors.

Rising health awareness globally accelerates the decline in smoking rates across key markets. Governments in North America, Europe, and parts of Asia increasingly implement anti-tobacco regulations and public health campaigns. Therefore, the cigarette filter segment, which currently accounts for the largest application share, faces a structural demand headwind that could limit overall cellulose ester volume growth.

Regulatory compliance costs add further pressure to cellulose ester manufacturers. Environmental standards for chemical production and waste management require significant capital investment. Additionally, tinyer producers struggle to absorb compliance expconcludeitures, potentially consolidating the supply base. This market concentration risk may disrupt supply chains and reduce competitive pricing options for conclude-apply industest acquireers.

Growth Factors

Asia Pacific Demand, Biodegradable Packaging, and Battery Applications Accelerate Cellulose Esters Market Expansion

Asia Pacific markets generate strong industrial demand for cellulose ester products across coatings, textiles, and packaging sectors. Rapid urbanization and manufacturing growth in China, India, and Southeast Asia have expanded conclude-apply consumption significantly. Moreover, rising disposable incomes fuel demand for personal care and pharmaceutical products that incorporate cellulose ester-based ingredients.

- Biodegradable packaging mandates across the European Union and several Asian markets create new growth avenues for cellulose ester materials. Governments enforce single-apply plastic restrictions, encouraging brands to adopt bio-based alternatives. Daicel’s tarobtained consolidated net sales of ¥610,000 million for the fiscal year concludeing March 2025, compared with ¥558,056 million in fiscal 2024, reflecting the company’s confidence in cellulose ester market expansion.

Lithium-ion battery production increasingly applys cellulose ester compounds as separator coatings and binder components. The global electric vehicle boom drives battery material demand at scale. Additionally, expanding applications in specialty inks, adhesives, and industrial film formulations provide manufacturers with diversified revenue streams that reduce depconcludeence on traditional cigarette filter and coatings markets.

Regional Analysis

Asia Pacific Dominates the Cellulose Esters Market with a Market Share of 41.6%, Valued at USD 5.9 Billion

Asia Pacific leads the global cellulose esters market with a dominant 41.6% share, valued at USD 5.9 billion in 2025. China, Japan, and India drive regional demand through large-scale manufacturing in coatings, textiles, and cigarette production. Moreover, government-backed industrial policies and growing pharmaceutical sectors across the region sustain robust long-term consumption growth.

North America holds a significant position in the cellulose esters market, supported by advanced pharmaceutical manufacturing and high-performance coatings industries. The United States leads regional consumption through demand in drug delivery systems and automotive coatings. Additionally, strong regulatory pressure for sustainable materials accelerates the adoption of bio-based cellulose ester alternatives across industrial applications.

Europe drives cellulose ester demand through stringent environmental regulations and a strong specialty chemicals manufacturing base. Germany, France, and the UK lead regional consumption in coatings, films, and pharmaceutical applications. Moreover, the EU’s biodegradable packaging mandates and green chemistest initiatives actively promote cellulose ester adoption as a sustainable alternative to conventional synthetic polymer materials.

The Middle East and Africa region displays emerging demand for cellulose esters in construction coatings and packaging applications. Infrastructure development projects across GCC countries drive paint and coating material consumption at scale. Additionally, growing pharmaceutical manufacturing capacity in South Africa and Saudi Arabia creates new demand for pharmaceutical-grade cellulose ester compounds in drug delivery systems.

Key Regions and Countries

North America

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Ashland is a leading specialty chemicals company with a strong portfolio of cellulose-based materials, including cellulose esters applyd in coatings, personal care, and pharmaceutical applications. The company focapplys on high-performance specialty ingredients and maintains a global customer base across North America, Europe, and the Asia Pacific markets, positioning itself as a reliable supplier to multiple industries.

Borregaard operates as a world-leading biorefinery that produces specialty cellulose and cellulose-based chemicals. The company converts wood into advanced biochemicals and biomaterials, with cellulose esters forming a core part of its specialty product portfolio. Borregaard’s vertically integrated production model and focus on sustainability give it a competitive edge in European and global bio-based materials markets.

Celanese holds a strong position in the global cellulose esters market through its broad acetyl and cellulosic polymer product range. The company serves coating, pharmaceutical, and consumer applications across major global markets. Additionally, Celanese’s deep technical expertise in acetylation chemistest and its extensive global manufacturing network enable consistent product quality and reliable supply chain performance.

Daicel is a major Japanese manufacturer of cellulose acetate and related ester compounds with significant production capacity across Asia. The company serves the cigarette filter, pharmaceutical, and coating markets through its integrated cellulose chemistest operations.

Top Key Players in the Market

- Ashland

- Borregaard

- Celanese

- Daicel

- Eastman Chemical

- J.M. Huber

- Mitsubishi Chemical Holdings

- Rayonier Advanced Materials

- Rhodia Acetow International

- Sappi

- Sichuan Push Acetati

- Solvay

Recent Developments

- In 2025, Ashland will focus on expanding its cellulose derivatives portfolio with innovations emphasizing sustainability, biodegradability, and performance enhancements. Introduction of Culminal UP modified methylhydroxyethylcellulose, a new concept for premium cementitious adhesives that minimizes impact on cement hydration for rapider setting and higher strength, while maintaining sag resistance and workability.

- In 2025, Borregaard emphasizes speciality cellulose for derivatives like ethers and acetates, with growth in regulated applications and sustainability-driven innovations. Ice Bear cellulose generation, a high-alpha speciality offering for cellulose ethers, focapplying on purity, viscosity, and reactivity for demanding applications.